Bottom signals are emerging, sovereign wealth funds are secretly accumulating Bitcoin, and a liquidity-driven bull market for Bitcoin in 2026 is poised to begin.

- 核心观点:聪明资金正为2026年牛市提前布局。

- 关键要素:

- 主权基金在8-12万美元区间持续买入。

- 银行及资管巨头正加速向客户开放加密产品。

- 宏观流动性预期改善,ISM指数预示新周期。

- 市场影响:为市场提供长期结构性买盘支撑。

- 时效性标注:中期影响。

Compiled & translated by: Deep Tide TechFlow

Guest: Fabian, Crypto Analyst

Host: Miles Deutscher

Podcast source: Miles Deutscher Finance

Original title: Smart Money Is Front-Running Bitcoin 2026 (You're Not Bullish Enough)

Broadcast date: December 6, 2025

Key points summary

In this podcast episode, Miles Deutscher delves into Bitcoin's reaction to market fears, suggesting it could be a signal of the early stages of a liquidity cycle in 2026. He also explores how institutions, sovereign wealth funds, and major market players are actively positioning themselves ahead of a potential bull market expansion. Together with Fabian, he analyzes the macroeconomic forces driving Bitcoin, Ethereum, and the entire crypto market, revealing the real competitive advantages quietly emerging in the altcoin market.

Summary of key viewpoints

- The panic selling in the market is nearing its end.

- The four-year cycle never truly existed.

- A rate cut is practically a done deal.

- Some sovereign wealth funds are on standby, gradually increasing their holdings at 120,000, 100,000, and I know they bought even more at 80,000.

- The core driver of the Bitcoin market is liquidity, not technical chart lines or indicators like the 50-day moving average. Bitcoin is essentially a "liquidity sponge," absorbing liquidity from the market.

- The market may be underestimating the scope for interest rate cuts, and there will be more rate cuts next year than the market currently expects.

- The current market performance is more related to the macroeconomic environment than to internal Bitcoin events.

- We are currently in the bottoming-out phase, and the market is more likely to break upwards rather than continue to fall in the coming months or even quarters.

- After a period of significant market volatility, when the market rebounds to key resistance levels for the first time, it will inevitably encounter selling pressure. What truly matters is how the market reacts to these key levels, not just whether prices break through or fall below them.

- Banks gradually opening up access to cryptocurrencies to their customers is a long-term global trend.

- Financial institutions will eventually have to compromise and join the cryptocurrency trend; it has become inevitable.

- If you are a country or sovereign wealth fund and want to accumulate Bitcoin, you certainly won't announce it publicly at first, until you are satisfied with your holdings, or you may never announce it publicly because you don't want to be the first to market.

- Bitcoin is gradually becoming an attractive long-term diversification tool.

- Bitcoin-backed loans may be a sign of Bitcoin's growing legitimacy as an asset class.

- The main source of selling pressure on Ethereum is treasury funds; as long as they continue to hold, ETH may outperform in the short term.

- A significant advantage of prediction markets is that they allow you to trade the same assets as in traditional markets, but without the risk of being liquidated.

- The trading logic of predicting the market is simply "yes" or "no." This simplicity lowers the investment threshold and also reduces unnecessary risks.

- Prediction markets are a very basic but effective way of trading, especially in areas with low liquidity, such as pre-market markets. They are perhaps one of the most product-market fit innovations in the crypto space to date.

Psychological characteristics of Bitcoin bottom formation & key indicator analysis of extreme sell-offs

Miles: The past week has been filled with negative news, but the market's reaction to it has been relatively calm. Generally, FUD (Funds Uncertainty) often signals a bottom in the cryptocurrency market; events like China's ban on Bitcoin, negative news about Tether, and the Bank of Japan's policies often foreshadow local bottoms. This week, I've gathered some evidence that fund flows seem to be gradually shifting from bearish to bullish. Of course, there are still some things to watch out for, such as potential DAT selling pressure and some macroeconomic factors.

In summary, based on the information available, and from a probabilistic perspective, I believe the bottom may have already been reached. What do you think? Do you think Bitcoin has bottomed out?

Fabian:

My view is largely the same as yours; I believe the peak of the panic selling (peak capitulation, a large-scale sell-off triggered by market panic) has passed. We also mentioned this in last Friday's live stream. In fact, multiple indicators suggest we've already experienced extreme levels of selling. At the beginning of this week (Monday), the market saw a slight pullback, with prices falling to the mid-to-high range of 80,000, mainly due to another round of FUD (Fear, Uncertainty, and Demand) effects.

Last weekend, market concerns over MicroStrategy's financial situation, coupled with soaring Japanese government bond yields and news of renewed Chinese crackdowns on cryptocurrencies, reiterated their negative stance on the cryptocurrency. This news caused the market to open lower, but prices rebounded quickly within just a day or two. As you said, I think this indicates that those who wanted to sell at current prices have essentially completed their selling . In other words, the panic selling in the market is nearing its end.

However, the market's bottoming process may be complex. In the coming weeks or one or two months, prices may retest the 80,000 low, or even slightly break below it. Overall, I believe we are currently in a bottoming phase, and the market is more likely to break upwards than continue to fall in the coming months or even quarters.

