What is the role of Curator in DeFi? Could it be a hidden trap in this cycle?

- 核心观点:Curator模式存在巨大潜在风险。

- 关键要素:

- Curator资金池规模超80亿美元。

- 盈利模式驱动Curator追逐高风险策略。

- 用户缺乏风险认知,盲目追求高收益。

- 市场影响:可能引发系统性风险事件。

- 时效性标注:中期影响

Original article | Odaily Planet Daily ( @OdailyChina )

Author|Azuma ( @azuma_eth )

The sudden occurrence of two major security incidents (Balancer and Stream Finance) has once again brought the issue of DeFi security to the forefront. In particular, the Stream Finance incident exposed the huge potential risks of Curator, a player who has become a significant player in the DeFi market.

The term "Curator" primarily exists within DeFi lending protocols (such as Euler and Morpho, which were affected by the Stream incident). It typically refers to an individual or team responsible for designing, deploying, and managing specific "strategic vaults." Curators generally encapsulate relatively complex yield strategies into easy-to-use vaults, allowing ordinary users to "deposit with one click and earn interest." The Curator, on the other hand, determines the specific yield strategies for assets in the backend, such as asset allocation weights, risk management, rebalancing cycles, withdrawal rules, and so on.

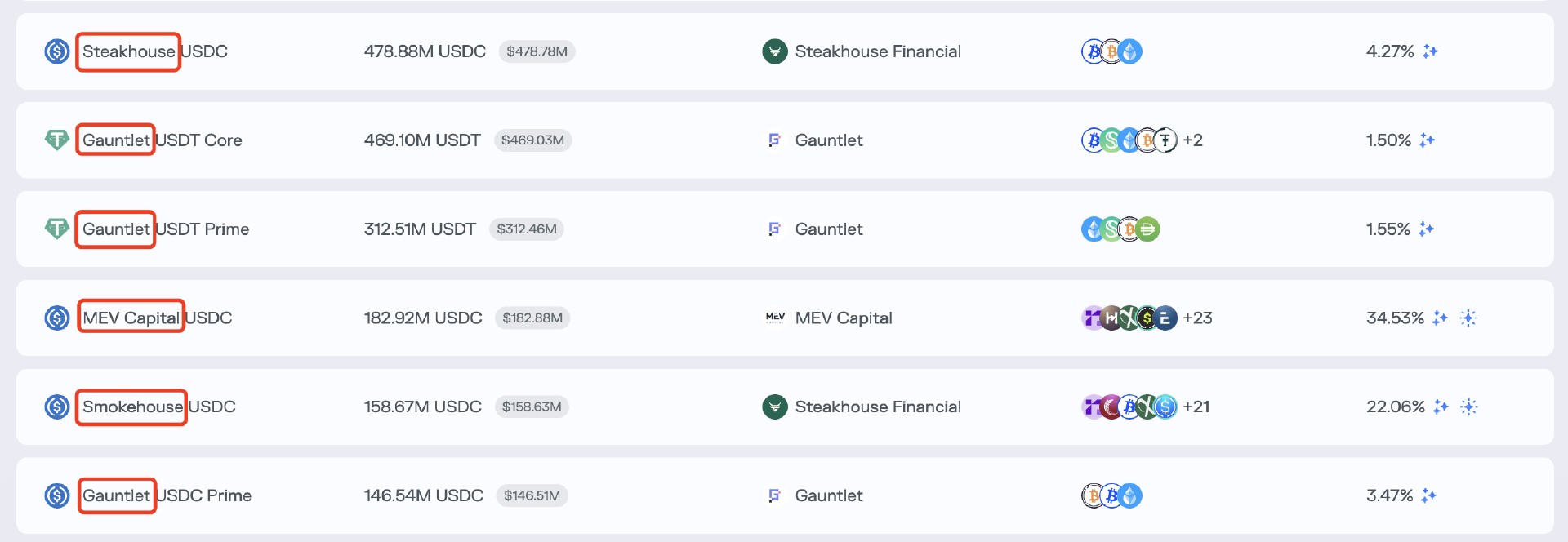

- Odaily Note: The image above shows the Curator fund pool on Morpho. The Steakhouse, Gauntlet, etc. in the red box are the names of the Curator entities, indicating that the entity is responsible for designing, deploying, and managing the fund pool.

