一年暴涨39倍,美股存储板块还能买吗?

- Core Thesis: The protagonist of the AI revolution is shifting from GPUs to storage hardware. The memory and storage sector is emerging as the new "pick-and-shovel" provider, with DRAM exhibiting the strongest structural scarcity, followed by NAND, and HDD showing stable growth. SanDisk stands out as the biggest dark horse, perfectly timing its independence.

- Key Factors:

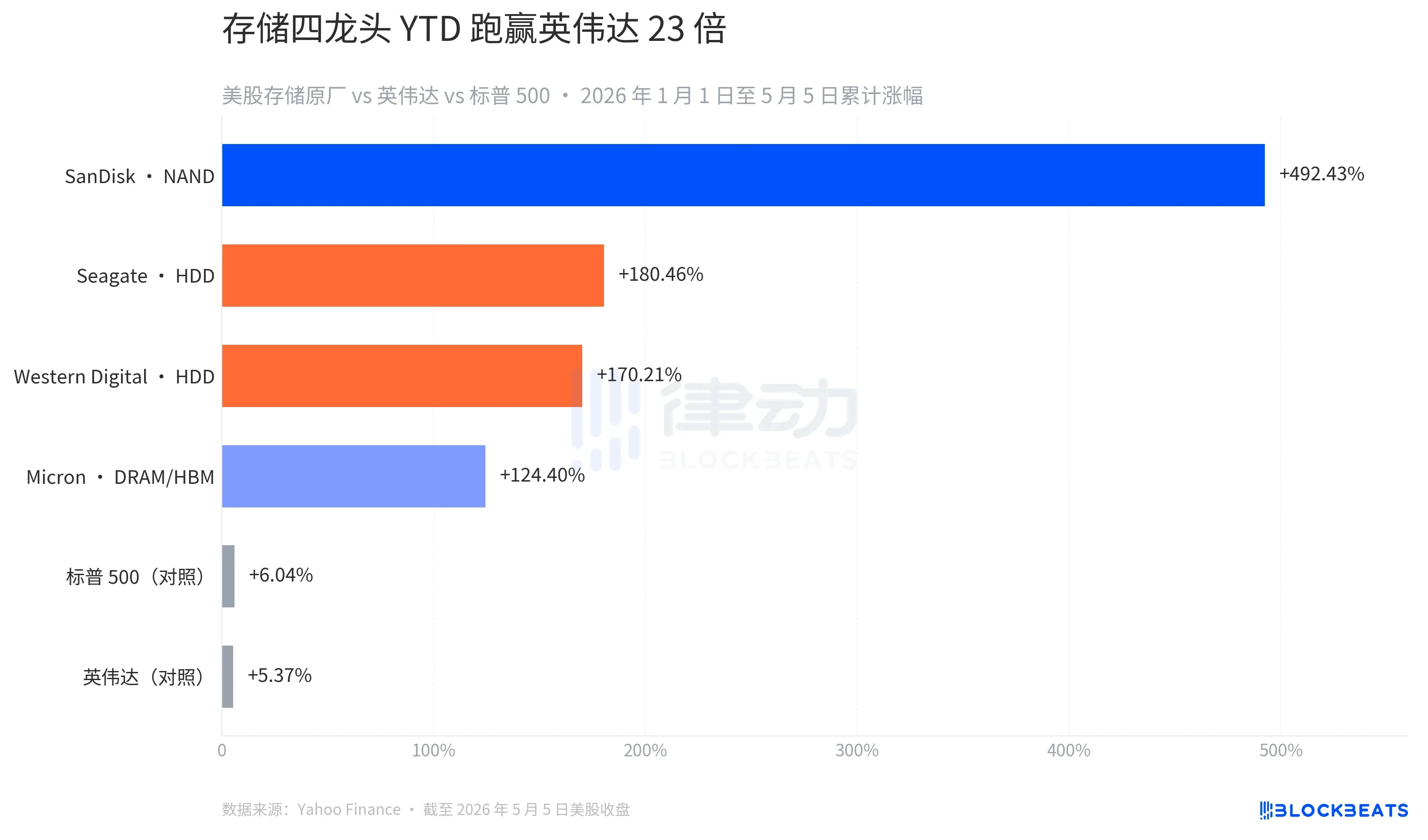

- From the beginning of 2026 to date, stock prices of the four major US storage manufacturers have surged between 124% and 492%, with the weakest performer far surpassing Nvidia (5.37%) and the S&P 500 (6.04%).