Breakthrough and Challenge of Long-Term Resistance Levels

Miles: There is still a significant resistance area above the market. If we look at the daily chart, we can see that the price is trying to break through the moving average above. On the 4-hour chart, the Point of Control (POC) of the Visible Volume Range (VRVP) is still around 96,000, which forms a clear resistance area.

While the market has seen a slight rebound recently, looking at indicators such as the weekly chart and the 50-week simple moving average (SMA), the price remains below key levels around 102,000. Therefore, I believe the 95,000 to 100,000 range will be a difficult area to break through. Until we successfully break through and hold these resistance levels, I will not choose to go all-in on risky assets or altcoins, nor will I take on excessive risk. What do you think?

Fabian:

I completely agree. My usual expectation is that, especially after such significant volatility, when the market first rallies to key resistance levels—particularly those converging resistance areas you mentioned—it will encounter selling pressure, at least in the short term. As for whether the market can break through these resistance levels in one go, I don't have a particularly strong opinion. However, overall, I think the market will perform relatively positively in the coming weeks and even months, with prices likely to test higher levels before we see how it unfolds.

Besides some positive factors within the cryptocurrency market itself (such as positive capital flows), we are also seeing a return to risk-on sentiment in traditional financial markets (TradFi). This is an external tailwind for Bitcoin. For example, the VIX index fell sharply this week, and the US dollar index (DXY) also retreated from its structural resistance level of 100-101. At the same time, retail investor interest in high-momentum stocks (such as Robinhood and robotics concept stocks) is also recovering. These signs indicate that market risk appetite is increasing. However, whether Bitcoin can break through the current resistance level in one go remains to be seen.

Miles: I agree with you. I think the market's reaction to these key levels reveals more comprehensive information than just whether prices break through them; it's more important to observe market inflows and outflows. For example, have ETFs returned to net inflows? Is market sentiment positive? Are we seeing high-volume candles indicating investor interest in these levels? Or is this just a short-lived "dead cat bounce"? Therefore, what really matters is how the market reacts to these key levels, not just whether prices break through or fall below them.

Smart money market positioning strategies & institutional investor adoption trends

Miles: Next, let's talk about the big players in the market and the strategies that "smart money" is employing. I've found the market positioning for 2026 to be very interesting, and I believe "smart money" is already prepared for the future market.

Let's start with Bank of America. Recently, they officially recommended that clients allocate 4% of their portfolios to Bitcoin and cryptocurrencies. I think this reflects a long-term trend of banks and financial institutions gradually opening up their attitudes towards crypto assets. We'll also talk about Vanguard's shift later, but overall, this change in banking is largely driven by deregulation policies and the Trump administration. Fabian, what are your thoughts on this trend of banks gradually opening up their cryptocurrency offerings to clients?

Fabian:

I believe this is a long-term global trend , potentially lasting for decades. It's not just in the US; we'll see more and more similar news globally. I even believe that one day China will change its attitude towards cryptocurrencies, though perhaps not today. Overall, the global adoption of Bitcoin and cryptocurrencies is almost irreversible; my overall assessment of this trend is that it will only rise. Pandora's box has been opened, and regardless of future US government changes (whether it's the midterm elections or the next presidential election), this trend will not turn back.

The core issue in the current market is how global adoption trends will counteract supply bottlenecks. In the early days of Bitcoin, a large portion of the supply was concentrated in the hands of a few major players, such as early holders or companies like MicroStrategy. As investors, we are essentially trading liquidity between these two groups. Furthermore, I've noticed an interesting divergence in sentiment between Crypto Twitter and traditional financial markets. Many in the crypto community are pessimistic about the market, believing the cycle is over; while traditional financial institutions view the current market correction as a "buy the dip" opportunity. This long-term perspective is very positive for the market, as these traditional financial institutions are currently the dominant force.

Miles: I completely agree with you. That's why we might see Bitcoin reach new highs next year, or even experience a strong upward trend. Speaking of the shift in "smart money" and major players, I'd like to specifically mention Vanguard. In 2024, Vanguard's CEO made it clear that they wouldn't offer a Bitcoin ETF and wouldn't change that stance. However, just one year later, with a new CEO in charge, they announced a Bitcoin ETF for 50 million clients. As a top global asset management company managing $11 trillion in assets, this shift is significant. What are your thoughts on this change in attitude?

Fabian:

This is a common path for almost all major financial institutions. Even leaders like Jamie Dimon of JPMorgan Chase, who were once publicly bearish on cryptocurrencies, have now had to accept this trend. It's essentially a "choice without choice." As publicly traded companies, their primary mission is to create value for shareholders and pursue profits. Ignoring the cryptocurrency market would not only mean missing out on enormous current and future revenue potential, but could also hand over customers to competitors offering crypto products. Therefore, regardless of their political stance or personal preferences, ultimately they have to compromise and join this trend; it has become inevitable.

