Wiping Out Three Years of Gains and Evaporating $2 Trillion, What Happened to the U.S. Stock Market?

- Core View: The sharp reversal in market interest rate expectations is causing a significant correction in U.S. tech giants (Mag 7) due to previously inflated valuations and uncertainty surrounding AI investment returns. Capital is flowing from the tech sector to cyclical areas such as energy and defense.

- Key Factors:

- Market interest rate expectations have completely flipped from rate cuts to hikes within three months. CME data shows the probability of a rate hike within the year has reached 52%, primarily driven by geopolitical conflicts pushing up oil prices and inflation expectations.

- Mag 7 stocks have given back all their year-to-date gains, with Microsoft experiencing the largest decline from its peak (35.7%), indicating the most severe contraction in its "certainty premium."

- Four major tech companies have budgeted up to $650 billion for AI capital expenditures in 2026, but the market is punishing those with unclear return paths (e.g., Microsoft, Meta) more than the scale of investment itself.

- Significant shifts in capital flows are evident, with ETFs in cyclical sectors like energy, materials, and industrials dominating net inflows year-to-date and achieving average gains (+20%) far exceeding the tech sector (-6%).

- Several institutions have raised their probability of a U.S. economic recession to between 30% and 50%, intensifying the market's repricing of high-valuation growth stocks in a rising interest rate environment.

