Earning $8,000 in 4 Days: A Complete Practical Guide to Market Making on Polymarket

- Core Viewpoint: Based on practical experience on Polymarket, the author has summarized a framework for a Liquidity Provider (LP) strategy aimed at stably earning market-making rewards while controlling risks. It emphasizes market selection, two-sided order placement, laddered structure, dynamic spread adjustment, and strict position management.

- Key Elements:

- Market Selection is Crucial: Prioritize markets with high trading volume, tight spreads, clear timelines, "quiet periods," and where incentive intensity is relatively high compared to liquidity. This enhances market-making efficiency and stability.

- Adhere to Two-Sided Order Placement and Neutral Positioning: The core is to simultaneously place YES and NO orders to capture spreads and rewards, not to speculate on direction. Actively manage positions through reverse orders or consolidation to avoid accumulating one-sided risk.

- Employ a Laddered Order Structure: Place small orders near the mid-price for high-frequency fills, and place larger orders further from the market price as buffers. This disperses fill prices to reduce the risk of being quickly swept.

- Dynamically Adjust Quote Spreads: Proactively widen spreads or pause order placement when market volatility spikes, significant news breaks, or positions become imbalanced. This avoids becoming a passive liquidity taker during sharp price movements.

- Utilize Tools to Enhance Efficiency: It is recommended to use Betmoar for market screening and data analysis, Polycule (TG Bot) for wallet monitoring and trade notifications, and PolyRewards for tracking reward earnings.

Original Title:My POLYMARKET LP Rewards Strategy ,Author: josele.sol(@joselebetis2)

Compiled by | Odaily(@OdailyChina);Translator | Asher(@Asher_ 0210)

Over the past few days, I have been continuously testing and optimizing an LP strategy on Polymarket, accumulating approximately $6,000 in Sponsored LP rewards and $2,000 in trading profits over 4 days.

Based on these practical results, this article outlines a complete market-making framework covering core aspects such as market selection, order placement structure, position management, and risk control. It is not the only solution, but under the current conditions of capital scale, risk appetite, and time commitment, this has proven to be the most stable and efficient approach.

First, Choosing the Right Market is More Important Than You Think

Market selection determines more than 50% of the outcome. High-quality markets typically mean narrower permissible bid-ask spreads, healthier order book structures, clearer execution paths, and more stable reward density. The screening logic mainly focuses on the following four points:

High Trading Volume + Narrow Spread

Prioritize markets that are actively traded with naturally narrow spreads. These markets facilitate easier continuous execution, have smaller slippage, more stable order book structures, and are more conducive to consistently earning market-making rewards.

Events with Clear Timelines

Events with precise timelines (e.g., matches, policy announcements, scheduled result releases) are more predictable. A clear timeline aids in planning ahead and reduces risks from completely random volatility.

Existence of "Quiet Periods"

Markets with low news flow phases are more suitable for market-making, such as nighttime or periods before an event starts. During these phases, price fluctuations are usually smaller, making it easier to place orders closer to the market price.

Higher Incentive Intensity Relative to Liquidity

The core metric is "how much reward per dollar of liquidity." When incentives are more concentrated relative to total liquidity, the reward density is higher, and overall market-making efficiency is better.

Second, Core Market-Making Principles

Two-Sided Order Placement (YES + NO)

Always place YES and NO orders on both sides around the mid-price. The core objectives are only three: capturing the spread, earning incentive rewards, and maintaining market-making eligibility. The essence of two-sided order placement is maintaining the "liquidity provider" role, not betting on direction.

Position Management (Avoid Excessive One-Sided Exposure)

If executions consistently favor one side, it indicates increasing risk, not stable profit. When one side is executed too much, you can:

- Place a reverse sell order near the market price;

- Recover liquidity through merging;

- Actively restore bilateral balance via market execution.

The core goal is to maintain a neutral structure, avoiding the transition from market-maker to directional speculator.

Actively Cancel Orders During Market Turmoil

During breaking news, real-time key events, or high-volatility phases, actively widen spreads or even temporarily stop placing orders. Maintaining tight spreads during sharp volatility is not an advantage but risks becoming the counterparty for others exiting liquidity. In comparison, disciplined active cancellation is often more important than continuously participating in order placement.

