Crypto's New Path: Building the Next Generation of Permissionless New Banks

- Core View: Crypto neo-banks are attempting to use blockchain technology to reconstruct the financial backend, building a global, composable, censorship-resistant value transfer system through stablecoins and public blockchains. Their development path may start by entering the value-added and lending scenarios with the highest capital flow velocity, then extend to payments and storage.

- Key Elements:

- Crypto neo-banks build their landscape around the four major financial relationships of "Save, Spend, Grow, Borrow." Their core value lies in leveraging blockchain's permissionless and programmable nature to achieve faster global capital movement.

- Regarding the construction path, entering from high capital velocity scenarios like "Grow" and "Borrow" (e.g., Hyperliquid, Aave) is more likely to succeed, as they can first capture value in motion and high user engagement.

- Current key challenges include: solving enterprise-grade privacy and compliance parity, achieving composability with real-world payment standards, and unlocking non-overcollateralized consumer credit.

- Stablecoin payments are a crucial breakthrough. On the retail side, experience is enhanced through crypto cards, while on the enterprise side, "stablecoin chains" focused on high-frequency payments (e.g., Tempo) are emerging. However, the key to success lies in merchant adoption and network scale.

- Wallets (e.g., MetaMask, Phantom), as user entry points, have distribution advantages. However, they need to transform into active trading and payment platforms to effectively monetize traffic and achieve the leap from "storage" to "full-stack finance."

Editor's Note: A decade ago, fintech neobanks improved the banking experience through mobile apps but did not change the underlying system of how money moves. Today, cryptocurrency technology is attempting to touch upon a deeper transformation, redefining "how money flows."

This article examines the development path and competitive landscape of crypto neobanks from the four dimensions of "Store, Spend, Grow, Borrow": from self-custody wallets and stablecoin payments to on-chain trading, lending, and yield mechanisms. Author Jay Yu (Research and Investment Team Member at Pantera Capital) suggests that, using the speed of capital flow as a clue, the breakthrough for crypto neobanks may first appear in high-frequency, high-turnover growth and borrowing scenarios, gradually extending to payments and storage.

Before issues of privacy, compliance, real-world connectivity, and credit systems are fully resolved, crypto neobanks remain in an early exploratory stage. However, it is certain that they are not merely new financial applications but are attempting to build an entirely new track for capital movement.

The following is the original text:

Introduction

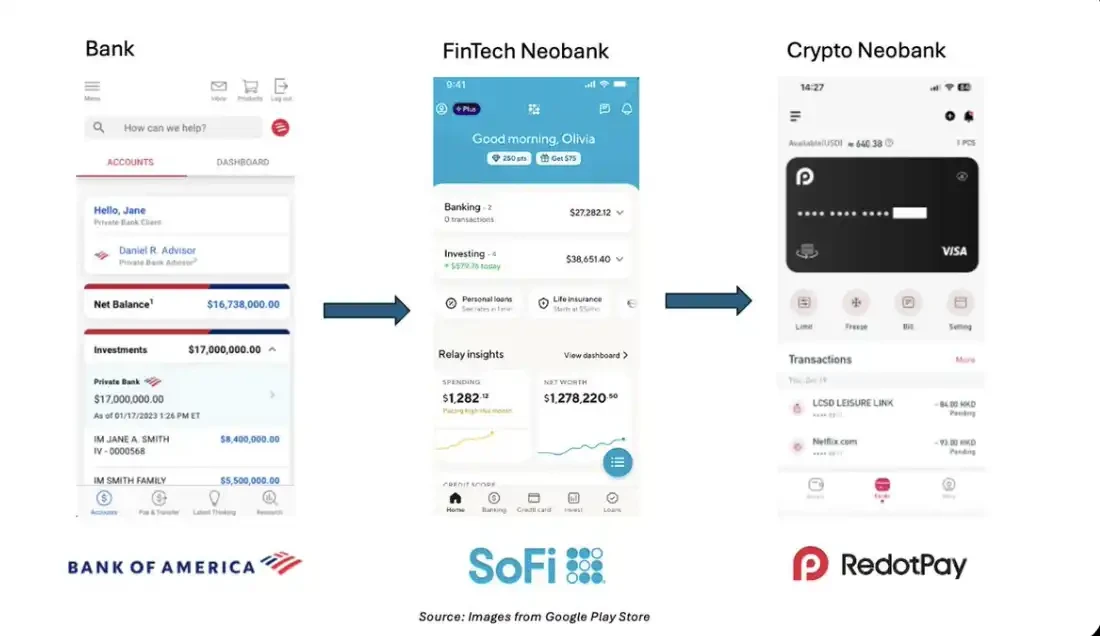

No matter which banking or fintech app you open today—be it Bank of America, Revolut, Chase, or SoFi—scrolling down the interface evokes a sense of déjà vu: Accounts, Pay & Transfer, Earn Yield. These interfaces are almost interchangeable.

