Is L2 a detour for Ethereum?

- 核心观点:L2网络价值捕获不足,用户流失严重。

- 关键要素:

- Linea空投价值远低于用户投入。

- L2活跃地址数大幅下跌超90%。

- 仅Base和Arbitrum交易表现相对较好。

- 市场影响:动摇市场对L2代币经济模型的信心。

- 时效性标注:中期影响。

Original | Odaily Planet Daily ( @OdailyChina )

By Wenser ( @wenser 2010 )

"Do you know how I have been through these past three years?" This may be the voice of many users who have participated in Linea interactions.

After three years, Linea, the Layer 2 (L2) network under Consensys, a prominent Ethereum orthodox faction, is finally about to hold its TGE. However, judging by the current airdrop amount and Linea's pre-market price, it's unlikely to satisfy heavily invested enthusiasts. Some claim to have invested hundreds of thousands of dollars, only to receive airdropped tokens worth only a few thousand dollars, or even less. Thus, after a period of hype and constant mention of Layer 2, the Ethereum network may have entered a phase where Layer 2 is losing public support.

After several years of development, the "L2 technology path" once singled out by Ethereum founder Vitalik Buterin may have become a detour in the Ethereum ecosystem's development. This article, Odaily Planet Daily, explores this perspective through the lens of Linea's token launch and the current state of mainstream L2 networks, inviting readers to engage in critical discussion.

Where the dream begins

According to the original idea of Ethereum founder Vitalik, the L2 network is a network system built on the basis of inheriting the security of the Ethereum main network, used to expand the Ethereum ecosystem and reduce usage costs.

In October 2020, Vitalik elaborated on the technical concept of the L2 route in the article "Rollup-centric Ethereum Roadmap" . Its core purpose is to simplify Ethereum's long-term expansion strategy and move computing execution mainly to L2 solutions (such as Rollup), so as to quickly achieve network scalability while alleviating the high gas fees and congestion problems of the main network at the time.

In addition, he mentioned the short-term actions and potential impact of this technical route: "We need to do more work on cross-L2 transfers to make the experience of moving assets between different L2s as close to instant and seamless as possible." "It is necessary for L2 projects to launch their own tokens - of course, the premise is that the tokens have real economic value (that is, the future fees captured by the L2 estimate). As a result, these L2 network-related protocols will be able to earn fees/MEV, thereby directly or indirectly (through supporting tokens to fund development) to fund their development. In the long run, this is a strategic move that is beneficial to the long-term economic sustainability of Ethereum."

Linea is about to issue a coin, but L2 activity is not as high as before

At present, among the major L2 networks, only Arbitrum and Base have performed well in value capture. The price of the former's token is mediocre, just like other L2 tokens. The latter has no intention of releasing native tokens and mainly relies on sorter income to generate revenue, earn network development fees and feed back to Coinbase.