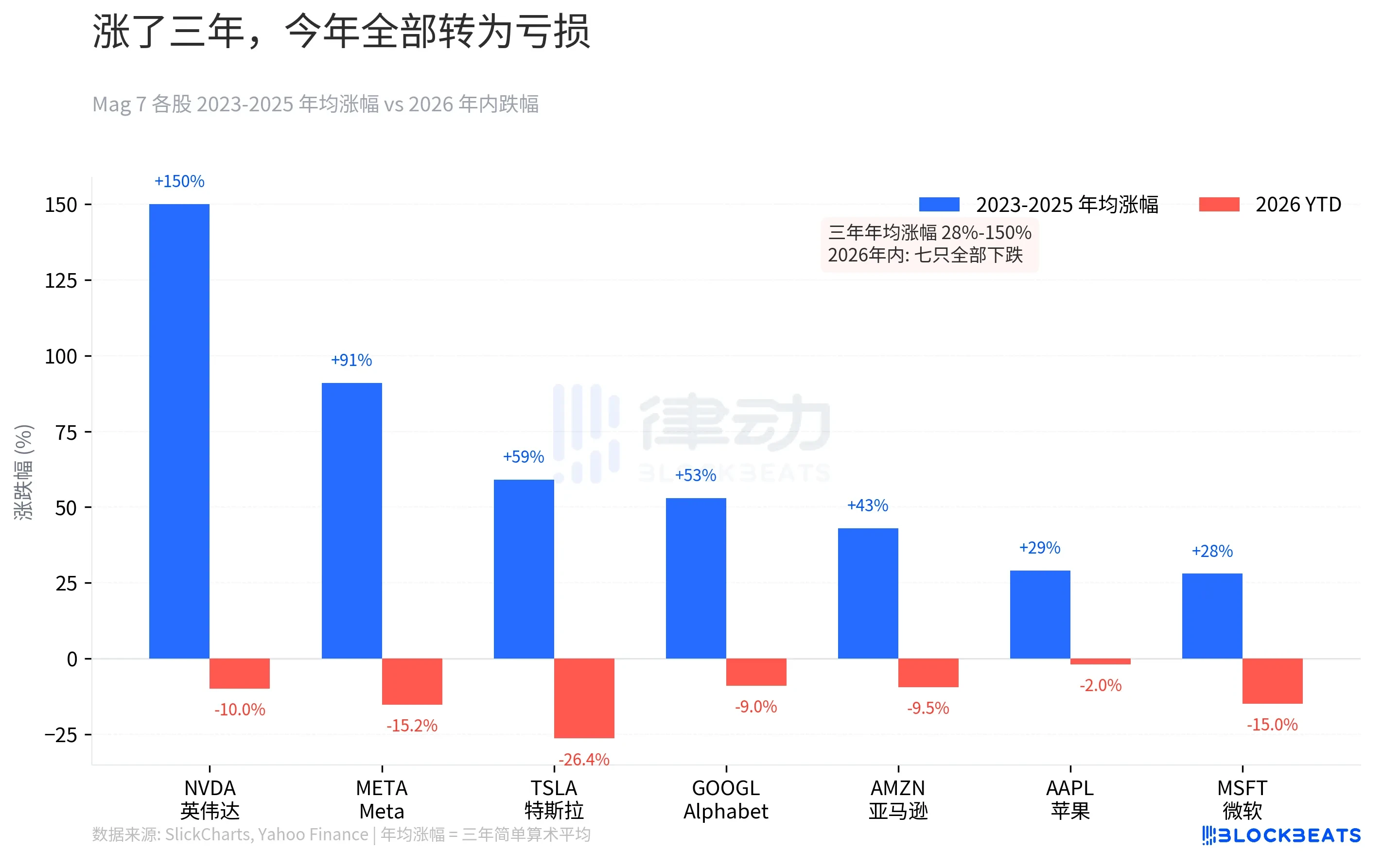

At the close of the U.S. stock market last weekend, all seven major tech stocks had completely erased their year-to-date gains, with none spared. According to Yahoo Finance data, Tesla is down 26.4% year-to-date, Microsoft down 15%, Meta down 15.2%, Nvidia down 10%, Amazon down 9.5%, Google down 9%, and Apple down 2%. Looking at broader market data, the S&P 500 has closed lower for five consecutive weeks, hitting a seven-month low, with a cumulative decline of 5.1% for the year. The Dow Jones Industrial Average entered correction territory that day. This marks the longest losing streak since 2022.

Nvidia surged 239% in 2023 but is now down 10% year-to-date. This number may seem mild, but if you bought at the peak in October 2025, you are actually down 21.2%. Meta rose 194% in 2023 and is now 15.2% off its peak. The faith accumulated over a three-year bull market is gradually eroding within three months.

The gains from 2024 and 2025 have already been decelerating, from 107% to 64% to 23%. Growth has slowed, but valuations haven't followed suit. When the music stops, the risk premium ignored over three years returns all at once.

Interest Rate Hike Expectations Flip: From Single Digits to 52% in Just Three Months

Falling stock prices are just the result. What has truly flipped are interest rate expectations.

According to CME FedWatch data, in early January 2026, the market was still pricing in rate cuts, with the probability of a hike within the year below 3%. The consensus at the end of 2025 was that the Federal Reserve would continue cutting rates in 2026.

The turning point began on February 28th. The "Operation Epic Fury" action escalated tensions in the Strait of Hormuz, directly threatening this critical chokepoint that carries 20% of the world's oil transportation. Brent crude closed at $112.57 on March 27th, marking a 45% gain year-to-date. Rising oil prices fueled inflation expectations, which in turn directly rewrote interest rate pricing.

On March 27th, the CME futures market priced in a probability of a rate hike within the year exceeding 50% for the first time, reaching 52%. This is the first time since early 2023 that the market has flipped from "expecting rate cuts" to "expecting rate hikes." According to the Atlanta Fed's Market Probability Tracker data, the probability of a 25 basis point hike has reached 19.8%.

From near zero to over half, in less than three months. At the beginning of the year, the discussion was about how many rate cuts; now, it's about whether there will be a hike.

