Bitcoin is in deep consolidation: a breakthrough path in the critical stage of Q4

- 核心观点:比特币市场面临需求枯竭与结构性疲软。

- 关键要素:

- 比特币跌破短期持有者成本基础。

- 长期持有者加速抛售超2.2万BTC/日。

- 期权市场看跌情绪浓厚,对冲行为盛行。

- 市场影响:可能进入更长期盘整,抑制反弹。

- 时效性标注:中期影响

Original article by Chris Beamish, CryptoVizArt, Antoine Colpaert, and Glassnode

Original translation: AididiaoJP, Foresight News

Bitcoin is trading below a key cost basis level, signaling exhausted demand and waning momentum. Long-term holders are selling on market strength, while the options market has shifted to a defensive posture with rising demand for put options and elevated volatility, signaling a period of caution before any sustainable recovery.

summary

- Bitcoin is trading below its cost basis for short-term holders, signaling weakening momentum and growing market fatigue. Repeated failures to reclaim the upper bound increase the risk of a longer-term consolidation phase.

- Long-term holders have accelerated their selling since July, now exceeding 22,000 BTC per day, signaling persistent profit-taking that continues to weigh on market stability.

- Open interest is at a record high, but market sentiment is bearish as traders favor puts over calls. A short-term rally is being met with hedging rather than renewed optimism.

- Implied volatility remains elevated while realized volatility has caught up, ending a period of calm and low volatility. Market makers’ short positions amplified the sell-off and dampened the rebound.

- Both on-chain and options data suggest the market is in a cautious transition phase. Market recovery may depend on the emergence of new spot demand and easing volatility.

