Eight-Year Industry Retrospective: Crypto Ultimately Chose Another, More Valuable Path

- Core Thesis: After eight years of development, the crypto industry has failed to realize the initial vision of decentralization disrupting traditional finance. However, through the waves of stablecoins and tokenization, it is progressively integrating with mainstream finance, building a new internet-native financial infrastructure whose practical value far exceeds initial expectations.

- Key Elements:

- Having weathered the ICO bubble, DeFi Summer, the NFT craze, and the systemic collapse of 2022 (e.g., the implosions of Terra and FTX), the industry has continuously rebuilt itself through speculative cycles, with its focus shifting towards financial infrastructure.

- Stablecoins (such as USDC and USDT) have become the core use case, with their current supply exceeding $300 billion and a projected settlement volume of $100 trillion in 2025. By being pegged to U.S. Treasuries, they align with America's national strategic interests.

- After the chaotic proliferation of Memecoins, Trump's election victory has fostered a more regulation-friendly environment. The passage of the GENIUS Act provides clear rules for stablecoins, prompting Wall Street to explore asset tokenization, as evidenced by BlackRock's CEO expressing support.

- The convergence of Artificial Intelligence and crypto technology will see AI agents utilizing stablecoins and wallets for autonomous transactions, paving the way for the emergence of independent commercial entities and accelerating the industry's mainstream adoption and the replacement of backend infrastructure.

Original author: Connor Dempsey

Original translation: Chopper, Foresight News

On Monday, I will start a new job. Before embarking on my fifth career chapter, I want to write this article to reflect on my eight-year journey in the crypto industry.

When I entered the crypto industry in 2017, I believed this technology would change everything.

Government fiat currencies would be replaced by decentralized tokens; blockchains would eliminate all intermediary giants collecting rents in transaction chains; power would shift back from large corporations to ordinary users.

Looking back now, almost none of those original visions have materialized, but the industry has carved out a completely different path.

Over eight years working at four crypto companies, I've witnessed the industry's market cap grow from less than $1 billion to over $4 trillion, weathered several speculative bubbles, and experienced one systemic collapse. I've gradually come to realize that what the industry is actually building is far more valuable than I initially imagined.

Before starting my next role, I want to document what I've seen and heard, and where I predict the industry is headed.

The Illusory Wealth Frenzy: The 2017–2018 ICO Mania

In early 2017, I stumbled upon Bitcoin in a book and was completely hooked. Soon after, I devoured every Bitcoin book I could find and harbored the idea of moving to Singapore to write a blog and dive deep into this new technology.

At the time, I didn't realize I was at the tail end of the ICO (Initial Coin Offering) super-speculative bubble. ICOs allowed anyone to raise funds globally by selling cryptocurrencies to investors to crowdfund creative projects.

And Ethereum was the star of this carnival.

In November 2017, I published a beginner-friendly guide to Ethereum that went viral on Reddit. It coincided perfectly with the peak of the bubble, which burst just one month later.

Reading that article again now, it feels like a time capsule: capturing the era's widespread optimism while also prophesying a future that never came true.

My main argument was that blockchain networks like Ethereum could be used to build new consumer applications.

Traditional internet platforms (Facebook, Uber, etc.) saw most value captured by giant corporations and a few investors. In contrast, value generated by blockchain applications would be shared among early participants and ICO investors.

The article also envisioned building a decentralized Uber. In this system, early users and drivers would receive tokens for each completed ride, thereby owning a stake in the network, leading to a fairer distribution of value to early builders.

The vision looked good on paper, but this decentralized revolution ultimately failed completely.

It was purely a crypto speculative feast reminiscent of the 2001 dot-com bubble.

Ethereum became the most powerful fundraising platform in history, with over 3,000 ICO projects globally raising a total of $22 billion.

But just like the dot-com bubble, the underlying technology wasn't mature enough to justify the sky-high valuations the market gave it.

More fatally, ICOs completely distorted the incentive structure between entrepreneurs and investors. Project teams could raise tens of millions of dollars overnight with just an idea; investors only held tokens, hoping the project would materialize and appreciate. Founding teams, holding large amounts of native tokens, could cash out immediately upon listing, losing all motivation to build a solid product.

During bull markets, founders and early investors made fortunes; during bear markets, ordinary retail investors were left holding the bag. Despite some well-intentioned builders, ICOs ultimately became a breeding ground for greed, hype, and scams.

Throughout hundreds of years of financial history, every speculative bubble has looked exactly like this.