The continued accumulation of sovereign wealth funds & the long-term structural demand for Bitcoin

Miles: Let's talk about the market positioning of sovereign wealth funds, which could be one of the next important narratives for Bitcoin. Larry Fink mentioned some things about sovereign wealth funds today, and I think that's very noteworthy.

Larry Fink: I can tell you that some sovereign wealth funds are on standby, gradually increasing their positions at 120,000, 100,000, and I know they bought even more at 80,000. They are building long-term positions.

He said he knew these funds bought a lot in the 80,000 area, which explains why we're seeing such a strong market reaction in this price range. Clearly, big players have entered the market at this level.

Regarding the narrative surrounding sovereign wealth funds, I think there's a lot of discussion in the market about ETFs and retail investors, even about corporate ETFs, but the deployment of sovereign wealth funds hasn't received enough attention. I know there were rumors that the Trump administration might use Bitcoin as a strategic reserve, but this plan hasn't been fully realized. Although they retained the confiscated Bitcoin, there were no plans to significantly increase the reserves.

This reminds me of an idea: if you're a country or sovereign wealth fund wanting to accumulate Bitcoin, you certainly wouldn't announce it publicly at first, until you're satisfied with your holdings, and you might never even announce it because you don't want to be frontrunners. You just accumulate quietly. As these funds continue to buy, the market's decline will gradually decrease, and volatility will also decrease, but they probably won't publicly acknowledge this. That's what I find interesting. Fink knows these big players, and perhaps some countries are secretly accumulating Bitcoin. What do you think of this sovereign Bitcoin narrative? I feel this point hasn't been fully discussed, but it's clearly one of the important reasons why Bitcoin as an asset has become more mature and its volatility has decreased.

Fabian:

Indeed, this is a very interesting perspective. Over the past few decades, most countries' central banks and sovereign wealth funds have primarily concentrated their holdings in two types of assets: US assets (such as US stocks) and government bonds (whether domestic or foreign, mainly US bonds).

However, the safety and diversification capabilities of these two asset classes have been questioned in recent years. Treasury bonds have underperformed since 2020, and countries with excessive holdings of U.S. assets risk systemic problems should the U.S. economy falter. Therefore, we are seeing a growing number of central banks and sovereign wealth funds seeking to diversify their portfolios.

Currently, there are not many high-quality assets available. Emerging markets are riskier and more uncertain, and gold remains the mainstream choice among commodities. However, Bitcoin is gradually emerging as an attractive long-term diversification tool. While sovereign wealth funds may not increase their Bitcoin holdings as rapidly as they accumulate traditional assets, the process of gradually increasing from zero allocation has already begun, and this trend is likely to continue in the coming years.

Miles: Not only BlackRock and Vanguard, but even JPMorgan Chase has begun offering structured Bitcoin products based on IBIT to institutional clients. These products not only deliver significant returns when Bitcoin prices surge, but also incorporate downside protection and risk control parameters. These tools start with Bitcoin ETFs and can then be further developed into more complex financial derivatives, such as Bitcoin-backed bonds— a completely new use case we've never seen before.

Furthermore, if these tools become more sophisticated, will we see Bitcoin-backed mortgages? I believe this would be a sign of Bitcoin's gradual legitimization as an asset class. While this trend is underway, it's evolving slowly and won't happen overnight. You might feel pessimistic if Bitcoin's price drops to 80,000, 70,000, or 90,000 in the short term, but in the long run, the trend is very clear, which is why I remain a staunch long-term Bitcoin holder.

Fabian:

That's true. This reminds me of MicroStrategy's statement earlier this week that they were considering lending using Bitcoin as collateral. Based on this, I think the Bitcoin lending market could become a completely new vertical and grow rapidly in the coming years.

Miles: Yes, but do you know why MicroStrategy did this? In my opinion, their goal was to avoid the risk of a downgrade by MSCI (Morgan Stanley Capital International), which means being removed from relevant indices. Their method of avoiding downgrade was to offer more complex financial instruments, such as bonds or lending products, thus preventing themselves from being seen as a passive fund. If a company simply holds Bitcoin without generating revenue, they are easily classified as a fund. But by activating some of their Bitcoin holdings, they can be redefined as a revenue-generating company, thereby mitigating the risk of downgrade.

Fabian:

Another explanation is that they did this to gain more flexibility in terms of financing. If Bitcoin assets face potential downside risks, transferring more debt can help them better protect themselves. This strategy is essentially aimed at enhancing the company's resilience to market volatility.

Macroeconomic factors that are favorable to the crypto market

Miles: Before we delve into the core drivers of the market, I'd like to share some news that just broke: Eric Trump's "America Bitcoin" fund has just purchased 363 bitcoins worth $34 million. The Trump family's continued Bitcoin purchases are undoubtedly a positive sign for the market. As long as the Trump family has influence in politics, this support will be beneficial to the market.

Fabian:

Indeed, this demonstrates their continued support for Bitcoin. While the size of this purchase isn't enough to directly drive the market, it sends a clear message: their stance remains unchanged, and I expect this trend to continue as long as they maintain a certain level of political influence.

