Gate Institutional Weekly Report: BTC Volatility Rises, LST Sector Declines Across the Board

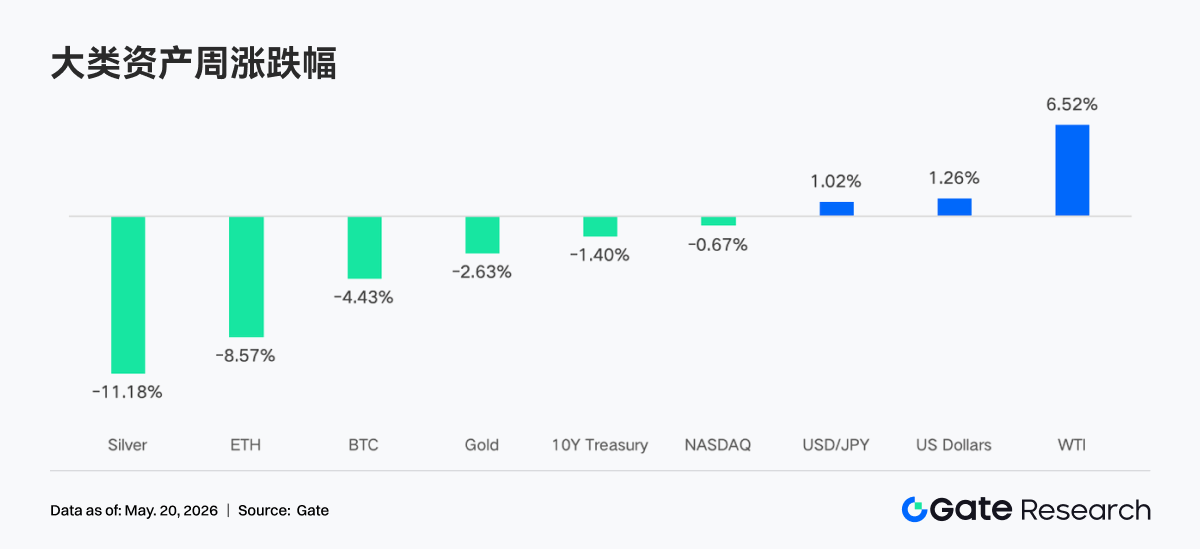

- Core View: Last week, driven by stronger-than-expected US CPI data, a lack of breakthroughs in US-China talks, and escalating tensions in the Strait of Hormuz, market risk appetite reversed sharply. This led to a sell-off in US stocks, with BTC and ETH ETFs recording net outflows of approximately $996 million and $255 million, respectively. The derivatives market entered a deleveraging phase, with BTC funding rates turning negative and demand for protective options increasing, as the market reassesses the path of macroeconomic policy.

- Key Factors:

- Sharp Deterioration in Macro Environment: US CPI rose 3.8% year-over-year in April, exceeding expectations. The 10-year Treasury yield climbed to 4.58%. Combined with geopolitical risks in the Middle East, risk assets came under pressure.

- ETF Capital Outflows: BTC ETFs saw net outflows of approximately $996 million for the week, while ETH ETFs had net outflows of about $255 million. Institutional capital shifted towards defensive allocations, although overall AUM remains at historically high levels.

