Stop packaging high-risk investments as stablecoins.

- 核心观点:派息稳定币实为高风险理财产品。

- 关键要素:

- xUSD闪崩88%,暴露5亿美元风险。

- 项目使用4倍杠杆,资产不透明。

- DeFi借贷协议Curator助推风险扩散。

- 市场影响:引发DeFi市场挤兑和信任危机。

- 时效性标注:短期影响。

Original author: Sleepy.txt

The world of stablecoins is never short of stories, but it lacks respect for risk. In November, stablecoins ran into trouble again.

A "stablecoin" called xUSD experienced a flash crash on November 4th, plummeting from $1 to $0.26. As of today, it continues to fall, having dropped to $0.12, wiping out 88% of its market capitalization.

Image source: Coingecko

The project that ran into trouble was Stream Finance, a high-profile project that managed $500 million in assets.

They packaged their high-risk investment strategy as the dividend-paying stablecoin xUSD, claiming it was "pegged to the US dollar and automatically generates interest," essentially just incorporating investment returns into it. However, any investment strategy cannot guarantee perpetual profits. On October 11th, the day of the crypto market crash, their off-chain trading strategy failed, resulting in a loss of $93 million, equivalent to approximately 660 million RMB. This amount is enough to buy more than forty 100-square-meter apartments within Beijing's Second Ring Road.

A month later, Stream Finance announced the suspension of all deposits and withdrawals, and the xUSD price was decoupled.

Panic spread rapidly. According to research firm Stablewatch, over $1 billion fled various dividend-paying stablecoins in the following week. This is equivalent to a run on all deposits in a mid-sized city commercial bank within seven days.

Alarms are sounding throughout the DeFi investment market. In some protocols, borrowing rates have even reached a staggering -752%, meaning that collateral has become worthless and no one will repay the money to redeem it, plunging the market into chaos.

All of this stems from a seemingly attractive promise: stability and high interest rates.

When the illusion of "stability" is shattered by a large bearish candlestick, we must re-examine which stablecoins are truly stablecoins, which are just high-risk investments disguised as stablecoins, and why high-risk investments can now brazenly call themselves "stablecoins".

The Emperor's New Clothes

In the world of finance, the most beautiful masks often conceal the sharpest fangs. Stream Finance and its stablecoin xUSD are a prime example.

It claims that xUSD uses a "Delta-neutral strategy." This is a complex term originating from the professional trading field, designed to hedge against the risk of market volatility through a series of sophisticated financial instruments, which sounds very safe and professional. The project's narrative is that users can obtain stable returns regardless of market fluctuations.

In just a few months, it attracted as much as $500 million in investment. However, stripped of its facade, according to on-chain data analysts, xUSD's true operating model is riddled with flaws.

First, there's the extreme lack of transparency. Of the claimed $500 million in assets, less than 30% can be traced on the blockchain; the remaining "Schrödinger's $350 million" operates entirely in the shadows. Nobody knew what was happening inside this black box until the moment it collapsed.

Secondly, there was the astonishingly high leverage. The project team used only $170 million in real assets to leverage up to $530 million in loans through repeated collateralization and lending on other DeFi protocols, resulting in a real leverage ratio of over 4 times.

What does this mean? You think you're exchanging for a firmly pegged "digital dollar," and you're dreaming of a stable high annual interest rate of over ten percent. In reality, you're buying LP shares of a 4x leveraged hedge fund, and you can't even see 70% of the fund's holdings.

What you perceive as "stability" is actually your money being traded at extremely high frequency in the world's largest digital casino.

This is precisely where the most dangerous aspect of these "stablecoins" lies. They use the label of "stable" to mask their true nature as "hedge funds." They promise ordinary investors the security of bank savings, but at their core, they operate with high-risk strategies that only the most professional traders can manage.

Following the incident, Deddy Lavid, CEO of blockchain security company Cyvers, commented: "Even if the protocol itself is secure, external fund managers, off-chain custody, and human oversight remain critical weaknesses. This Stream crash was not a code problem, but a human problem."

This viewpoint hits the nail on the head. The root of Stream Finance's problem lies in the fact that the project team has carefully packaged an extremely complex, high-risk, and unregulated financial game as a "stable investment product" that ordinary people can easily participate in.

Dominoes

If Stream Finance manufactured a bomb, then Curator, a DeFi lending product, became the courier of that bomb, ultimately leading to a far-reaching chain of explosions.