This highly similar design reveals the common underlying logic of banking: banks are essentially the interface manifestation of the four core relationships we have with "money":

- Store: A place to hold and preserve assets

- Spend: A mechanism for daily expenses and transfers

- Grow: A set of tools for passive or active wealth management

- Borrow: A channel for accessing external capital and utilizing leverage

Over the past decade, the proliferation of mobile technology has driven the rise of "neobank" apps like SoFi, Revolut, and Wise. They have made financial services more inclusive and redefined what "going to the bank" means—replacing physical branches with intuitive, always-online digital interfaces.

Today, as crypto technology enters its second decade, a new paradigm is emerging. From self-custody wallets and stablecoins to on-chain credit and yield mechanisms, the permissionless and programmable nature of blockchain enables banking-like experiences to become global, instant, and composable.

If mobile internet gave birth to neobanks, then crypto technology is nurturing permissionless neobanks: a unified, interoperable, self-custody-centric interface that allows users to store, spend, grow, and borrow capital within the on-chain economy.

The History of Fintech Neobanks

Similar to the crypto industry, the rise of neobanks also occurred after the 2008 financial crisis. Unlike traditional banks replicating physical branch networks, neobanks are more like technology platforms, delivering banking services to users through mobile interfaces.

Most neobanks partner with traditional banks in the backend, with the latter providing deposit insurance and compliance infrastructure, while the neobanks themselves manage the frontend user relationship. With fast account opening, transparent fee structures, and digital experience-centric design, many neobanks have gradually become users' primary entry point for saving, spending, and managing wealth.