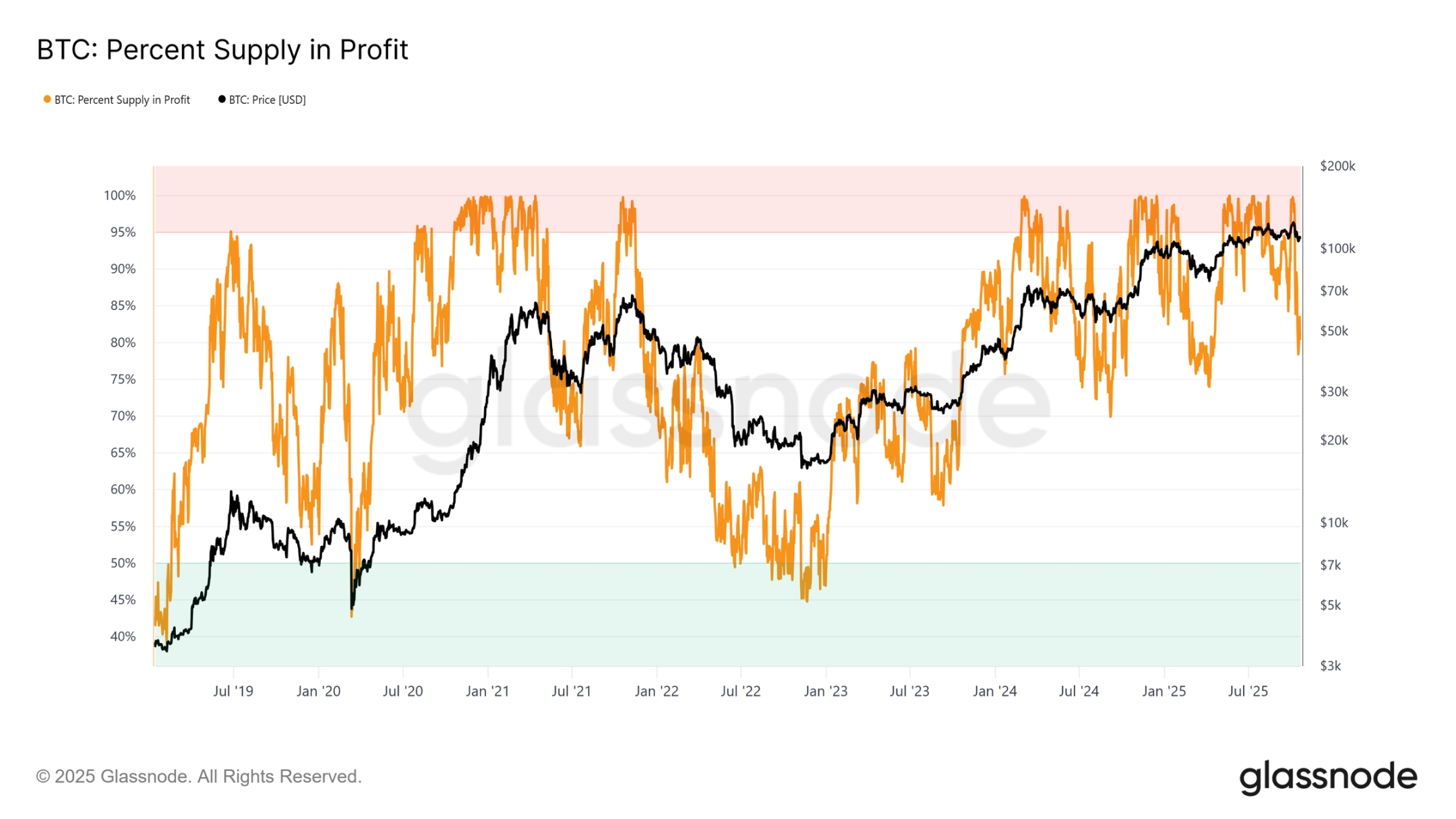

Bitcoin has gradually retreated from its recent all-time highs, stabilizing below the short-term holder cost basis at approximately $113,000. Historically, this structure often signals the beginning of a medium-term bearish phase as weaker holders begin to capitulate.

In this issue, we assess the market's current earnings landscape, examine the scale and persistence of spending by long-term holders, and finally evaluate options market sentiment to determine whether this pullback is a healthy consolidation or a harbinger of deeper weakness to come.

On-chain insights

Testing Faith

Trading near the short-term holders' cost basis marks a critical phase where the market tests the conviction of those who bought near recent highs. Historically, a break below this level after setting an all-time high has caused the profitable supply percentage to fall to approximately 85%, meaning that more than 15% of the supply is trading at a loss.

We have witnessed this pattern for the third time in the current cycle. If Bitcoin fails to reclaim above approximately $113.1k, a deeper contraction could push a larger portion of supply into losses, exacerbating near-term buyer pressure and potentially setting the stage for broader market capitulation.

