Reflections after October 11th: How do exchanges balance “relative fairness” and “absolute transparency”?

- 核心观点:DEX与CEX竞争焦点转向透明度。

- 关键要素:

- 币安技术故障引发193亿美元清算。

- Hyperliquid链上交易实现透明可验证。

- DEX市场份额增至现货19%、合约14%。

- 市场影响:推动交易所透明化与责任明晰化。

- 时效性标注:中期影响。

Original | Odaily Planet Daily ( @OdailyChina )

By Golem ( @web3_golem )

While the epic October 11th sell-off has concluded and the market is gradually recovering, the record single-day liquidation of $19.3 billion set during that plunge still casts a shadow over the market. Many investors believe that Trump, known for his outspokenness, bears the primary blame. Others point the finger at Binance, arguing that the decoupling of the USDE, BNSOL, and WBETH prices is the primary cause of the further decline.

Binance officially explained the decoupling issue as a brief technical failure of some platform modules due to the overall market setback. As for the extremely low prices of some spot trading pairs, they were mainly caused by historical limit orders being triggered under unilateral liquidity and UI display accuracy issues.

Binance has assumed platform responsibility, compensating users who lost collateral due to the depegging of USDE, BNSOL, and WBETH, totaling $283 million. Despite this, some investors remain unconvinced, arguing that Binance is also responsible for the collapse of altcoins and reiterating concerns about centralized exchanges being "market manipulation," "data black boxes," and "deliberately unplugging."

On October 13th, Hyperliquid co-founder Jeff.hl also engaged in a heated exchange with Binance founder CZ on social media. Jeff.hl initially stated that all Hyperliquid orders, trades, and liquidations are executed on-chain, ensuring transparency and verifiability. He also argued that some centralized exchanges (CEXs) significantly underreport their liquidation data, specifically calling out Binance.

In response to this, Binance founder CZ also quickly responded to all doubts, saying that "when others choose to ignore, hide, shirk responsibility or attack competitors, key BSC ecosystem participants (including Binance, Venus, etc.) pay hundreds of millions of dollars out of their own pockets to protect users" and believes that this is a different value system.

There are many different opinions in the market, and no single solution can satisfy all market participants. During this sensitive period, Jeff.hl's public questioning of Binance essentially reflects the different trade-offs between CEX and DEX between "relative fairness" and "absolute transparency."

Performance is no longer the main difference between DEX and CEX

In the past, while DEXs were considered the ultimate form of crypto exchanges, CEXs still dominated the market share, primarily due to the significant performance gap between DEXs and CEXs. Issues such as high transaction latency, limited market depth, low capital efficiency, and poor transaction execution accuracy have consistently impacted traders' experience on DEXs. Consequently, despite the persistent criticism of CEXs for centralization risks and even recent debacles (such as the FTX incident), traders ultimately gravitate towards the low latency and ease of use offered by CEXs.

However, by 2025, these performance issues are no longer the primary obstacle hindering DEX market expansion. Take Hyperliquid, a DEX that boasts CEX-level performance, for example. Its on-chain central limit order book (CLOB) model offers a significant performance improvement compared to previous AMM DEXs, with an average transaction confirmation time of just 0.07 seconds, comparable to CEXs. Furthermore, while some niche tokens on Hyperliquid still face issues with insufficient liquidity and high slippage, Hyperliquid's transaction slippage for mainstream tokens like BTC and ETH is now below 0.1%, comparable to CEXs.

As the performance gap gradually narrows, the trend of funds and traders migrating to DEX has indeed been happening since 2025.

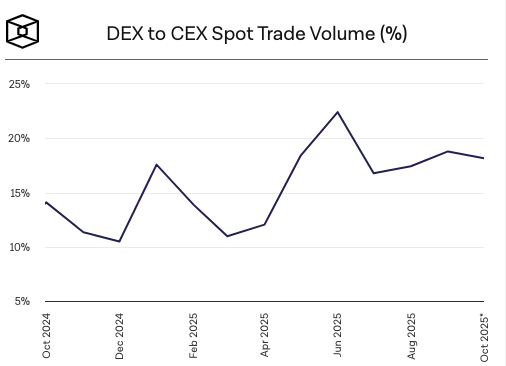

According to data from The Block , in the spot market, compared with CEX, the market share of DEX will generally increase in 2025, reaching 19% in the third quarter of 2025.

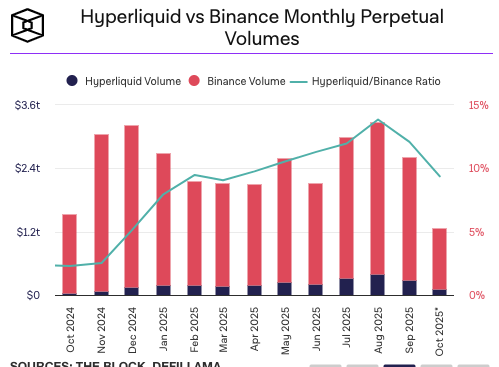

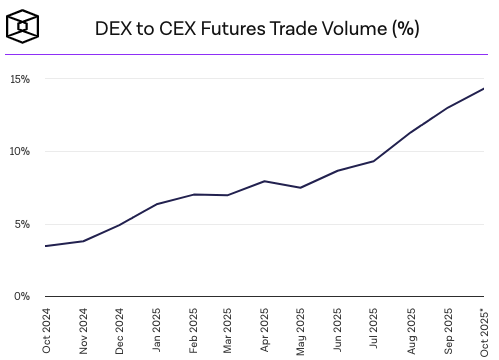

In the perpetual contract market, DEX's market share grew even faster, from only 4.9% of CEX's contract market at the end of 2024 to 14.33% in October 2025.