Third, Tiered Order Placement Structure

Instead of placing one large order on each side, a more robust approach is to build a "tiered" structure—distributing multiple orders across different price levels. This allows for continuous liquidity provision without becoming a precise target for rapid price movements. The structure is as follows:

- Place small orders near the mid-price (narrower spread): Increases execution probability, maintains a steady execution pace, and continuously earns incentives and fee revenue.

- Place larger orders further from the mid-price (wider spread): Forms a buffer zone during price movements, reduces the risk of being quickly swept, and provides more room for position adjustments.

The tiered structure lowers the probability of being "precisely harvested" and disperses executions across different price levels, making positions easier to control—especially when implementing LP strategies across multiple markets on Polymarket simultaneously, this layered structure is particularly important.

Fourth, Spread Rules

First, set a target spread, then dynamically widen or narrow orders based on market conditions. The real advantage doesn't come from keeping the spread extremely narrow at all times, but only quoting close to the market price during relatively safe and stable periods.

Main adjustment criteria include:

- Sudden increase in volatility: When prices start moving rapidly, actively widen the spread to avoid being swept by consecutive orders.

- News or real-time events: During major announcements or critical moments, market repricing is fast; quotes should be appropriately widened, or paused if necessary.

- Position imbalance: If executions consistently favor one side, widen the quotes on the frequently executed side while moderately bringing the quotes on the side needing rebalancing closer to the market.

In summary, when the market becomes unstable, prioritize widening spreads or temporarily stepping back. When conditions stabilize, bring quotes closer to the market price.

Fifth, Position Management

Position imbalance is the real reason that overwhelms most market-makers.

If executions consistently favor one side, that's not "making more money" but continuously accumulating a one-sided position, increasing risk. The goal of market-making is to continuously provide orders while avoiding being trapped by one-sided position risk.

When executions clearly favor one side, the following strategies can be adopted:

- Reduce order size on the dominant side: If one side is consistently executed, actively reduce its size to prevent the position from continuously expanding.

- Strengthen quotes on the hedging side: Moderately increase the attractiveness of the other side to accelerate rebalancing executions and gradually restore position balance.

- Gradual adjustments: Make small, continuous corrections to the position, avoiding emotional or one-time aggressive hedging.

Two Methods to Clear Positions

Method one is selling the existing position. Sell the one-sided position in batches, gradually reducing risk and freeing up capital for continued operation.

Method two is merging after filling the gap. If YES and NO positions are asymmetric, buy the missing side and execute a merge on Polymarket to eliminate risk exposure and release capital.

Don't Become the "Liquidity Taker"

This is more about execution discipline than being clever. Sometimes, placing orders very close to the market price is not an advantage but merely actively taking on chips that others are eager to exit.

The following situations typically warrant avoiding close-to-market quotes:

- Major announcements or real-time key events: Market repricing is far faster than manual adjustments, making it easy to be instantly swept.

- Low-liquidity events: Insufficient trading volume, disorderly price jumps, often resulting in poor execution quality.

- Sudden price discovery events: New information emerges, the market is re-finding a price range, and direction is not yet stable.

A more robust approach is: significantly widen spreads, reduce order size, or temporarily exit, waiting for the order book structure to stabilize before re-engaging. Only in this way can you avoid passively taking on risk during sharp volatility.

Sixth, Time Commitment Management

This strategy does not require 24/7 monitoring, but it is certainly not "set and forget." It can run in the background most of the time, but you must remain ready to respond at any moment to quickly adjust when market conditions change.

The time structure is roughly as follows:

- Approximately 10–20% active operation time: Deploying capital, adjusting tiered structures and spreads, correcting positions.

- Approximately 80–90% passive running time: The system continuously places orders, but attention is still required.

The key is to always maintain a state of readiness to respond to changes. Typically, operate near a computer with mobile notifications enabled so that once the market shows unusual movement, you can immediately adjust spreads, pause orders, or rearrange the order structure.