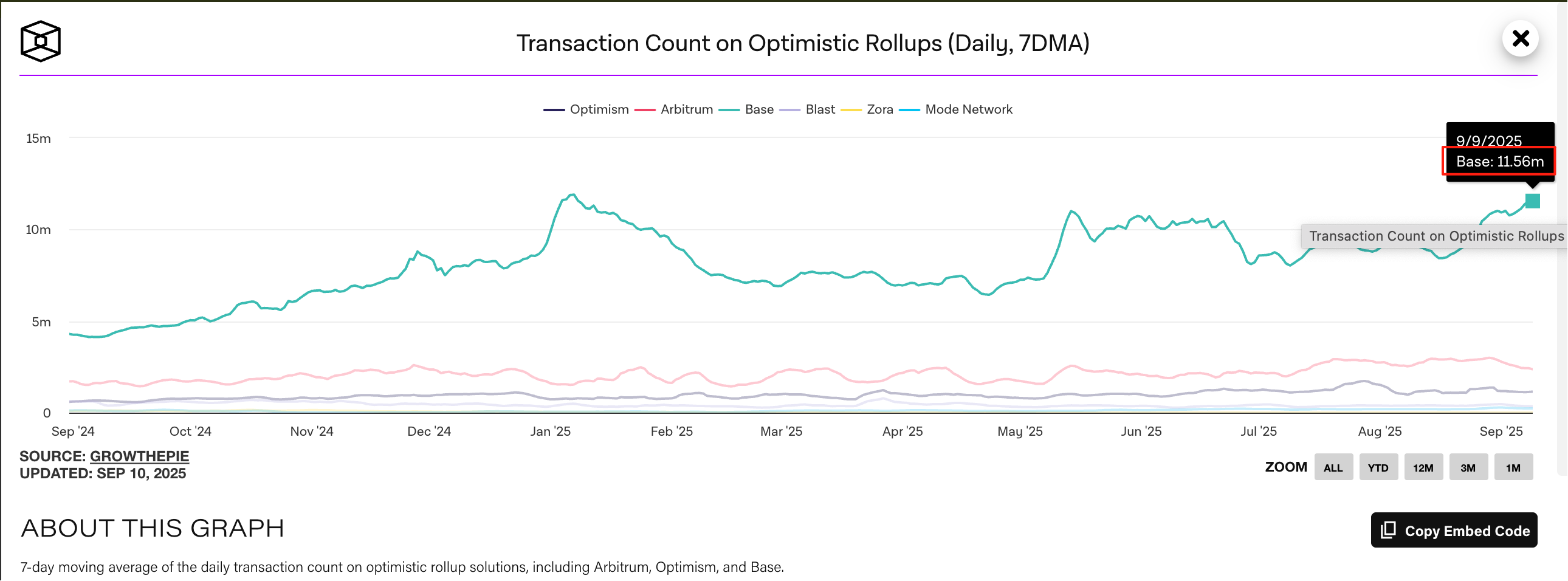

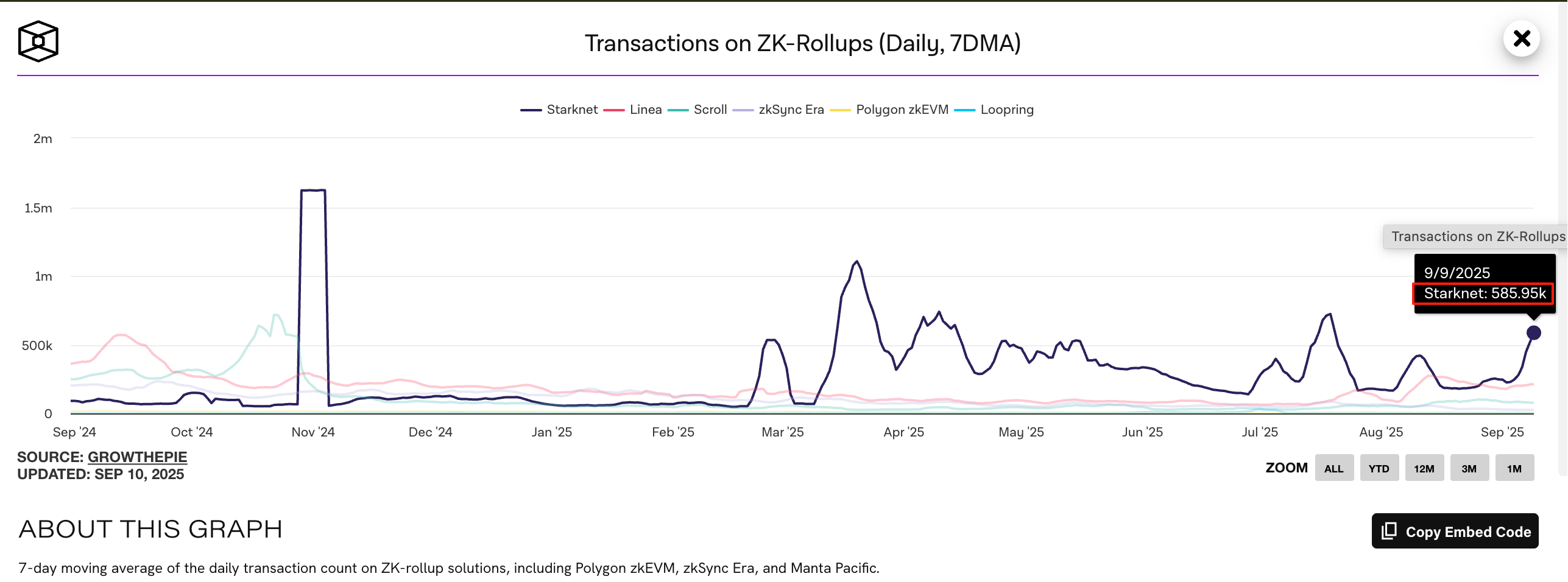

According to data from TheBlock , on September 9, the number of transactions on Base alone (seven-day average) reached 11.56 million, the number of transactions on Arbitrum was 2.36 million, the number of transactions on Optimism was 1.15 million, the number of transactions on Blast was only 344,000, and the number of transactions on Mode Network was only 233,000; among the ZK-based L2 networks, Starknet had the most transactions (585,000), and the transaction numbers of the remaining networks, from most to least, were Linea (211,000), Scroll (76,000), ZKSync Era (25,000), Polygon zkEVM (4,000), and Loopring (250).

