BTC Breaks Through $97,000, Crypto Market Stands at a New Structural Inflection Point

- Core View: The crypto market is at a critical inflection point of structural change; its rebound requires meeting more complex conditions rather than simply relying on historical cycle patterns.

- Key Factors:

- Positive signals emerge in capital flows. BTC spot ETFs have shifted from consecutive outflows to two consecutive days of net inflows, with a single-day net inflow reaching as high as $750 million on January 13th.

- The macro landscape lacks short-term easing catalysts. December CPI data was moderate, but inflation remains sticky, and the market widely expects the Fed to keep rates unchanged in January.

- Regulatory legislation enters a critical stage. The CLARITY Act is under review in the Senate, but public opposition from institutions like Coinbase highlights internal industry divisions.

- Market structure has changed. BTC has not shown typical four-year cycle strength in 2025, the altcoin cycle has nearly vanished, and capital is highly concentrated in top-tier assets.

- A future rebound requires meeting multiple conditions, including an expanded ETF configuration scope, sustained price increases in core assets to create a wealth effect, and a large-scale return of retail investor attention.

Original | Odaily (@OdailyChina)

Author | DingDang (@XiaMiPP)

Following yesterday's strong breakout above the key resistance level of $95,000, BTC continued its upward momentum in the early hours of today, reaching a high of $97,924. It is currently trading at around $96,484. ETH broke through $3,400 and is now around $3,330. SOL rose to a high of $148 and is currently around $145. Compared to BTC, ETH and SOL are still hovering around key resistance zones, without forming a clear trend breakout.

In the derivatives market, according to Coinglass data, total liquidations across all exchanges reached $680 million yesterday, with short liquidations at $578 million and long liquidations at $101 million. Glassnode noted that the market rebound led to short liquidations reaching their highest level since the "October 11 crash."

According to msx.com data, while the three major U.S. stock indices closed lower, crypto-related stocks generally rose, with ALTS up over 30.94% and BNC up over 11.81%. This situation is not common. What is driving such a strong rally in the crypto market?

ETF Fund Flow Shift

On the capital front, since mid-October 2025, the overall trend for spot Bitcoin ETFs has been net outflows or weak small-scale net inflows, lacking clear signals of incremental capital. However, after four consecutive trading days of net outflows last week, spot Bitcoin ETFs have seen two consecutive days of net inflows. Notably, the net inflow on January 13 alone reached $750 million, serving as a significant signal for this phase. In contrast, spot Ethereum ETFs continue to show weakness.

From a price action perspective, a noteworthy change is occurring. Bitcoin's cumulative return during North American trading hours is approximately 8%, while the European session recorded only a modest gain of about 3%, and the Asian session even dragged down the overall performance.

This phenomenon stands in stark contrast to the end of 2025. Back then, Bitcoin accumulated a decline of up to 20% during North American hours, with prices once falling back to around $80,000. In the fourth quarter, the U.S. market open often coincided with selling pressure, and spot Bitcoin ETFs faced almost daily outflows.

Now, the strongest returns are occurring shortly after the U.S. stock market opens, which was precisely the period of Bitcoin's weakest performance over the past six months.

Macro Data: No Bad News, But Lacking Easing Catalysts

On the macro front, the December CPI released this week showed a year-over-year rate of 2.7% (unchanged from the previous reading, meeting market expectations), while the core CPI year-over-year rate edged up to 2.7% (previous 2.6%, slightly above some expectations), indicating inflation pressure remains somewhat sticky. However, the November PPI year-over-year unexpectedly rose to 3.0% (higher than the expected 2.7%), and retail sales month-over-month also recorded strong growth (exceeding market expectations), showing robust consumer data. This supports the view that economic growth remains resilient.

Although the December CPI data was generally moderate (month-over-month 0.3% met expectations, year-over-year rate did not accelerate further), inflation has not clearly fallen back to the Federal Reserve's comfort zone. Combined with the labor market resilience shown in previous employment reports, the market widely believes the probability of the Fed maintaining interest rates unchanged at the end-of-January FOMC meeting is extremely high, with almost no expectation of a rate cut. This also means catalysts for policy easing remain scarce in the short term. According to CME's "FedWatch Tool," the probability of the Fed holding rates steady in January is 95%.

However, rate cut expectations for 2026 are worth anticipating, with Fed Governor Mester reiterating the need for 150 basis points of cuts this year.

Regulatory/Legislative Progress: CLARITY Act in Focus

Beyond short-term price action, the most significant mid-to-long-term variable recently is the legislative progress of the CLARITY Act. This bill aims to establish a comprehensive regulatory framework for the U.S. crypto market, with main objectives including:

- Clarifying the regulatory boundaries between the SEC (for securities-like assets) and the CFTC (for commodity-like digital assets);

- Defining digital asset classifications (securities, commodities, stablecoins, etc.);

- Introducing stricter requirements for disclosure, anti-money laundering, and investor protection, while leaving room for innovation.