Seventh, Recommended Supporting Tools

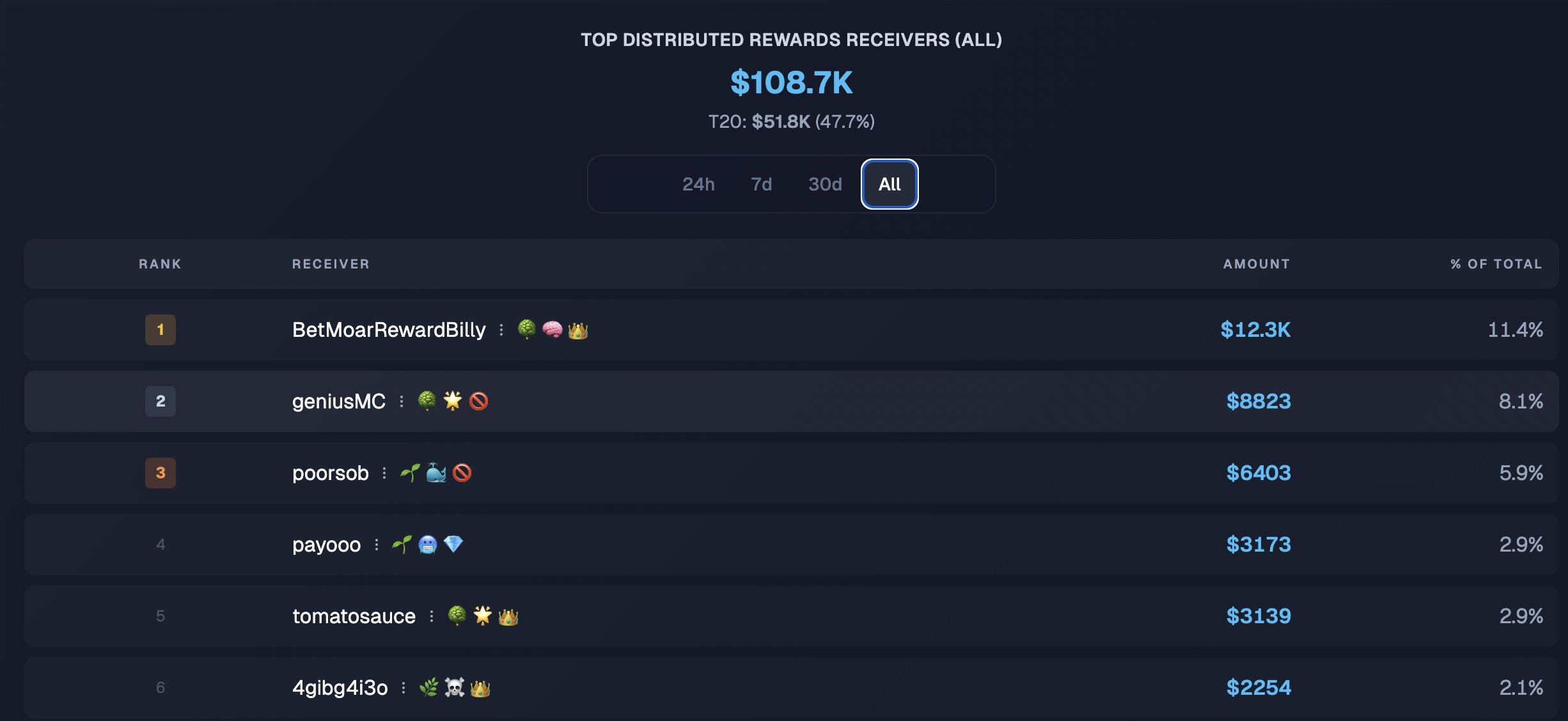

Betmoar(@betmoardotfun)

Used for market screening and data observation. Its advantage lies in more clearly displaying market structure and reward distribution, especially being more efficient when screening for markets with high Sponsored LP Rewards.

Currently, Polymarket's internal display and filtering of rewards are still not intuitive enough, so using external tools can help identify markets with higher reward density more quickly. (Although subsequent optimizations have been made, the information obtained here is usually more accurate.)