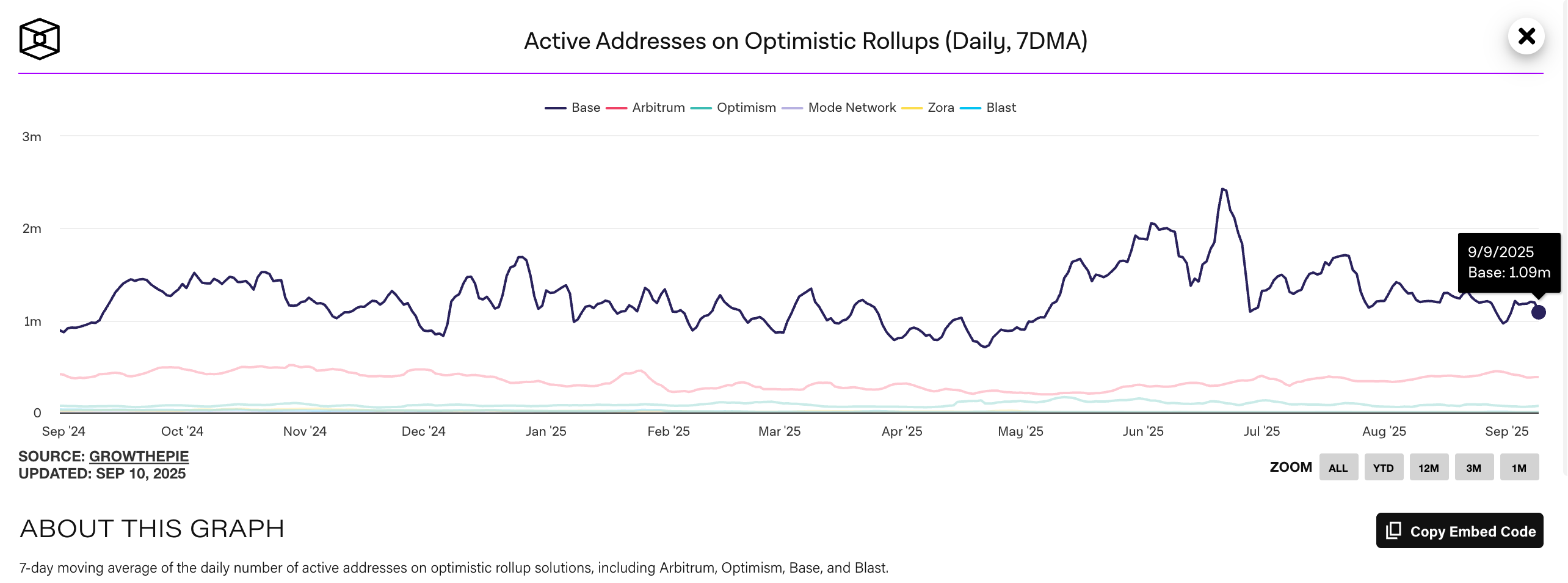

In terms of the average daily number of active addresses , taking September 9 as an example, Base (seven-day average) in the Optimism L2 network was far ahead with 1.09 million addresses. The remaining networks and their corresponding address numbers were: Arbitrum (384,000); Optimism (72,000); Mode Network (3,450); Zora (3,440); and Blast (2,800).