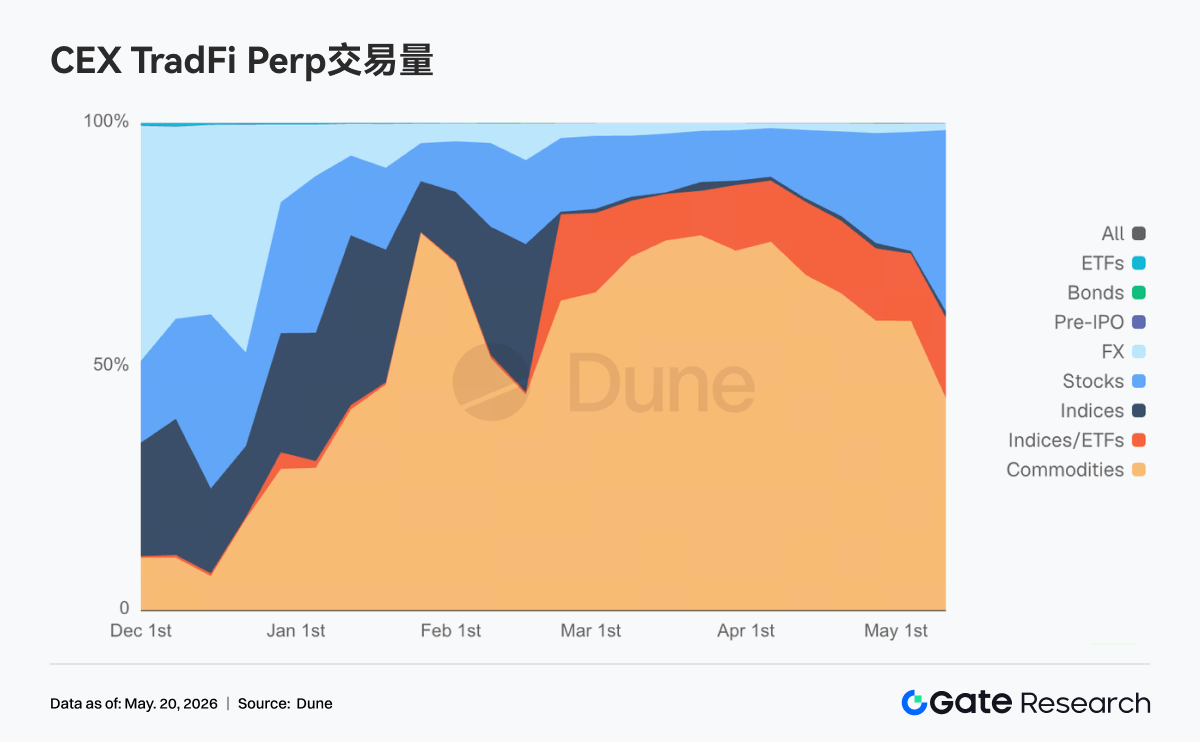

- Traditional Finance Dominance: Trading in TradFi on-chain and CEX derivatives remained dominated by safe-haven assets like gold. The share of equity-based trading rebounded to around 30% following increased volatility in US stocks.