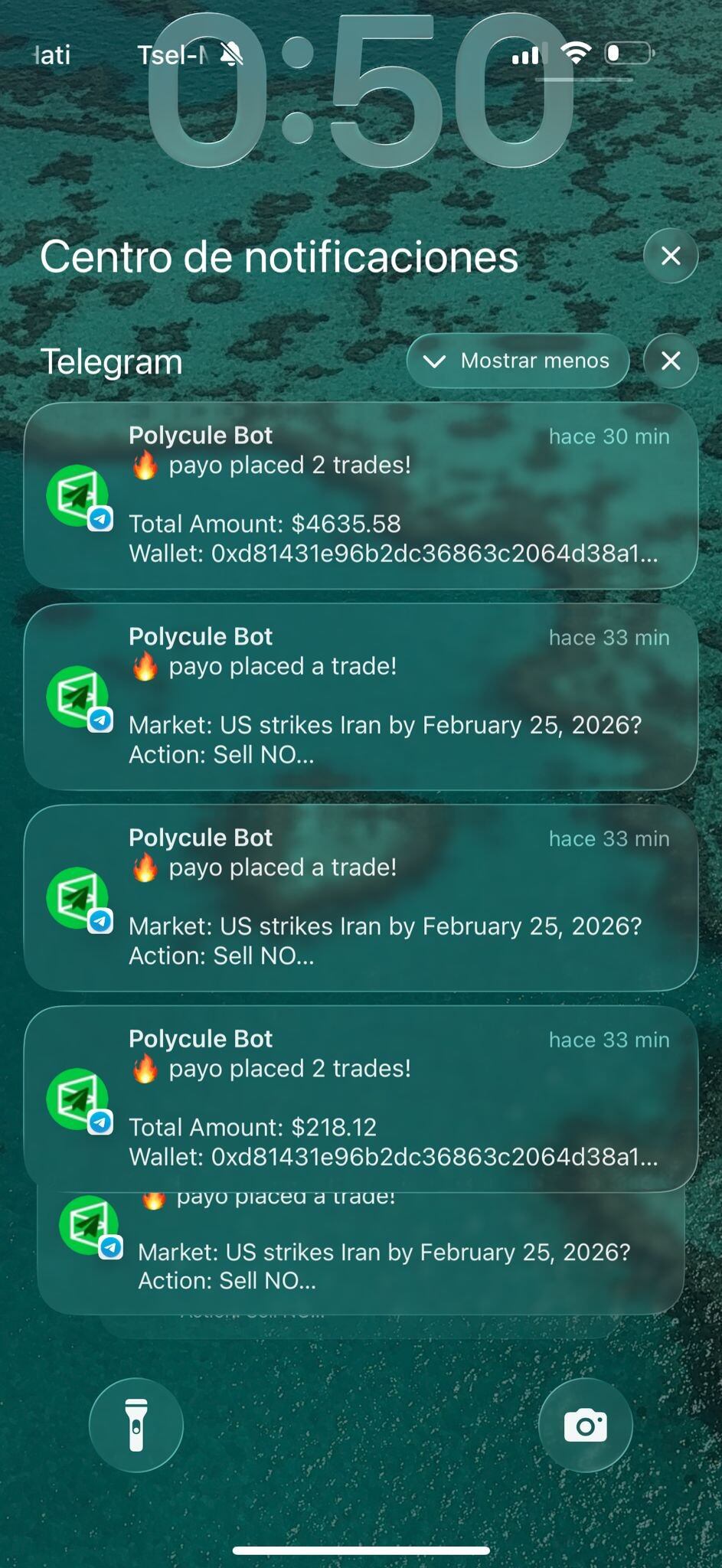

Polycule(TG Bot)

Primarily used for wallet tracking and execution notifications. Other features are not core use cases; the focus is on timely notifications and clear records, facilitating monitoring of executions and position changes.

Additionally, use the PolyRewards(@PolyReward) reward tracking tool to quickly view reward earnings and overall data performance (link: https://polyrewards.fun/).

The above content outlines a personal LP market-making strategy and is not the only method. This strategy is suitable for the current capital scale, risk tolerance, and available time and effort. Results may vary significantly under different conditions; furthermore, incentive rules and market environments are subject to change at any time.