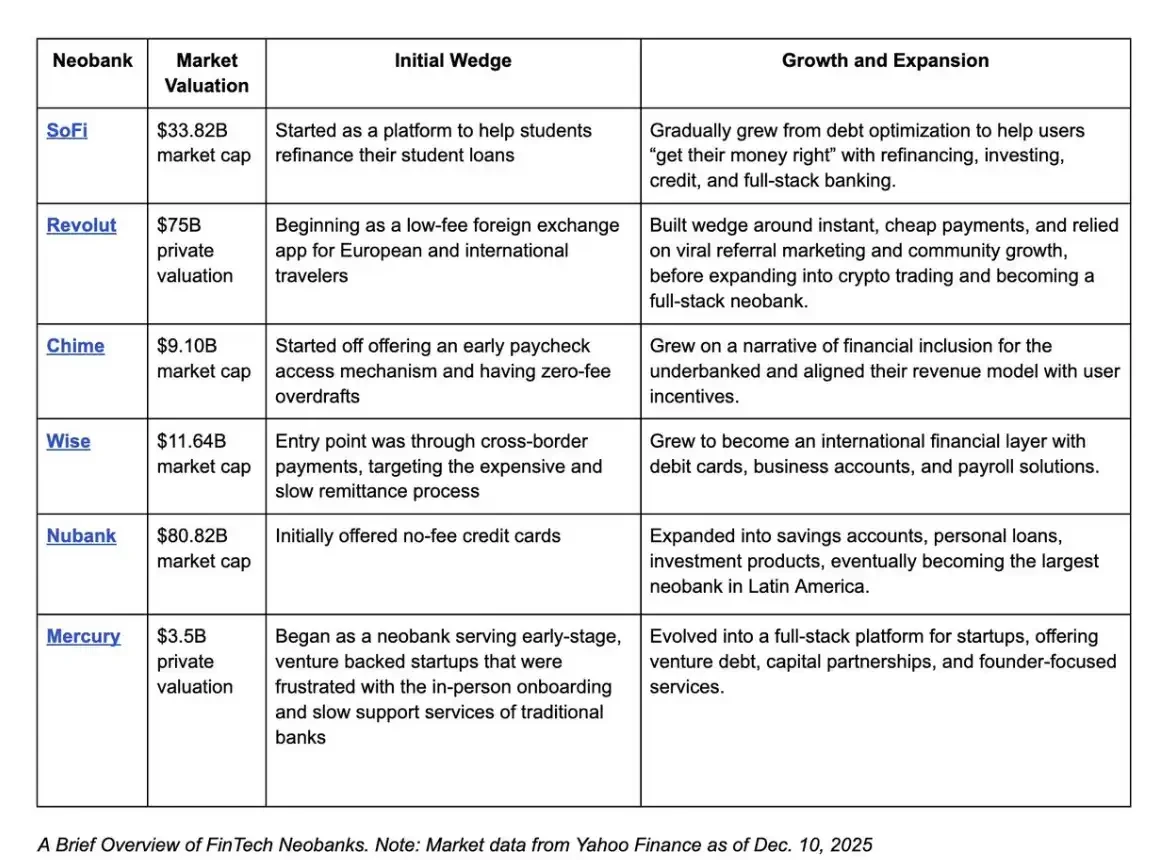

Reviewing the growth paths of these billion-dollar neobank startups reveals a commonality: they captured user relationships through unique digital product forms, whether through refinancing services, early wage access, transparent foreign exchange rates, or other differentiated features. This initiated a user-centric transaction volume flywheel, which then gradually expanded the product matrix to monetize existing users.

Simply put, the victory of fintech neobanks lies in their capture of the "entry point for money": by reshaping the medium through which users save, spend, invest, and borrow, they firmly occupied the interface layer for capital interaction.

Today, the crypto industry is at a node similar to where neobanks were 5–10 years ago. Over more than a decade of development, crypto has already spawned a series of its own "wedge products":

- Censorship-resistant asset storage via self-custody wallets

- Low-barrier digital dollars via stablecoins

- Permissionless credit markets represented by protocols like Aave

- And 24/7 global capital markets that can even transform internet memes into wealth vehicles

Just as mobile internet infrastructure opened the era of neobanks, programmable blockchains are providing a permissionless financial backend architecture.

The logical next step is to combine these permissionless backend capabilities with neobank-style user-friendly frontends. The first generation of neobanks moved the bank's frontend from physical branches to mobile interfaces while retaining the traditional banking system as the backend. Today's crypto neobanks, conversely, retain the convenient mobile experience but begin to change the underlying path of capital flow: from traditional banking rails to stablecoins and public blockchains.

In other words, if neobanks rebuilt the bank's frontend on top of mobile internet, then crypto technology is offering an opportunity: to rebuild the bank's backend on top of permissionless rails.