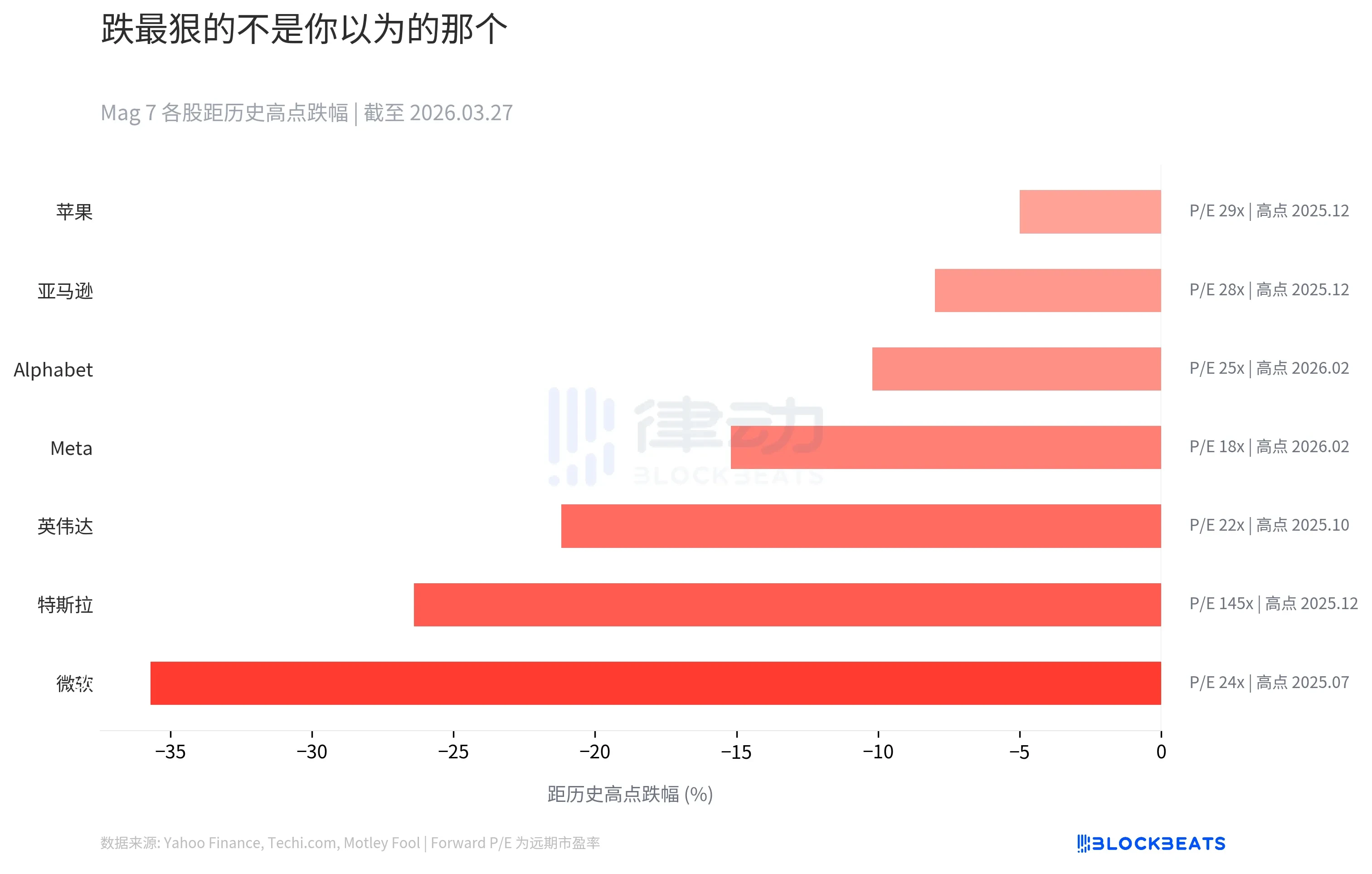

Microsoft Fell the Hardest, Not Tesla

Intuition tells you that Tesla should have fallen the most among the Magnificent 7. It has the highest volatility and the most controversy. But the data presents a different reality.

According to comprehensive data from Techi.com and Motley Fool, Microsoft has fallen 35.7% from its July 2025 peak (around $534), making it the biggest decliner from its all-time high among the Magnificent 7. Tesla ranks second with a 26.4% drop, and Nvidia third with 21.2%.

But looking at the Forward P/E column on the right, the story gets more complex. Tesla's forward P/E is 145x, while Microsoft's is only 24x. Microsoft fell more because the market's expectation pricing for it was more rigid. When the overall environment worsens, the "certainty premium" contracts the most sharply.

Apple is the most resilient among the seven, down only 5% from its peak. But a 29x Forward P/E means this "safety" isn't cheap.