Rebuilding from the Ruins: The 2018–2019 Circle Incubation Phase

As the market soured, leveraging the small reputation I built on Reddit, I joined Circle in early 2018 for an entry-level marketing role.

At that time, Circle was four years old. Its multiple consumer-facing products (investing, payments, exchange) were unprofitable, but its over-the-counter (OTC) trading desk was quietly and consistently generating revenue, supporting the entire company.

Over the next two years, the industry was mired in the post-ICO bust depression. The vast majority of ICO projects were abandoned and defunct, countless tokens went to zero, and industry sentiment hit rock bottom.

But this dark age also sowed the seeds for the next renaissance in crypto.

The industry's focus shifted away from consumer applications towards rebuilding the traditional financial system on the internet.

Dollar-pegged stablecoins, initially created to facilitate traders easily moving in and out of crypto positions, maintained their $1 peg through 1:1 reserves of US dollars and Treasury bills.

Tether's USDT rose rapidly during the ICO boom, storing most of its dollar reserves in bank accounts outside the US. Initially used mainly for trading, stablecoins soon benefited another group: people who couldn't access the traditional banking system but wanted to hold dollar-denominated assets.

For example, citizens trying to circumvent capital controls, wealthy Chinese seeking to diversify assets overseas, and people in Argentina and Turkey suffering from inflation.

In 2018, Circle partnered with Coinbase to launch the regulated US dollar stablecoin USDC. Its early uses were still primarily trading, but people began envisioning this internet-native currency allowing anyone with an internet connection to access US dollars 24/7 without barriers.

Meanwhile, the surviving quality projects from the ICO era were largely focused on finance. Ethereum wasn't just for fundraising; it could also rebuild the underlying infrastructure of financial markets: Uniswap in trading, Aave and Compound in lending, forming the decentralized finance (DeFi) ecosystem.

Stablecoins and DeFi became deeply integrated, and a once-in-a-century global pandemic would propel them to their peak.

Return to the Wild West of the Internet: The 2019–2021 Messari Era

In late 2019, I joined Messari, a data research startup with just 13 people, as their first full-time marketing hire.

The company had only 4 analysts, delving into cutting-edge DeFi research when the total DeFi market cap was just $665 million.

