Decoding the CoinShares 2026 Report: Saying Goodbye to Speculative Narratives and Embracing the Year of Practicality

- 核心观点:数字资产转向实用价值驱动。

- 关键要素:

- 比特币ETF等推动主流化进程。

- 稳定币、RWA等混合金融崛起。

- 监管框架(如MiCA)提供清晰度。

- 市场影响:加速行业成熟与机构采用。

- 时效性标注:中期影响。

Original author: CoinShares

English translation: Deep Tide TechFlow

As the year draws to a close, various organizations release their annual review and outlook reports.

Adhering to the principle of "don't read too long," we also tried to quickly summarize and extract the key points from each company's long reports.

This report comes from CoinShare, a leading European digital asset investment management company founded in 2014, headquartered in London, UK and Paris, France, with assets under management exceeding $6 billion.

This 77-page report, "Outlook 2026: The Year Utility Wins," covers core topics such as macroeconomic fundamentals, Bitcoin mainstreaming, the rise of hybrid finance, competition among smart contract platforms, and the evolution of the regulatory landscape. It also provides in-depth analysis of sub-sectors such as stablecoins, tokenized assets, prediction markets, mining transformation, and venture capital.

The following is a summary and distillation of the core content of this report:

I. Core Theme: The Arrival of the Year of Practicality

2025 will be a turning point for the digital asset industry, with Bitcoin hitting a record high and the industry shifting from speculation-driven to value-driven.

2026 is expected to be the "utility wins" year, with digital assets no longer attempting to replace the traditional financial system, but rather to enhance and modernize the existing system.

The report's core argument is that 2025 marks a decisive shift in digital assets from speculative to value-driven growth, and 2026 will be a crucial year for accelerating this transformation.

Digital assets are no longer attempting to establish a parallel financial system, but rather to enhance and modernize the existing traditional financial system. The integration of public blockchains, institutional liquidity, regulatory market structures, and real-world economic use cases is progressing at a pace exceeding optimistic expectations.

II. Macroeconomic Foundation and Market Outlook

Economic Environment: A Soft Landing on Thin Ice

Growth Outlook: The economy may avoid recession in 2026, but growth will be weak and fragile. Inflation continues to ease but not decisively, with tariff disruptions and supply chain restructuring keeping core inflation at levels not seen since the early 1990s.

Federal Reserve policy: Cautious rate cuts are expected, with the target rate potentially falling to the mid-3% range, but the process will be slow. The Fed is still fresh in the memory of the 2022 inflation surge and is unwilling to shift course quickly.

Three scenarios for analysis:

- Optimistic Scenario: Soft landing + productivity surprises could see Bitcoin break $150,000

- Baseline scenario: Slow expansion, Bitcoin trading range of $110,000-$140,000

- Bear Market Scenario: Recession or stagflation could see Bitcoin fall to the $70,000-$100,000 range.

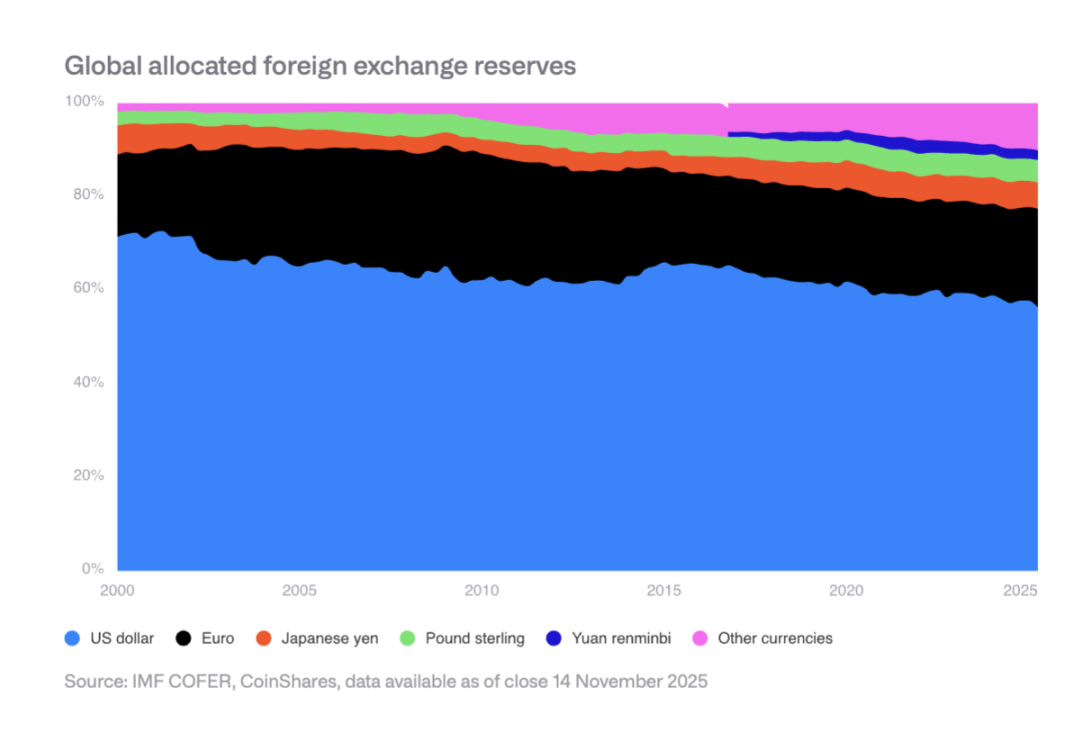

The slow erosion of the dollar's reserve status

The US dollar's share of global foreign exchange reserves has fallen from 70% in 2000 to around 50% currently. Emerging market central banks are diversifying their holdings, increasing their reserves of assets such as the renminbi and gold. This creates a structural advantage for Bitcoin as a non-sovereign store of value.