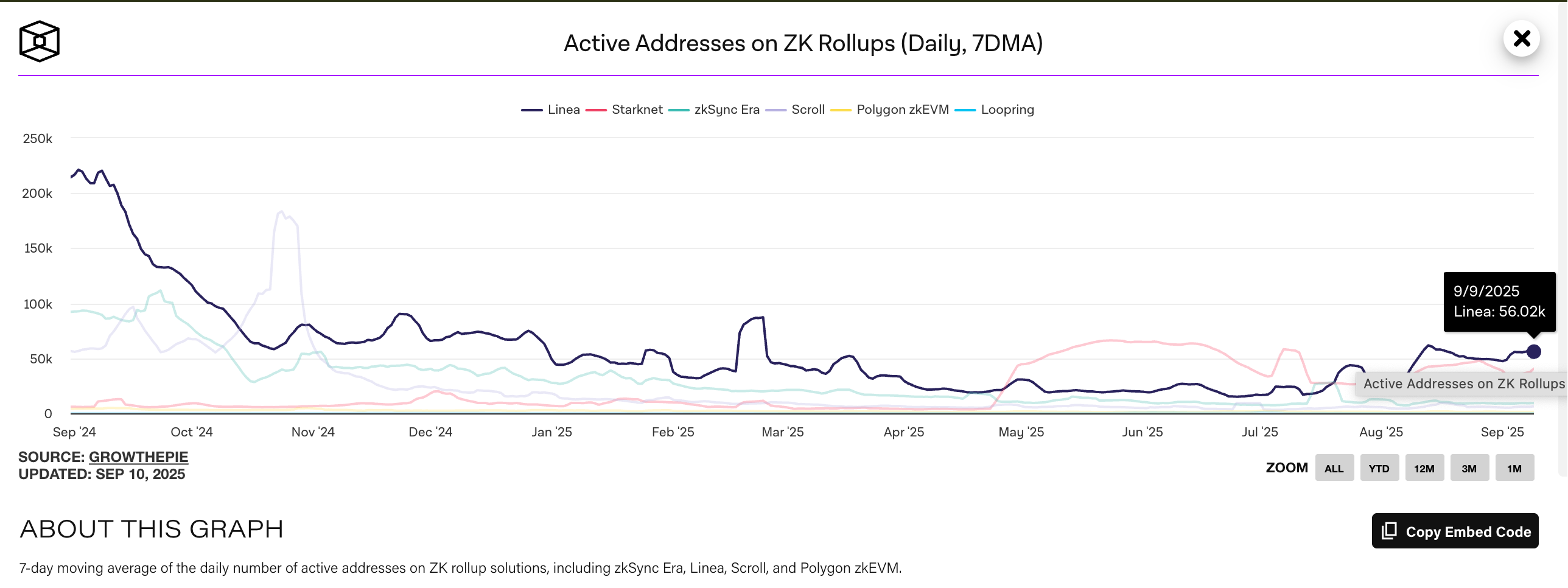

The performance of the ZK-based L2 network is also disappointing. On September 9 , perhaps benefiting from the impact of the upcoming TGE, the average daily active addresses of the Linea network increased to 56,000, a drop of more than 90% compared to the average daily active addresses of about 750,000 in July 2024; the average daily active addresses of the remaining L2 networks all remained below 50,000: Starknet (about 40,000); ZKSync Era (about 9,200); Scroll (about 6,300); Polygon zkEVM (about 1,200); Loopring had only a rather bleak 18 active addresses.

Furthermore, while the explosion of L2 networks has improved the efficiency of the Ethereum ecosystem to a certain extent, it has also provided a breeding ground for frequent protocol security incidents within the ecosystem. Furthermore, after the gradual implementation of EIP proposals to optimize gas fees, such as EIP-1559 and EIP-7999, gas costs on the Ethereum mainnet have been significantly reduced, and transfer and transaction efficiency has far exceeded previous levels.

Therefore, after several years of L2 development, people have come to realize that the core proposition for the Ethereum ecosystem is:

First, does the Ethereum ecosystem have the goal of user retention and activity?

Second, can Ethereum L2 network tokens achieve value capture?

At present, the current situation in both aspects is not optimistic.

The path to value breakthrough for the Ethereum ecosystem: stablecoins and ETH treasury reserves

Judging from the results, the L2 route has still made a huge contribution to the development of the Ethereum ecosystem. In addition to saving a large amount of gas fees, the strategic value of L2 is mainly reflected in two aspects:

First, the value of TVL (TVL) is significant . According to data from the l2beat website , as of September 10th, the total TVL of the Ethereum L2 network had grown to $54.7 billion. While this represents a decrease of over $10 billion from the $65.5 billion TVL in December of last year, it still provides more liquidity for the Ethereum ecosystem and ample funding for numerous protocols and projects within it.

Second, seamless integration with traditional financial assets . Beyond crypto-native networks like Arbitrum and Optimism, traditional tech companies like Sony's L2 public chain Soneium, Alibaba's Ant Digits' RWA L2 public chain Jovay, and Robinhood's Arbitrum-based L2 public chain for trading tokenized stock products are also emerging. As a mature blockchain ecosystem with a decade of stable operation, Ethereum remains the best choice for traditional companies targeting the RWA market, and L2 networks provide a relatively stable and smooth entry window and channel bridge.

From today’s perspective, the subsequent path for the Ethereum ecosystem to break through its value may still rely on its connection with the traditional financial sector and the coupling of assets on a wider scale. The former’s main medium is stablecoins, and subsequent development routes include PayFi, DePIN, cross-border trade, etc. The latter mainly relies on many listed companies to promote ETH treasury reserves to complete the tokenization and assetization of RWA assets such as stocks.

Looking ahead to 2025, the 10th anniversary of the launch of the Ethereum mainnet, although most L2 networks have gradually become detritus in the long history of cryptocurrencies in the vicious cycle of "fundraising-issuing coins-disappearing", they have also become the soil and nutrients for nurturing new innovative products while becoming a "crypto bubble".

Many L2 networks, including Linea, which has not issued coins for a long time, may have few ecological projects and sluggish token prices in the market, but they have also provided many technological updates and project products for the narrative boom in the crypto market. This may be an "industry bubble" when the crypto industry has developed to a certain stage, but it is by no means a so-called "industry black history."

As to whether the Ethereum ecosystem can develop further, it may still take time to verify.