Unlike traditional centralized wealth management services, Curator does not have direct access to or control over user funds. Assets deposited by users into the lending protocol will always be stored in a non-custodial smart contract. Curator's authority is limited to configuring and executing policy operations through the contract interface, and all operations must be subject to the contract's security restrictions.

Market demand for Curator

Curator's original intention was to leverage its professional strategy management and risk control capabilities to bridge the supply and demand mismatch in the market— on the one hand, to help ordinary users who are struggling to keep up with the increasing complexity of DeFi to amplify their returns; on the other hand, to help lending protocols expand their TVL while reducing the probability of systemic events.

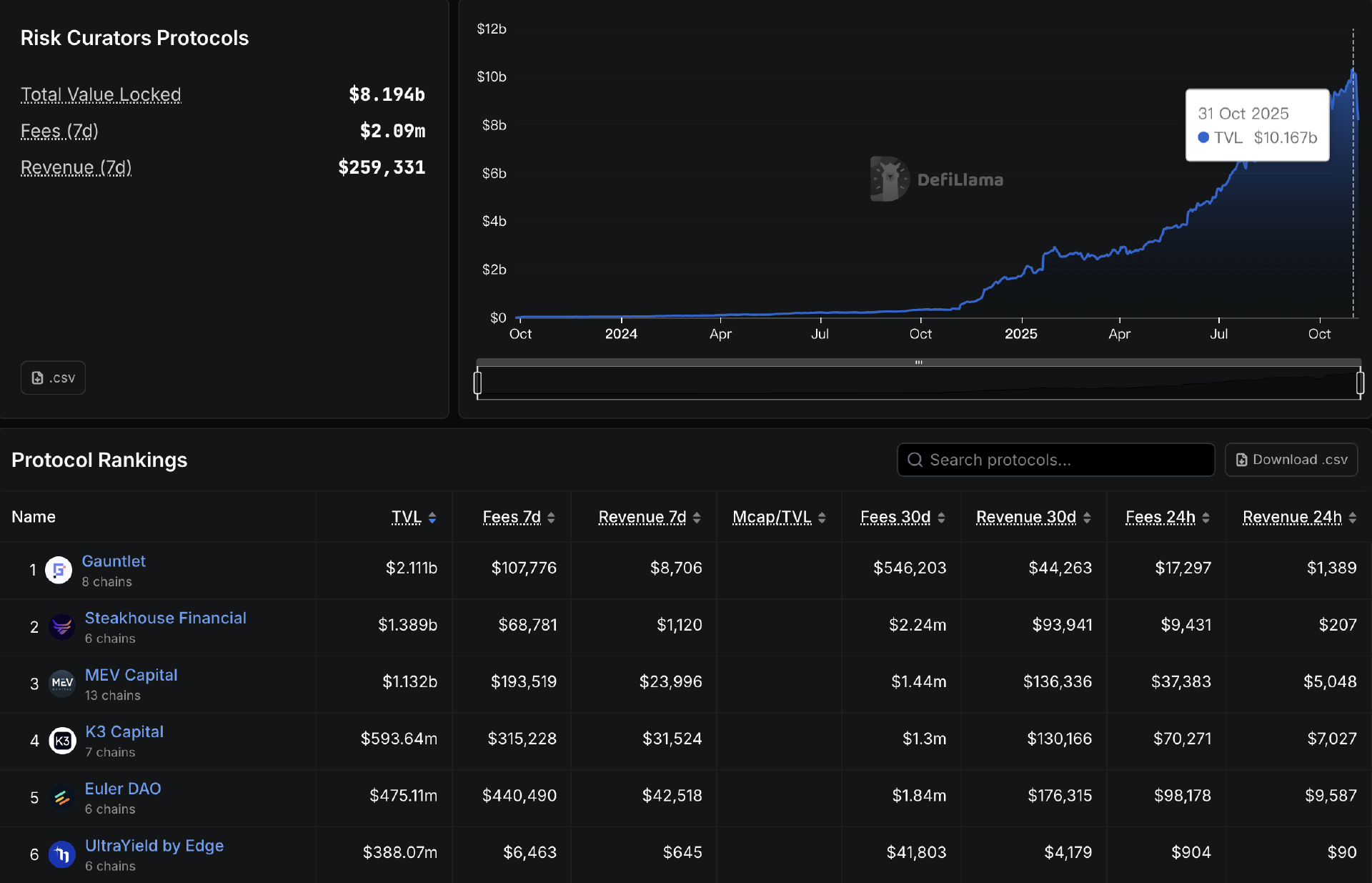

Because Curator's managed funds often offer more attractive returns than classic lending markets like Aave, this model naturally attracts capital. Defillama data shows that the total size of Curator-managed funds has grown rapidly over the past year, briefly exceeding $10 billion on October 31, and is currently reported at $8.19 billion.

Amidst fierce competition, Gauntlet, Steakhouse, MEV Capital, and K3 Capital have gradually emerged as some of the largest Curators in terms of assets under management, each managing massive sums in the hundreds of millions. Meanwhile, lending protocols like Euler and Morpho, which primarily utilize the Curator pooling model, have also achieved rapid growth in their total value of loans (TVL), successfully securing a leading position in the market.

Curator's profit model

Having seen this, Curator's role seems quite clear, and it also has sufficient market demand. So why is it a potential risk threatening the DeFi world right now?

Before analyzing the risks, we need to understand Curator's profit logic. Curator primarily relies on the following methods to generate revenue:

- Performance sharing : After the strategy generates profits, Curator receives a certain percentage of the net profit.

- Fund management fee : Based on the total assets of the fund pool, it is charged at a certain annualized rate.

- Protocol Incentives and Subsidies : Lending protocols typically incentivize Curator with tokens to encourage the creation of new, high-quality strategies;

- Brand-derived revenue : For example, Curator can launch its own products or even tokens after establishing its brand.