III. The Mainstreaming Process of Bitcoin in the United States

The United States achieved several key breakthroughs by 2025, including:

- Spot ETFs approved and launched

- The formation of a top-tier ETF options market

- Retirement plan restrictions lifted

- Application of Fair Value Accounting Rules

- The US government has designated Bitcoin as a strategic reserve.

Institutional adoption is still in its early stages

Although structural barriers have been removed, practical adoption remains constrained by traditional financial processes and intermediaries. Wealth management channels, retirement plan providers, and corporate compliance teams are still gradually adapting.

2026 forecast

Key progress is expected in the private sector: the four major brokerages will open up Bitcoin ETF allocations, at least one major 401(k) provider will allow Bitcoin allocations, at least two S&P 500 companies will hold Bitcoin, and at least two major custodian banks will offer direct custody services.

IV. Risks of Miners and Enterprises Holding Coins

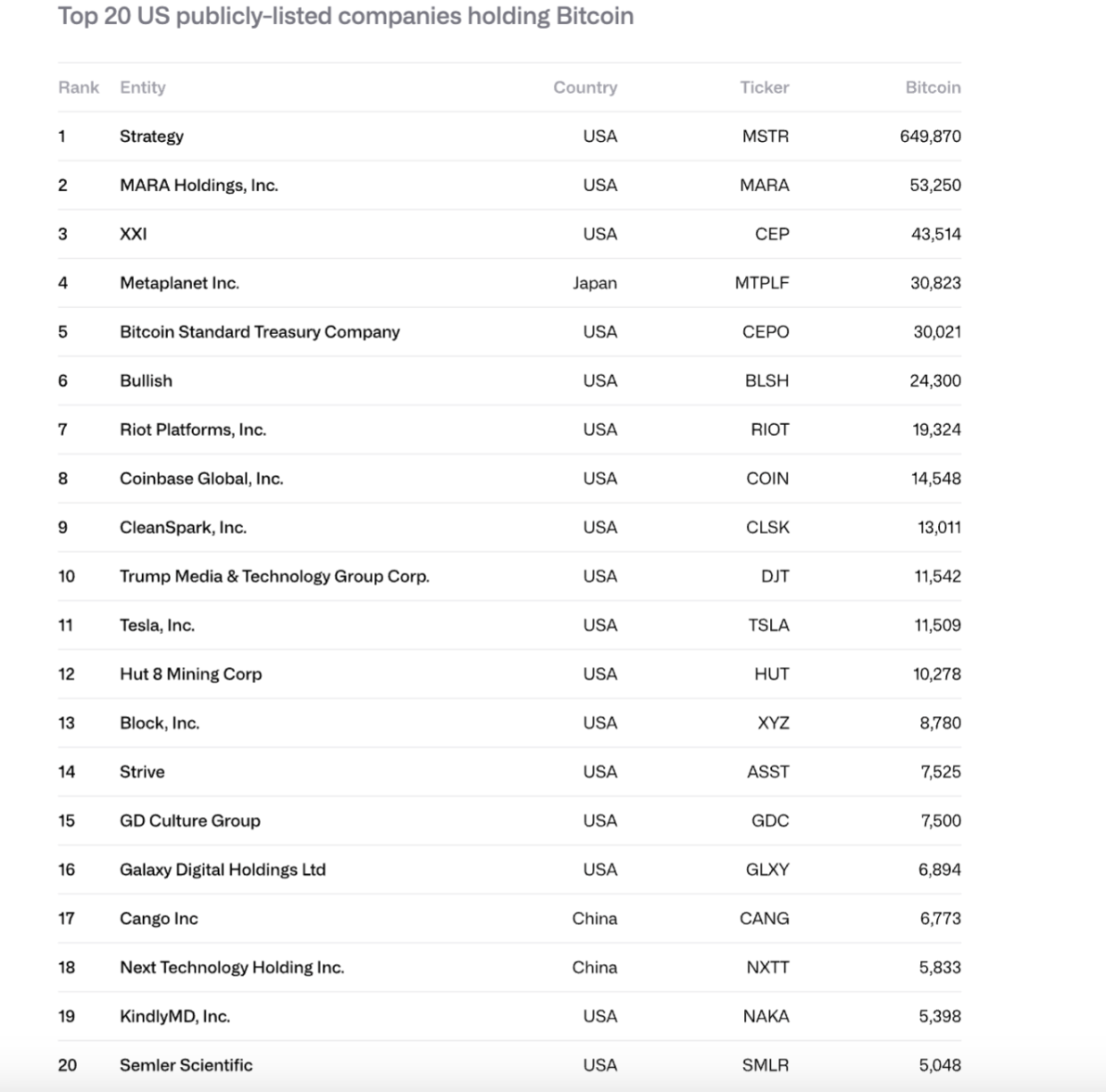

Corporate holdings surge

Between 2024 and 2025, the amount of Bitcoin held by publicly traded companies increased from 266,000 to 1,048,000, with a total value rising from $11.7 billion to $90.7 billion. Strategy (MSTR) held 61% of the total, and the top 10 companies controlled 84%.

Potential sell-off risk

Strategy faces two major risks:

- Unable to fund perpetual debt and cash flow obligations (annual cash flow of nearly $680 million).

- Refinancing risk (the most recent bond maturing in September 2028)

If mNAV approaches 1x or cannot be refinanced at zero interest rates, it may be forced to sell Bitcoin, triggering a vicious cycle.

