$200,000 for $1,000? Opinion Airdrop "Rug Pull" Sparks Community Outrage

- Core Viewpoint: The TGE of the prediction market protocol Opinion, due to its tokenomics design—particularly the airdrop allocation falling far below expectations—has caused significant losses for early points users and triggered a community trust crisis. Meanwhile, its previously astonishing trading volume data has been questioned as primarily driven by points incentives, casting doubt on its sustainability.

- Key Elements:

- Token Distribution Controversy: The Q1 airdrop released only 3% of the total token supply, far below market expectations, causing the secondary market price of points to plummet over 85% and resulting in heavy losses for users who invested substantial funds early on.

- Community Trust Erosion: The project team is accused of using the points mechanism to attract user data and traffic contributions, only to unilaterally change the rules upon redemption, crossing a red line for community trust.

- Abnormal Trading Data: Opinion supported 31% of the industry's trading volume with an extremely low number of transactions (accounting for 3% of the industry), with an average transaction size far exceeding peers, allegedly artificially inflated by the points incentive structure.

- Questionable User Growth: The platform's active user count fluctuates wildly, and per capita trading volume rises abnormally as scale expands, which does not align with patterns of organic growth.

- Strong Capital Backing: The project has received investment from several well-known institutions, with cumulative financing exceeding $25 million, and has secured support from Binance's ecosystem resources, positioning itself to serve the Asia-Pacific market.

- Future Core Uncertainty: After the points incentives end, real trading volume and user retention will become the key determinants of the project's value.

Original author: ChandlerZ, Foresight News

The rising star in the prediction market sector, Opinion, is about to have its TGE moment. However, this long-awaited token launch has not brought celebration, but rather widespread user anger and a list of losses.

According to its published OPN tokenomics, the first-quarter airdrop accounts for only 3% of the total token supply, a stark contrast to previous market expectations; the pre-market price of Opinion points plummeted from a high of $45 per point to $6 per point; influencers like @daidaibtc publicly stated that they burned $200,000 participating in point accumulation, only to receive 2,000 OPN in the end, equivalent to approximately $1,000.

This is one of the most controversial TGEs at the beginning of 2026.

Pre-market Price Surges Over 30% Briefly, Yet Airdrop Users Are in Tears

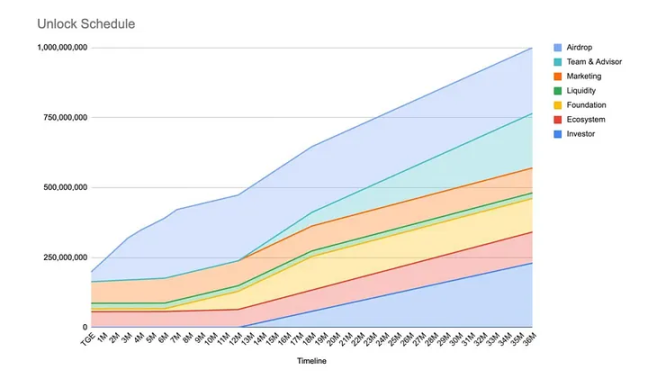

On the evening of March 2, the Opinion Foundation officially announced the tokenomics and roadmap for its native token OPN. The total supply of OPN is 1 billion tokens, with an initial circulating supply of 198.5 million tokens, to be deployed on Ethereum and BNB Chain. Regarding token distribution, the airdrop accounts for 23.5% (235 million tokens), with 3.5% released at TGE and the remainder vesting over 7 months; investors account for 23% (230 million tokens), and the team & advisors account for 19.5% (195 million tokens), both subject to a 12-month lock-up period followed by 24-month linear vesting.

The Foundation allocation is 12% (120 million tokens), with 1% released at TGE; Ecosystem & Incentives is 11.1% (111 million tokens), with 5.65% released at TGE (including 3.5% locked airdrop rewards and 2.15% retroactive incentives); Marketing is 8.9% (89 million tokens), with 7.7% released at TGE; Liquidity & Market Making is 2% (20 million tokens), with 2% released at TGE.

After Opinion announced the airdrop check website, the Binance pre-market price briefly surged over 30%, breaking above $0.57.