The Landscape of Crypto Neobanks

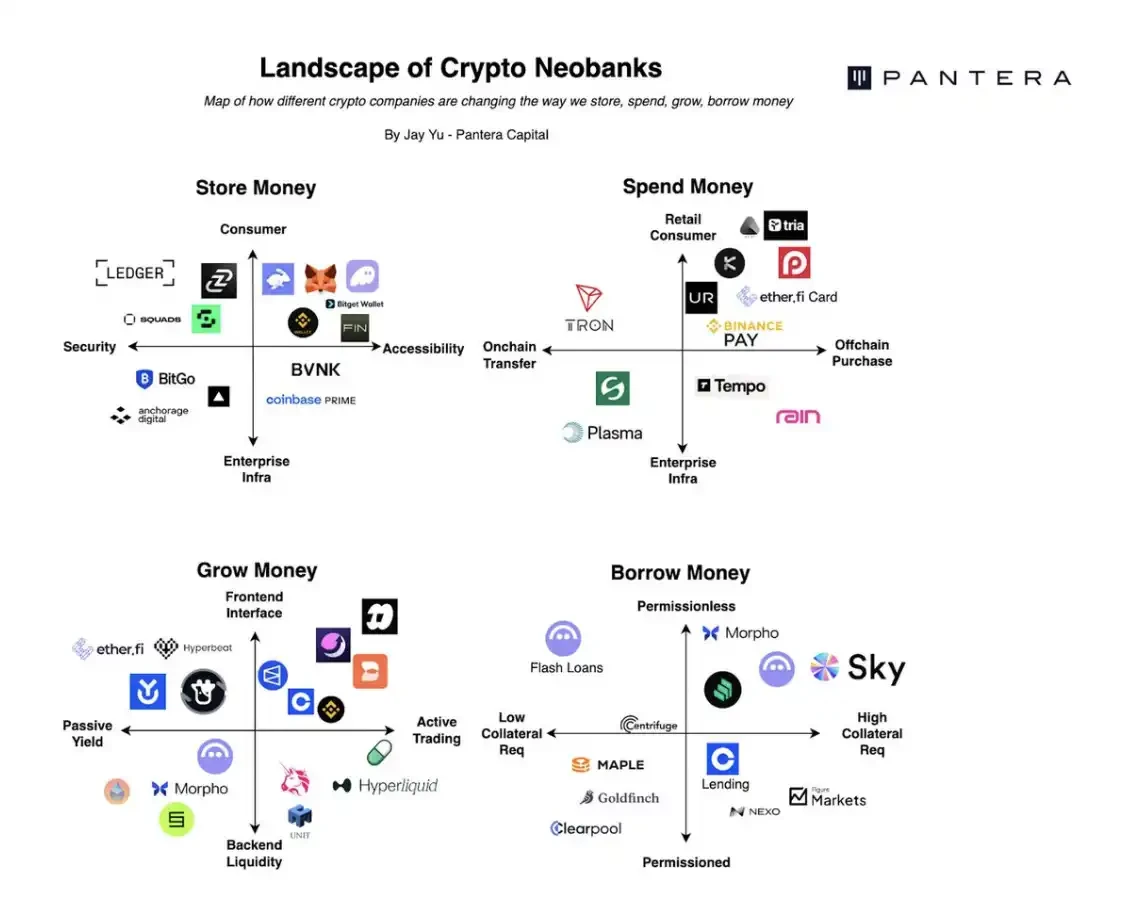

The Landscape of Crypto Neobanks

Today, an increasing number of projects are converging under the vision of "crypto neobanks." We have seen that on permissionless crypto rails, the foundational capabilities surrounding the four financial relationships of store, spend, grow, and borrow are gradually taking shape:

- Self-custody asset storage via hardware wallets like Ledger

- Daily payments via Etherfi cards or Bitget QR codes

- Trading on platforms like Hyperliquid for asset growth

- On-chain borrowing via protocols like Morpho

Simultaneously, numerous supporting participants are bolstering the underlying infrastructure, including: Wallet-as-a-Service, stablecoin settlement systems, compliance licensing services, localized on/off-ramp channel partners, and cross-protocol orchestration routers.

Furthermore, in some cases, crypto exchanges themselves, such as Binance and Coinbase, are already converging towards fintech neobanks, attempting to further capture the core relationship between users and their assets.

For example, Binance Pay provides payment support for over 20 million merchants globally; while Coinbase allows users to automatically earn up to 4% rewards simply by holding USDC on the platform.

In such a complex, multi-layered crypto neobank ecosystem, it is necessary to systematically map this landscape: How are different crypto platforms competing to become users' "primary financial relationship interface"? Which aspects of users' saving, spending, investing, and borrowing are they targeting?