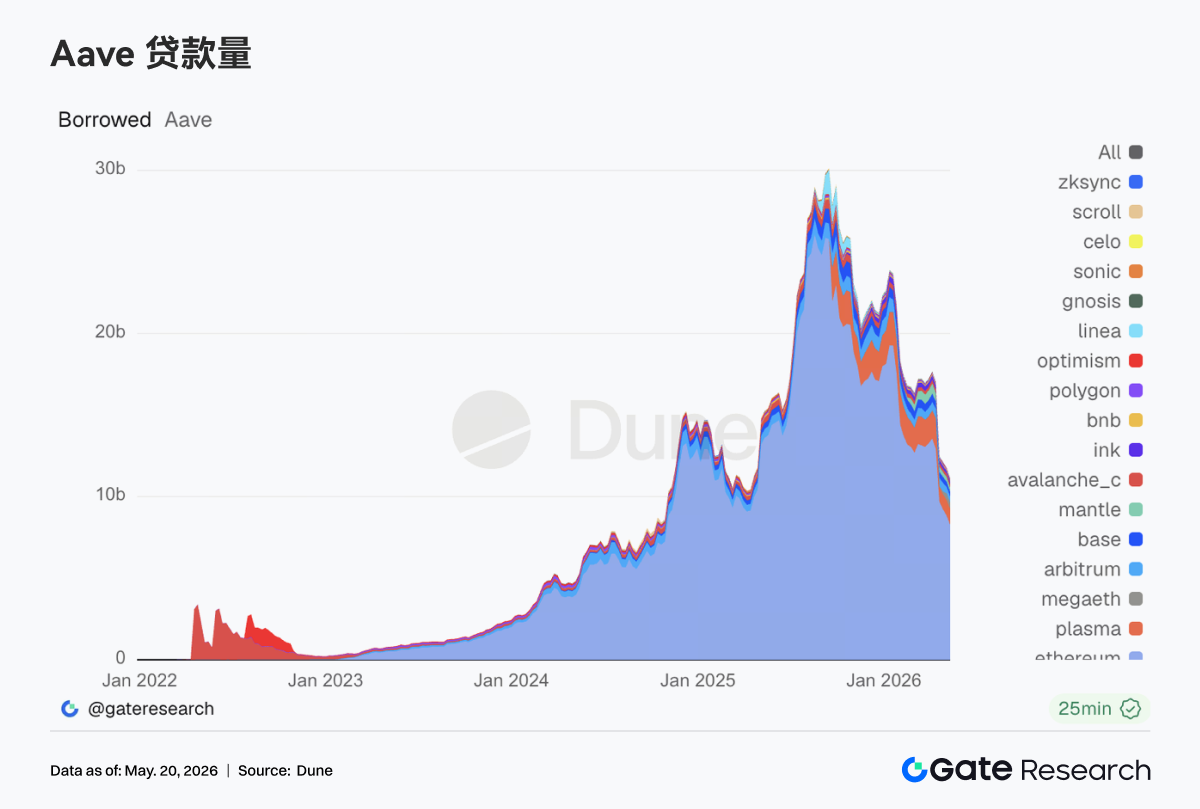

- On-Chain Lending Deleveraging: Lending on Aave's mainnet contracted for the second consecutive week. The TVL of the LST sector on the ETH side declined by about 10%, with capital migrating to new chains like Plasma.

- Derivatives Pricing Risk: BTC funding rates turned from positive to negative, with open interest falling to around $25.5B. The 25-delta skew across tenors remained deeply negative. The DVOL volatility index rose above 41, indicating increased pricing for downside risk.

- Gate Institution's Counter-Cyclical Growth: Institutional spot market share grew by 10% month-over-month. Fully collateralized margin lending volume increased by 10%, and core trading system latency was optimized by 91%.

Summary

• The market landscape experienced a sharp reversal last week. A higher-than-expected US April CPI, a lack of substantial breakthroughs in US-China talks, and renewed escalation in the Strait of Hormuz collectively pushed US Treasury yields higher and triggered a risk asset pullback. The S&P 500 and Dow Jones, after hitting new all-time highs, saw a significant retreat on Friday, prompting the market to reassess the Fed's policy path under the Walsh era.

• BTC ETFs saw net outflows of approximately $996 million for the week, while ETH ETFs recorded net outflows of about $255 million, both markedly weaker than the previous week, indicating a phase shift towards defensive positioning by institutional capital. However, the overall AUM for both BTC and ETH ETFs remains near historical highs.

• TradFi on-chain and CEX derivatives trading continued to be dominated by safe-haven assets like gold. The higher-than-expected US CPI and geopolitical risks drove increased volume in gold-linked perpetual swaps. Meanwhile, the share of trading related to equities and tech stocks rebounded, highlighting a stronger macro-driven characteristic.