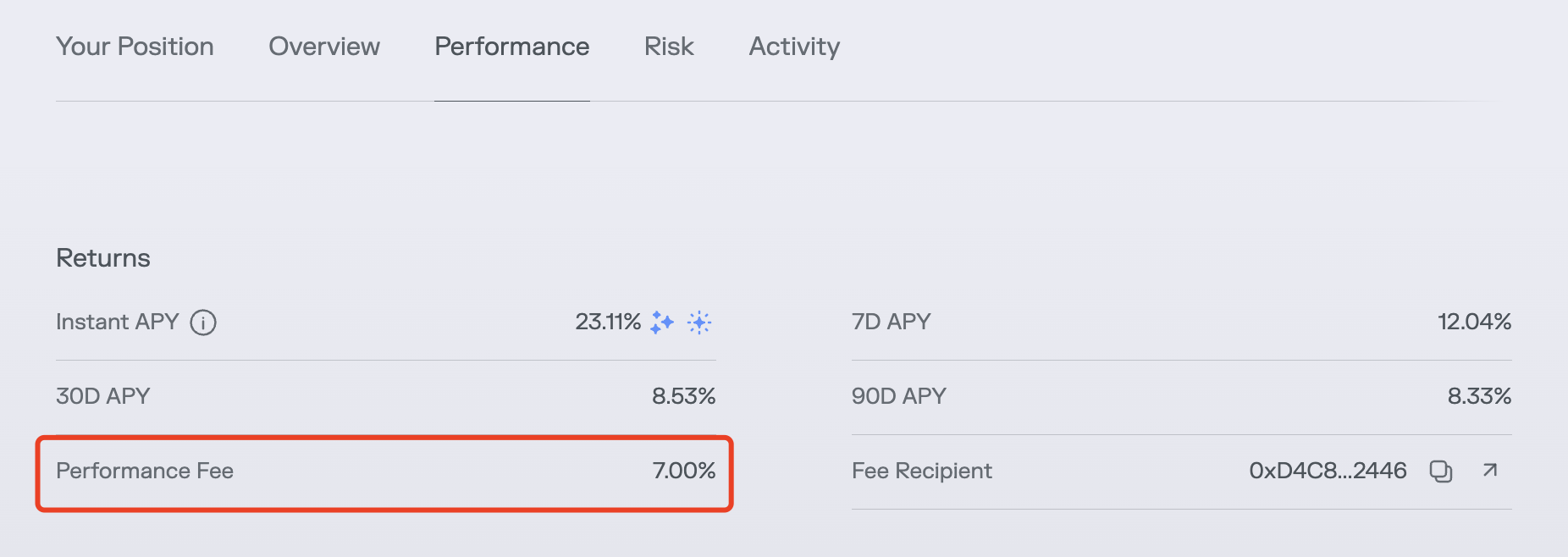

In reality, performance-based revenue sharing is the most common source of income for Curators. As shown in the diagram below, Morpho charges a 7% performance-based share for the USDC liquidity pool managed by MEV Capital on the Ethereum mainnet.

This profit model dictates that the larger the pool of funds managed by Curator and the higher the strategy's return rate, the greater Curator's profit will be . Of course, theoretically, Curator could also increase revenue by increasing the commission rate, but in the face of relatively fierce market competition, no Curator dares to arbitrarily take away profits from users.

At the same time, since most depositors are not sensitive to Curator's brand differences, their choice of which pool to deposit into often depends solely on the apparent APY figure. This makes the attractiveness of the pool directly linked to the strategy yield, thus making the strategy yield the core factor ultimately determining Curator's profitability.

Driven by yields, risks are gradually being overlooked.

Astute readers may have already sensed that a problem is brewing. In a yield-driven model, Curators can only achieve higher profits by constantly seeking "opportunities" with higher yields. Since yield and risk are often positively correlated, some Curators gradually overlook the safety issues that should be their primary concern and choose to take risks—"Anyway, the principal belongs to the users, and the profits are mine."

Taking Stream Finance as an example, a key reason for such a large-scale impact was that some Curators on Euler and Morpho (including well-known brands such as MEV Capital and Re7) ignored the risks and allocated funds to Stream Finance's xUSD market , which directly affected users who deposited funds into the relevant Curator pools, and subsequently caused bad debts in the lending protocol itself, indirectly expanding the scope of the impact.