Some influencers noted that before the tokenomics were announced, the secondary market price for OPN points once reached $45 per point. As the official disclosure revealed that the first-season airdrop would release only 3% of the total token supply, the pre-market price rapidly plunged to $6 per point, a cumulative drop exceeding 85%.

Even more bizarre is that the token price movement itself was completely opposite to the experience of airdrop users. Precisely because the initial circulating supply was extremely low, the pre-market OPN price briefly rallied. The logic of low circulation and high control temporarily worked on the price level, but point holders had already been washed out in the pre-market crash. Based on feedback from several well-known studios, the cost of points ranged between $5 to $20 per point. When converted to the post-TGE airdrop value, almost none resulted in positive returns.

Influencer "带带带比特" publicly shared his loss breakdown: investing $200,000 to farm points, ultimately receiving 2,000 OPN, worth about $1,000 at current prices. "$200k for 2000 tokens. Yes, you read that right." This statement quickly went viral in the Chinese crypto community.

Polymarket data shows the probability of the bet "OPN FDV exceeding $500 million one day after listing" is 64%, indicating market expectations are not overly pessimistic. However, the anger of airdrop users primarily lies in the distribution logic itself.

"带带带比特" stated, "I certainly accept getting rekt while farming airdrops. Who said farming must be profitable? You win some, you lose some. What I'm angry about is the betrayal. You could learn from Lighter and simply not issue points. If you don't issue points, see if any farmers will help you generate data? But you issued points, told everyone to come farm, help me generate data, used the community, and then at TGE, you say the points were just for fun, now they don't count. Does that make any sense?"

The project actively recruited users with a points mechanism to generate data and buzz, but unilaterally reset the implicit contract when it came time to deliver. Losses themselves are common in the current climate, but the operational logic of "use and discard" violates the community's bottom line regarding basic trust.

Backed by Multiple Renowned VCs, Founders with Hong Kong/Wall Street Background

Opinion (Opinion Labs) is an on-chain prediction market protocol. Unlike the binary settlement mechanisms of mainstream platforms like Polymarket and Kalshi, Opinion focuses on a continuous prediction market model. Users don't need to wait for event settlement; they can buy, sell, and adjust positions at any time during topic evolution, with market prices continuously reflecting changes in collective expectations. The platform's underlying architecture uses a CLOB (Central Limit Order Book), while also introducing AI-assisted market creation features, allowing any user to launch structured prediction markets covering topics from macro-financial events to esports, entertainment, regional politics, and other Asia-Pacific-specific content.

Regarding the founding team, Opinion CEO Forrest Liu graduated from Columbia University and previously worked as a corporate financing advisor at CMB International Capital, bringing traditional financial institution experience. The co-founding team also includes former JPMorgan members. The project positions itself to fill the gap left by Western platforms (Polymarket, Kalshi) in the Asia-Pacific content market, making it one of the few on-chain protocols in the prediction market sector targeting Asian users as its core audience.

Opinion has completed two funding rounds, raising over $25 million in total. In March 2024, Yzi Labs announced the 13 early-stage projects selected for its 7th MVB Accelerator Program, which included Opinion. In March 2025, Opinion announced the completion of a $5 million seed round led by Yzi Labs, with other investors including angel investment community Echo, Animoca Ventures, Manifold Trading, Amber Group, etc.

YZi Labs' endorsement meant Opinion directly gained access to Binance ecosystem resources, subsequently launching on Binance Launchpool and the Binance Wallet Booster program as scheduled. Changpeng Zhao tweeted in October 2025, "YZi Labs is only a minority investor in prediction market Opinion, but will try our best to help add strategic value."

In February 2026, Opinion announced another $20 million Pre-Series A funding round, co-led by Hack VC and Jump Crypto, with participation from Primitive Ventures, Decasonic, and Continue Fund.

The Other Side of High Growth: OI/Vol Anomalies and Data Scrutiny

However, Opinion's high-speed growth narrative has never escaped one质疑: is the trading volume real?