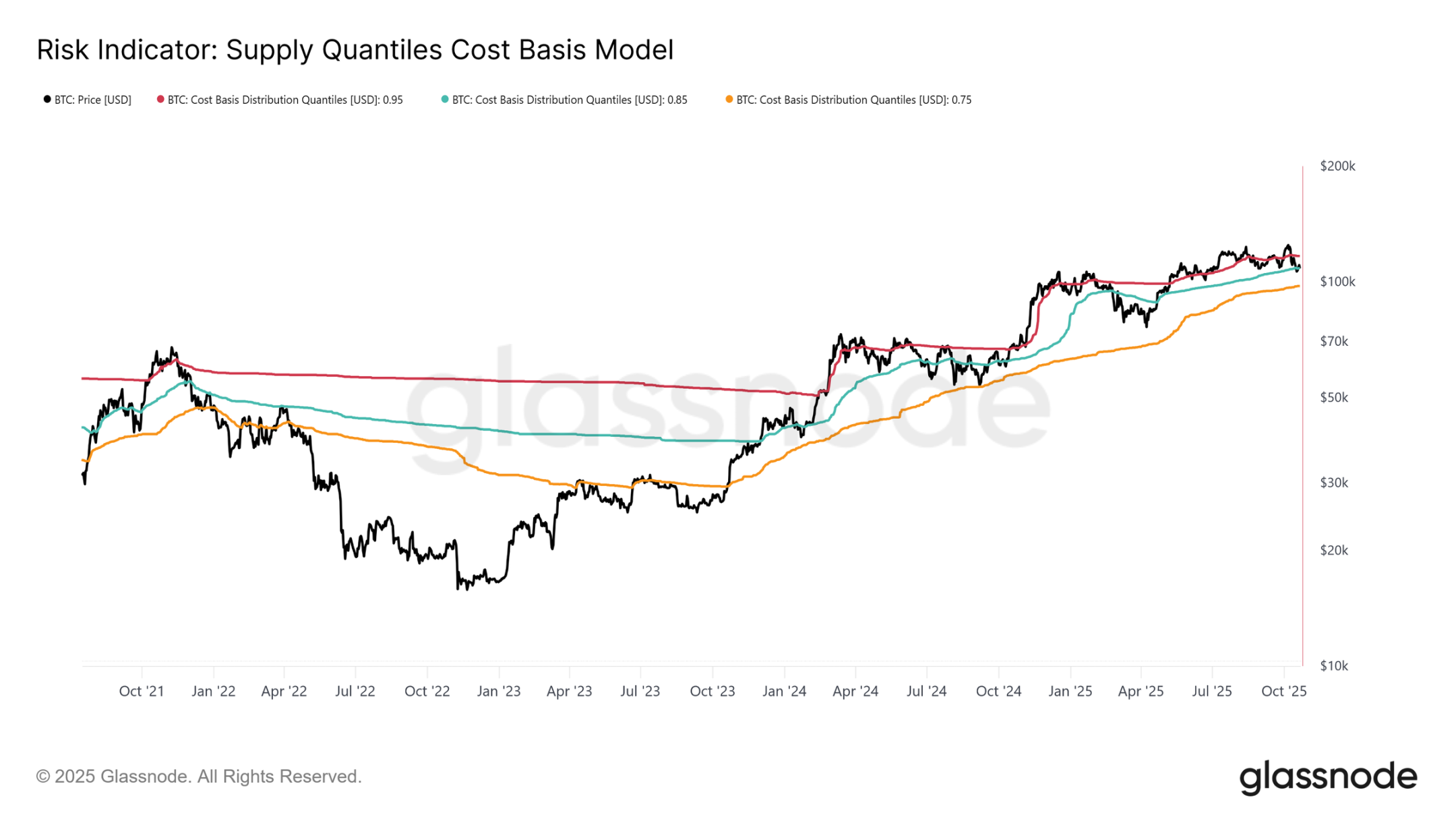

Critical thresholds

To further understand this structure, it's key to understand why regaining short-term holder cost basis is crucial to sustaining a bullish phase. The Supply Quantile Cost Basis Model provides a clear framework by mapping the 0.95, 0.85, and 0.75 quantiles, indicating levels where 5%, 15%, and 25% of supply are in the red, respectively.

Currently, Bitcoin is not only trading below the short-term holder cost basis ($113.1k), but is also struggling to hold above the 0.85th percentile at $108.6k. Historically, failure to hold this threshold has signaled weakness in market structure and often foreshadowed a deeper correction towards the 0.75th percentile, currently located around $97.5k.

Demand dries up

The third contraction below the short-term holders' cost basis and the 0.85 percentile in this cycle raises structural concerns. From a macro perspective, repeated demand exhaustion suggests the market may need a longer consolidation phase to regain strength.