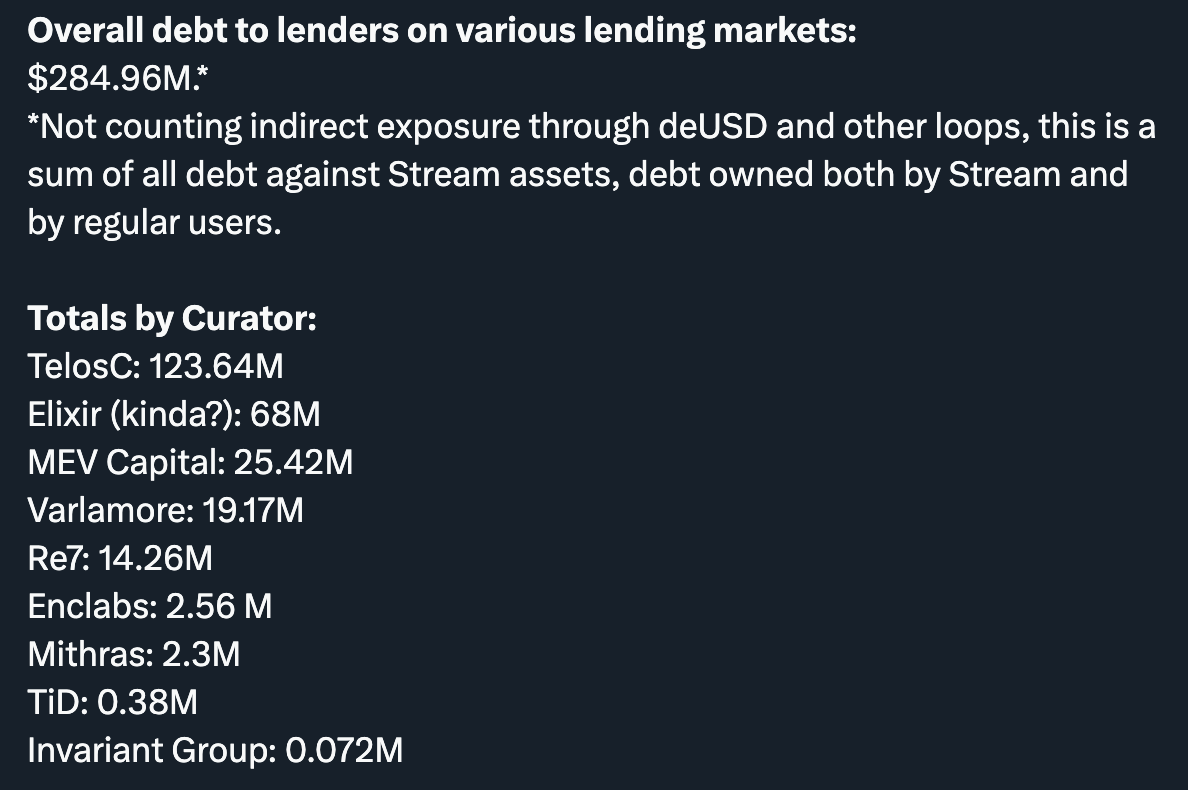

- Odaily Note: The image shows a summary of the debt positions of various Curators in the Stream Finance incident by the DeFi community YAM.

Several days before the Stream Finance incident, several KOLs and institutions, including CBB (@Cbb0fe), had warned of potential transparency and leverage risks associated with xUSD, but these Curators clearly chose to ignore them.

Of course, not all Curators were affected by Stream Finance. Several leading Curators, such as Gauntlet, Steakhouse, and K3 Capital, never deployed funds to xUSD. This shows that professional entities like Curators are capable of identifying and avoiding potential risks when they effectively fulfill their security responsibilities.

Will Curator pose even greater risks?

Following the Stream Finance incident, Curator and its potential risks and impacts have attracted even more attention.

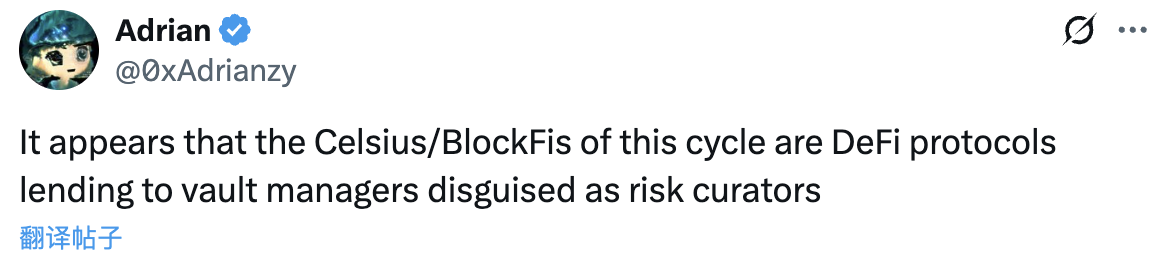

Chorus One investment analyst Adrian Chow, in an article published on X, directly compared Curator and its related lending protocols to Celsius and BlockFi in this cycle. Indeed, from a purely data perspective, Curator's pool of funds, with a total value exceeding $8 billion, already has an impact comparable to the black swan events of the previous cycle, and Curator's widespread presence across mainstream lending protocols also implies a significant scope of influence.

Will Curators trigger a larger-scale risk event in this cycle? This is a difficult question to answer. From the original intention of Curators, their role was supposed to be to reduce individual risk for ordinary users through their professional management capabilities. However, their business model and profit path make Curators themselves an easy entry point for concentrated risk. For example, if multiple lending protocols in the market rely on a few Curators, and their models experience unexpected deviations (such as oracle price errors), all parameters will be misadjusted simultaneously, thus affecting multiple liquidity pools at once.

Another point worth mentioning is that, in the current market environment, many users who deposit money into lending agreements are not even fully aware of the role or existence of Curators, simply believing that they are investing their funds in a well-known lending agreement to earn interest. This leads to the role and responsibility of Curators being obscured. When incidents occur, it is the lending agreement that directly faces the anger and accountability of users, which further encourages some Curators to pursue profits too aggressively.