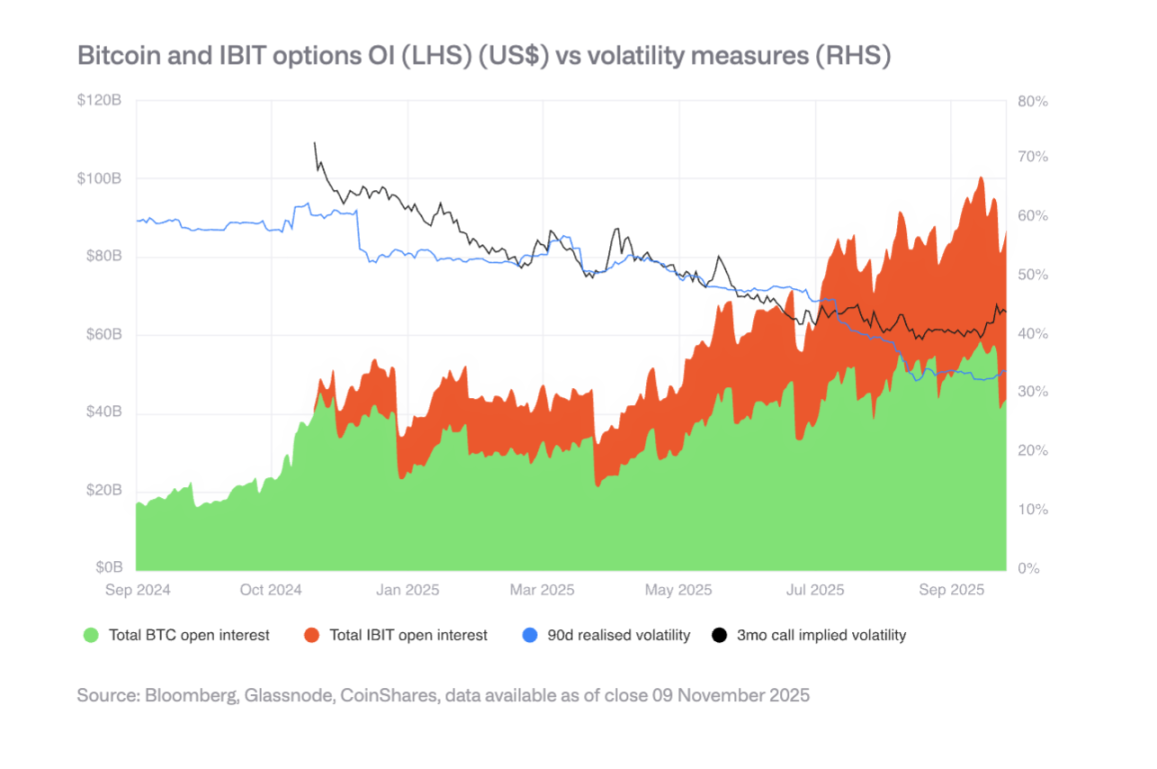

Options Market and Declining Volatility

The development of the IBIT options market has reduced Bitcoin volatility, a sign of maturity. However, decreased volatility may weaken demand for convertible bonds, impacting corporate purchasing power. A turning point in volatility decline was anticipated in the spring of 2025.

V. Differentiation in the Regulatory Landscape

EU: Clarity of MiCA

The EU possesses the world's most comprehensive legal framework for crypto assets, covering issuance, custody, trading, and stablecoins. However, harmonization limitations were exposed in 2025, and regulators in some countries may challenge the cross-border access permit.

United States: Innovation and Fragmentation

The US has regained momentum thanks to its deepest capital markets and mature venture capital ecosystem, but regulation remains fragmented across multiple agencies, including the SEC, CFTC, and the Federal Reserve. Stablecoin legislation (the GENIUS Act) has been passed, but its implementation is still underway.

Asia: Moving towards prudent regulation

Hong Kong, Japan, and other regions are advancing Basel III requirements for crypto capital and liquidity, while Singapore maintains its risk-based licensing regime. A more coherent regulatory group is emerging in Asia, converging around risk-based and bank alignment standards.