In emerging lending protocols like Morpho and Euler, Curator acts as a "fund manager." They are mostly professional investment teams responsible for packaging complex DeFi strategies into "strategy vaults," allowing ordinary users to deposit funds with a single click and enjoy returns, much like buying wealth management products on a bank app. Their main income comes from a percentage of user earnings as performance fees.

In theory, they should be professional risk gatekeepers, helping users screen for high-quality assets. However, their performance fee business model has also laid the groundwork for them to pursue high-risk assets. Because in the extremely competitive DeFi market, higher annualized returns mean attracting more users and funds, thereby earning more performance fees.

When Stream Finance, an asset packaged as "stable and high-yield," appeared, it immediately became a hot commodity in the eyes of many Curators.

The Stream Finance incident exemplifies this worst-case scenario. On-chain data tracking reveals that several prominent Curators, including MEV Capital, Re7 Labs, and TelosC, have heavily invested in high-risk xUSD across their vaults on protocols like Euler and Morpho. TelosC alone has a risk exposure of $123 million.

More importantly, this configuration was not an unintentional mistake. Evidence suggests that several industry KOLs and analysts had publicly warned of transparency and leverage risks associated with xUSD in the days leading up to the incident, but these Curators, who held substantial funds and should have been primarily responsible for the risks, chose to ignore them.

However, some Curators themselves were also victims of this packaging scam. K3 Capital was one of them. This Curator, which managed millions of dollars in assets through the Euler protocol, lost $2 million in the explosion.

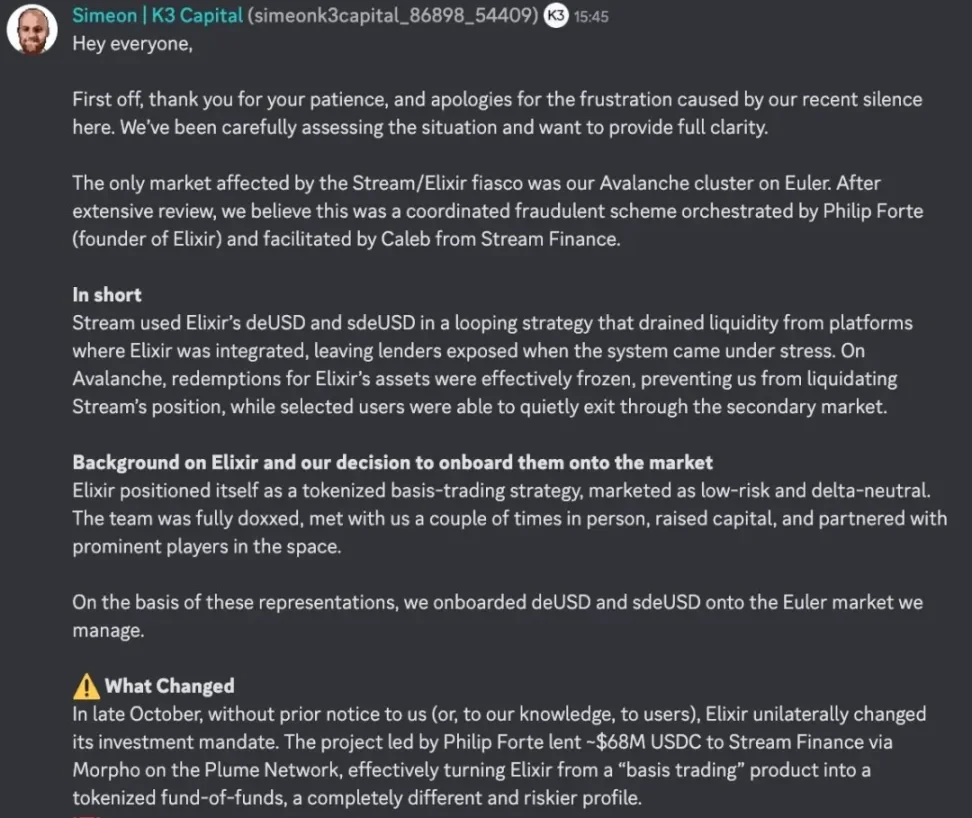

On November 7, the founder of K3 spoke out publicly on Euler's Discord channel, revealing how they were scammed.

Image source: Discord

The story begins with another "stablecoin" project. Elixir is a project that issues a dividend-paying stablecoin called deUSD. It claims to use a "basis trading strategy," and K3 allocated deUSD in its managed vaults based on this promise.