Furthermore, I believe that as the midterm elections approach, they may intensify their supportive rhetoric on the crypto market in an attempt to regain voter support. Last year, during the campaign, they tried to garner support from the crypto community because data showed a significant proportion of US voters held Bitcoin, and this voter group could play a crucial role in the election results. While the exact figures may be unclear, the crypto community has experienced a period of volatility since then. I expect they will try to boost market confidence before the election by supporting Bitcoin and the crypto market; we can wait and see.

Macroeconomic Trend Analysis in 2026

Miles: Ultimately, the core driver of the Bitcoin market is liquidity, not technical chart lines or indicators like the 50-day moving average. Bitcoin is essentially a "liquidity sponge," absorbing market liquidity. In the current market environment, Bitcoin remains a risk asset, and risk assets typically perform well in a liquid, venture-friendly macro environment.

ISM Manufacturing Index and Business Cycle Outlook

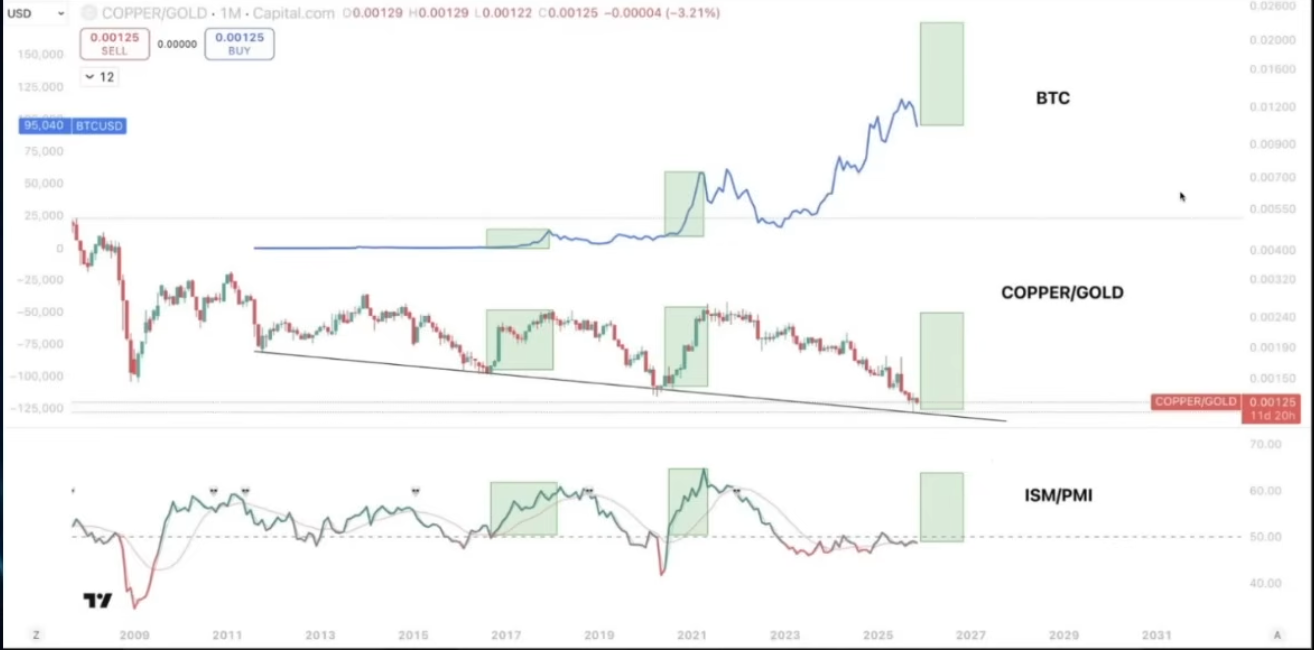

Miles: If we want to determine whether the market will be bullish in 2026, we must analyze it from a macroeconomic perspective. Let's start by talking about the ISM Manufacturing Index (this indicator is actually a key economic indicator used to track business cycles) . Currently, the ISM index is much lower than in previous cycles, and Bitcoin usually shows an upward trend before the ISM. Nevertheless, the ISM is expected to rebound in the future. If we look back at the past three cycles, Bitcoin only peaked when the ISM exceeded 55; in other words, the current Bitcoin rally has not truly begun.

To determine whether 2026 will ultimately be bullish, we need to look at the macro picture, which is also your strength. First, I want to discuss the ISM. I know Raoul Pal talks about this frequently; the ISM index is actually much lower than in previous cycles, and Bitcoin typically leads the ISM, so it's performing well. But we expect to see a rebound. If you look at the past three cycles, Bitcoin only peaked when the ISM was above 55. It hasn't really started its big rally yet.

Raoul Pal (CEO of Real Vision)'s core theory is that he believes the ISM index will rebound in the first half of 2026, while liquidity conditions will become more relaxed, which will be a key trigger for the next Bitcoin surge. Are you paying attention to this indicator?

Fabian:

The ISM is a macroeconomic indicator that I pay close attention to. It reflects the overall growth of the US economy and the business cycle, but it is itself a relatively lagging indicator. The business cycle, in turn, lags behind the liquidity cycle, which is the precursor to all these economic activities, and there is a close relationship between them.