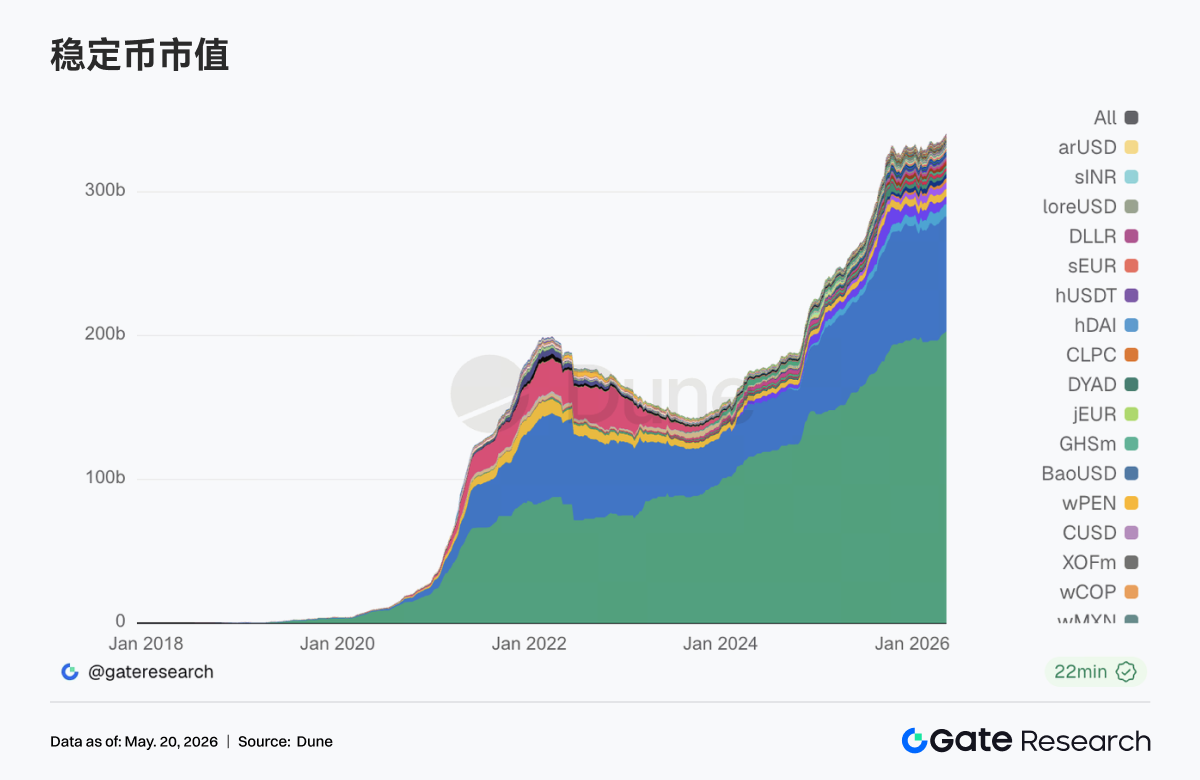

• On-chain liquidity continued to concentrate in top DEXs like PancakeSwap and Raydium. Volume on deep liquidity and stablecoin swap protocols contracted notably. The stablecoin market favored dollar-denominated assets with stronger compliance, payment, and banking channel attributes.

• Lending on the Aave mainnet and the LST sector saw a pullback, with leveraged demand on ETH and Solana sides cooling simultaneously. Concurrently, new chains like Plasma and MegaETH continued to attract structural capital migration.

• The derivatives market entered a deleveraging phase. BTC funding rates turned negative, OI continued to decline, the share of Put volume and the negative 25D Skew widened, and the DVOL center of gravity oscillated higher, indicating a clear uptick in market pricing of downside risk and volatility.

• Gate's institutional spot market share bucked the trend, growing 10% month-over-month. Cross-margin lending scale increased by 10% week-over-week. The Spot SBE upgrade is expected to go live in June. Order placement and cancellation latency on CrossEx's key exchange was reduced from 16.6ms to 1.5ms, an improvement of 91%.

1. Market Focus

Over the past week, the market environment reversed sharply. Stronger-than-expected inflation data and heightened policy uncertainty challenged the rally in risk assets. US stocks hit record highs on Thursday, with the S&P 500 closing above 7,500 for the first time and the Dow Jones returning to the 50,000 mark. However, they pulled back significantly on Friday as the market reassessed the inflation and policy outlook. Firstly, the April CPI data released on Tuesday was stronger than expected, with headline inflation rising 3.8% year-over-year, above the consensus estimate of 3.7%, and 0.6% month-over-month. Secondly, the bilateral US-China talks on Wednesday and Thursday failed to yield substantial policy breakthroughs. Thirdly, geopolitical tensions escalated again on Friday with renewed military conflict in the Strait of Hormuz, raising concerns about a potential deterioration of the de-escalation process.

Interest rate markets reacted strongly. With federal funds futures prices adjusting significantly amid expectations of tighter policy, the 10-year US Treasury yield rose 28 basis points for the week to 4.58%, its highest level since September 2025. The USD/JPY pair continued to climb on a stronger dollar. The market lowered expectations for easing and began to price in the possibility of further tightening. The Powell era officially ended last Friday, as Jerome Powell's term as Fed Chair concluded on May 15, and Kevin Walsh was sworn in as his successor over the weekend. Walsh will preside over the FOMC meeting on June 16-17, which will include updated Summary of Economic Projections and a revised dot plot, offering the market its first formal look at the policy outlook under Walsh's leadership.

2. Liquidity Analysis

2.1 BTC ETF Scale Continues to Fluctuate

Last week, the BTC ETF market exhibited clear capital outflows. The week started with a net inflow of approximately $27.2 million on May 11, but market sentiment quickly deteriorated. May 12 and May 13 saw large net outflows of roughly $233.2 million and $630.4 million, respectively, indicating a concentrated withdrawal of institutional capital from risk assets. Overall, cumulative net outflows from Bitcoin ETFs last week totaled approximately $995.5 million, nearing the $1 billion mark. Compared to the net inflow of about $623 million in the prior week (May 4 to May 8), market risk appetite reversed significantly, with institutional investors generally leaning towards profit-taking and phase-wise risk aversion.

The ETH ETF market also came under pressure. Over the past week, ETH ETFs recorded net outflows for several consecutive trading days, with weekly cumulative net outflows of approximately $255.2 million, a stark contrast to the previous week's net inflow of about $70.49 million. This indicates that, against the backdrop of macroeconomic uncertainty and heightened market volatility, ETH assets were also affected by capital reduction, with overall sentiment weaker than previously anticipated.