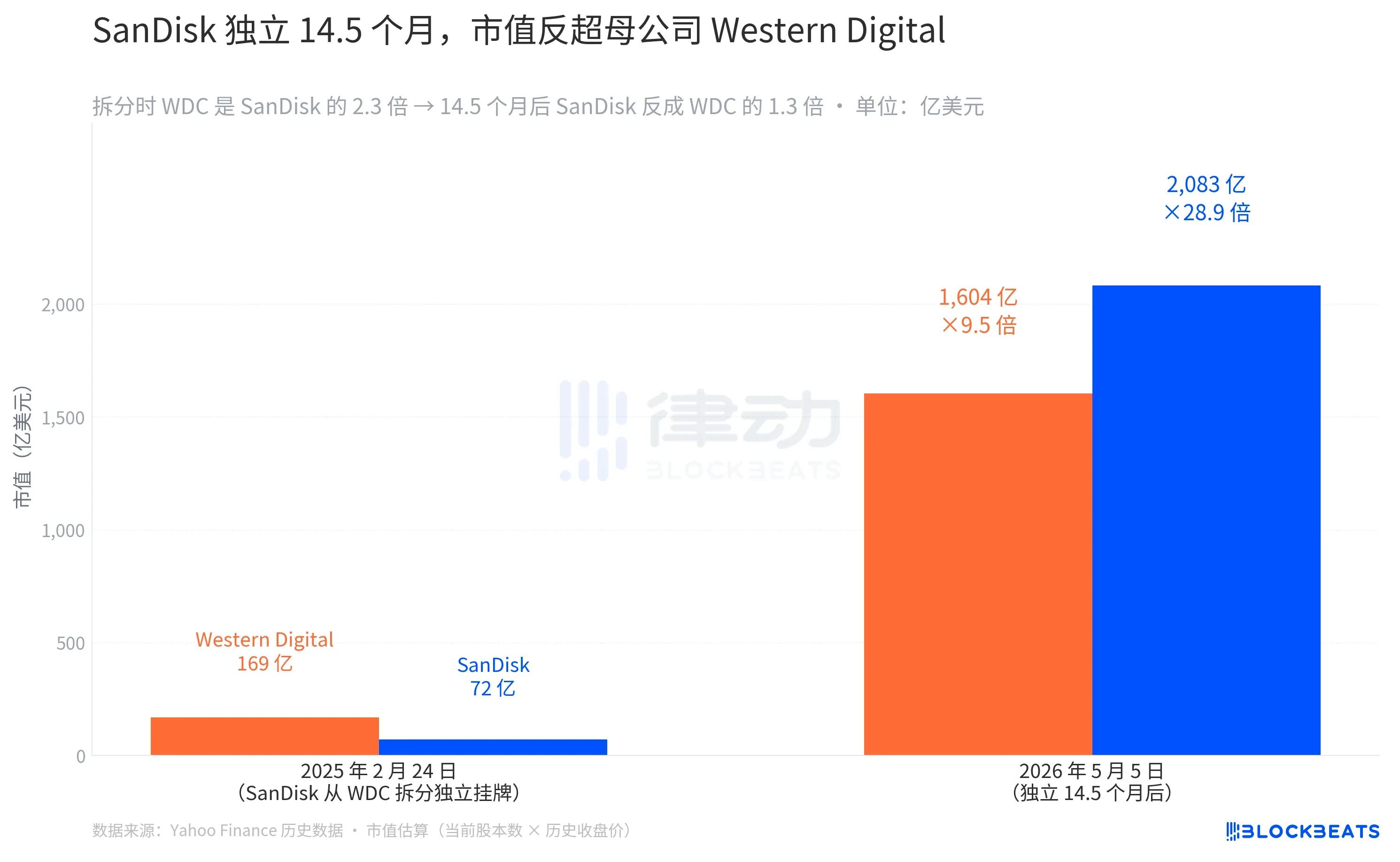

- SanDisk has skyrocketed 492% year-to-date. Just 14.5 months after its spin-off, its market capitalization ($208.3 billion) has overtaken its former parent company, Western Digital ($160.4 billion), defying typical cases of corporate separations.