The Rise of Hybrid Finance

Infrastructure and settlement layer

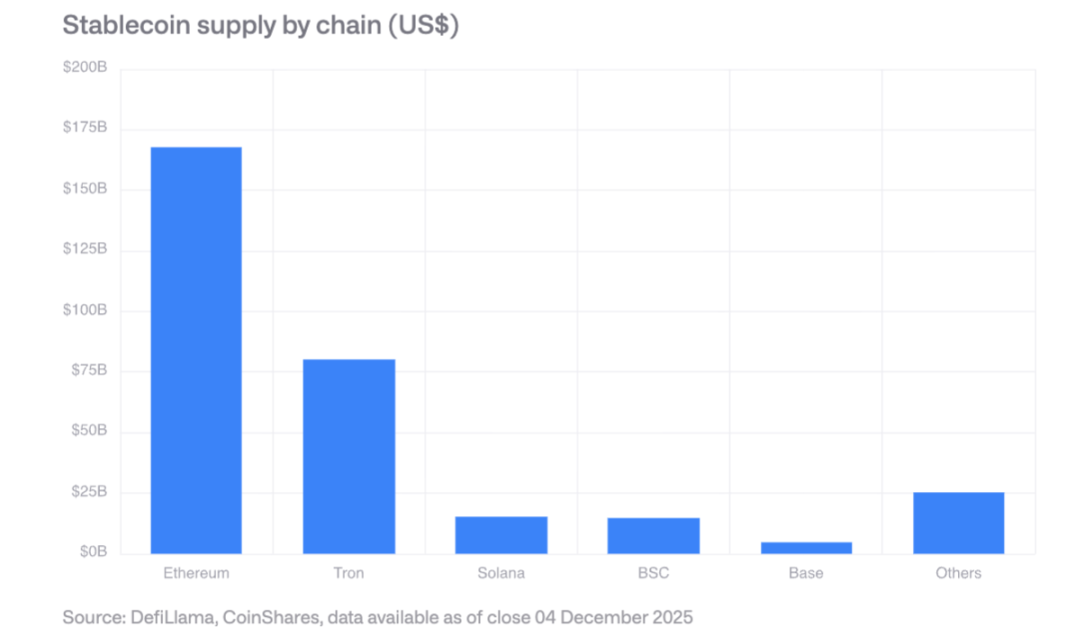

Stablecoins: The market size exceeds $300 billion, with Ethereum holding the largest share and Solana experiencing the fastest growth. The GENIUS Act requires compliant issuers to hold U.S. Treasury reserves, creating new demand for Treasury securities.

Decentralized exchanges: monthly trading volume exceeds $600 billion, with Solana processing $40 billion in trading volume per day.

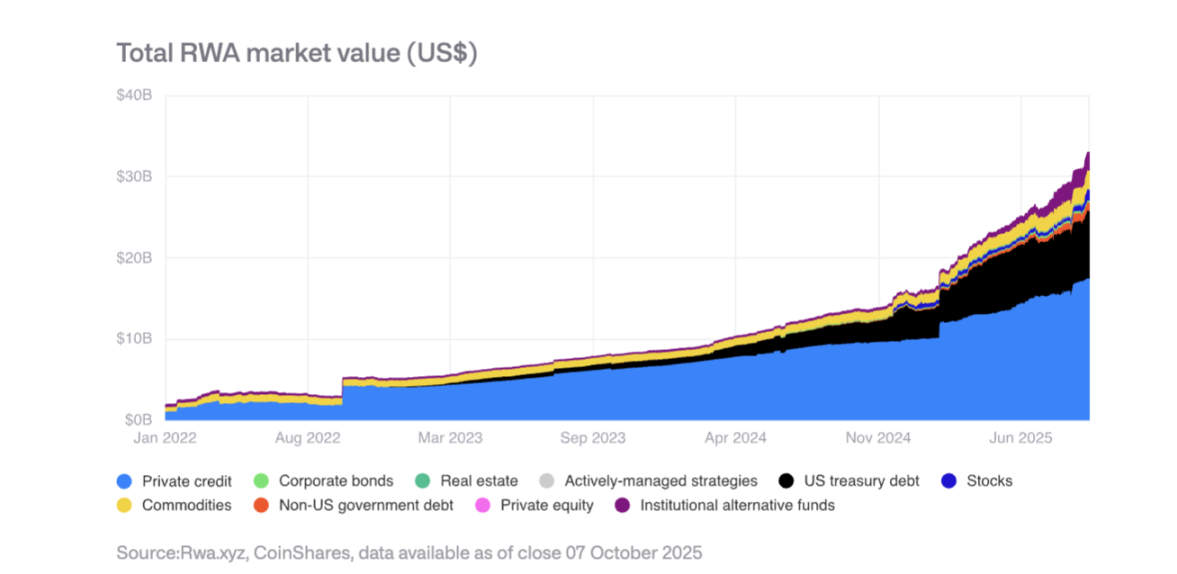

Tokenization of Real-World Assets (RWA)

The total value of tokenized assets is expected to grow from $15 billion at the beginning of 2025 to $35 billion. Private lending and U.S. Treasury tokenization saw the fastest growth, while gold tokens exceeded $1.3 billion. BlackRock's BUIDL fund assets expanded significantly, and JPMorgan Chase launched the JPMD tokenized deposit on Base.