Saving Money the Crypto Way

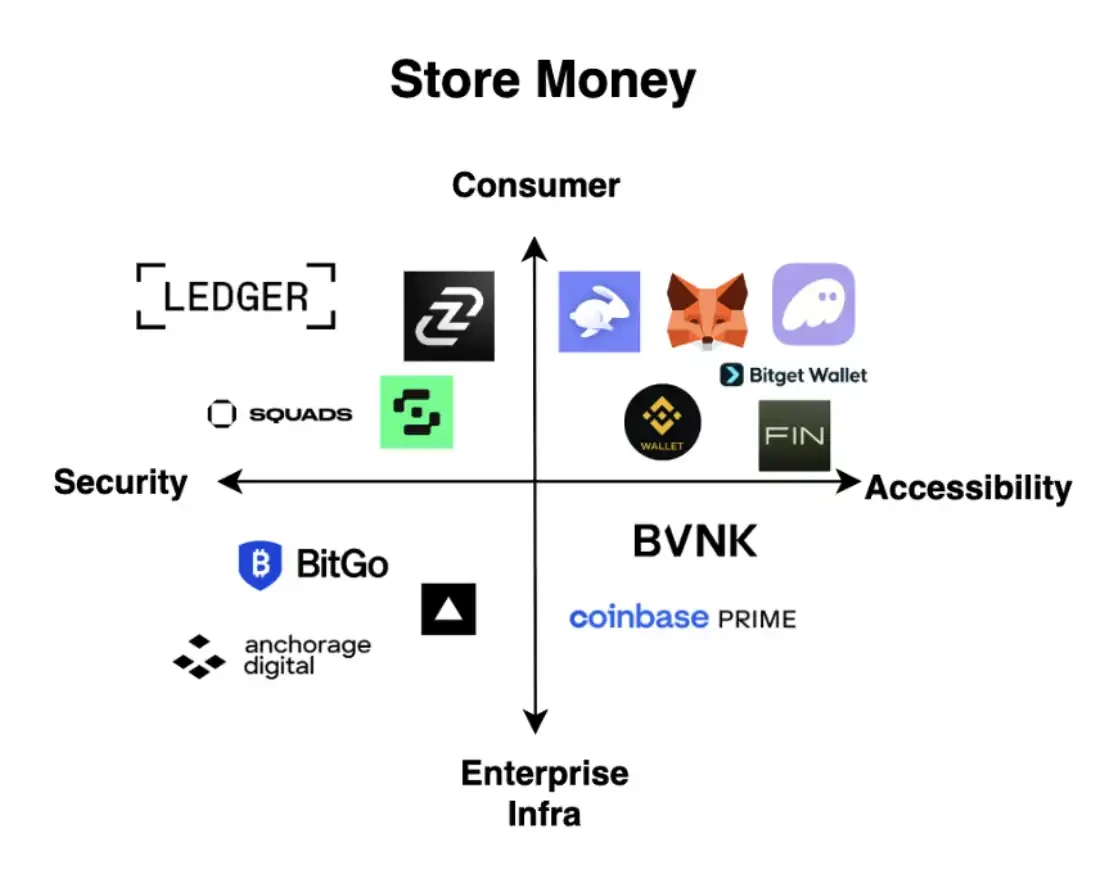

To truly achieve self-custody of crypto assets and interact with blockchains, users must first possess some form of crypto wallet. Roughly, the crypto wallet ecosystem can be divided along two axes: the security ↔ usability spectrum, and the consumer app ↔ enterprise infrastructure spectrum.

Differentiated winners with strong distribution capabilities have emerged across these quadrants:

- Ledger represents secure, consumer-facing hardware wallets;

- Fireblocks and Anchorage provide secure enterprise-grade wallet infrastructure;

- MetaMask, Phantom, and Privy are consumer-facing wallets focused on enhancing usability and user experience;

Turnkey and Coinbase Prime occupy more of the "high accessibility + enterprise-grade" infrastructure positions.

The core advantage of building a neobank with a wallet app as the beachhead is that the wallet frontend—like MetaMask and Phantom—often controls the entry layer for user interaction with crypto assets. The so-called "fat wallet thesis" posits that the wallet layer captures the vast majority of consumer-facing distribution power and order flow, and the cost for end-users to switch wallets is extremely high.

Indeed: Currently, about 35% of Solana transaction volume is processed through the Phantom wallet. This moat formed by excellent mobile experience and user stickiness is substantial.

Moreover, as consumers (especially retail) often prioritize convenience over price, wallets like Phantom and MetaMask can command take rates as high as 0.85%; in comparison, swap protocols like Uniswap might charge only 0.3% per token exchange.

However, on the other hand, building a complete, profitable neobank solely on a single wallet platform is surprisingly difficult. The reason is: to achieve profitable scale, users must not only "store" tokens but also frequently use those tokens within the wallet.

Phantom, MetaMask, and Ledger may have household brand recognition, but if users treat crypto wallets merely as "cash shoeboxes under the bed," they can hardly monetize. In other words, wallets must transform into active trading and payment platforms to convert distribution advantages into revenue.

MetaMask and Phantom are clearly moving in this direction.

For example, MetaMask recently launched the MetaMask Card, attempting to monetize its existing crypto-native user base and become the default solution for "spending crypto." Phantom has followed suit by launching Phantom Cash and further entering the "grow money" space—by integrating Hyperliquid's builder codes to offer perpetual contract trading within the app.

As Blockworks stated: "While Drift or Jupiter might be Solana's native darlings, the real money has flowed to Hyperliquid."

This is a universally applicable lesson for the entire wallet sector: you must not only control the user's wallet itself but also control the scale of capital flowing in and out of the wallet through actions like 'spend, grow, borrow.'

