Tether Financial Analysis: Requires an additional $4.5 billion in reserves to maintain stability.

- 核心观点:Tether 资本充足率接近监管底线。

- 关键要素:

- Tether 业务本质是未受监管的银行。

- 其资本充足率在3.87%至10.89%之间。

- 集团留存收益非代币持有者的法定资本。

- 市场影响:引发对稳定币储备充足性的审视。

- 时效性标注:中期影响。

Original author: Luca Prosperi

Original article translated by: Deep Tide TechFlow

When I graduated from college and applied for my first management consulting job, I did what many ambitious but cowardly male graduates often do: I chose a company that specializes in serving financial institutions.

In 2006, banking was a symbol of "cool." Banks were typically housed in the grandest buildings in the most beautiful neighborhoods of Western Europe, and I was looking forward to traveling the world. However, no one told me that this job came with a more secretive and complex condition: I would be "married off" to one of the world's largest and most specialized industries—banking—indefinitely. The demand for banking experts has never disappeared. During economic expansions, banks become more innovative and need capital; during economic contractions, banks need restructuring, and they still need capital. I tried to escape this vortex, but like any symbiotic relationship, breaking free is much harder than it seems.

The public often assumes that bankers are experts in banking. This is a reasonable assumption, but it's a misconception. Bankers tend to isolate themselves in industry and product "silos." A banker in the telecommunications industry might know everything about telecommunications companies (and their financing methods), but little about the banking industry itself. Those who dedicate their lives to serving the banking industry (i.e., "bankers' bankers," or the group of financial institutions (FIGs)) are a peculiar group, and generally disliked. They are "losers among losers."

Every investment banker, working late into the night on spreadsheets, dreams of escaping banking for private equity or startups. But FIG bankers are different. Their fate is sealed. Trapped in a golden "enslavement," they live in a self-imposed isolation, almost ignored by everyone else. Banking, serving banks, is philosophically profound, occasionally revealing a kind of beauty, but most of the time it remains invisible. Until the advent of decentralized finance (DeFi).

DeFi has made lending fashionable, and suddenly, every marketing genius at every fintech company feels entitled to comment on topics they barely understand. As a result, the ancient and serious discipline of "banking for banks" has resurfaced. If you come to DeFi or the crypto industry with a box of brilliant ideas about reshaping finance and understanding balance sheets, know that somewhere in London's Canary Wharf, on Wall Street, or in Basel, an unknown FIG analyst may have already conceived of these ideas two decades ago.

I was once a tormented "banker's banker." This article is my revenge.

Tether: Schrödinger's Stablecoin

It has been two and a half years since I last wrote about one of the most mysterious topics in the crypto world—Tether's balance sheet.

Few things have captured the industry’s imagination as much as the composition of USDT’s financial reserves. However, most of the discussion still revolves around whether Tether is “solvent” or “insolvent,” lacking a framework that could make the debate more meaningful.