On-chain applications that generate revenue

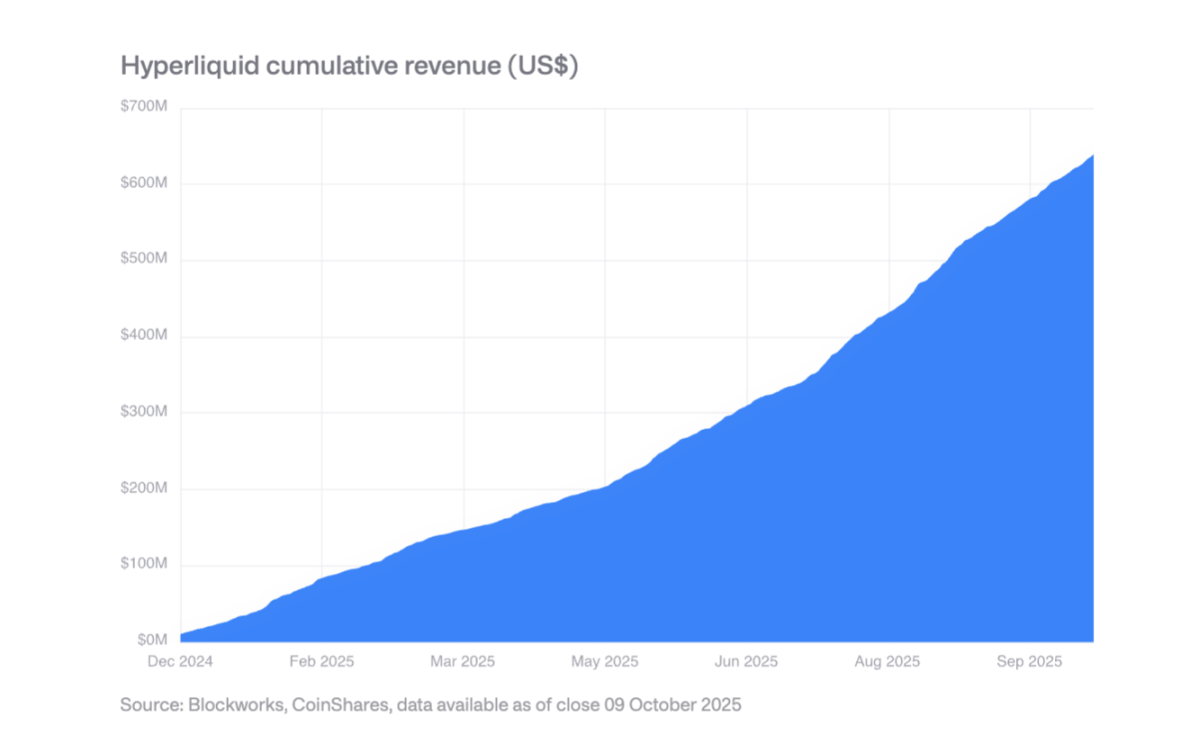

More and more protocols are generating hundreds of millions of dollars in annual revenue and distributing it to token holders. Hyperliquid uses 99% of its revenue to buy back tokens daily, and Uniswap and Lido have also introduced similar mechanisms. This marks a shift in tokens from purely speculative assets to equity-like assets.

VII. The Dominance of Stablecoins and Corporate Adoption

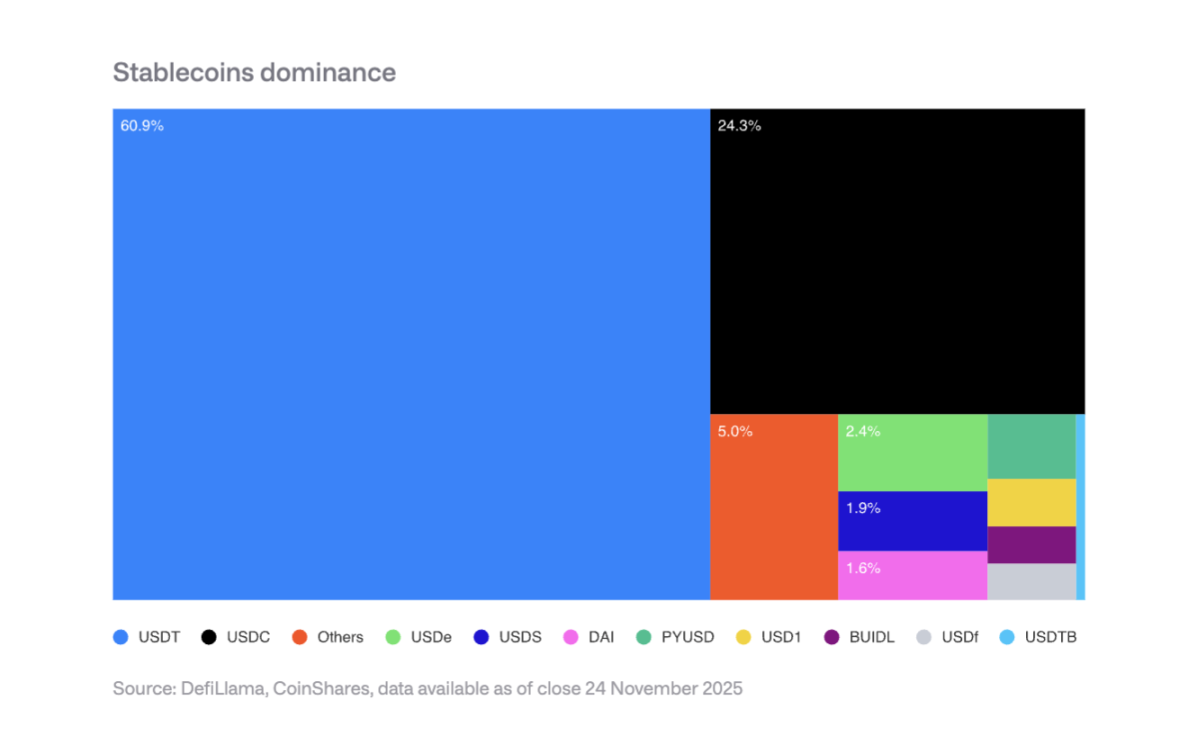

Market concentration

Tether (USDT) holds 60% of the stablecoin market, while Circle (USDC) holds 25%. New entrants like PayPal's PYUSD face challenges from network effects and are unlikely to shake the duopoly.

Enterprise adoption expected in 2026

Payment processors such as Visa, Mastercard, and Stripe have structural advantages that allow them to switch to stablecoin settlements without altering the front-end experience.

Banks: JPMorgan Chase's JPM Coin has demonstrated its potential, and Siemens reports foreign exchange savings of up to 50%, with settlement times reduced from days to seconds.

E-commerce platform Shopify now accepts USDC payments, and is piloting stablecoin provider payments in Asian and Latin American markets.

Income impact

Stablecoin issuers face the risk of declining interest rates: if the Federal Reserve's interest rate falls to 3%, $88.7 billion in new stablecoins would be needed to maintain current interest income.