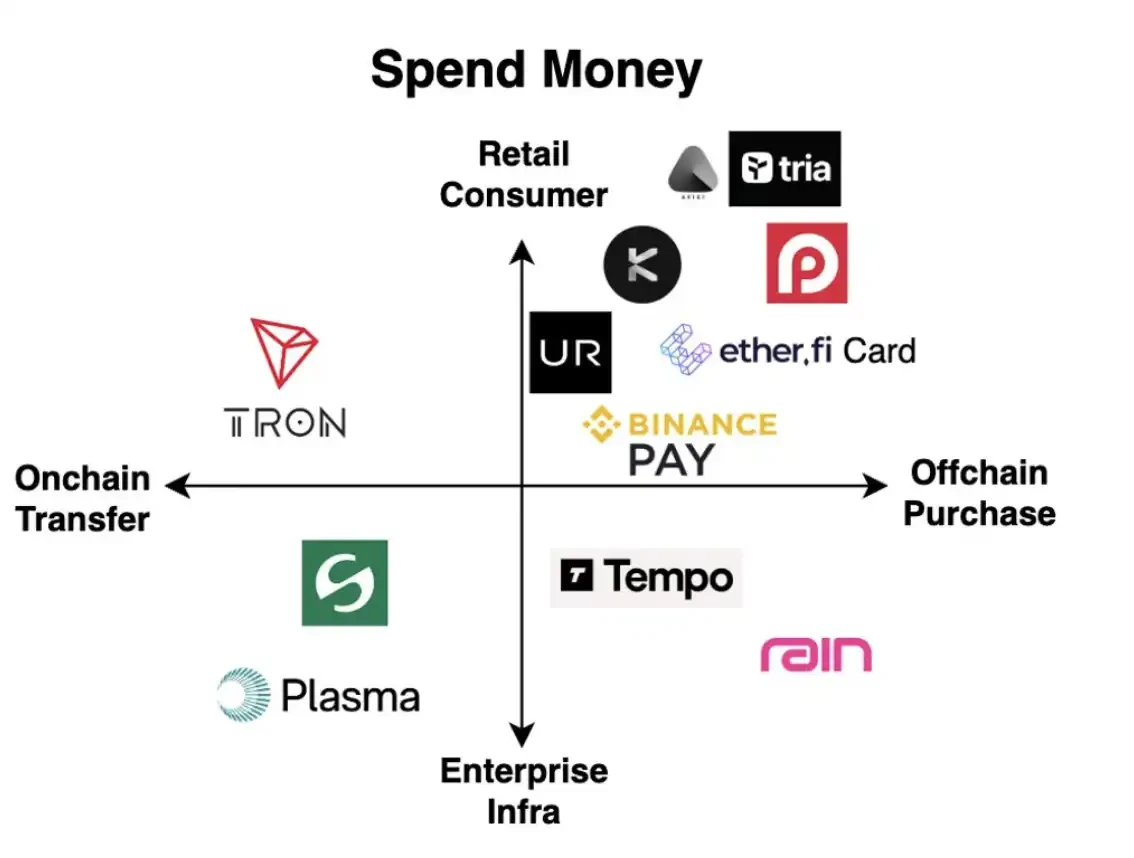

Spending Money the Crypto Way

The second category of competitors for crypto neobanks are platforms that enable users to spend cryptocurrency.

Similar to "saving money the crypto way," we can also categorize "spending money the crypto way" applications along two dimensions: from on-chain transfers to off-chain consumption (e.g., buying a coffee); and from retail consumer-facing apps to enterprise infrastructure.

Interestingly, many "neobank" projects that have gained market attention in recent months—such as Kast, Tria, Tempo, Stable—almost all target the "spending crypto" wedge. Market enthusiasm is particularly concentrated in two major directions:

Retail consumer-facing apps integrating stablecoin cards, such as Avici, Tria, Redotpay, EtherFi;

Enterprise-focused "stablecoin chains" or "stablecoin infrastructure," such as Stable, Plasma, Tempo.

Retail Side: Making Crypto Apps More Like Banks

The first category of retail-facing "payment-first apps" essentially makes crypto apps increasingly resemble traditional banks or fintech neobanks at the user experience level: familiar interface tabs like "Home, Banking, Card, Invest" are all present.

With the maturation of crypto card issuers like Rain and Reap, and the expansion of Visa and Mastercard's support for stablecoins, crypto cards themselves have gradually become commoditized. The real differentiation lies not in "issuing a card," but in the ability to consistently drive and retain transaction volume—whether through innovative cashback mechanisms, localized merchant acquisition capabilities, or onboarding non-crypto-native users onto the platform.