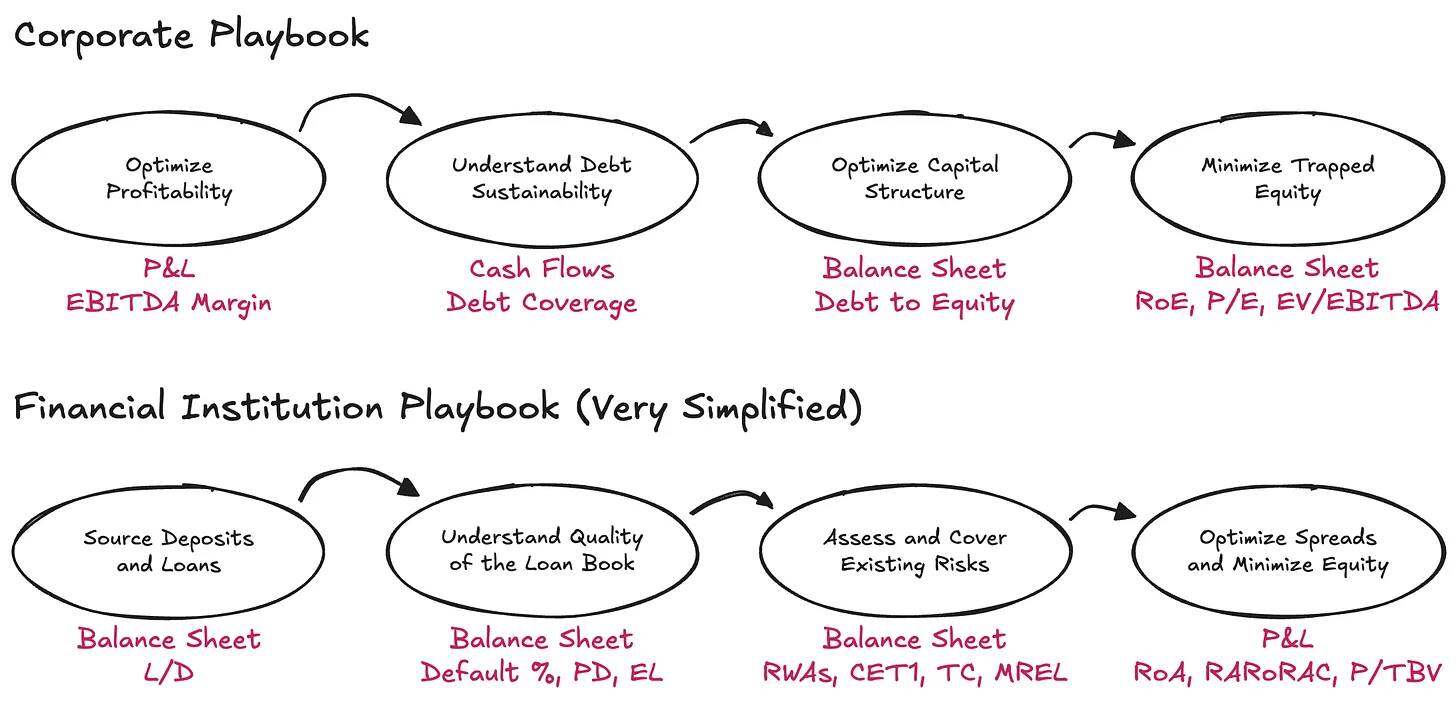

In traditional businesses, the concept of solvency has a clear definition: at least assets must match liabilities. However, when this concept is applied to financial institutions, its logic becomes less stable. In financial institutions, the importance of cash flow is downplayed, and solvency should be understood as the relationship between the amount of risk carried by the balance sheet and the liabilities owed to depositors and other financing providers. For financial institutions, solvency is more of a statistical concept than a simple arithmetic problem. If this sounds counterintuitive, don't worry—bank accounting and balance sheet analysis have always been among the most specialized areas in finance. It's both amusing and frustrating to see some people improvise their own solvency assessment frameworks.

In reality, understanding financial institutions requires overturning the logic of traditional businesses. The starting point for analysis is not the profit and loss statement (P&L), but the balance sheet—and cash flow must be ignored. Debt here is not a constraint, but rather the raw material for the business. What truly matters is the arrangement of assets and liabilities, whether there is sufficient capital to cope with risks, and whether it leaves enough returns for capital providers.

Tether (Tether) has recently become a hot topic again due to a report by S&P. While the report itself is simple and mechanical, its real appeal lies in the attention it has garnered, rather than the content itself. By the end of the first quarter of 2025, Tether had issued approximately $174.5 billion in digital tokens, the majority of which were stablecoins pegged to the US dollar, with a smaller amount of digital gold. These tokens offered eligible holders a 1:1 redemption right. To support these redemptions, Tether International, SA de CV held approximately $181.2 billion in assets, meaning its excess reserves were approximately $6.8 billion .

So, is this net asset value figure satisfactory enough? To answer this question (without creating a new customized valuation framework), we need to ask a more fundamental question first: What existing valuation framework should be applied? And to choose the right framework, we must start with the most fundamental observation: What kind of business is Tether?

A Day at the Bank

Essentially, Tether's core business is issuing on-demand digital deposit instruments that can circulate freely in the crypto market, while simultaneously investing these liabilities in a diversified asset portfolio. I deliberately chose the term "investment liabilities" rather than "holding reserves" because Tether doesn't simply hold these funds with the same risk/maturity; instead, it actively allocates assets and profits from the spread between its asset yields and the (nearly zero-cost) liabilities. All of this is done within a framework of broadly defined asset allocation guidelines.

From this perspective, Tether (USDT) is more like a bank than a simple money transfer institution—more precisely, an unregulated bank . In its simplest framework, a bank is required to hold a certain amount of economic capital (I will use "capital" and "net assets" synonymously, my FIG friends, please forgive me) to absorb the impact of expected and unexpected volatility in its portfolio, as well as other risks. This requirement exists for a reason: banks enjoy a state-granted monopoly on safeguarding the funds of households and businesses, and this privilege necessitates that banks provide corresponding buffers for potential risks on their balance sheets.