As you mentioned, while there may be some concerns about the liquidity cycle in the long term over the next few years, we are likely to see a significant increase in global liquidity, particularly in the US, at least in the first half of next year, the next few quarters. This liquidity expansion typically drives a recovery in growth and the business cycle, and eventually permeates all risk assets, including Bitcoin. So I think your point is valid, and at least for the next few quarters, I agree with you.

Miles: We can see that Bitcoin's price is typically highly correlated with the ISM's movement. For example, in the 2018 cycle, Bitcoin peaked when the ISM peaked. While Bitcoin's performance is driven by other factors, the ISM hasn't peaked yet. If the ISM starts to rebound, could this be a trigger for the next Bitcoin rally? This is one of the indicators we need to focus on.

In addition, several related indicators are worth noting, such as the copper-gold ratio and the ISM PMI ratio . These indicators all seem to have the potential for a rebound. When you begin to analyze this evidence, you'll find that the four-year cycle theory doesn't actually hold true. Many people believe that Bitcoin's four-year cycle is due to the halving event, but if that's the case, why did the US stock market, the copper-gold ratio, and the ISM all peak at similar times?

If the four-year cycle truly exists, does that mean Bitcoin's halving cycle is more important than the entire US manufacturing index or business cycle? This clearly doesn't make sense. Bitcoin is just a small part of the business cycle. From my perspective, the four-year cycle has never truly existed, and 2026 might prove this, completely overturning this theory.

If Bitcoin can rebound in the first half of next year, it will completely change market perception. People will realize that Bitcoin is a liquidity-driven asset, rather than simply an asset dependent on halving cycles. This shift in perception could attract more investors, especially those who were previously skeptical of the four-year cycle theory.

Fabian:

Simply put, the market is never that simple. We cannot rely solely on simplistic theories like the "four-year cycle" to predict market trends. As you said, the sample size for the four-year cycle is very limited, with only two cycles (N=2), which is clearly insufficient to draw strong conclusions. Moreover, the performance of these cycles happens to coincide with the major macroeconomic inflection points of liquidity and growth cycles.

Furthermore, the impact of Bitcoin halvings on price has significantly diminished over time. The reduction in supply resulting from halvings represents a smaller percentage of the total supply, and the primary market driver has shifted to global and institutional fund flows. These flows are more influenced by macroeconomic cycles than by the Bitcoin halving event itself.

Therefore, I have never believed in the four-year cycle theory. Current market performance is more related to the macroeconomic environment than to internal Bitcoin events.