Arthur, founder of DeFiance Capital, also commented on this phenomenon yesterday: "This is why I've always been skeptical of Curator-based DeFi lending models. Lending platforms bear reputational risk and a responsibility to care for their users, and whether they like it or not, a few poorly managed, unethical Curators can negatively impact the platform. "

I personally do not believe that using Curator to maintain a fund pool is a failed business model, and I do have funds in some Curator fund pools (currently only Steakhouse remains). However, I also agree that the aggressive tendencies of some Curators may breed a wider range of risks. The deeper reason for this situation lies in the lack of risk control by the user group and some Curators. Furthermore, due to the profit-driven motives mentioned above, the latter may have certain subjective factors.

While we consistently urge users to evaluate protocols, pools, and strategy configurations themselves, this is clearly difficult to achieve because most users lack the time, expertise, or willingness to do so. Against this backdrop, many users unknowingly invest in Curator pools, which generally offer higher yields, thus driving the rapid growth of Curator's assets under management. Conversely, some Curators cleverly exploit this situation to attract more funds, employing more aggressive strategies to increase pool yields, thereby drawing in even more capital through higher returns.

How can we improve the current situation?

Growth always involves growing pains. While the Stream Finance incident dealt another heavy blow to the DeFi market, it may also become an opportunity for users to increase their understanding of Curators and for the market to improve its constraints on Curator behavior.

From a user's perspective, we still recommend that users conduct as much independent research as possible. Before investing funds in a specific Curator fund pool, users should pay attention to the reputation of the Curator entity and the design of the fund pool. Research methods include, but are not limited to:

- Are there any publicly available risk models or stress test reports?

- Are the access boundaries transparent? Are they subject to multi-signature or governance restrictions?

- How often did the strategies draw down in the past, and how did they perform in extreme market conditions?

- Has there been a third-party audit?

- Does the incentive mechanism align with the interests of users?

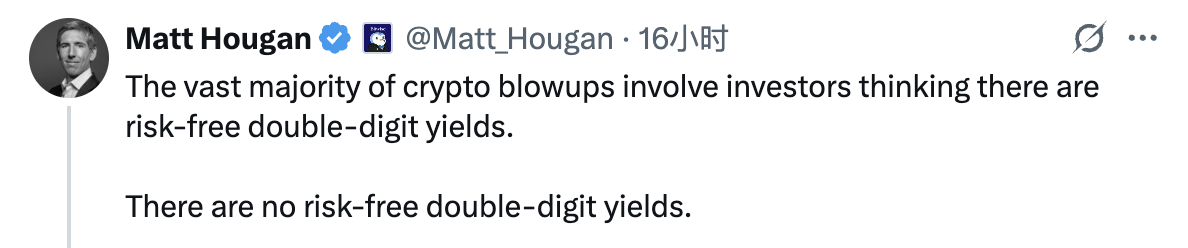

Most importantly, users need to realize that risk is always positively correlated with return. Before making investment decisions, they should be prepared for the most extreme scenarios. They can always keep in mind this quote from Matt Hougan, Chief Investment Officer of Bitwise: " The vast majority of cryptocurrency crashes are due to investors being misled by double-digit risk-free returns, when there is no such thing as a risk-free double-digit return in the market."

As for Curators, they need to simultaneously improve their risk awareness and risk management capabilities. DeFi research firm Tanken Capital has summarized the basic risk control requirements for an excellent Curator, which specifically include:

- Possess compliance awareness in the traditional financial sector;

- Portfolio risk management and return optimization;

- Learn about new tokens and DeFi mechanisms;

- Understand oracles and smart contracts;

- It has the ability to monitor the market and perform intelligent reconfiguration.

As for the lending agreement directly associated with Curator, it should continuously optimize the constraints on Curator by requiring Curator to disclose its strategy model, independently verify the model with data, introduce a staking penalty mechanism to maintain accountability for Curator, and regularly evaluate Curator's performance and decide whether to replace it. Only through continuous and proactive monitoring, and by minimizing the risk space, can the risk resonance of the entire system be more effectively avoided.