For banks, regulators are particularly focused on the following three aspects:

- Types of risks that banks need to consider

- Conforming to the nature of the definition of capital

- The amount of capital that banks must hold

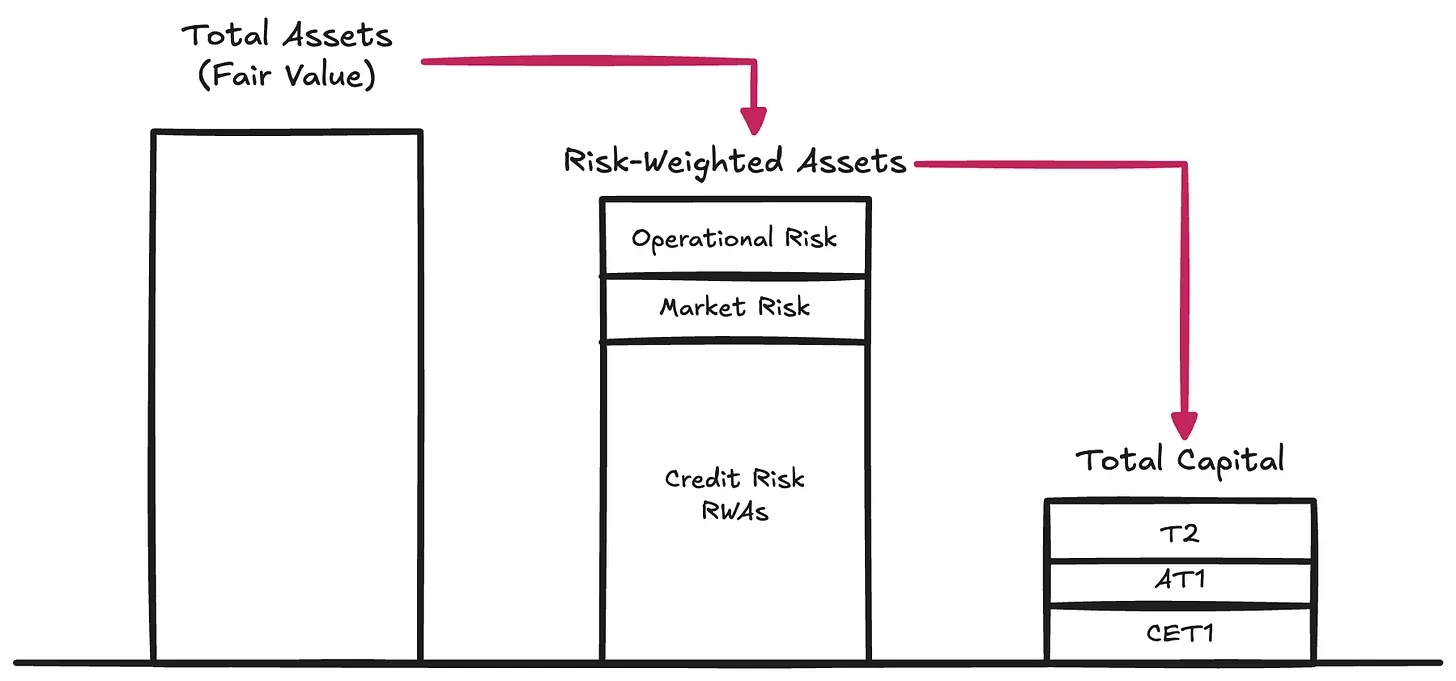

Risk Types → Regulators have defined various risks that could erode the redeemable value of bank assets, risks that will become apparent when the assets are ultimately used to pay off their liabilities:

Credit risk refers to the possibility that a borrower will fail to fully perform its obligations when required. This type of risk accounts for as much as 80%-90% of the risk-weighted assets of most global systemically important banks (G-SIBs).

Market risk refers to the risk that an asset's value may fluctuate adversely relative to the currency in which the liability is denominated, even in the absence of credit or counterparty deterioration. This could occur when depositors expect to redeem their assets in US dollars (USD), but the institution chooses to hold gold or Bitcoin ($BTC). Interest rate risk also falls into this category. This type of risk typically accounts for 2%-5% of risk-weighted assets.