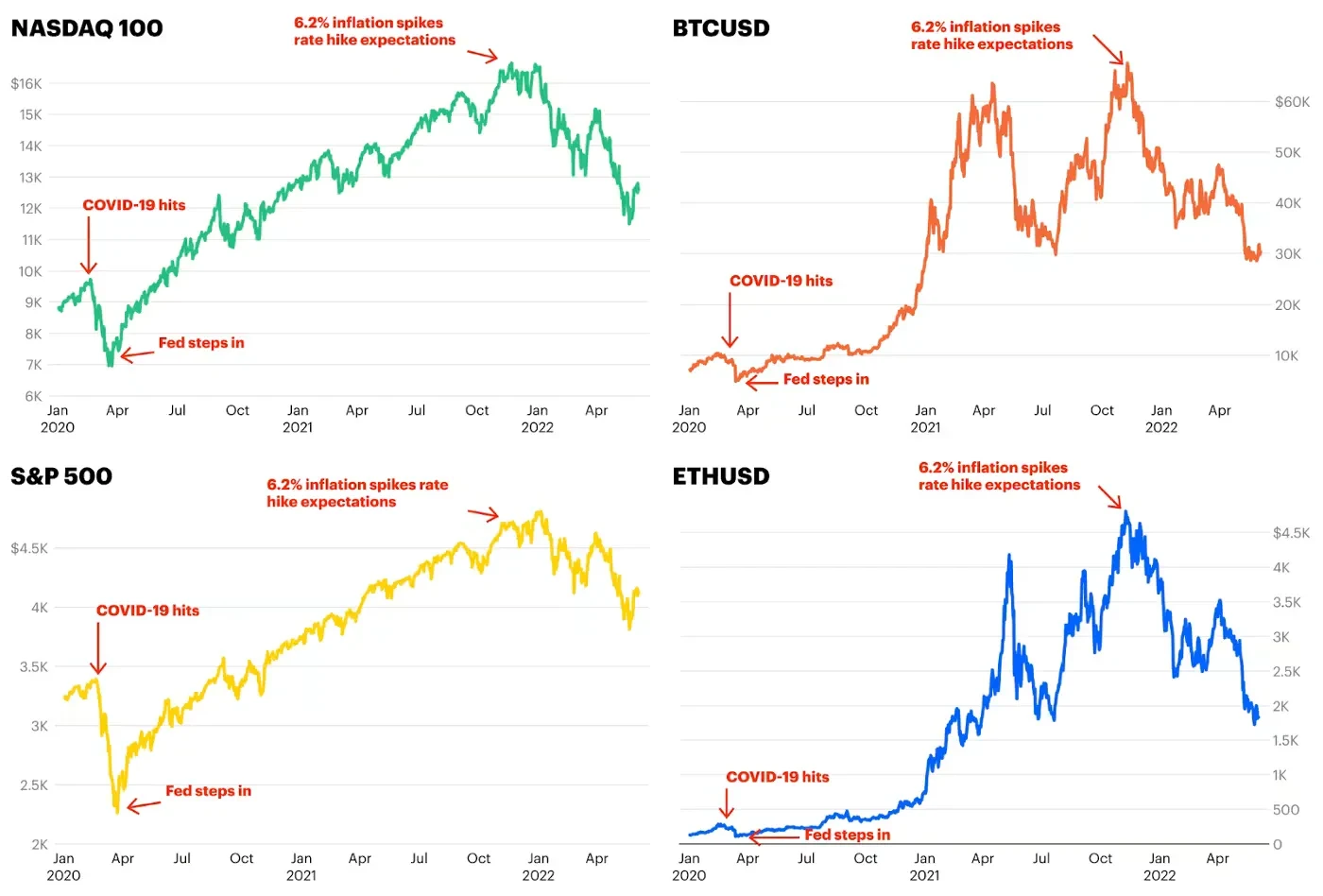

In early 2020, the COVID-19 pandemic struck, bringing the global economy to a standstill and causing all asset classes to plummet.

To prevent an economic collapse, central banks worldwide launched massive quantitative easing, injecting a staggering $9 trillion into the market in 2020 alone.

With an avalanche of liquidity seeking a home and people confined to their homes, vast sums of hot money flooded into Bitcoin, Ethereum, DeFi, and various speculative assets.

Bitcoin surged from under $4,000 to nearly $70,000, its market cap surpassing $1 trillion with institutional backing, outperforming macro assets like gold.

The loose monetary environment also gave birth to the famous DeFi Summer, where the market cap of DeFi protocols skyrocketed 250 times to $180 billion.

While DeFi was supposed to revolutionize traditional finance, the DeFi Summer felt more like a massive online game dominated by profit-seeking traders, with tens of billions of real dollars entering the fray.

The core gameplay was yield farming. Anonymous developers launched new protocols one after another, with project names bizarrely clustering around various foods: YAM Finance, Spaghetti Money, SushiSwap. Traders could deposit mainstream tokens like ETH, USDC, and USDT to claim newly issued tokens from these projects: YAM, SPAGHETTI, SUSHI.

The scene was absurd yet frenzied: Newly launched projects with these novel food-themed tokens could reach a market cap of over $1 billion within days. Early players would cash out at the top, and the token price would subsequently crash.

This was the true Wild West of the internet.

Like the ICO mania before it, DeFi Summer created a new class of wealthy individuals but ultimately succumbed to the bursting of the bubble. This wave also minted a new crypto billionaire, Sam Bankman-Fried, who would later become the central figure in the industry's next disaster.

At the Peak of the Bubble: The 2021 Coinbase Era

Shortly after Coinbase went public with a ~$100 billion market cap in April 2021, I was invited to join its corporate development and venture capital team.

My role involved corporate mergers and acquisitions, analyzing early-stage crypto venture investments, writing industry trend analyses, and helping produce Coinbase's short-lived podcast. To this day, it remains one of the best teams I've ever been a part of.

It was also during this period that another speculative bubble quietly took shape: the NFT boom, centered around digital artwork.

If DeFi was the arena for professional traders, NFTs completely broke into the mainstream public consciousness. They offered artists a new way to monetize their work online and laid the foundation for establishing ownership of digital assets on the internet.

But just like ICOs and DeFi Summer, NFT speculation quickly spiraled out of control. Digital collectibles like cartoon apes, punks, and penguins sold for millions of dollars each. A collage by artist Beeple fetched an absurd $69 million at Christie's auction house.

Crypto concepts thoroughly permeated the mainstream: Larry David mocked crypto skeptics in a Super Bowl ad; Sam Bankman-Fried's exchange FTX spent $135 million to secure naming rights for the Miami Heat's arena. Everyone seemed to be getting rich off tokens, NFTs, and crypto-related stocks.