Even under extreme market conditions, today's DEXs have withstood the test. Following the October 11th crash, Hyperliquid officially stated , "Despite record-breaking platform traffic and transaction volumes during these extreme market conditions, the Hyperliquid blockchain experienced no downtime or latency."

On the same day, Binance, the world's largest exchange, experienced a partial system outage due to technical issues. However, this doesn't necessarily mean Hyperliquid is currently performing better than Binance, as the systems they face are under different pressures. On October 11th, Hyperliquid's perpetual contract trading volume exceeded $10 billion, while Binance's volume was over 10 times that. Data from The Block shows that in September, Hyperliquid's contract trading volume was $282.47 billion, while Binance's was $2.34 trillion, representing only 12% of Binance's.

The market is always "relatively fair"

When performance is no longer the primary difference between CEXs and DEXs, will all investors truly choose DEXs? Despite the criticism leveled against Binance following the October 11th crash, post-2000s trader Vida remains vocal in his support for Binance, arguing that it remains committed to its users at all times.

Some investors complained that Vida's comments were due to Binance's bias. During extreme market conditions, the exchange compensated and appeased stakeholders like large traders and "Binance users," while ignoring the impacted retail investors and other market participants. Binance's growth was built on the bodies of countless silent victims, with the wealthy being paid back in full and the common people's money split 70-30.

However, aside from the "conspiracy theories" surrounding CEXs, fairness in this market is always relative. Even DEXs, which champion decentralization and fairness, can falter in the face of a crisis . On March 26th of this year, Hyperliquid faced its biggest crisis since its founding. A whale manipulated the price of the meme coin JELLY, forcing Hyperliquid (HLP) to take on a large short position and risk losing $240 million. However, Hyperliquid opted for a "plug-and-drag" approach by delisting the JELLY contracts, resulting in a $700,000 profit for HLPs, which were expected to lose money.

Hyperliquid's move also caused a public outcry, making a mockery of decentralization and fairness. This wasn't the first time traders had exploited Hyperliquid's vulnerabilities for profit. Other incidents included "a whale's forced liquidation caused a $4 million loss in HLP" and "a series of XPL liquidations reaped $46 million." Hyperliquiquid failed to compensate users in these incidents.

This made investors understand that Hyperliquid did not adhere to decentralization and fairness, but chose to "do nothing" before the crisis spread to itself. It can be said that every upgrade and improvement of Hyperliquid was stepped on countless "corpses" .

The market needs "absolute transparency"

The trading market is never truly fair. Frankly speaking, if one party makes money, another party will inevitably lose money. Whether it is a DEX or a CEX, it is impossible for them to be responsible for everyone. But even if fairness is relative, transparency can be absolute.

During extreme market conditions, CEXs are often embroiled in conspiracy theories. The primary reason is that CEXs are inherently tamper-resistant "black boxes." Even with enhanced regulatory and compliance measures, a lack of transparency persists, fostering public distrust. Investors rely solely on exchange announcements for their so-called truth. While authoritative, these statements can also be easily challenged. For example, Hyperliquid co-founder Jeff.hl has accused Binance of fabricating its clearing data, and Binance would have to "cut open its belly and show how many bowls of noodles it's had" to prove its claims.

While Hyperliquid's values differ from Binance's, the transparency and verifiability of its on-chain transaction data are undeniable. This transparent settlement mechanism not only significantly reduces the possibility of market manipulation by the platform but also provides peace of mind for investors, mitigating the risk of conspiracy theories. For example, during several Hyperliquid crises, people watched the actions of the "whales" on-chain, while investors suffered losses and lamented their losses. Despite Hyperliquiquid's indifference, few believed the platform was behind the incident.

While mechanisms aren't perfect, transparent, open, and automated trading mechanisms within established rules will always reduce controversy compared to the black boxes and chaos of centralized exchanges. Even DEXs can be subject to suspicion if they lack transparency. For example, the previously popular Prep DEX Aster was accused of fraudulent trading and data fabrication due to its private order features. DeFiLlama even temporarily delisted Aster.

With the development of the crypto market, CEXs and DEXs are no longer mutually exclusive. The boundaries between CEXs and DEXs are narrowing, with DEX experiences becoming more similar to CEXs. CEXs are also expanding their on-chain businesses through exchange user wallets. Both CEXs and DEXs have their own risk quadrants. CEXs can provide a safety net for users in the event of a real crisis, but investors criticize their power. DEXs, while adhering to the principle of "code is law," do not impose excessive restrictions on user behavior, but investors appreciate the benefits of centralized compensation in the event of a crisis.

But from the trend point of view, "transparency and openness" is the foundation of Crypto and one of its development trends. Even if the value systems of CEX and DEX are different, both should move in this direction: higher verifiability, clearer responsibility boundaries, and more sound crisis response mechanisms.