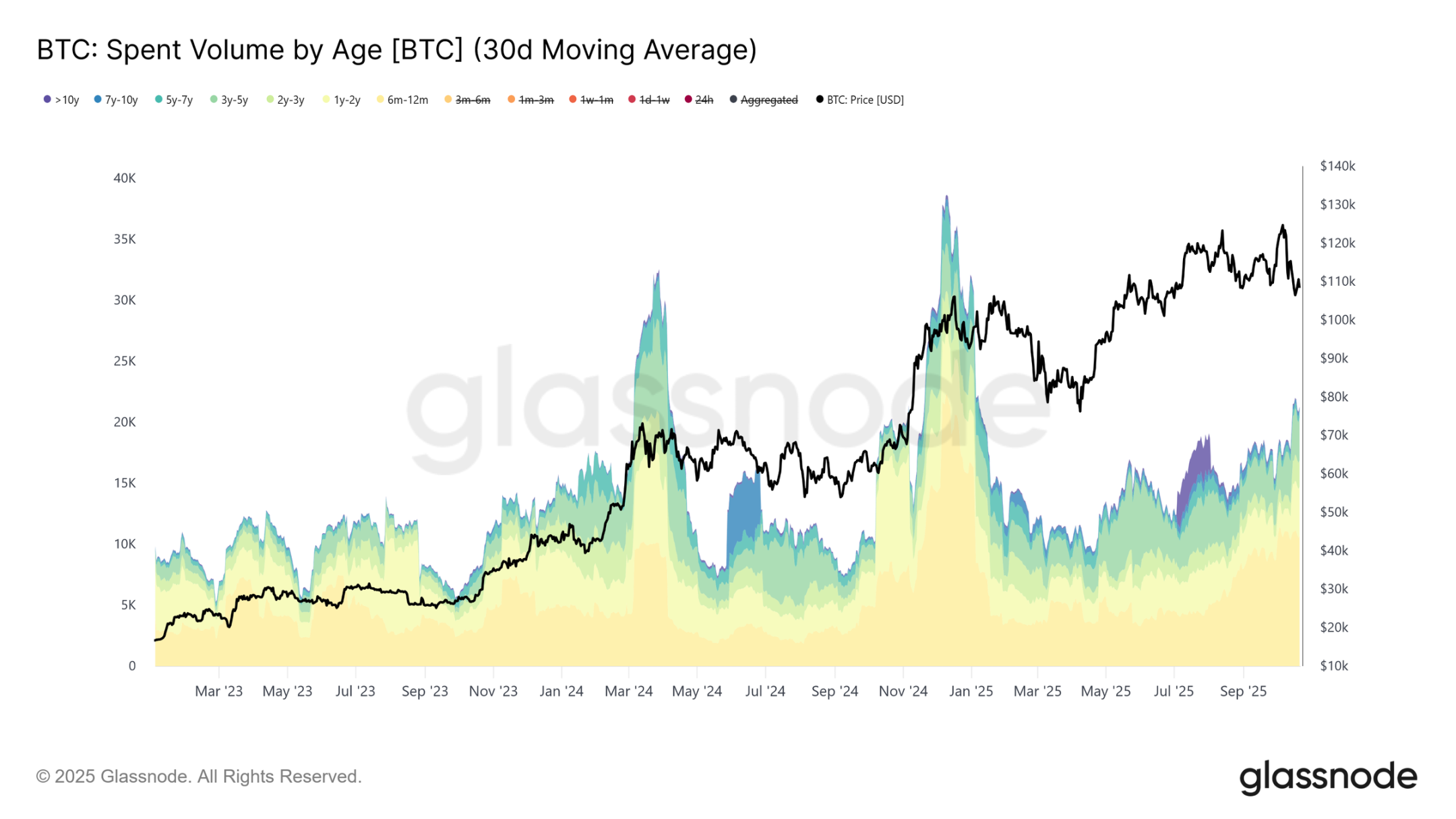

This depletion becomes even clearer when examining long-term holder spending. Since the market peak in July 2025, long-term holders have steadily increased their spending, with the 30-day simple moving average rising from a baseline of 10,000 BTC to over 22,000 BTC per day. Such sustained distributions indicate profit-taking pressure among experienced investors, a key factor in the current market fragility.

Having assessed the risk that demand exhaustion could lead to a prolonged bearish phase, we now turn to options markets to gauge short-term sentiment and observe how speculators position themselves amidst rising uncertainty.

Off-chain insights

Open interest rises

Bitcoin options open interest has reached a record high and continues to expand, signaling a structural evolution in market behavior. Investors are increasingly using options to hedge their exposure or speculate on volatility, rather than selling spot. This shift reduces direct selling pressure in the spot market but amplifies short-term volatility driven by hedging activity by market makers.

As open interest grows, price volatility is more likely to stem from delta- and gamma-driven flows in futures and perpetual swaps markets. Understanding these dynamics is becoming crucial, as options positioning now plays a leading role in shaping short-term market movements and amplifying reactions to macro and on-chain catalysts.