This trajectory closely resembles the rise of fintech neobanks: success was never just about "issuing cards" or "building an app," but about capturing a specific user segment, from students (SoFi), to low-income families (Chime), to international travelers (Wise and Revolut), and building trust, loyalty, and scaled transaction volume on that foundation.

If executed correctly, these "payment-first" crypto neobanks could become significant entry points driving mass adoption of blockchain infrastructure.

Furthermore, crypto neobanks may also guide users towards a new generation of payment systems that go beyond traditional card rails.

Card-based spending might be just a transitional phase—it still relies on Visa and Mastercard's clearing networks and inherits their centralized constraints. New signals are emerging: for example, Bitget Wallet has launched QR-code-based stablecoin payment pilots in Indonesia, Brazil, and Vietnam. This points to a potential future where crypto-native settlement systems could completely bypass traditional card issuers.

Enterprise Side: Stablecoin Infrastructure & "Stablecoin Chains"

The second category of recently emerging "neobank" applications are stablecoin infrastructure projects built for enterprises, including Stable, Plasma, Tempo, Arc, often referred to as "stablecoin chains."

An important backdrop for their rise is the increasing demand from institutional players—traditional banks, fintech companies like Stripe, and existing payment networks—for more efficient capital rails.

These "stablecoin chains" often share similar characteristics:

- Using stablecoins as Gas tokens to avoid fee volatility from custom Gas token price fluctuations

- Streamlined consensus mechanisms to accelerate high-frequency, high-value payments from A to B

- Enhanced transfer privacy via Trusted Execution Environments (TEE)

- Custom data fields to accommodate international payment standards like ISO 20022

However, technical improvements alone do not guarantee adoption.

For payment-focused blockchains, the real moat is merchants. The key question is how many merchants and businesses are willing to migrate their operations to a specific chain.

For instance, Tempo attempts to leverage Stripe's vast merchant base and payment network to drive transaction volume and adoption [12], onboarding a new cohort of merchants onto crypto rails. Other chains, like Plasma and Stable, aim to become "first-class citizens" for Tether USDT, strengthening the role of stablecoins in inter-institutional flows.

In this space, the most instructive case study is Tron. It processes about 25–30% of global stablecoin transaction volume.

Tron's rise is largely attributed to its strength in emerging markets—such as Nigeria, Argentina, Brazil, and Southeast Asia. With low fees, fast confirmations, and global reach, Tron has become a common settlement layer for merchant payments, cross-border remittances, and USD-denominated savings accounts.

For all emerging payment-focused blockchains, Tron is an incumbent competitor that must be confronted. Challenging it requires a 10x improvement on a base that is already "cheap, fast, and global"—which often means focusing on merchant acquisition and network scale expansion rather than marginal technical optimizations.