• Overall AUM: As of May 14, cumulative net inflows into BTC ETFs stood at approximately $58.63 billion, with Assets Under Management (AUM) of about $107.75 billion. Cumulative net inflows for ETH ETFs totaled approximately $11.9 billion, with an AUM of about $13.45 billion. Despite short-term fluctuations in capital flows, the overall scale of ETFs remains near historical highs, suggesting no fundamental reversal in institutional allocation demand.

• Institutional Moves: Capital differentiation was evident last week. In the BTC ETF space, BlackRock's IBIT saw net outflows of about $317.1 million for the week, while Morgan Stanley's MSBT bucked the trend with net inflows of roughly $39.1 million, reflecting that some institutions are still undertaking structural portfolio adjustments and allocations at lower levels. For ETH ETFs, BlackRock's ETHB saw minor net inflows, while ETHA experienced relatively large outflows, indicating market divergence in liquidity, fee structures, and long-term allocation value across different products.

2.2 TradFi Liquidity

• TradFi Perp DEX: Over the past week, the trading structure of TradFi assets on Perp DEXs continued its pattern of "commodities leading, indices supporting, equities recovering." Looking at trading volume shares, commodities remained the absolute core, maintaining an overall weekly share roughly between 45% and 65%. Although slightly down from the peak period in March-April, they remain the primary source of liquidity for on-chain TradFi derivatives trading. Gold-linked assets continued to be the core trading focus, reflecting the market's persistent preference for safe-haven assets and macro trading themes amidst recurring inflation, rising geopolitical risks, and fluctuating USD interest rate expectations. Meanwhile, the share of equity-class assets rebounded notably over the week, climbing from below 10% back to near 30%, suggesting that with renewed expansion in US stock market volatility, on-chain users' demand for trading tech stocks, US stock indices, and AI-related concepts has picked up. The current on-chain TradFi Perp user base remains predominantly crypto-native traders with a high volatility and high leverage preference, rather than a full-scale migration of traditional macro capital.

• TradFi Perp CEX: Last week, overall trading activity in the CEX TradFi perpetual swap market remained high, but the structure exhibited a clear characteristic of "precious metals leading, equities supporting, other sectors inactive." Analyzing the daily trading volume distribution of TradFi Perps, Metals assets like gold maintained an absolute core position, with daily volumes on most trading days ranging between $300 million and $700 million, occasionally exceeding $1 billion during periods of high volatility. There was a phase in mid-to-late March with a peak exceeding $1.5 billion. While last week's overall volumes were lower than those earlier extremes, they remained significantly higher than early February levels, indicating robust safe-haven and macro trading demand. In terms of rhythm, volumes notably expanded again in the second week of May, especially against the backdrop of a stronger-than-expected US CPI, escalating geopolitical risks in the Middle East, and fluctuating USD interest rate expectations, making gold-linked perpetual swaps the primary trading direction for capital. Concurrently, equity-class asset trading volumes also rebounded, reflecting short-term trading demand driven by volatility in US stock indices and tech stocks. Overall, the current CEX TradFi Perp market is gradually shifting from purely crypto beta trading towards a stronger macro-driven and cross-asset allocation logic.