Volatility regime shift

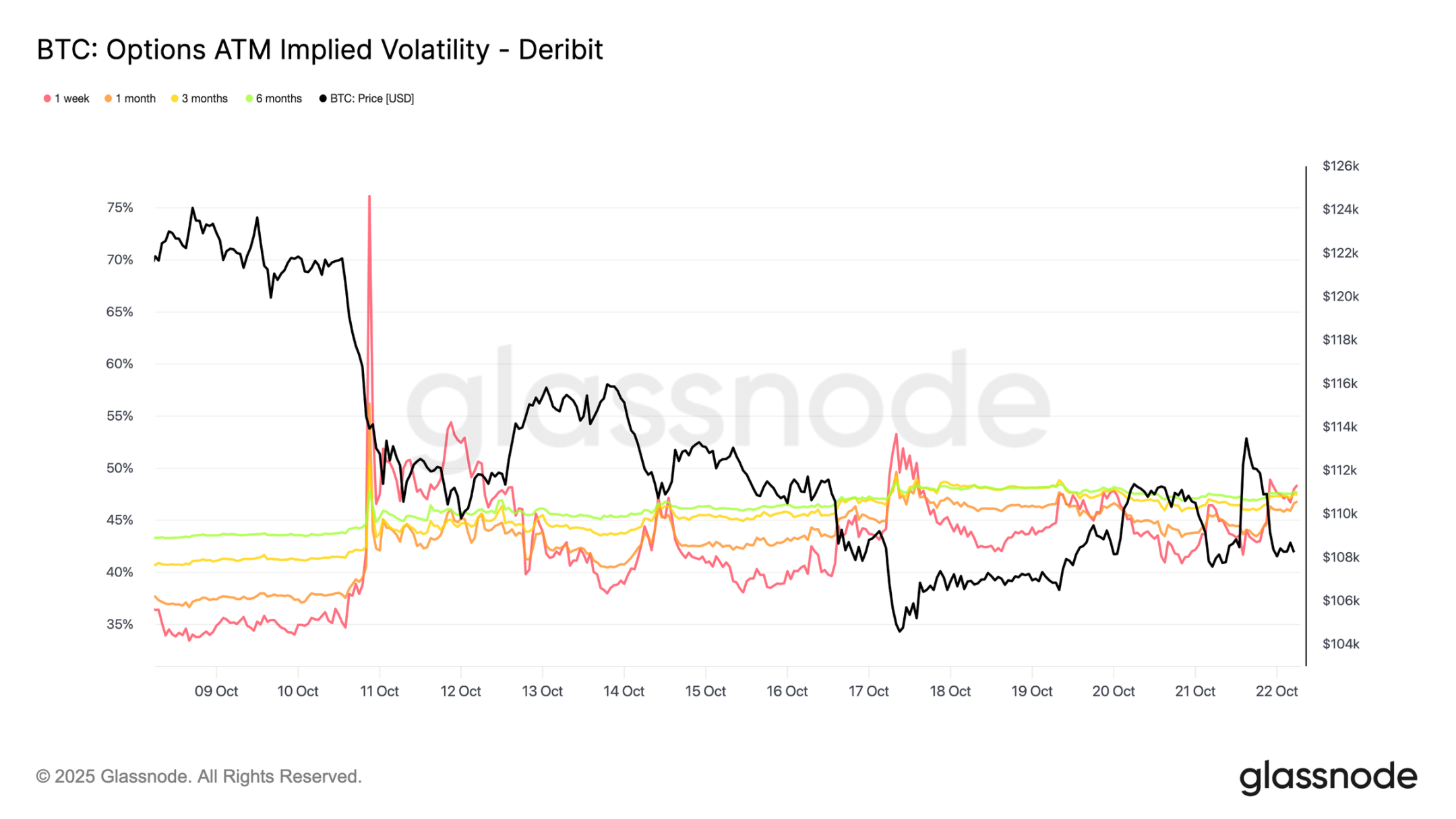

Since the liquidation event on the 10th, the volatility landscape has shifted significantly. Implied volatility is now around 48 across all tenors, compared to just 36-43 two weeks ago. The market hasn't fully priced in this shock yet, and market makers are remaining cautious and refraining from selling volatility cheaply.

30-day realized volatility is 44.1%, while 10-day realized volatility is 27.9%. As realized volatility cools, we can expect implied volatility to decline and normalize over the coming weeks. For now, volatility remains elevated, but this looks more like a short-term repricing than the beginning of a sustained period of high volatility.