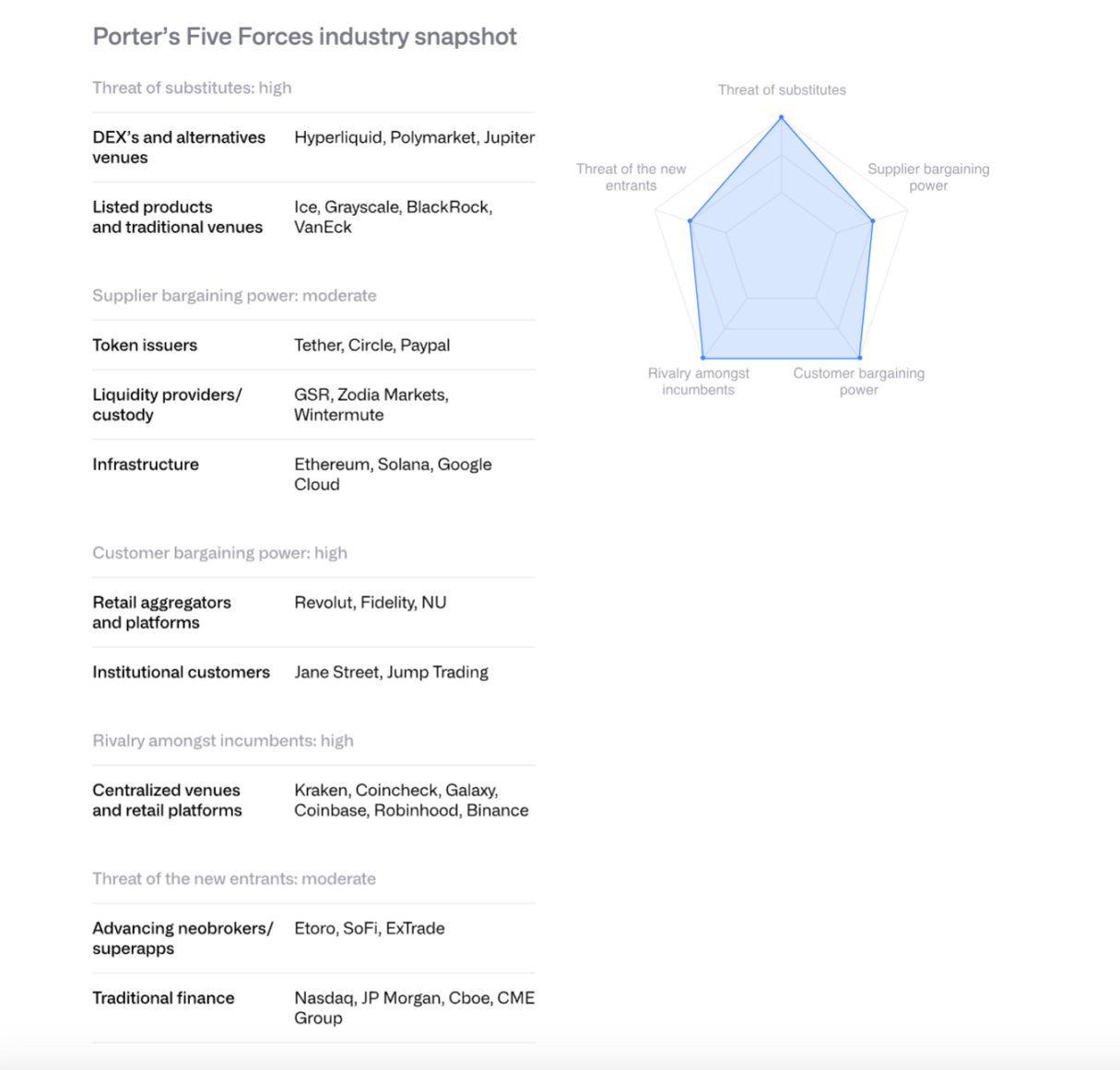

8. Analyze the competitive landscape of stock exchanges using Porter's Five Forces model.

Existing competitors: Competition is fierce and intensifying, with commission rates falling to low single-digit basis points.

Threat of new entrants: Traditional financial institutions such as Morgan Stanley E*TRADE and Charles Schwab are preparing to enter the market, but will need to rely on partners in the short term.

Supplier bargaining power: Stablecoin issuers (such as Circle) are increasing their control through the Arc mainnet. Coinbase's USDC revenue-sharing agreement with Circle is crucial.

Client bargaining power: Institutional clients account for over 80% of Coinbase's trading volume and possess strong bargaining power. Retail users are price-sensitive.

Threat of alternatives: Decentralized exchanges such as Hyperliquid, prediction markets such as Polymarket, and CME crypto derivatives pose a competitive threat.

Industry consolidation is expected to accelerate in 2026, with exchanges and large banks acquiring customers, licenses and infrastructure through mergers and acquisitions.

IX. Competition among smart contract platforms

Ethereum: From Sandbox to Institutional Infrastructure

Ethereum has scaled through the Rollup Centralized Roadmap, increasing Layer-2 throughput from 200 TPS a year ago to 4800 TPS. Validators are pushing for higher base layer gas limits. The US spot Ethereum ETF has attracted approximately $13 billion in inflows.

In terms of institutional tokenization, BlackRock's BUIDL fund and JPMorgan Chase's JPMD have demonstrated Ethereum's potential as an institutional-grade platform.

Solana: A High-Performance Paradigm

Solana stands out with its monolithically optimized execution environment, accounting for approximately 7% of the total TVL in DeFi. Stablecoin supply exceeds $12 billion (up from $1.8 billion in January 2024), RWA projects expand, and BlackRock's BUIDL increases from $25 million in September to $250 million.

Technological upgrades include the Firecanver client and the DoubleZero validator communication network. The spot ETF launched on October 28th has already attracted $382 million in net inflows.

Other high-performance chains

Next-generation Layer-1 blockchains such as Sui, Aptos, Sei, Monad, and Hyperliquid compete through architectural differentiation. Hyperliquid focuses on derivatives trading, accounting for more than one-third of total blockchain revenue. However, the market is highly fragmented, making EVM compatibility a competitive advantage.