Operational risk refers to the various potential risks faced by a business during its operations, such as fraud, system failures, legal losses, and various internal errors that may damage the balance sheet. This type of risk typically constitutes a small proportion of risk-weighted assets (RWAs) and is considered residual risk.

These requirements form the first pillar (Pillar I) of the Basel Capital Framework, which remains the dominant framework for defining prudent capital for regulated entities. Capital is the fundamental raw material for ensuring that balance sheets have sufficient value to cope with redemptions by liability holders (i.e., liquidity risk at typical redemption rates).

The Essence of Capital

Equity is expensive—as the most subordinate form of capital, equity is indeed one of the most expensive ways to finance a company. Over the years, banks have become extremely adept at using various innovative methods to reduce the amount of equity required and its cost. This has given rise to a range of so-called hybrid instruments, financial instruments that behave like debt in economic terms but are designed to comply with regulatory requirements and are thus considered equity capital. Examples include perpetual subordinated notes, which have no maturity date and can absorb losses; contingent convertible bonds (CoCos), which automatically convert to equity when capital falls below a trigger point; and Additional Tier 1 instruments, which can be completely written down under stress scenarios. We witnessed the role of these instruments in the Credit Suisse restructuring. Due to the widespread use of these instruments, regulators have differentiated the quality of capital. Common Equity Tier 1 (CET1) sits at the top, representing the purest and most loss-absorbing form of economic capital. Below it are other capital instruments with progressively lower purity.

However, for the purposes of our discussion, we can temporarily disregard these internal classifications and focus directly on the concept of **Total Capital**—the overall buffer used to absorb losses before liability holders face risks.

The amount of capital

Once banks have risk-weighted their assets (and categorized them according to regulatory definitions of capital), regulators require them to maintain minimum capital ratios for these risk-weighted assets (RWAs). Under Pillar I of the Basel Capital Framework, the classic minimum ratio requirements are as follows:

- Common Equity Tier 1 (CET1) : 4.5% of Risk-Weighted Assets (RWAs)

- Tier 1 capital : 6.0% of RWAs (including CET1 capital)

- Total Capital : 8.0% of RWAs (including CET1 and Tier 1 capital)

Building on this, Basel III also incorporates additional context-specific buffers:

- Capital Retention Buffer (CCB) : Increased by 2.5% for CET1.

- Countercyclical capital buffer (CCyB) : Increase by 0–2.5% depending on macroeconomic conditions.

- Global Systemically Important Banks Surcharge (G-SIB Surcharge) : An increase of 1–3.5% for systemically important banks.

In practice, this means that under normal Pillar I conditions, large banks must maintain a CET1 ratio of 7–12%+ and total capital of 10–15%+. However, regulators do not stop at Pillar I. They also implement stress testing regimes and, if necessary, add additional capital requirements (i.e., Pillar II). Therefore, the actual capital requirement can easily exceed 15%.

If you want to gain a deeper understanding of a bank’s balance sheet structure, risk management practices, and capital holdings, look at its Pillar III disclosures—and this is no joke.

For reference, data from 2024 shows that the average CET1 ratio of global systemically important banks (G-SIBs) was approximately 14.5%, and the total capital ratio was approximately 17.5% to 18.5% of risk-weighted assets.

Tether: An Unregulated Bank

We can now understand that the debates about whether Tether is "good" or "bad," whether it is "solvent" or "insolvent," and whether it reflects "fear and uncertainty" (FUD) or "fraud" have all missed the point. The real question is simpler and more structural: Does Tether hold sufficient total capital to absorb the volatility of its portfolio?

Tether has not released any disclosures similar to a Pillar III report (for reference, here is UniCredit's report); instead, it has only provided a brief reserve report—this is its latest version. While this information is extremely limited by Basel standards, it is sufficient to attempt a rough estimate of Tether's risk-weighted assets.