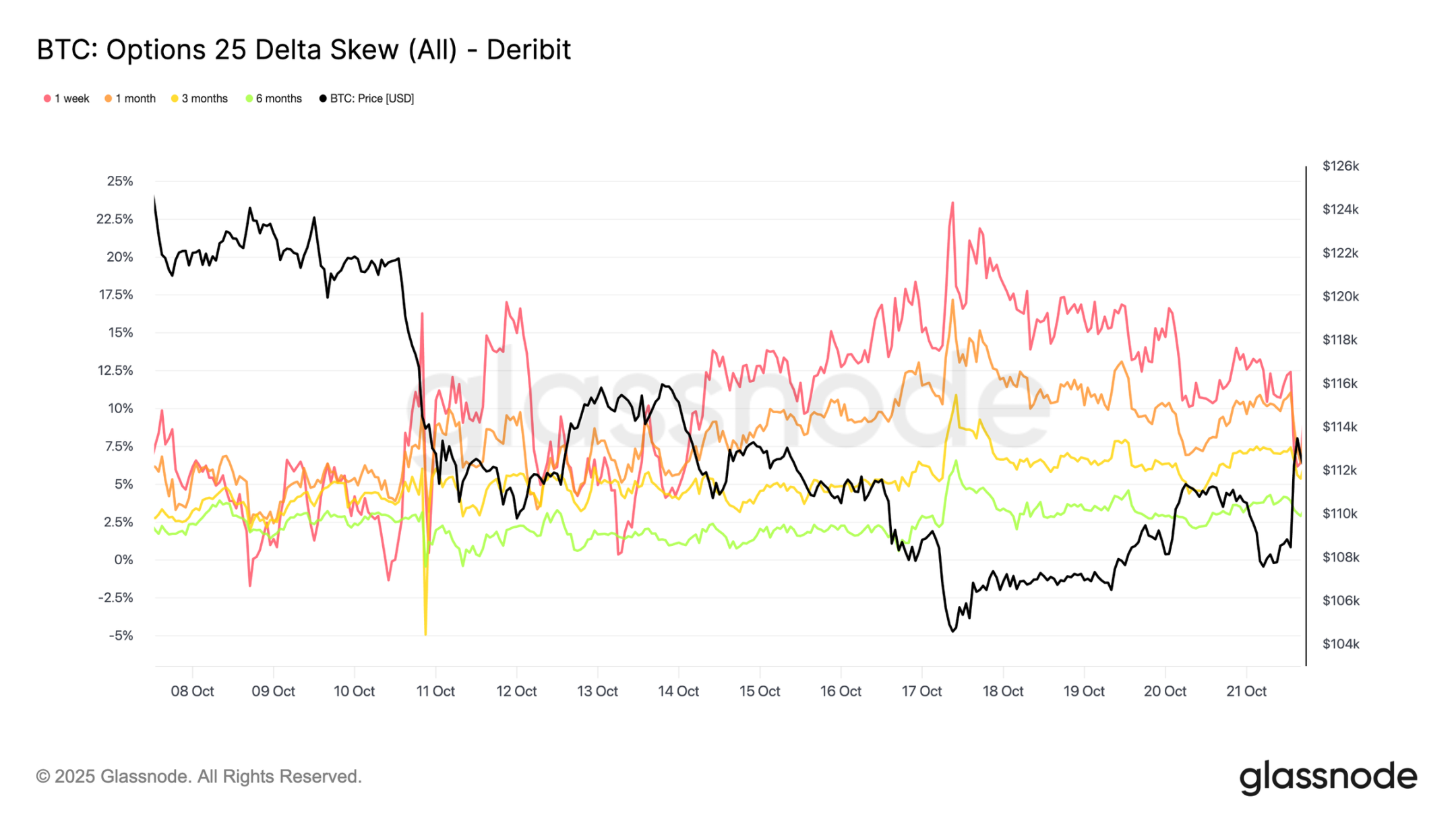

Put options intensify

Put options have steadily increased over the past two weeks. A massive surge in liquidations pushed the put skew sharply higher, and while it briefly reset, the curve has since stabilized at a structurally higher level, meaning puts remain more expensive than calls.

The 1-week skew has fluctuated over the past week but remained in high uncertainty territory, while all other maturities have moved 2-3 volatility points further in the put direction. This widening across maturities suggests that caution is spreading across the curve.

This structure reflects a market willing to pay a premium for downside protection while maintaining limited upside exposure, balancing short-term fears with a long-term outlook. Tuesday’s slight rebound illustrated this sensitivity, with put option premiums halving in a matter of hours, demonstrating how nervous market sentiment remains.