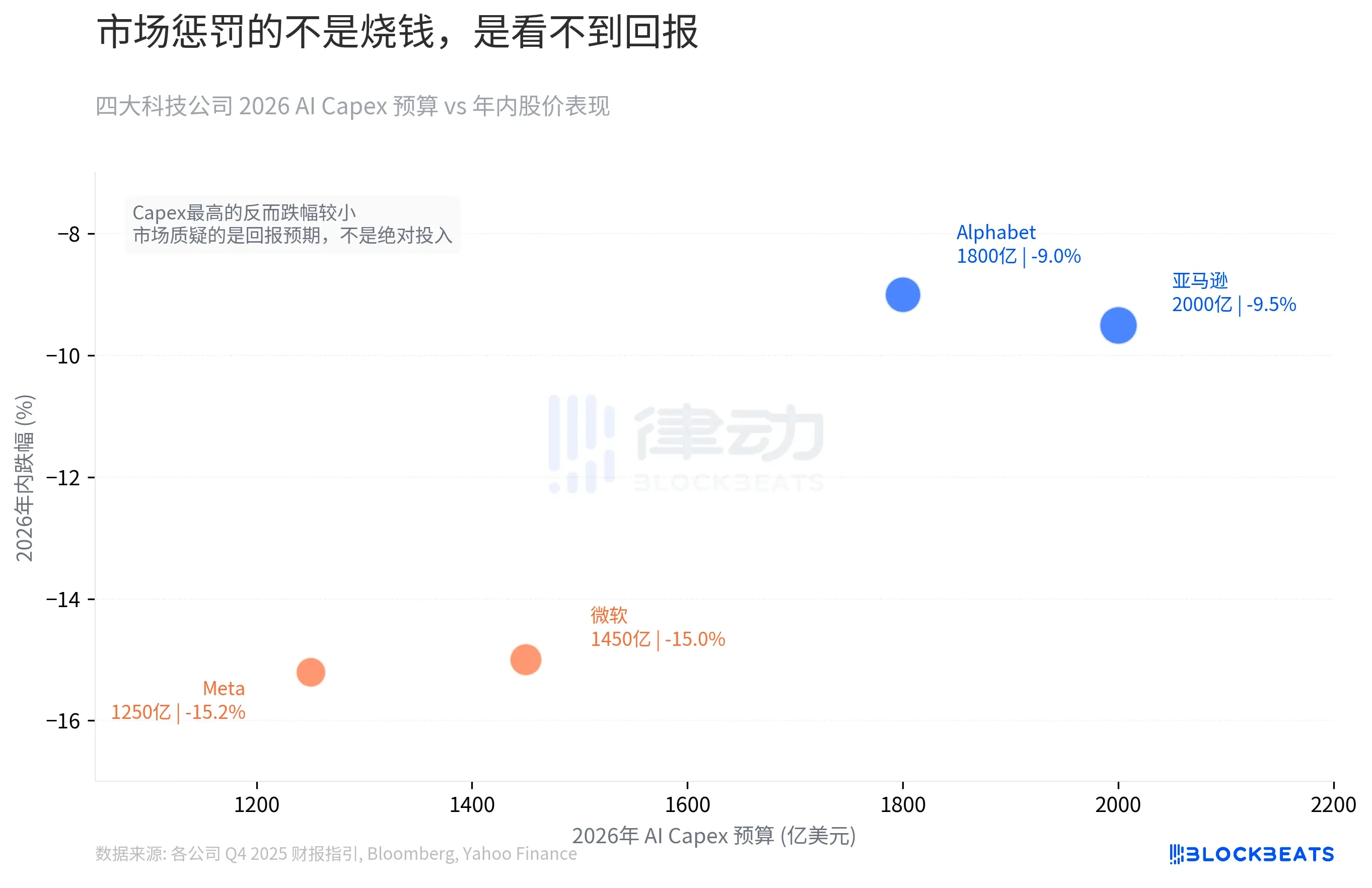

$650 Billion AI Capital Expenditure: Spending Isn't the Problem, Return Expectations Are

The Magnificent 7 have written themselves an unprecedented check for 2026.

According to Q4 2025 earnings guidance from each company and Bloomberg aggregated data, the combined 2026 AI capital expenditure budget for Amazon, Google, Microsoft, and Meta is approximately $650 billion, representing a roughly 67% increase from the $381 billion in 2025. Each company's budget this year is close to or exceeds the sum of the past three years.

Amazon (with the largest Capex at $200 billion) and Google ($180 billion) are down only 9.5% and 9% year-to-date, respectively. In contrast, Microsoft ($145 billion) and Meta ($125 billion), with lower Capex, are down 15% and 15.2%. The ones spending the most fell the least.

The market is not punishing the absolute scale of investment but the visibility of returns. Amazon's AI investment directly serves its cash flow engine, AWS. Google's investment has a clear monetization path through search ads. Where Microsoft and Meta's AI spending will land is still a guess for investors; the enterprise penetration rate of Copilot and the strategic pivot from the metaverse to AI Agents have yet to materialize into numbers. The rate hike cycle doesn't wait for the story to finish.

Capital is Already Voting with Its Feet

According to State Street Global Advisors' monthly fund flow data, from the beginning of 2026 to date, ETFs in cyclical sectors such as energy, materials, and industrials have seen net inflows of $19 billion, accounting for 65% of all sector ETF inflows, far exceeding these sectors' 47% market weight. According to Morningstar data, natural resources funds saw inflows of $7.5 billion in January, setting a new monthly record for the sector.

According to ETF Trends data, cyclical sectors have averaged a +20% gain year-to-date, while the tech sector is down -6%, and the S&P 500 overall is up only +0.5%. The defense ETF (SHLD) saw net inflows exceeding $1 billion in January alone and is up +20% year-to-date. The tech sector hasn't completely bled out, with $6 billion still flowing in during February, but returns have significantly underperformed cyclical sectors.

Once interest rate expectations flipped, the $650 billion AI expenditure became the most conspicuous line item on the balance sheet. Institutional capital is already moving, shifting to energy and defense.

EY-Parthenon's chief economist, Gregory Daco, calls the current situation "multidimensional disruption." He puts the probability of a U.S. recession at 40%. Goldman Sachs gives 30%, and Moody's chief economist Mark Zandi puts the number close to 50%.

Three years of overperformance, flipped in three months, with $650 billion hanging in the balance during a rate hike cycle. The $2 trillion in market capitalization evaporated from the Magnificent 7 isn't just panic on a single day. Is the market repricing for a cycle that has already ended?