repricing of interest rate cut expectations

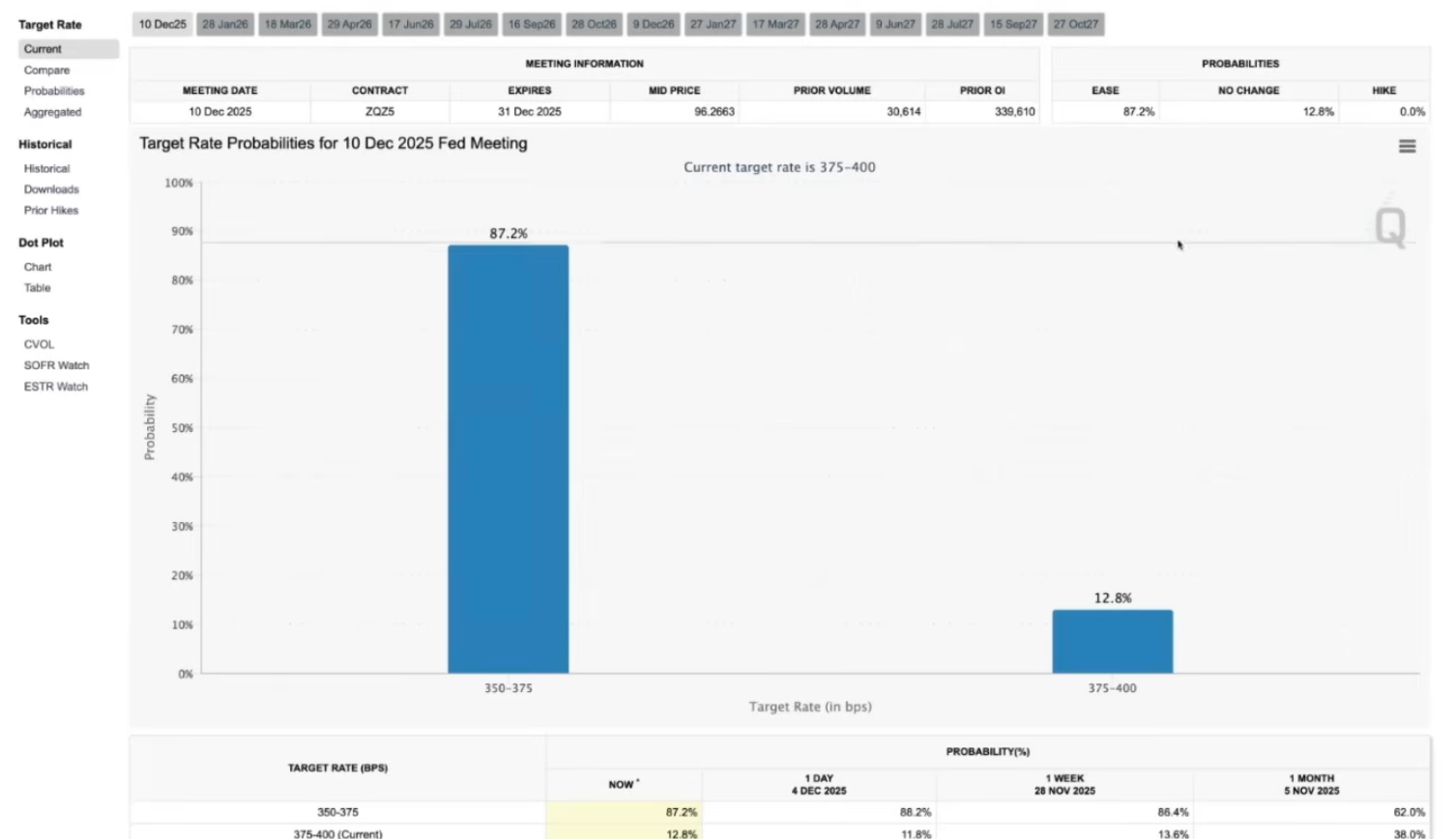

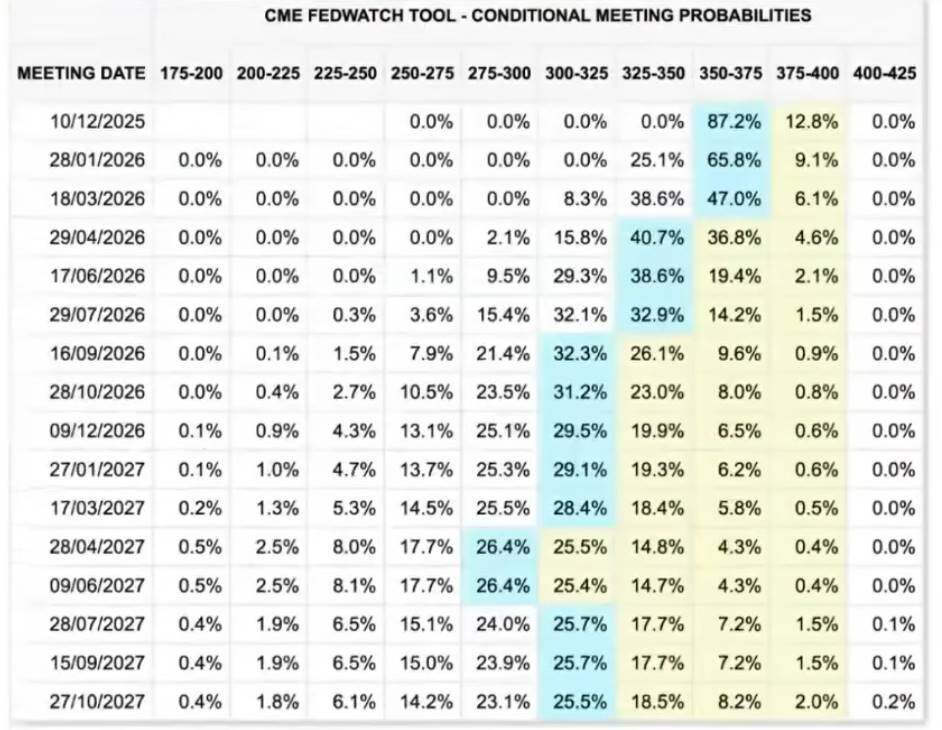

Miles: The probability of a rate cut at the next Fed meeting has increased significantly, and it's almost considered a certainty. Multiple authoritative sources also indicate that a rate cut is imminent. Have you noticed any changes in rate cut expectations this week? Or do you think this will be another catalyst for the market?

Fabian:

At this point, a rate cut is practically a foregone conclusion. I actually had a similar assessment last week, but typically, as the decision date approaches, the market's implied probability leans more towards one direction. The Federal Reserve has a history of signaling in advance, so we can be more confident in our expectation of a rate cut.

The next question is, to what extent has the market priced in this rate cut? Currently, US stocks are near historical highs, while Bitcoin has lagged slightly, but it also has its own unique challenges. Therefore, I tend to view US stocks as a more representative indicator of market pricing.

However, I believe that even if a rate cut does occur, Powell may adopt a more hawkish stance at the press conference. After all, at the FOMC meeting at the end of October, he stated that they were unsure whether to cut rates without sufficient supporting economic data. Since then, key economic data has not changed significantly. Therefore, to justify this rate cut, Powell may emphasize that it is a forward-looking measure, but future rate cuts require more data to support them. He may signal a "hawkish rate cut," telling the market not to have overly high expectations for further rate cuts.

This "hawkish rate cut" may cause short-term market volatility, but overall, I remain optimistic about the current market positioning. Based on market pricing, there may only be two more rate cuts before the end of 2026, bringing the federal funds rate down to around 3%. However, the Trump administration and some potential Fed chair candidates (such as Bessent and Hasset) have stated that they believe the federal funds rate should be closer to 2.5%, meaning the market may be underestimating the room for further rate cuts.