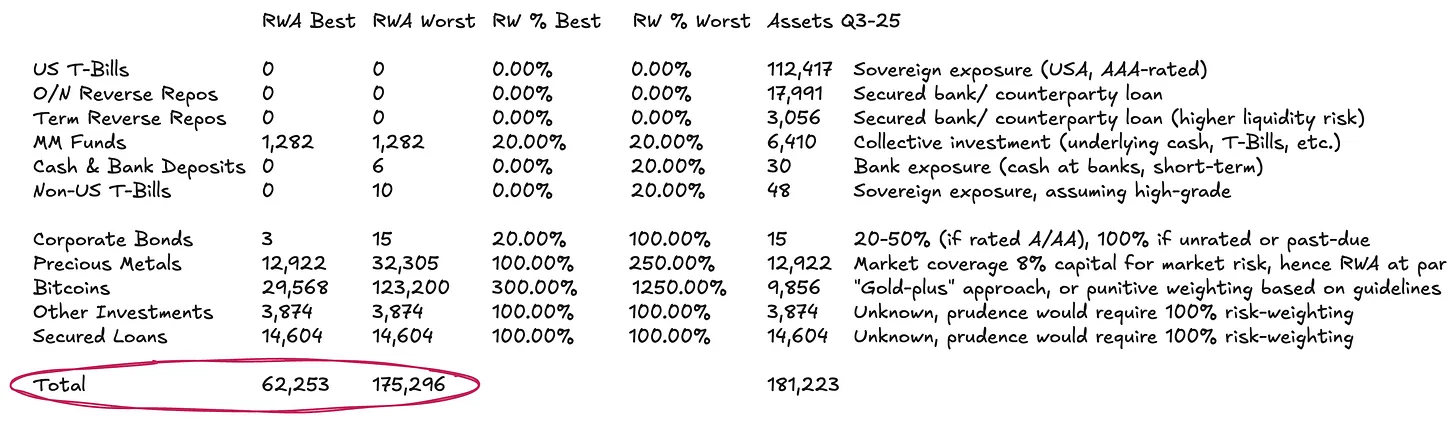

Tether's balance sheet is relatively simple:

- Approximately 77% of the investments are in money market instruments and other dollar-denominated cash equivalents—assets that, according to standardized approaches, require little or no risk weighting.

- Approximately 13% of the investment is in physical and digital goods.

- The remainder consists of loans and other miscellaneous investments that were not assessed in detail in the disclosure.

Risk-weighted classification (2) requires careful handling.

Under standard Basel guidelines, Bitcoin ($BTC) is assigned a risk weight of up to 1,250% . Combined with the 8% total capital requirement for risk-weighted assets (RWAs) (see above), this effectively means regulators require $BTC to be fully reserved—i.e., a 1:1 capital deduction—assuming it has absolutely no loss-absorbing capacity. We included this in our worst-case scenario, although this requirement is clearly out of step—especially for issuers with liabilities circulating in the crypto market. We believe $BTC should be viewed more consistently as a digital commodity.

Currently, there are clear frameworks and common practices for handling physical commodities (such as gold)—Tether holds a significant amount of gold: if it's directly custodied (as is the case with Tether's partial gold storage, and $BTC is likely to follow suit), there is no inherent credit or counterparty risk. The risk is purely market risk, as the liability is denominated in US dollars, not commodities. Banks typically hold 8%–20% of their capital in gold positions to buffer against price volatility—equivalent to a risk weight of 100%–250% . A similar logic can be applied to $BTC, but it needs to be adjusted for its drastically different volatility characteristics. Since the approval of Bitcoin ETFs, $BTC's annualized volatility has been 45%–70% , while gold's volatility has been 12%–15% . Therefore, a simple benchmark approach is to scale $BTC's risk weight approximately three times relative to gold's risk weight.

Risk-weighted classification (3) results in a completely opaque loan book. For loan portfolios, transparency is virtually zero. Given the lack of information such as borrowers, maturity dates, or collateral, the only reasonable option is to apply a 100% risk weight. Even so, this remains a relatively lenient assumption, given the complete absence of any credit information.