The madness of 2017 was reoccurring, but magnified four times over due to unprecedented monetary expansion.

The Reckoning: The 2022 Industry Collapse

But the party didn't last. The industry soon descended into a crash.

The factors that inflated all asset prices – low rates, QE, fiscal stimulus – eventually fed into consumer price inflation. By late 2021, Bitcoin, Ethereum, the Nasdaq, and the S&P 500 peaked simultaneously. With inflation spiraling out of control, central banks were forced to tighten policy – the very policy that had pushed stocks and crypto to all-time highs.

As interest rate hikes began and fiscal support withdrew, investors reevaluated their high-valuation assets. Is that cartoon ape really worth $1 million? Why does a sushi-themed token have a $3 billion market cap? How can Dogecoin support a $90 billion valuation?

Pessimism took hold, triggering a systemic chain reaction of failures within the industry.

If the ICO crash was akin to the 2001 dot-com bubble burst, the 2022 event felt more like the 2008 global financial crisis: a small number of toxic assets, combined with high leverage, nearly brought down the entire industry.

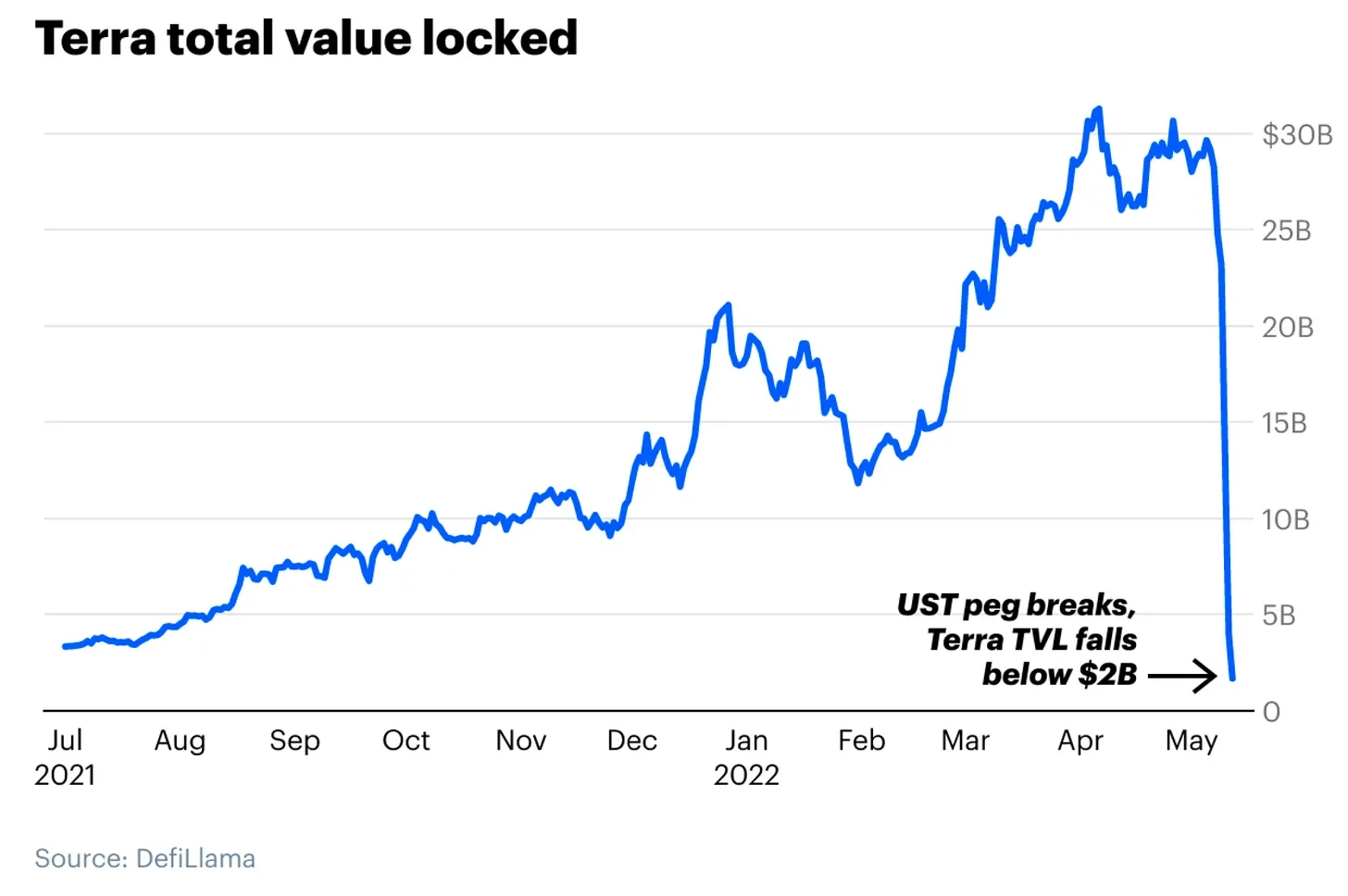

The first domino to fall was Terra's algorithmic stablecoin, UST.