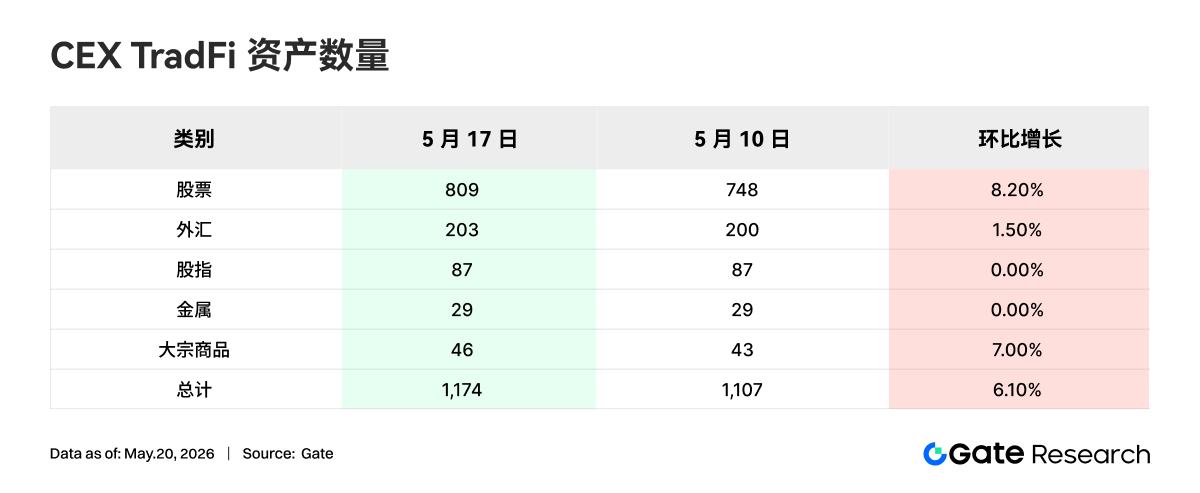

• Number of CEX TradFi Assets: The number of TradFi asset categories on CEXs expanded further over the past week. The total number of TradFi assets (only counting TradFi and CFD sectors, excluding perpetual swaps) on three major CEXs increased from 1,107 to 1,174, a sequential increase of 6.10%. Equities showed the most significant growth, rising from 748 to 809, a sequential increase of 8.20%. Among the three CEXs, Gate exhibited the highest growth rate, with its equity-class TradFi assets increasing by 62, or 16.71%.

• TradFi Order Book Depth: We selected XAUT, the highest-volume TradFi asset, to analyze its order book depth (Delta). Last week, XAUT order book liquidity exhibited a clear "inflow of safe-haven capital followed by weakening" characteristic. Between May 6 and May 12, XAUT's price consolidated at highs around $4,700, accompanied by multiple large positive Delta inflows. Around May 12, there was a net liquidity influx of nearly $2.8 million, indicating short-term capital concentration into gold-related assets for safe-haven positioning, triggered by the higher-than-expected US CPI and escalating Middle East geopolitical risks. However, the market structure reversed sharply after May 13, with the order book showing consecutive large negative Deltas, with single outflows exceeding $2 million. XAUT's price concurrently broke below $4,650 and subsequently fell to the $4,520 - $4,550 range, reflecting profit-taking by earlier safe-haven capital. Notably, between May 15 and May 17, although the price continued to weaken, the order book accumulated medium-scale positive Deltas consecutively, suggesting some capital began attempting to buy the dip, and the market was not in a state of one-sided liquidity evacuation. Overall, XAUT seems to be in a "post-safe-haven sentiment cooling, high-level rebalancing" phase. Short-term movements will remain highly dependent on macro variables such as Fed rate cut expectations, the US interest rate path, and developments in the Strait of Hormuz situation.