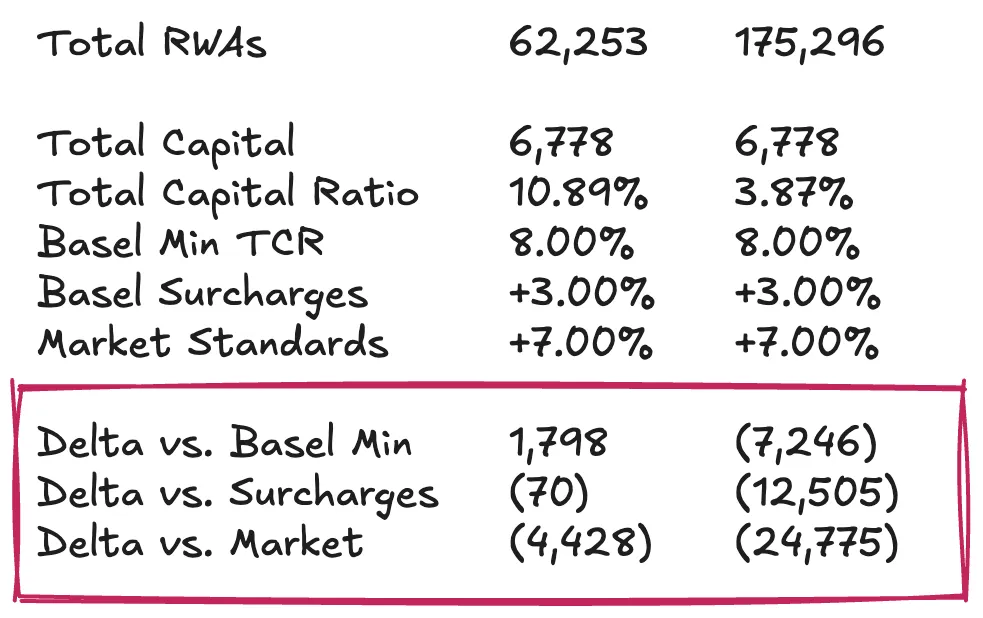

Based on the above assumptions, for Tether with total assets of approximately US$181.2 billion , its risk-weighted assets (RWAs) could range from approximately US$62.3 billion to US$175.3 billion , depending on how its commodity portfolio is treated.

Tether's capital status

Now, we can fill in the final piece of the puzzle by examining Tether's equity or excess reserves from the perspective of relative risk-weighted assets (RWAs). In other words, we need to calculate Tether's Total Capital Ratio (TCR) and compare it to regulatory minimums and market practices. This step of the analysis inevitably carries a degree of subjectivity. Therefore, my goal is not to provide a definitive conclusion on whether Tether has sufficient capital to reassure $USDT holders, but rather to offer a framework to help readers break down this issue into easily understandable parts and form their own assessment in the absence of a formal prudential regulatory framework.

Assuming Tether's excess reserves are approximately $6.8 billion , its Total Capital Adequacy Ratio (TCR) will fluctuate between 3.87% and 10.89% , depending primarily on how we handle its $BTC exposure and our level of conservatism regarding price volatility. In my view, while fully reserving $BTC aligns with the most stringent Basel interpretation, it appears overly conservative. A more reasonable baseline assumption is to hold sufficient capital buffers to withstand 30%-50% price volatility in $BTC, a range well within the historical fluctuation range.

Under the aforementioned baseline assumptions, Tether's collateral level generally meets the minimum regulatory requirements. However, compared to market benchmarks (such as well-capitalized large banks), its performance is less satisfactory. By these higher standards, Tether might require an additional $4.5 billion in capital to maintain its current $USDT issuance. With a more stringent, fully punitive approach to $BTC, the capital shortfall could be between $12.5 billion and $25 billion . I believe this requirement is overly demanding and ultimately does not meet practical needs.

Independent vs. Group: Tether's Refutations and Controversies

Tether's standard rebuttal on the collateral issue is that, from a group-level perspective, it has a substantial amount of retained earnings as a buffer. These figures are indeed impressive: as of the end of 2024, Tether reported annual net profits exceeding $13 billion , with a group equity exceeding $20 billion . The more recent third-quarter audit for 2025 shows that its year-to-date profit has already exceeded $10 billion .

However, a counter-argument to this is that, strictly speaking, these figures cannot be considered regulated capital for $USDT holders. These retained earnings (on the liability side) and proprietary investments (on the asset side) belong to the group level and are outside the scope of segregated reserves. While Tether has the capacity to allocate these funds to the issuing entity in the event of problems, it has no legal obligation to do so. It is this liability segregation arrangement that gives management the option to inject capital into the token business if necessary, but this does not constitute a hard commitment. Therefore, considering the group's retained earnings as capital fully available to absorb $USDT losses is an overly optimistic assumption.

A rigorous assessment requires examining the group's balance sheet, including its holdings in renewable energy projects, Bitcoin mining, artificial intelligence and data infrastructure, peer-to-peer telecommunications, education, land, and gold mining and concession companies. The performance and liquidity of these risky assets, and whether Tether is willing to sacrifice them in times of crisis to protect the interests of token holders, will determine the fair value of its equity buffer.

If you're expecting a definitive answer, I'm sorry to say you might be disappointed. But that's exactly Dirt Roads ' style: the journey itself is the greatest reward.