With the Senate Banking Committee's revised text and vote scheduled for January 15, U.S. crypto legislation has officially entered the "final sprint." Committee Chairman Tim Scott (Republican) released the 278-page revised text on January 13. This text followed months of bipartisan closed-door negotiations and quickly sparked over 70 (some counts say 137) proposed amendments. Disagreements over stablecoin yields and DeFi regulation intensified rapidly, with the crypto industry, banking lobbyists, and consumer protection groups all heavily involved.

Furthermore, the crypto industry itself is not unified in its stance. On January 14, Coinbase CEO Brian Armstrong publicly announced the withdrawal of support, stating that after reviewing the text, he believed the bill had "too many problems regarding DeFi bans, stifling stablecoin reward mechanisms, and excessive government surveillance, making it worse than the status quo." He emphasized that Stand With Crypto would score the Thursday amendment vote, testing whether senators "stand with bank profits or consumer/innovation rewards." Industry insiders believe Coinbase's public opposition is "significant" and could sway the bill's fate.

Following Coinbase's public opposition, several leading institutions and associations including a16z, Circle, Kraken, Digital Chamber, Ripple, and Coin Center publicly expressed support for the Senate Republican version, arguing that "any clear rules are better than the status quo," would inject long-term certainty into the market, and position the U.S. as the "global crypto capital." (Recommended reading: CLARITY Act Review Suddenly Postponed, Why Is Industry Divergence So Severe?)

Other Observations: Strong Ethereum Staking Demand & Strategy Continues Accumulation

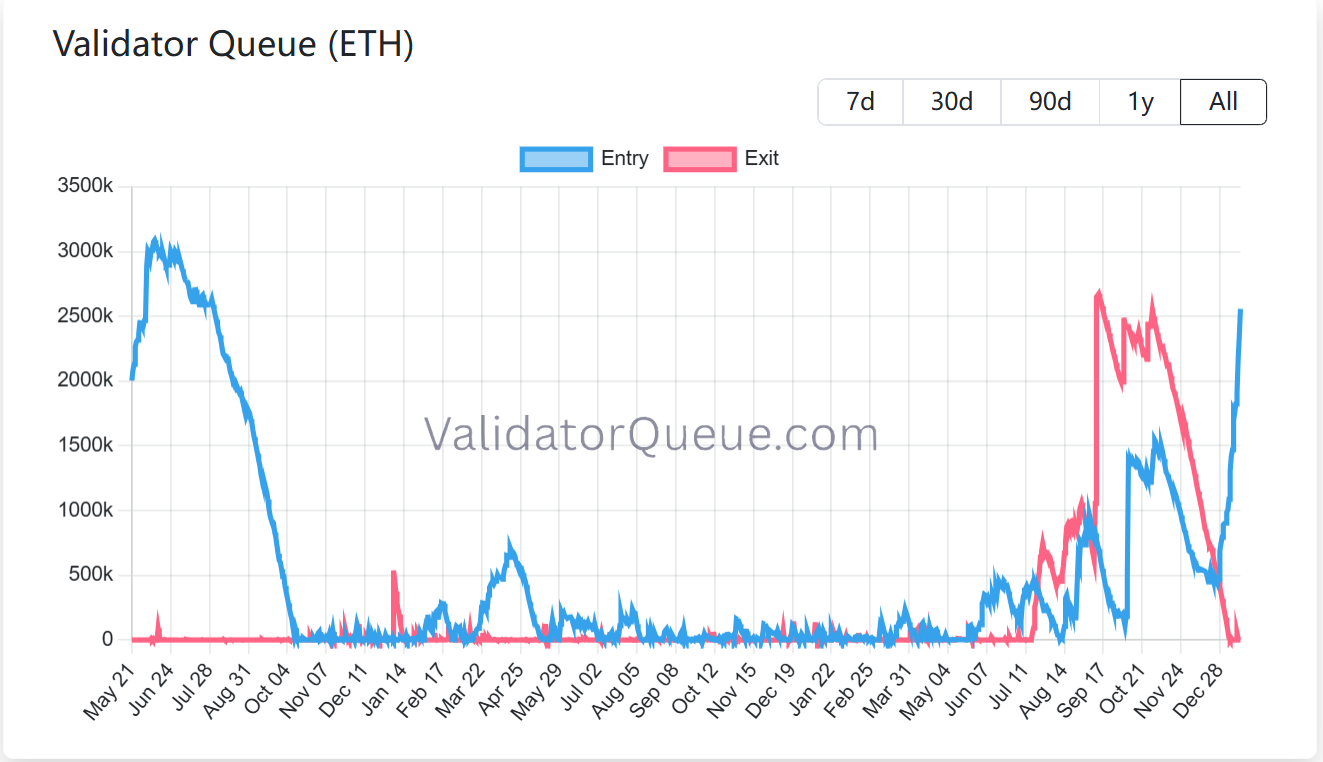

Ethereum staking demand continues to strengthen. Currently, the amount of ETH locked in the Beacon Chain has exceeded 36 million, accounting for nearly 30% of the network's circulating supply, with a corresponding staking market value exceeding $118 billion, continuously setting new historical highs. The previous peak share was 29.54%, recorded in July 2025. The Ethereum network currently has about 900,000 active validators, with approximately 2.55 million ETH still queued waiting to enter the staking queue. This means, at least from on-chain behavior, existing stakers' short-term selling意愿 remains limited, and the network overall leans more towards "locking rather than releasing."