3. On-Chain Data Insights

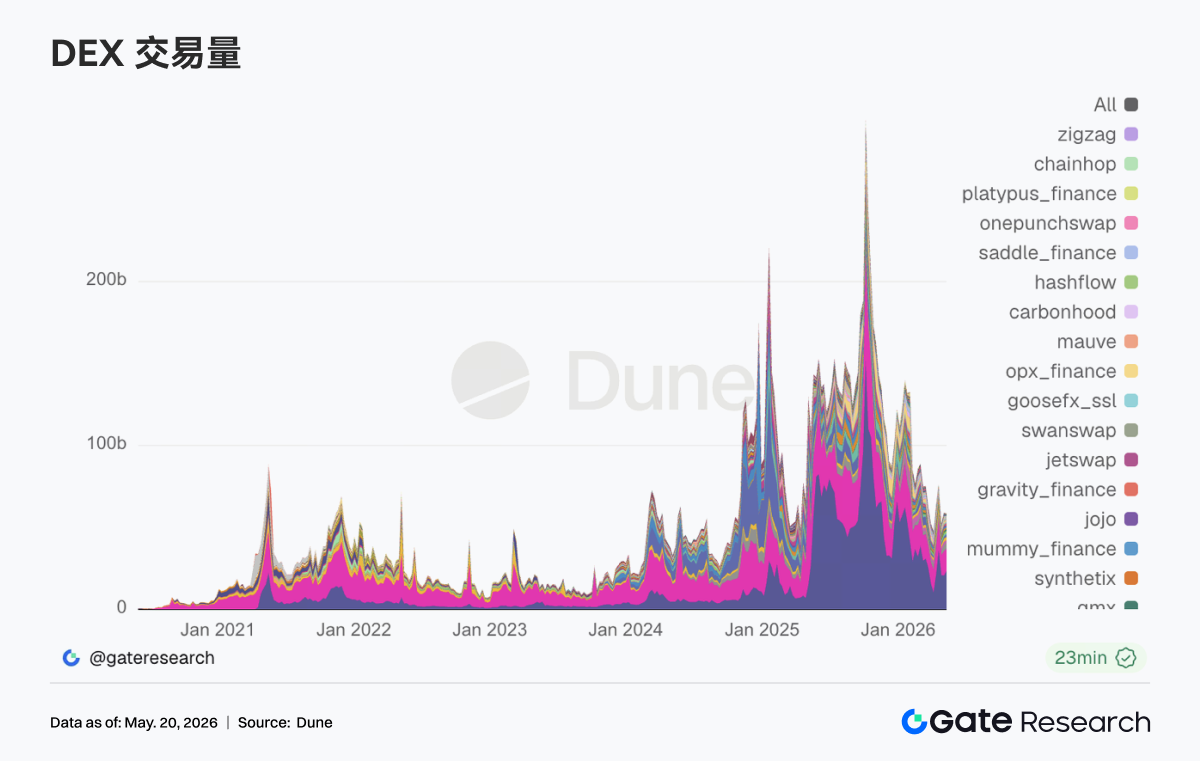

3.1 Leading DEX Volume Concentrated on PancakeSwap, but Vertical Protocol Divergence Intensifies

PancakeSwap rose approximately 12% compared to last week, with BNB chain spot collateral traffic serving as the main battlefield for both institutions and retail. Uniswap fell about 7% week-over-week. Aerodrome on Base grew roughly +3% sequentially. Activity on the Solana side remained, with the structure leaning towards high transaction counts and medium dollar volumes. Raydium saw an increase of about $1.26 billion compared to last week, while Meteora was essentially flat. High on-chain transaction counts indicate that Meme and routing-type trades haven't completely died down. Deeper liquidity and stablecoin swap-focused vertical DEX protocols like Fluid and Curve saw significant volume contraction this week.

3.2 Compliant and Payment Stablecoins Relatively Outperform, Synthetic Dollar Variants Show Increased Volatility

With USDT and USDC dominating, second-tier stablecoins such as PYUSD, RLUSD, EURC, and USDG, which are closer to payment, custodial compliance, and banking channels, outperformed older on-chain dollar stablecoins like DAI in terms of stock growth. USDe expanded notably this week, reflecting demand for yield-bearing and synthetic dollars for arbitrage and staking in volatile markets, particularly across networks. Furthermore, following the enactment of the GENIUS Act, institutional capital expenditure on stablecoin infrastructure has accelerated notably. Institutions like Bitwise have publicly stated that GENIUS reduces regulatory uncertainty for stablecoins and tokenization projects, suggesting subsequent market structure legislation like the Clarity Act will be key growth variables.

3.3 LST Sector Pulls Back Across the Board, Solana-based Assets Decline More Deeply

On the ETH side, LST protocols like Lido, Rocket Pool, and StakeWise recorded TVL pullbacks ranging from mid-to-high single digits to approximately 10%, reflecting the beta downside as staking tokens shrink in tandem with ETH. On the Solana side, high-beta LSTs like jupSOL and Sanctum saw even deeper declines, as capital prioritized cutting high-volatility staking exposure when risk appetite fell. Overall, LSTs remain a slow-moving tool for long-term ETH/SOL allocation, but the past week was not a sector-wide deleveraging event; leading Ethereum LSTs, supported by scale and liquidity, showed slightly smaller retracements compared to smaller-cap LSTs.

3.4 Aave Mainnet Lending Continues to Contract, Plasma / MegaETH Attracts Structural Migration

The Ethereum main market remains the absolute core but has contracted for a second consecutive week, indicating that institutions and whales remain conservative in the mainnet collateral market following the rsETH-related risk event in April. Concurrently, older L2s like Arbitrum and Ink also weakened. Relative bright spots were in Plasma and MegaETH. Capital continues to migrate towards new chain incentives and closed-loop collateral scenarios. This aligns with Aave's risk team's recent direction of raising caps on new assets, shifting the growth engine from mainnet leverage expansion towards more regulated, clear stablecoins and new chain closed loops.