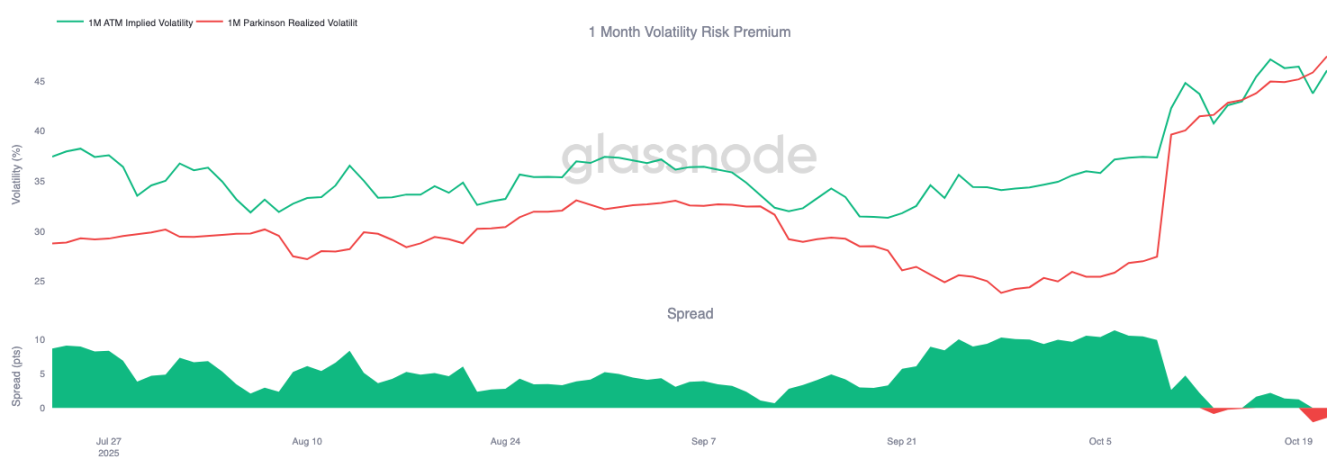

Risk premium shift

The one-month volatility risk premium has turned negative. For months, implied volatility has remained elevated while realized price movements have remained muted, resulting in steady returns for traders shorting volatility.

Now, realized volatility has surged to match implied volatility, erasing that advantage. This marks the end of the quiet regime: Volatility sellers can no longer rely on passive income and are instead forced to actively hedge in more volatile conditions. The market has shifted from a state of quiet contentment to a more dynamic and responsive environment, putting increasing pressure on short positions as real price fluctuations return.

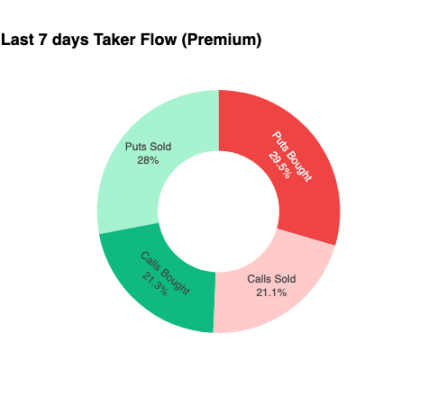

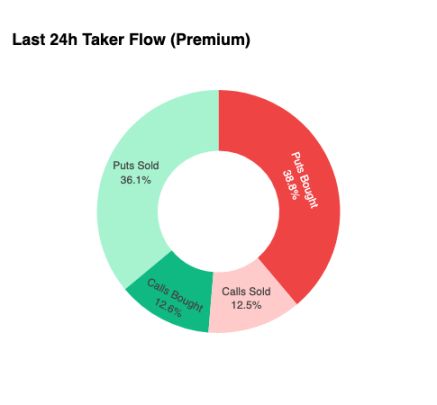

Fund flows remain defensive

To focus our analysis on the very short term, we zoom in on the past 24 hours to observe how options positioning responded to the recent rally. Despite a 6% rebound from $107,500 to $113,900, buying of call options provided little confirmation. Instead, traders increased their put option exposure, effectively locking in higher price levels.

This positioning configuration leaves market makers short on the downside and long on the upside, a setup that often causes them to suppress rallies and accelerate sell-offs, a dynamic that will continue to act as resistance until positioning resets.