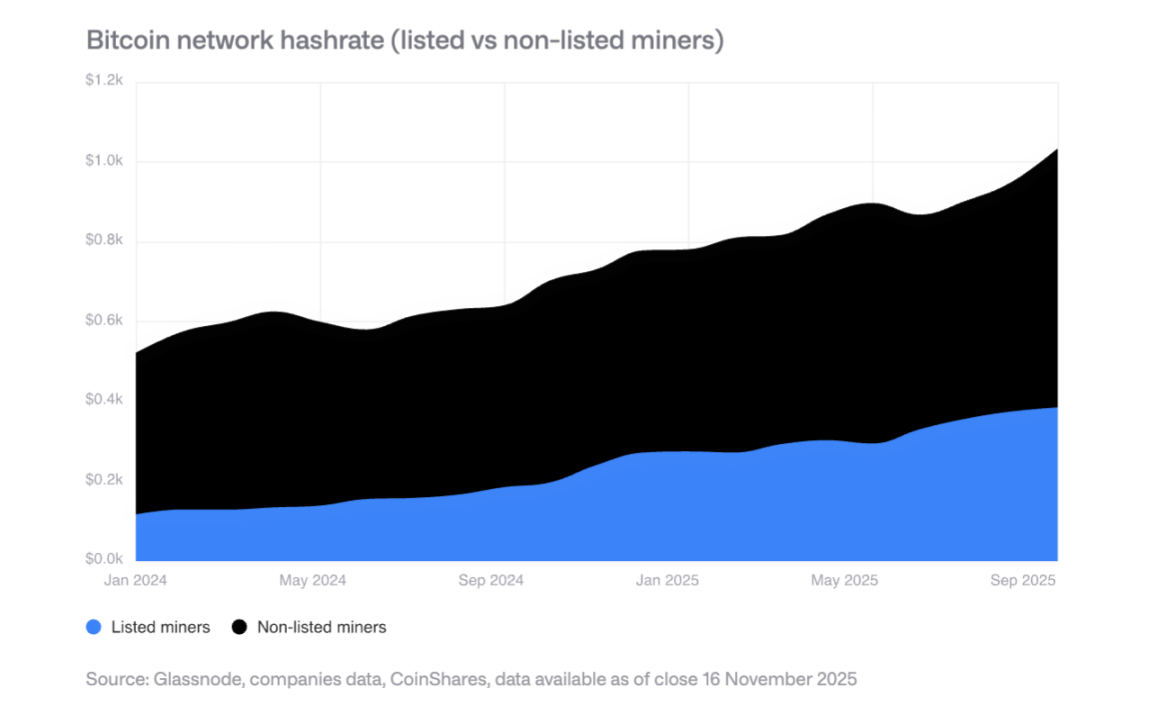

10. Mining Industry Transformation into HPC (High-Performance Computing Center)

Expansion in 2025

The hashrate of listed miners increased by 110 EH/s, mainly from Bitdeer, HIVE Digital and Iris Energy.

HPC Transformation

Miners announced $65 billion in HPC contracts, and it is projected that Bitcoin mining revenue will account for less than 20% of total revenue by the end of 2026, down from 85%. HPC operations are expected to have an operating profit margin of 80-90%.

Future Mining Model

The future of cryptocurrency mining is expected to be dominated by the following models: ASIC manufacturers, modular mining, intermittent mining (coexisting with HPC), and sovereign nation mining. In the long term, mining may revert to small-scale, decentralized operations.