While major stablecoins like USDC and USDT are backed by cash and Treasuries, UST relied on a complex algorithmic mechanism to maintain its $1 peg. The mechanism worked in calm markets but completely collapsed during a selling panic.Cipher

Within days, $32 billion in market value evaporated, and countless holders saw their investments wiped out.

Next came the collapse of Three Arrows Capital, a multi-billion dollar hedge fund, which went bankrupt due to its heavy exposure to Terra and highly leveraged bets. Three Arrows had borrowed heavily from crypto lending platforms like Celsius and Voyager. These platforms had lent out user crypto deposits chasing seemingly stable 8% annual yields. When Three Arrows Capital imploded, the lending platforms froze withdrawals and filed for bankruptcy, leaving ordinary users' deposits worthless.

During my time at Coinbase, we witnessed FTX and Sam Bankman-Fried swoop in to rescue several failing crypto lenders like BlockFi. He was hailed as the "JPMorgan of Crypto" and the industry's white knight.

But the truth eventually surfaced: SBF and FTX were the riskiest players of all.

Remember FTX's massive arena naming rights deal? That expense, and indeed SBF's entire business empire, was propped up by the exchange's proprietary token, FTT, issued out of thin air. SBF took out massive loans using FTT as collateral. When FTT's price crashed, the loans were liquidated, and FTX declared bankruptcy.

Worse still, FTX had secretly used customer funds for investments and to plug holes in its financial accounts. This once $32 billion behemoth crumbled within a week, with $8 billion in customer deposits vanishing.

SBF violated the cardinal rule of exchange operation: never touch user assets.

This was crypto's "Lehman Moment."

Gambling and Casinos: The 2023–2025 Memecoin Mania

After the FTX collapse, SBF was sent to prison. Within 12 months, the crypto market cap shrunk from $3 trillion to under $1 trillion.

Subsequently, the Biden administration launched a comprehensive crackdown on the US crypto industry.

SEC Chair Gary Gensler sued most domestic compliant crypto companies for securities violations, including Coinbase, Kraken, Uniswap, and Robinhood. Those who had operated within the regulatory framework for years became the primary targets of the SEC's enforcement actions.

Meanwhile, Senator Elizabeth Warren pressured traditional banks to sever ties with crypto clients, isolating crypto companies from the banking system and forcing many teams to move overseas.

This regulatory approach led to several unintended consequences.

First, any crypto project with a viable business model (like various DeFi protocols) was deemed a potential securities violation, facing imminent legal risk. The safest option from a legal standpoint became Memecoins – tokens with no practical application or clear vision, purely narrative-driven.

Platforms like Pump.fun launched millions of Memecoins. Celebrities like Iggy Azalea, Caitlyn Jenner, and the Hawk Tuah girl issued their personal Memecoins, all of which eventually devolved into farces.

The crypto industry devolved into a massive casino once again, on a scale far exceeding previous cycles. Over 6 million Memecoins were launched, and the sector's peak market cap reached $150 billion in late 2024, a bubble larger than the NFT mania.

Institutionalization Beckons: The 2025–2026 Crossmint Era

Away from the casino floor, the crypto industry's bet on Donald Trump's election paid off.

As the likelihood of a Trump victory became clear, Bitcoin reached new all-time highs. The market priced in a shift from hostile to friendly regulation in the world's largest economy. Gary Gensler resigned, the new SEC dropped lawsuits against American crypto firms, and traditional banks reopened their doors to crypto business.

Most importantly, the GENIUS Act was passed in July 2025, the first comprehensive federal crypto legislation in the US, establishing clear regulatory rules for stablecoins.

Washington sent a clear signal to Wall Street: the crypto industry, particularly stablecoins, was becoming a major institutional-grade business. Stablecoin companies like Bridge and BVNK were acquired by Stripe and Mastercard for over $1 billion valuations; Rain raised nearly $2 billion in Series C funding; and my former employer, Circle, issuer of USDC, went public, reaching a peak valuation of $60 billion in June 2025.