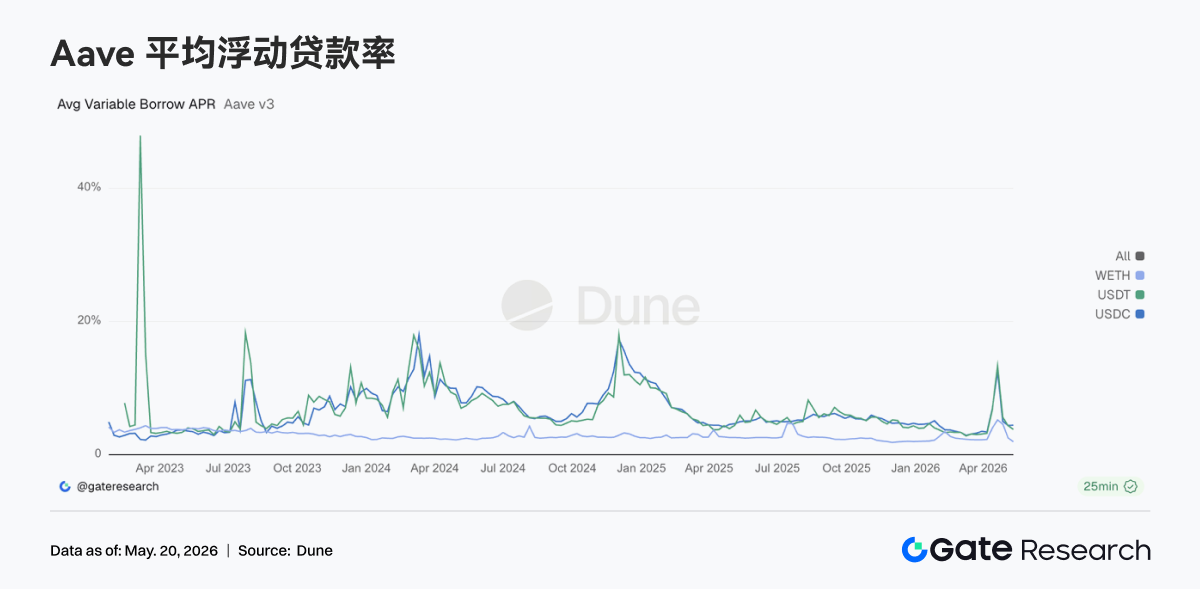

3.5 Aave Core Borrowing Rates Return to Normal, WETH Leverage Ebb is Most Pronounced

Stablecoin borrowing costs returned to the mid-single digits, reflecting eased liquidity stress and the subsiding of liquidation waves. WETH saw the largest decline, confirming that the rapid decrease in ETH leveraged demand and the decline in mainnet lending stock are mutually reinforcing. Market behavior shifted from competing for liquidity and defending positions to selectively borrowing stablecoins. The stablecoin side still sees support from structural arbitrage, cross-border dollar demand, and new chain incentive mining; the ETH side is undergoing active deleveraging. This also explains why protocol layers are more willing to raise caps for compliant stablecoins and new chain dollars rather than simply stimulating WETH loop lending.

3.6 Stablecoin Issuance is the Bedrock, Hyperliquid Expands Event Contract Trading

Tether and Circle contribute the most stable cash flow, consistent with the dominant role of existing dollar coins. Circle is strengthening vertical integration across issuer, settlement chain, and agent payments via Arc financing and Agent Stack. Hyperliquid's revenue declined slightly sequentially but remains in the top tier of on-chain derivatives in absolute terms, while continuing to expand product lines like Bitcoin outcome markets. The market continues to pay for a comprehensive financial stack combining perpetuals + prediction/outcome markets + validator/reserve narratives. Aave's revenue this week notably declined compared to last week, coinciding with the contraction in lending stock and normalization of interest rates – i.e., risk premiums fell, but active borrowers also decreased.

4. Derivatives Tracking

4.1 BTC Funding Rate Turns Negative, OI Decline Indicates Rising Deleveraging Pressure

Between May 11 and May 17, 2026, BTC price followed a pattern of rallying then retreating. Prices held around 81K early in the week, with funding rates in modestly positive territory from May 11 to May 13, suggesting lingering short-term bullish sentiment. However, prices failed to break higher, weakening rapidly after May 14 and falling back to around 77K by May 17, shifting the market from high-level consolidation to a pullback.

Regarding OI, it showed a downward trend overall this week. OI hovered around 26.8B on May 11, briefly rose above 27B on May 14, but then declined quickly, settling near 25.5B by the weekend. The combined decline in price and OI suggests this downturn is more associated with the liquidation of leveraged positions rather than a massive build-up of new short positions.

The funding rate structure also underwent a notable shift. The rate was slightly