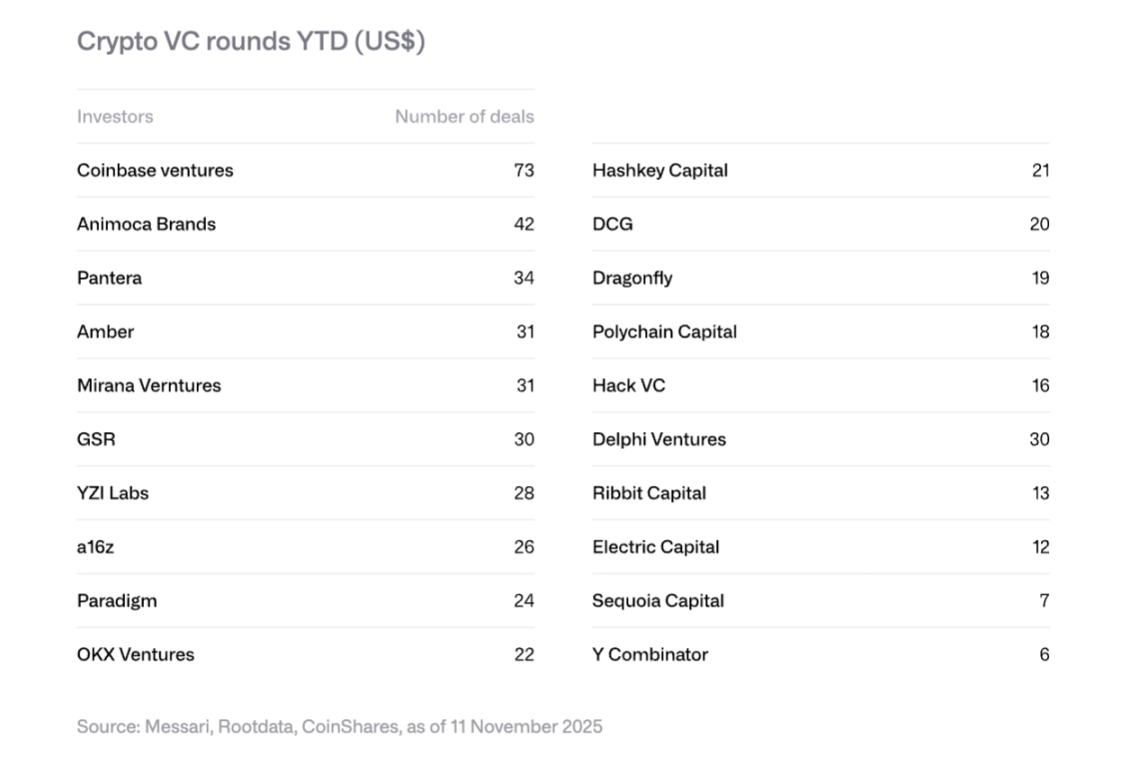

XI. Venture Capital Trends

Recovery in 2025

Crypto venture capital funding reached $18.8 billion, surpassing the total for 2024 ($16.5 billion). This was primarily driven by large deals: Polymarket secured $2 billion in strategic investment (ICE), Stripe's Tempo received $500 million, and Kalshi raised $300 million.

Four major trends in 2026

RWA tokenization: Securitize's SPAC, Agora's $50 million Series A funding round, and other initiatives demonstrate institutional interest.

The combination of AI and encryption accelerates applications such as AI agents and natural language transaction interfaces.

Retail investment platforms: Decentralized angel investment platforms such as Echo (acquired by Coinbase for $375 million) and Legion are emerging.

Bitcoin infrastructure: Layer-2 and Lightning network-related projects are gaining attention.

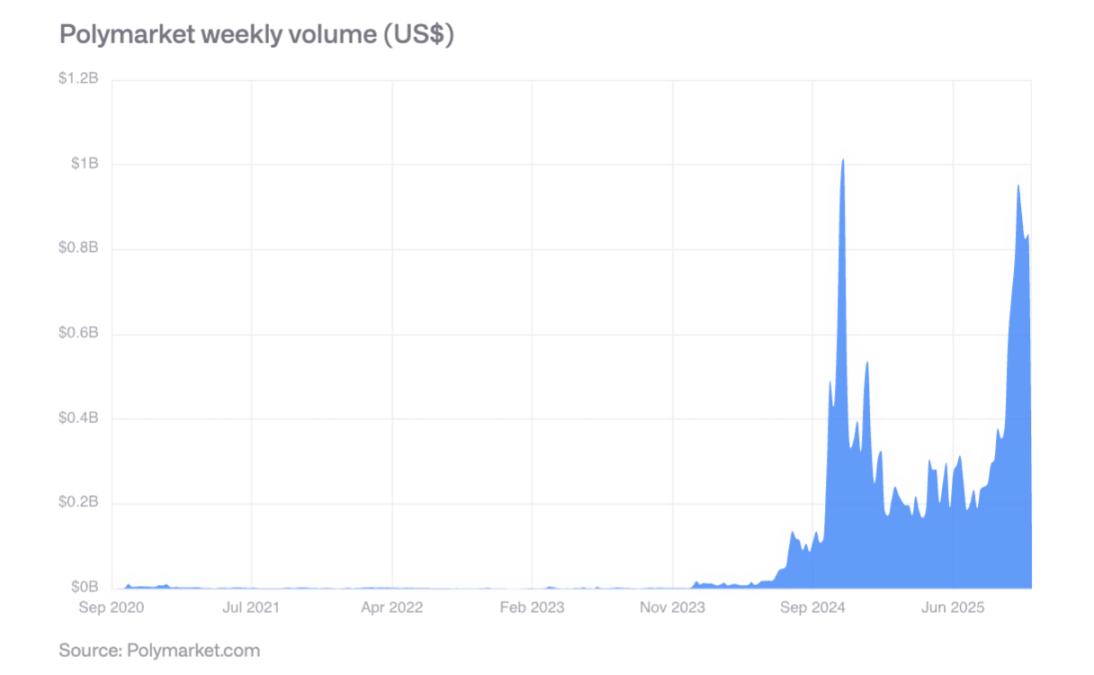

12. Predicting the Rise of the Market

Polymarket saw weekly trading volume exceeding $800 million during the 2024 US presidential election, and its post-election activity remained strong. Its predictive accuracy has been validated: events with a 60% probability occurred approximately 60% of the time, and events with an 80% probability occurred approximately 77-82% of the time.

In October 2025, ICE made a strategic investment of up to $2 billion in Polymarket, signifying recognition from a mainstream financial institution. Weekly trading volume is projected to exceed $2 billion in 2026.

XIII. Key Conclusions

Accelerated maturation: Digital assets are shifting from speculation-driven to utility- and cash flow-driven, with tokens increasingly resembling equity assets.

The rise of hybrid finance: The integration of public blockchains with traditional financial systems is no longer a theory, but is becoming visible through the robust growth of stablecoins, tokenized assets, and on-chain applications.

Increased regulatory clarity: The US GENIUS Act, the EU MiCA, and Asian prudential regulatory frameworks lay the foundation for institutional adoption.

Institutional adoption will be gradual: Although structural barriers have been removed, actual adoption will take several years, with 2026 being a year of incremental progress for the private sector.

Reshaping the competitive landscape: Ethereum remains dominant but faces challenges from high-performance chains such as Solana, making EVM compatibility a key advantage.

Risks and opportunities coexist: High concentration of corporate holdings of cryptocurrencies brings the risk of sell-offs, but emerging fields such as institutional tokenization, stablecoin adoption, and prediction markets offer huge growth potential.

Overall, 2026 will be a pivotal year for digital assets, marking their transition from the margins to the mainstream, from speculation to practical use, and from fragmentation to integration.