However, in late October, without any Curator's consent, Elixir unilaterally changed its investment strategy, lending approximately 68 million USDC to Stream Finance through Morpho, turning basis trading into a nested investment scheme.

These are completely different products. Basis trading involves direct investment in a specific trading strategy, making the risk relatively controllable. In contrast, nested investment products involve lending money to another investment product, effectively adding another layer of risk on top of the existing high risk.

When Stream's bad debts were made public on November 3rd, K3 immediately contacted Elixir founder Philip Forte, demanding a guarantee of a 1:1 liquidation of deUSD. However, Philip remained silent and offered no response. Left with no other option, K3 forced a liquidation on November 4th, leaving behind $2 million in deUSD. Elixir announced insolvency on November 6th, offering a solution where retail investors and those in liquidity pools could exchange their deUSD for USDC at a 1:1 ratio, but deUSD held in Curator's vault would not be exchanged, requiring everyone to negotiate a solution.

Currently, K3 has hired top U.S. lawyers and is preparing to sue Elixir and Philip Forte for unilaterally changing terms and making false claims, demanding compensation for damage to its reputation and forcing the exchange of deUSD back to USDC.

When the gatekeepers themselves start selling risk, the fall of the entire fortress is only a matter of time. And when the gatekeepers themselves fall for it, who can be expected to protect the users?

Same old wine in new bottles

This "packaging-diffusion-collapse" pattern is so familiar in financial history.

Whether it's LUNA, which evaporated $40 billion in 72 hours in 2022 with its "algorithmic stability, 20% annualized return" narrative, or even earlier in 2008, when Wall Street elites packaged a bunch of high-risk subprime mortgages into AAA-rated "CDOs" through complex financial engineering, ultimately triggering the global financial crisis, the core principle remains strikingly consistent: to complexly package high-risk assets to make them appear as low-risk products, and then sell them through various channels to investors who cannot fully understand the risks behind them.

From Wall Street to DeFi, from CDOs to "dividend-paying stablecoins," the technology changes, the names change, but human greed remains unchanged.

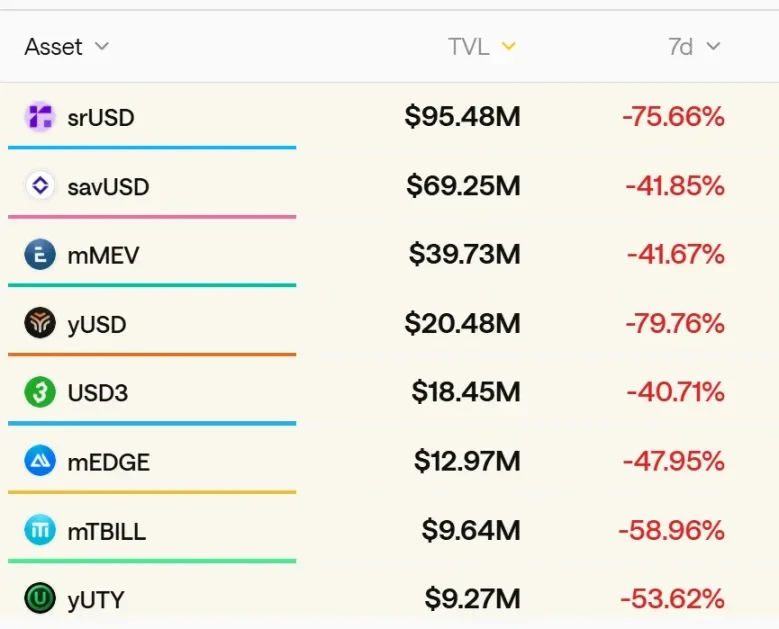

According to industry data, there are currently over 50 similar dividend-paying stablecoin projects operating in the DeFi market, with a total locked value exceeding $8 billion. Most of them use various complex financial engineering techniques to package high-leverage, high-risk trading strategies into stable and high-yield financial products.

Image source: stablewatch

The root of the problem lies in the fact that we've given these products the wrong name. The term "stablecoin" creates a false sense of security and a numbness to risk. When people see stablecoins, they think of dollar reserve assets like USDC and USDT, not a highly leveraged hedge fund.

A lawsuit can't save a market, but it can wake it up. When the tide goes out, we should see not only those who are swimming naked, but also those who never intended to wear swim trunks in the first place.

$8 billion, 50 projects, the next Stream could appear at any moment. Until then, remember this simple common sense: when a product needs to attract you with extremely high annualized returns, it is bound to be unstable.