Given that next year is a midterm election year and the Federal Reserve Board of Governors and Chairman will be replaced in May, I believe the market may readjust its expectations, anticipating more rate cuts. This repricing will provide strong support for bullish risk assets. Even if Powell is more hawkish at this meeting, I still believe there will be more rate cuts next year than the market currently expects.

Miles: You mentioned the inflation rate earlier. Actually, the inflation rate has declined somewhat. Although year-on-year data still shows an increase, according to True Inflation (a real-time inflation index), the inflation rate has fallen from its local peak. This may also be an important reason for the current interest rate cut.

I agree with you. If the interest rate cut does happen, it will be a potential bullish factor for the market and deserves our close attention.

Regarding the midterm elections, according to prediction market data, the Democrats seem more likely to win. From my understanding, the Republicans might try to win votes by pushing up the market before the midterm elections. Does this mean that loose monetary policy will continue? What would be the impact if the Democrats win the House? What are your thoughts?

Fabian:

First, in terms of direct impact, there is indeed a positive correlation between the Republican Party's probability of winning and the price of Bitcoin. The Republican Party is generally considered more pro-cryptocurrency, and they are pushing for some cryptocurrency-related legislation. If these bills fail to pass before the midterm elections, and the Republican Party subsequently loses some power, the legislative process could be stalled.

More interestingly, we did observe a degree of synchronicity between changes in the probability of a Republican victory and the price of Bitcoin. A few months ago, when the price of Bitcoin peaked, the probability of a Republican victory also peaked. While other factors are at play, this correlation cannot be ignored.

At a deeper level, I believe the market has already largely priced in these political risks, and may even have overreacted to this uncertainty due to the recent drop in Bitcoin. Going forward, I think the Trump administration will face even greater pressure to take all necessary measures to boost the economy and financial markets before the midterm elections to increase their chances of winning . This effort could support a rise in risk assets in the first half of next year.

My prediction is that the market may already be pricing in these expectations , especially with the new Federal Reserve Chairman taking office in May 2026. These factors could be a strong driver of market gains. Of course, volatility could increase as the midterm elections approach, as markets dislike uncertainty. But until then, these factors will provide a significant tailwind for the market.

How does the price relationship between ETH and BTC affect other cryptocurrencies?

Miles: We are likely to see Bitcoin peak in the first half of this year, and US stocks may peak around the same time. As for what will happen next, we need to continuously adjust our strategies based on market dynamics. Currently, we unanimously believe that the overall market outlook is bullish.

We recently saw the ETH/BTC exchange rate break upwards for the first time in a long time. This is quite interesting. Even more noteworthy is that this phenomenon occurred despite weak Bitcoin dominance. This is the first time I've seen Bitcoin's dominance fail to rise even with weak market performance. What do you think the combined significance of these two charts means? I feel this could mean that even if Bitcoin's price remains flat or rises slightly, altcoins could potentially outperform in this market cycle. What are your thoughts?

Fabian:

This is a very interesting question, and to be honest, I have some reservations about it. I have two seemingly contradictory viewpoints.

First, you're right, ETH has indeed shown relative strength against BTC recently. But is this simply because ETH has fallen more from its peak than Bitcoin, and is now just a case of mean reversion? That remains to be seen, but I currently tend to believe it's a result of mean reversion.

However, we've also noticed that BMNR (Tom Lee's Ethereum DAT treasury) is buying large amounts of Ethereum weekly, even exceeding MicroStrategy's Bitcoin purchases. This trend continues so far. While I haven't delved into BMNR's specific operations, this sustained accumulation clearly supports ETH's short-term performance. Therefore, as long as this buying activity continues, I believe ETH is likely to outperform in this rally.

However, from a longer-term perspective, I am cautious about ETH's performance. Large treasury firms hold 6% to 7% of ETH's market supply, a significantly higher percentage than MicroStrategy's holdings of Bitcoin. If these treasuries were forced to sell at some point in the future, it could have a greater impact on the market. Furthermore, ETH is considered a more volatile and lower-quality asset, making it less resilient to risk. Therefore, in the long run, I remain more bullish on Bitcoin and believe it will outperform.

Miles: In the long term, I agree with you. But if we look at it from a short-term perspective, I think you might also agree: if Bitcoin performs strongly in the first and second quarters of this year, which means the overall market is in a favorable state, then Ethereum may outperform Bitcoin. The reason is that Ethereum has a smaller circulating supply, with more supply held by DAT, and these institutions are likely to accumulate more actively. This structural advantage could allow Ethereum to outperform in the short term.

Of course, these tailwinds could quickly turn into headwinds if market conditions deteriorate. This is especially true when market concerns about centralization and potential sell-offs intensify, potentially acting as a catalyst for a decline. However, this phenomenon is reflexive and can also occur during market rallies, which is clearly very favorable for altcoins. Hopefully, we will see this positive trend.