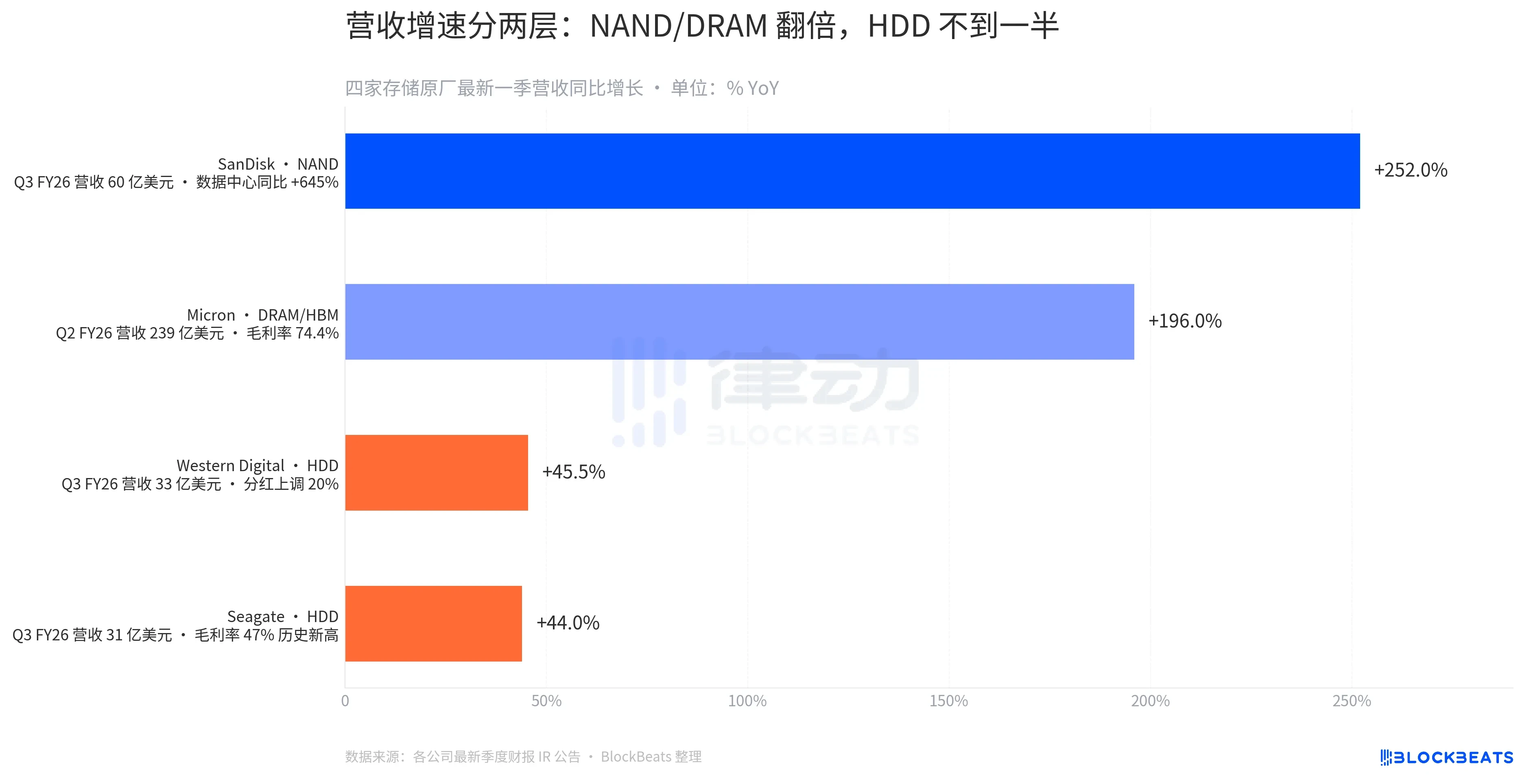

- Growth diverges sharply within the storage segment: NAND vendors (SanDisk) saw YoY revenue growth of +252%, DRAM/HBM vendor Micron +196%, while HDD vendors (Seagate and Western Digital) recorded ~44-45% YoY revenue growth—a 4-5x difference.