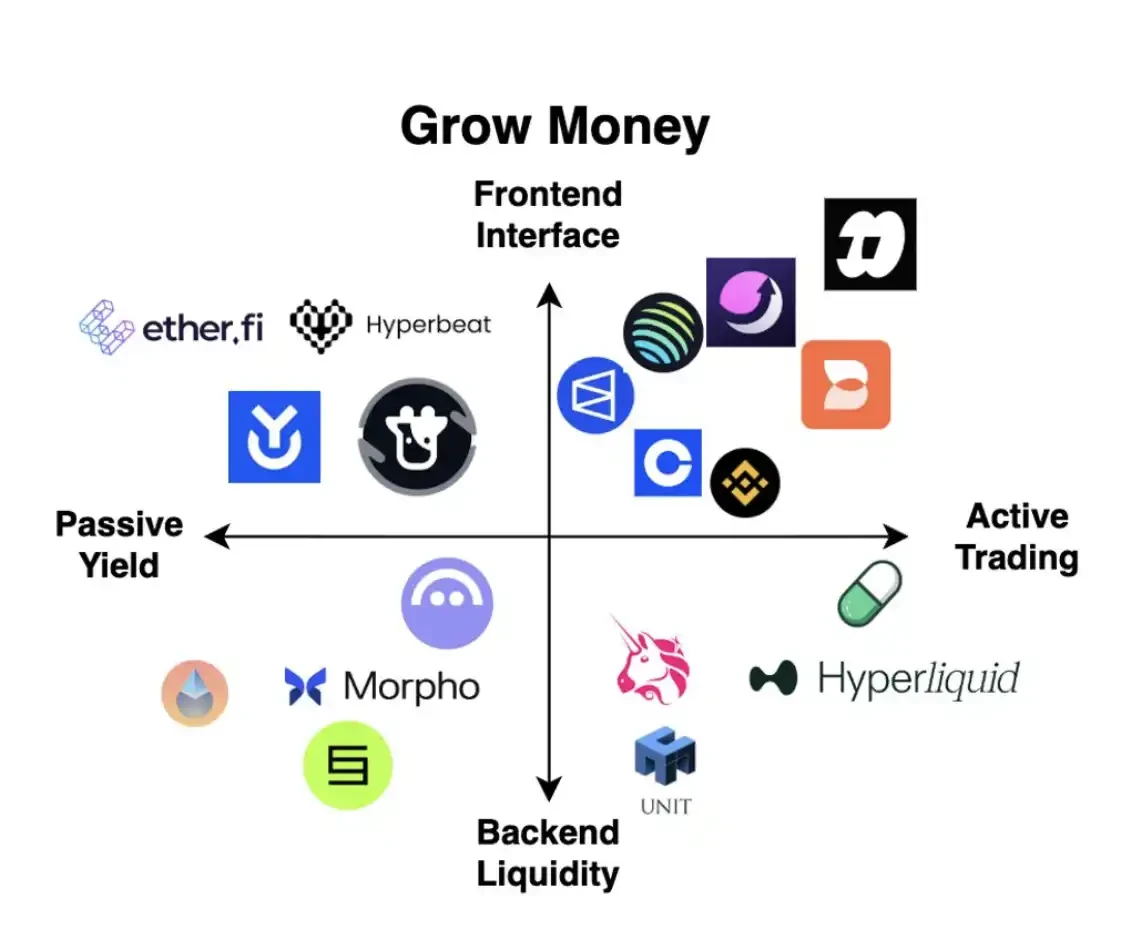

Growing Money the Crypto Way

The third relationship crypto neobanks establish with users is helping them grow their money. This is one of the most innovation-dense sectors in crypto, spawning multiple 0-to-1 financial primitives—from staking vaults and perpetual contract trading to token launch platforms and prediction markets. Similar to before, we can also categorize "grow money" applications along two dimensions: from passive yield to active trading, and from frontend interface to backend liquidity.

A classic example of a "grow money" application evolving into a full-fledged neobank comes from centralized crypto exchanges (CEXs) like Binance or Coinbase. Exchanges initially offered a simple yet effective value proposition—"this is where you grow your wealth by trading crypto assets." As trading volume continued to climb, exchanges gradually became core venues not only for growing but also for storing and managing assets.

Both Coinbase and Binance have launched their own blockchains, wallets, institutional products, and crypto cards, monetizing their core user bases through new products and network effects. For example, Binance Pay's adoption continues to rise, with more merchants using it to accept crypto payments for everyday goods.

The same path has been validated in DeFi projects. Take EtherFi as an example: it started as a liquid staking protocol for Ethereum, providing passive yield for users restaking ETH to EigenLayer. Subsequently, EtherFi launched a DeFi strategy vault called "Liquid," allocating user funds across the DeFi ecosystem to pursue higher yields under controlled risk. The project then expanded to EtherFi Cash—a groundbreaking card product enabling users to directly spend their EtherFi balances in the real world.

This expansion path closely resembles that of fintech neobanks: establishing a foothold through a unique product wedge (passive staking and yield), achieving scale by becoming the "best solution" in a niche, and then horizontally expanding the product matrix to monetize existing users (e.g., EtherFi Card).

To date, the crypto space has already birthed multiple 0→1 innovations supporting users' "grow money" needs: platforms like Hyperliquid for perpetual contracts have grown into some of the most profitable crypto companies; prediction markets like Polymarket are gradually entering the mainstream. It is highly likely that the next step for these platforms is also monetization through new product forms—enabling users to store more, spend more on the platform, leveraging network scale effects.

Starting as a "grow money platform," especially an active trading platform, has a distinct advantage: high trading frequency and transaction volume. For instance, Hyperliquid has processed $3 trillion in trading volume over the past 18 months. Compared to "save money platforms" and "pay money platforms," "g