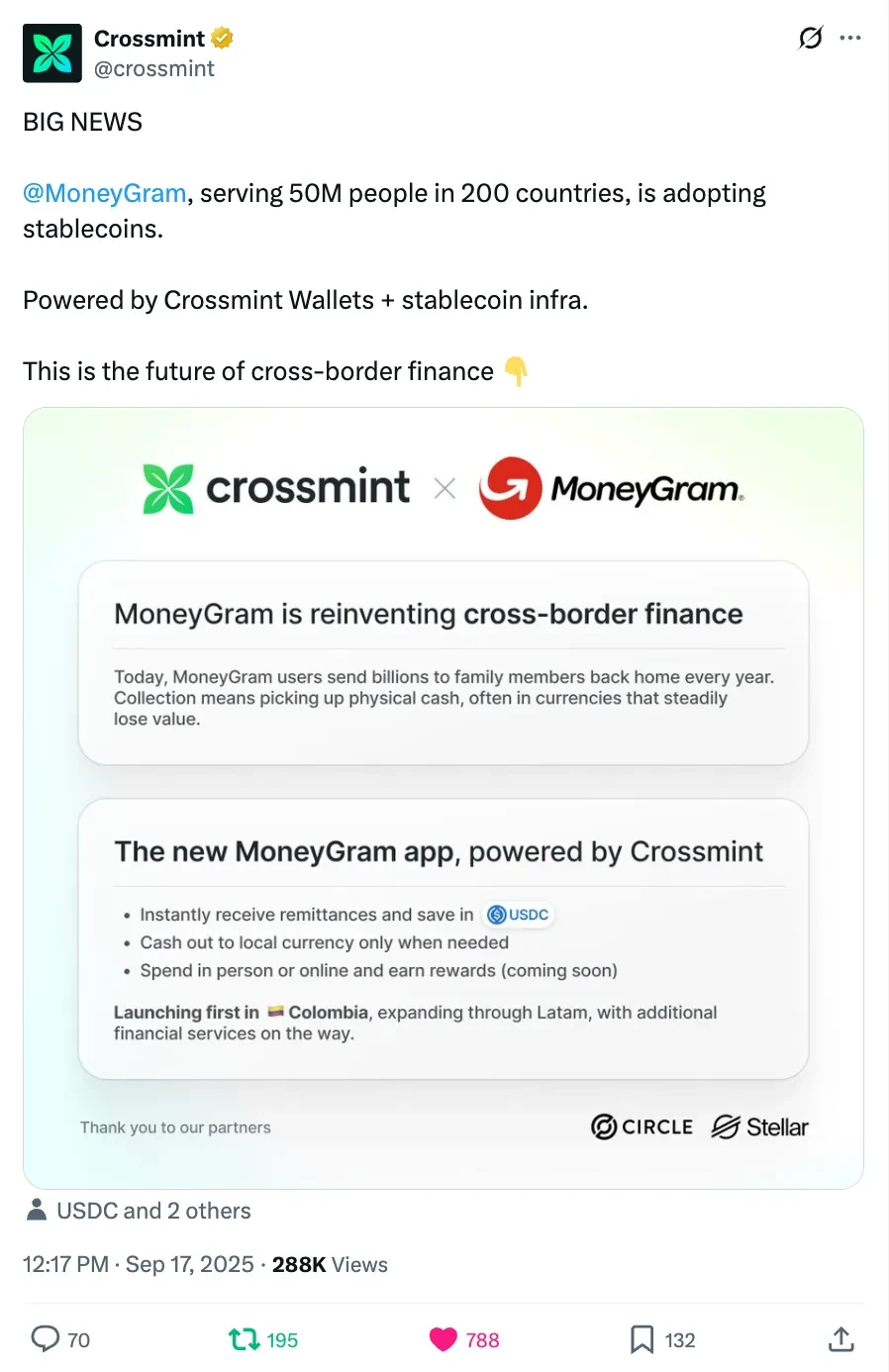

By that time, I was head of marketing at Crossmint, which partnered with MoneyGram to help the century-old money transfer giant use stablecoins for global cross-border fund movement.

As the value of dollar tokenization became evident, Wall Street started seriously planning to tokenize other assets on-chain. Even Larry Fink, CEO of BlackRock, who once called Bitcoin an "index of money laundering," changed his tune, stating that tokenization represents the next evolution of financial markets, where all asset classes like stocks and bonds will eventually be on the blockchain.