- The profit margin stratification is even more extreme: Micron's gross margin reached 74.4%, while Seagate's 47% margin is its historical high. This reflects HBM supply concentrated among three dominant players, giving them far greater pricing power compared to the fragmented HDD market.

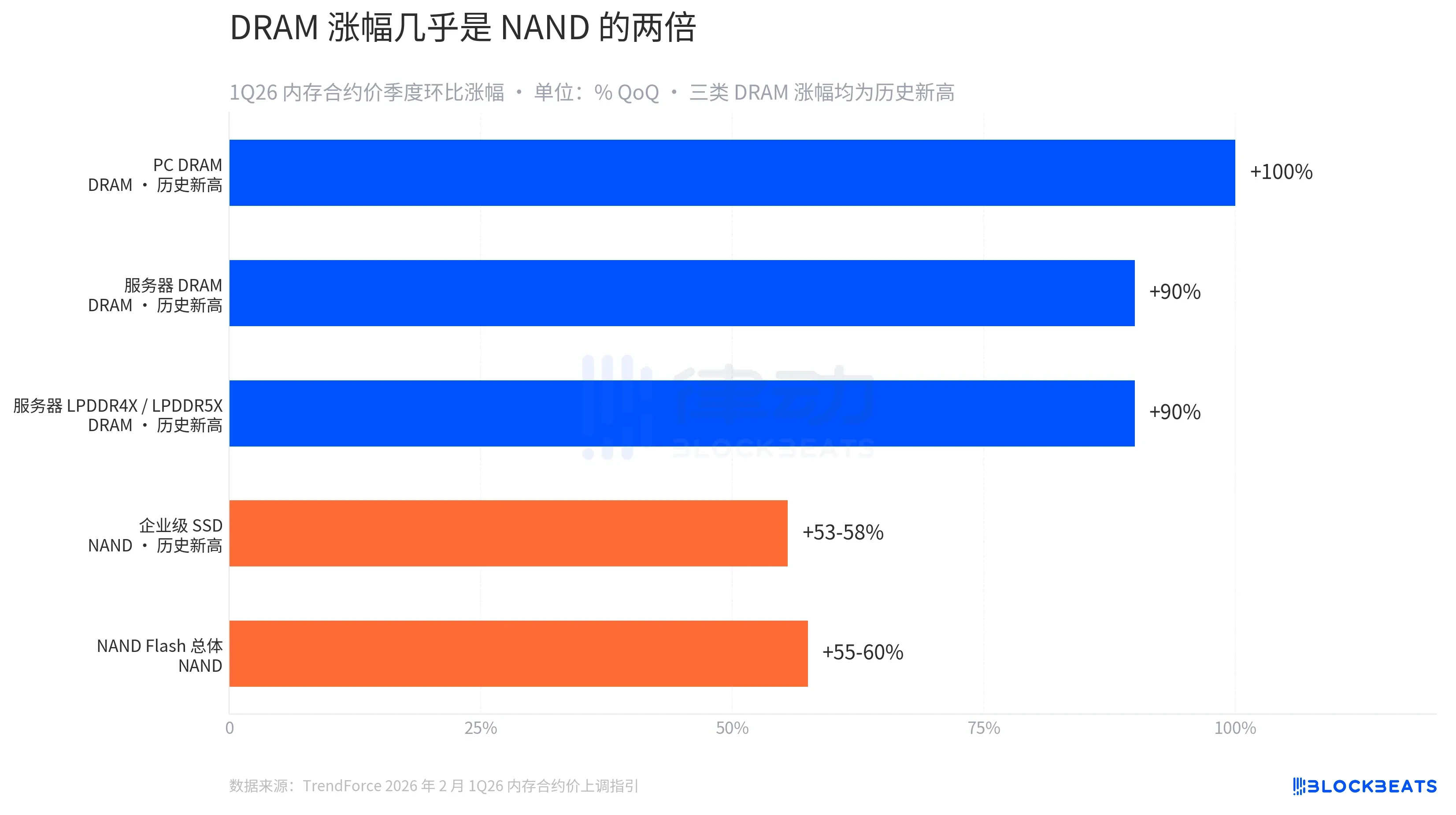

- TrendForce data shows memory contract prices hitting all-time highs in Q1 2026: PC DRAM up ~100% QoQ, server DRAM up ~90%, while enterprise SSDs increased ~53-58%. The supply-demand gap for DRAM is larger than for NAND.

- SanDisk has signed five long-term contracts and received $11 billion in financial guarantees. For its fiscal year 2027, over one-third of its NAND bits are already locked in by customers. This marks the first time the storage industry has adopted a prepaid long-term structure similar to wafer foundries.

The S&P 500 has risen 28% over the past 12 months, and Nvidia has gained 73%. However, compared to the storage sector, these gains still fall short. SanDisk, trading at $34.61 a year ago, is now at $1,406.32, a staggering 39-fold increase.

This NAND flash memory manufacturer, spun off from Western Digital just 14.5 months ago, is the best-performing stock on the US market so far in 2026, with a year-to-date surge of 492%. Behind it are Micron, Seagate, and Western Digital. The YTD gains for these four US storage manufacturers range from 124% to 492%, and even the lowest performer among them has beaten Nvidia by a factor of 23. The "picks and shovels" label of the AI revolution is shifting from the GPU side to the memory side.

The most notable day was May 5th. SanDisk rose 11.98% in a single day, Micron gained 11.06%, Western Digital added 5.18%, and Seagate was up 4.38%. Among the four US storage manufacturers, three hit 52-week highs.