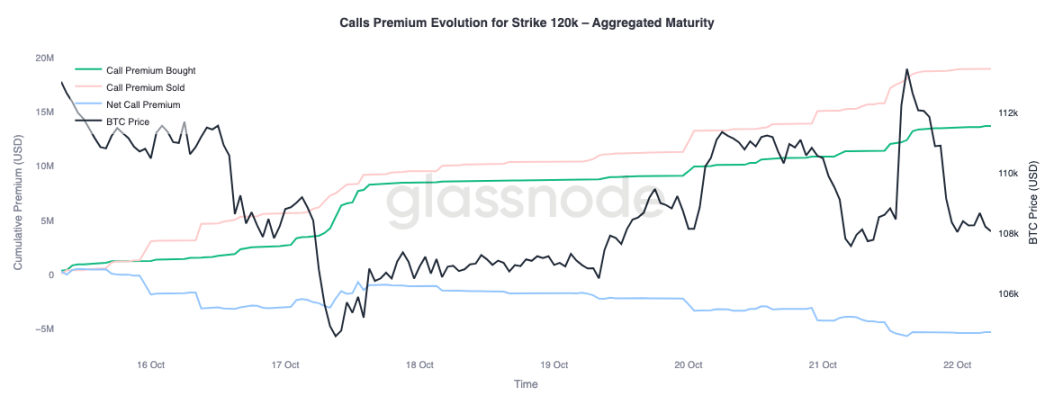

royalty

Glassnode's aggregated premium data, broken down by strike price, confirms the same pattern. At the $120,000 call option, the premium sold has risen with price; traders are restraining the upward move and selling volatility on what they perceive as a brief period of strength. Short-term yield seekers are taking advantage of the spike in implied volatility by selling call options on rallies rather than chasing the rally.

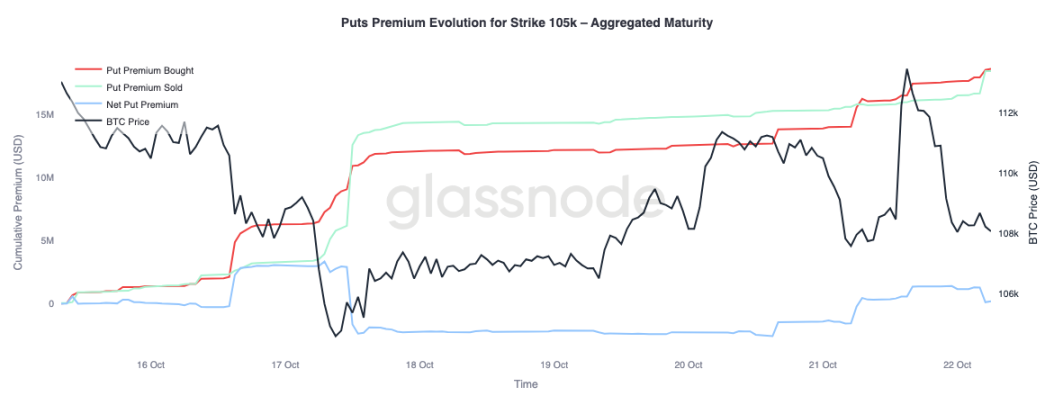

When looking at $105,000 put option premiums, the pattern is reversed, confirming our thesis. As prices rise, the net premium on the $105,000 put option increases. Traders are more eager to pay for downside protection than to buy upside convexity. This suggests the recent rally was met with hedging, not conviction.

in conclusion

Bitcoin's recent pullback below the short-term holder cost basis ($113,000) and the 0.85 percentile ($108,600) highlights growing demand exhaustion as the market struggles to attract new inflows while long-term holders continue to distribute. This structural weakness suggests the market may require a longer consolidation phase to rebuild confidence and absorb sold supply.

Meanwhile, the options market reflects a similarly cautious tone. Despite record-high open interest, positioning remains defensive; put skew remains elevated, volatility sellers are under pressure, and short-term rallies are being met with hedging rather than optimism. Taken together, these signals suggest the market is in a transitional phase: a period of fading exuberance and subdued structural risk-taking. Recovery will likely depend on restoring physical demand and mitigating volatility-driven flows.