In addition, developer activity and stablecoin transaction volume on Ethereum have both hit record highs. Recommended reading: ETH Staking Data Reversal: Exits Cleared vs. Entries Surge 1.3 Million, When to Buy the Dip?

Bitcoin reserve company Strategy (formerly MicroStrategy) continued its long-term accumulation strategy this week, spending approximately $1.25 billion to purchase 13,627 BTC at an average price of about $91,519. Consequently, its total Bitcoin holdings have increased to 687,410 BTC, valued at approximately $65.89 billion, with an overall average cost basis of about $75,353 per BTC.

Investment bank TD Cowen recently lowered its one-year price target for Strategy from $500 to $440, citing dilution effects from continued issuance of common and preferred stock, which weakens Bitcoin yield expectations. Analysts expect Strategy to acquire approximately 155,000 more Bitcoin in fiscal year 2026, higher than previous forecasts, but a higher proportion of equity financing will reduce the Bitcoin-per-share growth.

TD Cowen also noted that despite short-term yield pressure, related metrics are expected to improve in fiscal year 2027 as Bitcoin prices recover. The report also emphasized that Strategy's choice to continue accumulating during recent Bitcoin price pullbacks, with most financing proceeds directly used to purchase Bitcoin, shows its strategic objectives remain firm. Overall, analysts remain relatively positive on Strategy's long-term value as a "Bitcoin exposure tool" and believe some of its preferred shares offer attractiveness in terms of yield and capital appreciation. Regarding index inclusion, MSCI has not yet removed Bitcoin reserve companies from its index system, which is seen as a positive factor in the short term, but uncertainty remains in the medium to long term.

Arthur Hayes also stated that his core trading strategy for this quarter is going long on Strategy (MSTR) and Metaplanet (3350), using them as leveraged bets on BTC resuming its upward trend.

Market Outlook: Structural Changes & Conditions for a Rebound

In summary, the crypto market stands at a critical inflection point. Whether the traditional "four-year cycle" remains valid will likely be revealed in the coming months.

In its latest digital asset OTC market review, crypto market maker Wintermute analyzed: In 2025, Bitcoin did not exhibit the strong characteristics typical of a four-year cycle, and the altcoin cycle almost disappeared. In their view, this phenomenon is not a short-term fluctuation or timing misalignment but a deeper structural change.

Under this premise, Wintermute believes that for a truly strong rebound to occur in 2026, the triggering conditions will be significantly higher than in previous cycles and will no longer rely on a single variable. Specifically, at least one of the following three outcomes needs to materialize.

First, the allocation scope of ETFs and crypto treasury (DAT) companies must expand beyond Bitcoin and Ethereum. Currently, U.S. spot BTC and ETH ETFs objectively concentrate a large amount of new liquidity onto a few large-cap assets. While this enhances the stability of top assets, it also significantly compresses market breadth, leading to severe performance divergence. Only when more crypto assets are included in ETF products or corporate balance sheets can the market potentially regain broader participation and a liquidity foundation.

Second, core assets like BTC, ETH, as well as BNB and SOL, need to experience sustained strong rallies again, recreating sufficiently明显的 wealth effects. In 2025, the traditional transmission mechanism of "Bitcoin rising — funds flowing into altcoins" largely failed. The average uptrend周期 for altcoins was compressed to about 20 days (compared to about 60 days the previous year), with many tokens weakening under unlock selling pressure. Without sustained rallies in top assets, funds lack the动力 to溢出 downward, making it naturally difficult to activate an altcoin行情.

Third, and most decisive, retail attention needs to genuinely return to the crypto market. Although retail has not completely left, their new capital is currently flowing more towards high-growth themes like the S&P 500, AI, robotics, and quantum computing. The memory of extreme drawdowns in 2022-2023, platform bankruptcies, and liquidations, combined with the reality of crypto assets underperforming traditional stocks in 2025, has significantly weakened the narrative吸引力 of "crypto = getting rich quick." Only when retail重新相信 the crypto market has the potential for超额回报 and returns in a规模化 manner can the market potentially regain the highly emotional,近乎狂热 upward momentum of the past.

In other words, against the backdrop of structural changes already occurring, the future rebound is no longer a question of "if it will come," but rather "under what conditions and through which path it will be reignited."