The catalysts were two earnings reports and a supply narrative. On April 28th, Seagate reported Q3 FY26 revenue up 44% year-over-year, with a gross margin of 47% – an all-time high. CEO Dave Mosley stated on the conference call that "AI is ushering Seagate into a new era of structural growth," with nearline exabyte capacity already allocated through 2027.

Two days later, SanDisk reported Q3 FY26 revenue of $5.95 billion, up 252% year-over-year and exceeding the high end of guidance by $1.15 billion. Data center revenue surged 645% year-over-year, nearly doubling sequentially, while Q4 guidance pointed to another 308% to 334% year-over-year increase. Coupled with a credit rating upgrade for Micron from Fitch, the entire sector rallied in unison on Monday.

But this is the surface level. Looking at the four stocks individually, the idea of a "broad storage sector rally" is actually a misleading generalization. They are rallying on three entirely different supply narratives, with vastly divergent gains.

From a year-to-date perspective: SanDisk +492.43%, Seagate +180.46%, Western Digital +170.21%, and Micron +124.40%, occupying four completely distinct tiers. Over the same period, the S&P 500 is up 6.04%, and Nvidia is up 5.37%. Nvidia has even fallen 7.82% in the last five days. The "primary beneficiary of AI" label is migrating: the GPU story driven by large model training has completed its valuation expansion cycle over the past year. Capital is now shifting downstream, into the memory and storage required to handle AI workloads.

This shift is not uniform. It is stratified along the lines of media properties.

The latest quarter's earnings figures clearly illustrate this stratification. On the NAND side, SanDisk's revenue grew 252% year-over-year. On the DRAM/HBM side, Micron's revenue grew 196% year-over-year. On the HDD side, both Western Digital and Seagate saw revenue growth between 44% and 45% year-over-year. NAND and DRAM represent the explosive tier in this cycle, while HDD represents a steady growth tier, with a 4 to 5 times difference between the two.