Fabian:

You're right, and I'm completely open to the idea that Ethereum could indeed outperform Bitcoin in the short term, as long as these DATs don't sell off and continue to accumulate, ETH has the potential to perform exceptionally well.

In contrast, Bitcoin currently faces some unique structural problems. For example, miners may continue to sell as they transition into AI data centers. Additionally, some early investors (OG holders) may continue to sell, as they tend to believe in the four-year cycle theory.

There are also some potential tail risks, such as Bitfinex's Bitcoin debt issue. The US government currently owes Bitfinex approximately 100,000 bitcoins, which may be repaid at some point in the future. If these bitcoins are liquidated and returned to creditors, this will create additional selling pressure in the market.

In contrast, the main source of selling pressure on Ethereum is these treasuries, and as long as they continue to hold, I agree that ETH may outperform in the short term.

Predicting investment opportunities and excess returns in the market

Miles: Prediction markets are a topic I plan to explore in depth over the next few weeks, as I'm also experimenting with some new things, such as creating automated trading bots using AI, and these projects will be public soon. But I know you already have several months of practical experience in prediction markets, especially in pre-market trading. Could you share your experience and why you believe this is an investment area worth watching in the coming months?

Fabian:

Prediction markets are a very interesting area. I especially enjoy using them for pre-market trading, particularly in the pre-TGE (Pre-Token Generation Event) token market. A unique advantage of prediction markets is that they provide investors with a low-risk environment, making them particularly suitable for shorting new tokens that are overvalued by the market.

Based on experience from the past year and even earlier, we've found that pre-market trading often overvalues new tokens. Most new tokens experience a "down-only" price movement after launch, as seen with Plasm recently. Many new tokens have excessively high pre-market valuations, such as Stable (an upcoming Plasma competitor, a stablecoin blockchain), ME, and Monad (which just launched last week). These valuations clearly don't reflect the actual market situation.

A major reason for this mispricing is that many investors are hesitant to short these tokens in traditional pre-market markets. Short sellers often face short squeezes in these markets, resulting in significant losses. The advantage of prediction markets lies in their provision of an "options"-like trading model, particularly put options. You can bet that a token's price will fall within 24 hours after the TGE (Time Limit Expired) without worrying about price fluctuations or the risk of liquidation. This mechanism makes prediction markets an ideal tool for shorting overvalued tokens.

Over the past month, I've made several trades on several upcoming new tokens. For example, I bought the "No" option in the pre-market for Stable at valuations of $4 billion and $5 billion, and it performed exceptionally well. I also bought the "No" option in the pre-market for Me and Monad. This trading method leverages discrepancies in market mispricing and is a highly effective strategy. While everyone knows how these tokens will perform after listing, few are able to effectively capitalize on this before listing. Prediction markets offer a unique opportunity for investors to capture these discrepancies.

Miles: In traditional markets, when panic sets in, many investors sell their positions, causing prices to plummet. However, in pre-market trading, investors cannot engage in panic selling because these trades are typically based on contracts and lack a mechanism for selling physical goods. Unless a large number of investors short the market, price fluctuations in the pre-market are relatively small. Even if a liquidation spike occurs, it often deters some investors, further reducing market volatility.

One significant advantage of prediction markets is that they allow you to trade the same assets as in traditional markets, but without the risk of liquidation. I believe this is a very important feature, which is why prediction markets are a field worth exploring in depth.

Furthermore, I find the simplicity of the prediction market very appealing. Compared to the complex options trading on Deribit, the prediction market is much more intuitive. In the options market, you need to consider strike price, expiration time, premium costs, and how to allocate appropriate call or put options based on your portfolio structure; while perpetual contract trading requires understanding changes in funding rates. These complex factors are not friendly to ordinary investors, and a slight mistake can lead to high transaction costs.

In contrast, the trading logic for predicting the market is simply "yes" or "no." If you believe the market is giving a probability that is lower or higher than your expectations, you only need to trade based on that, without considering other complex factors. This simplicity lowers the investment threshold and also reduces unnecessary risks.

I believe prediction markets will become an even bigger trend in the future. They have already achieved tremendous success in political and sports betting, and I think their potential is equally huge in the crypto space. I think this is an area worth continuing to watch because it offers investors more diverse options, rather than just being limited to holding positions or simple buying and selling.

Prediction markets are a very basic but effective way of trading, especially in areas with low liquidity, such as pre-market markets. They may be one of the most product-market fit innovations in the crypto space today.

Fabian:

One overlooked advantage of prediction markets is that they can be used not only for speculation but also as a hedging tool in many situations . For example, in the pre-market, if you are eligible for an airdrop of a certain token, you already know the quantity, but may not have enough capital or want to avoid the risk of being liquidated for shorting, you can use the pre-market to hedge some of the risk. While this hedging may not completely cover all risks, it does provide a flexible and practical way to manage risk.

Furthermore, prediction markets can help investors hedge against political or geopolitical risks. For example, if you believe that the price of Bitcoin may be affected by certain major events, and there happen to be related transactions in the prediction market, such as "the Republicans losing the House of Representatives in the midterm elections" or "Satoshi Nakamoto transferring funds before 2026," you can hedge against potential tail risks through these markets.