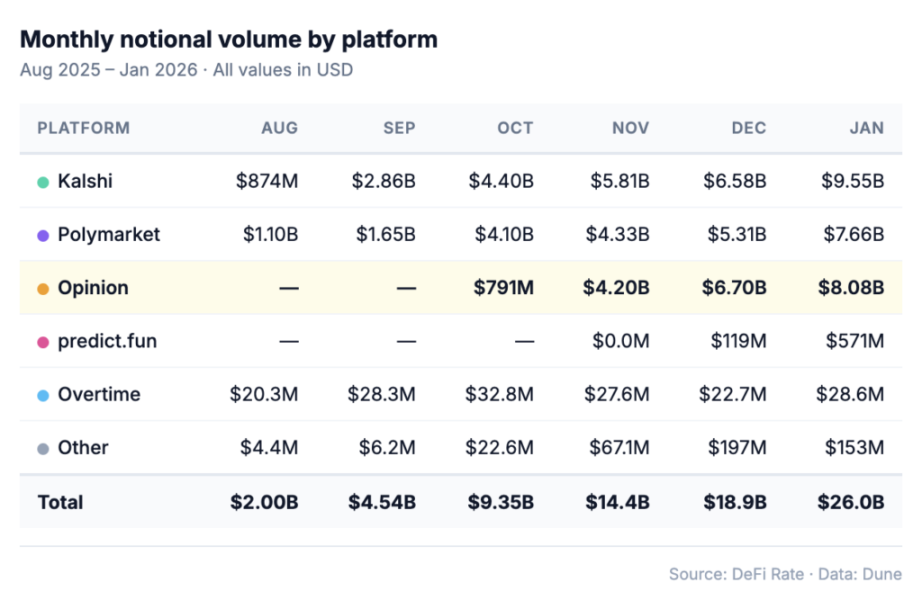

According to a report by DeFi Data, Kalshi's monthly trading volume grew from $874 million in August to $9.55 billion in January, an 11-fold increase, primarily driven by sports events. Polymarket's trading volume also grew from $1.1 billion to $7.66 billion, a 7-fold increase, with a more diversified business composition covering sports, cryptocurrency, politics, and other areas.

Opinion launched on October 23. In its first month (less than a full month), it achieved $791 million in revenue, reached $4.2 billion in November, and soared to $6.7 billion in December, surpassing Kalshi and Polymarket's revenue for that month.

While trading volume is a key metric, the actual number of trades tells a different story. In January 2026, Opinion's trading volume was $8.08 billion across 3.2 million trades, averaging about $2,525 per trade. In the same month, Kalshi's trading volume was $9.55 billion across 54.5 million trades (average $175 per trade). Polymarket's trading volume was $7.66 billion across 52 million trades (average $147 per trade).

Opinion, with less than 3% of the industry's total trade count, accounted for 31% of the industry's total trading volume. Its average trade size of $2,525 is 17 times that of Polymarket and 14 times that of Kalshi.

Such a deviation is almost impossible under organic user behavior. The report further points out two other anomalies: First, Opinion's active user count showed drastic fluctuations of up to 6x within weeks, whereas organically growing platforms typically have stable user bases. Second, as the platform scaled, Opinion's average trading volume per user did not decrease but instead continued to rise. This contradicts the pattern seen in almost all normally growing platforms.

The root of the problem highly points to Opinion's points incentive design (PTS). PTS fixedly distributes 100,000 points weekly, allocated proportionally among all users based on contribution. The core calculation weights for "contribution" include three items: trade size, holding duration, and the proximity of order price to the market mid-price. Among these, trade size directly impacts the score—larger single trades carry higher point weights.

DeFi Rate's conclusion is that these trades are real and occur on-chain, but the structural incentives create a data pattern highly deviated from organic demand. Opinion's data isn't necessarily fake, but it likely records capital behavior driven by points farming, not genuine prediction market demand.

With TGE落地, the points incentives have ended. The fuel driving that $8 billion monthly trading volume has been extinguished. Whether that capital remains on the platform will directly determine how substantial Opinion's real user base truly is.

Two Pending Questions

Opinion emerged at an excellent juncture in its sector. User education for prediction markets is largely complete, regulatory attitudes are becoming clearer, and the Asia-Pacific region holds vast potential market size. However, choosing to conduct its TGE during a market downturn with a tokenomics model that triggered massive community backlash—this combination of timing and approach inevitably means user retention in the post-airdrop era will face higher friction costs.

Two pending questions remain for Opinion: After removing the points incentives, how much of that $8 billion monthly trading volume remains? And among those early users who got "rekt," how many will choose to stay, and how many have already left for good? The answers to these two questions will jointly determine how much real value support OPN has before the wave of token unlocks arrives.