The stratification in gross margins is even more dramatic. Micron reported a gross margin of 74.4% for Q2 FY26. This is an extreme number achievable by a chipmaker, meaning for every $100 of DRAM and HBM sold, $74 flows into the profit statement. While Seagate's 47% gross margin is an all-time high for the company, it is still an order of magnitude behind the DRAM manufacturers. This disparity stems from differences in supply structure. HBM production capacity is concentrated in the hands of three players (SK Hynix, Samsung, Micron), and it is sold under long-term contracts through the end of 2026. HDD capacity, however, is more evenly distributed between Seagate and Western Digital, resulting in relatively dispersed pricing power.

The pricing signals tell the same story.

According to TrendForce's upward revision of memory contract price guidance for Q1 2026, PC DRAM is expected to increase roughly 100% quarter-over-quarter, server DRAM roughly 90%, and server LPDDR4X/5X roughly 90%. These DRAM price increases across all three categories are historic highs. On the NAND Flash side, enterprise SSDs are projected to rise 53% to 58% in the same period, with overall NAND up 55% to 60%, an amplitude only slightly more than half that of DRAM.

This represents a scissors differential that explains everything. AI servers require both NAND and DRAM, but have a greater need for bandwidth (HBM) and capacity density (DDR5, LPDDR5X). The supply-demand gap for DRAM is much larger than for NAND. In the Q2 FY26 earnings call, Micron's CEO succinctly stated this supply narrative with "We're sold out for 2026." HBM4 36GB 12H has already begun volume shipments for Nvidia's Vera Rubin platform, and the full-year FY26 capital expenditure has been raised from $20 billion to $25 billion, preparing for another leg up in 2027.

Among the four manufacturers, SanDisk is the one most worth examining individually.

SanDisk was spun off from Western Digital on February 24, 2025, and listed on Nasdaq. It opened at $52 on the first day and closed at $48.60, giving it a market cap of approximately $7.2 billion. On the same day, Western Digital closed at $49.02, with a market cap of about $16.9 billion. At the time of the spin-off, Western Digital was 2.3 times the size of SanDisk.

Today, 14.5 months later, SanDisk has a market cap of $208.3 billion, while Western Digital's market cap stands at $160.4 billion. SanDisk has reversed positions to become 1.3 times the size of Western Digital. This kind of inversion is uncommon in the history of large corporate spin-offs. In most cases, a subsidiary spends its first year rebuilding investor relations, and it typically takes 3 to 5 years for its market cap to catch up to its parent company. SanDisk did it in 14.5 months.

The reason is that it was spun off at precisely the right time. When Western Digital decided on the spin-off in 2024, the rationale was that "NAND and HDD are in different capital cycles and operating them separately provides clearer valuation." This judgment was later validated by the market: after independence, SanDisk focused on NAND, perfectly timing the explosive demand for enterprise SSDs from AI data centers. Western Digital focused on HDD, riding the wave of structural growth in cloud storage archiving. Separated, each company corresponds to a distinct narrative. If they hadn't been split, a single company housing two businesses with completely different supply cycles would have been valued by the capital market at a more conservative multiple, weighing it down.

On May 4th, Bernstein raised SanDisk's target price from $1,250 to $1,700, citing the visibility of its data center SSD business. SanDisk's earnings report disclosed that it has signed five long-term contracts, received $11 billion in financial guarantees, and locked in over one-third of its NAND bits for FY2027. This is a sector traditionally treated based on commodity cycles, now seeing a "long-term contract plus customer prepayment" structure for the first time, similar to advanced process wafer foundries.

In summary, capital is flowing from the GPU side to the memory side. DRAM is the true alpha in this cycle, while HDD represents a different rhythm of structural long-term growth. SanDisk, a company independent for just 15 months, has surpassed its parent company Western Digital in market capitalization on the back of its NAND data center business alone.

On the same trading day, May 5th, Nvidia fell 1.03%, TSMC fell 1.79%, and SanDisk rose 11.98%. All considered "AI beneficiaries," the market is already using its feet to vote, differentiating precisely which type of supply is the scarcest.