Is the end of stablecoins the public blockchain? A new attempt by the three giants

- 核心观点:稳定币发行商正加速自建公链。

- 关键要素:

- Tether扶持Plasma侧链及Stable链。

- Circle推出专为稳定币的Arc链。

- Ethena支持Converge链秋季测试。

- 市场影响:增强发行商控制力,重塑行业格局。

- 时效性标注:中期影响。

Throughout the evolution of the crypto market, stablecoins have always been a crucial piece of infrastructure. From the earliest USDT to today's USDC, DAI, and the emerging USDe, stablecoins have become a core driver of trading volume and liquidity. However, an accelerating trend is emerging: stablecoin issuers are no longer content with simply creating "tokens" but are beginning to build their own public chains. Tether, one of the three major stablecoin companies and the issuer of USDT, will begin supporting Plasma, a Bitcoin sidechain focused on stablecoin use cases, by the end of 2024. In early June of this year, Tether officially announced Stable, a new Level 1 chain backed by Bitfinex and USDT's unified liquidity protocol, USDT 0. Circle, which recently completed its IPD on the US stock market, also announced its in-house development of Arc, specifically designed for stablecoin finance and programmable money. Converge, backed by Ethena, the issuer of the new stablecoin giant USDe, will also launch its testnet this fall.

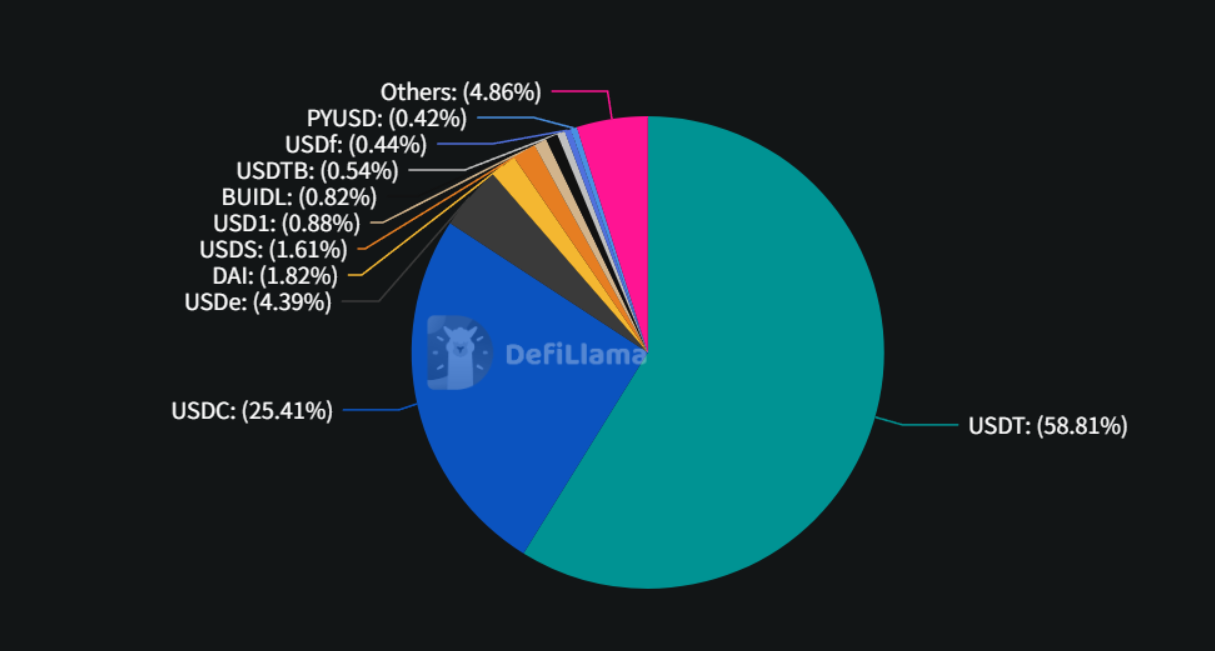

Stablecoin market capitalization distribution chart (Source: DefiLlama)

Why does a stablecoin need a public chain?

In the past, stablecoins were often based on Ethereum, Solana, and other mainstream public blockchains. This model seemingly leverages the liquidity of an open ecosystem, but it also implies a heavy reliance on underlying technical rules and transaction fee capture. As the crypto market continues to expand, stablecoin issuers are re-evaluating this landscape: Do they need to fully control the underlying infrastructure to further solidify their market position?

From the overall perspective of industry development, there are three core logics behind this trend:

Stablecoins have become the gateway to the ecosystem: In the crypto world, stablecoins serve as the "digital dollar," essential for nearly all on-chain activities. Buying Bitcoin requires USDT or USDC, and DeFi mining pools are also denominated in stablecoins. Many people even use stablecoins as their daily digital wallets. Stablecoin daily trading volume is often several times that of Bitcoin, making them the cornerstone of liquidity for the entire crypto ecosystem. If a stablecoin issuer also owns its own public blockchain, it effectively controls both the "currency issuance" and the "financial infrastructure." This dual control makes their position even more unassailable.

The strategic value of the settlement layer: Public chains are essentially giant toll booths, with every transaction subject to a toll. Currently, USDT transfers on Ethereum incur fees of several or even tens of dollars, all of which goes to Ethereum. USDT's daily trading volume easily reaches tens of billions of dollars, generating astronomical fee revenue. Tron (TRX) has risen to the top public chain largely due to its near-free USDT transfers, attracting a large number of users from Ethereum. If Tether had developed its own public chain, these users and revenue would have been its own. With its own public chain, stablecoin issuers can not only collect fees but also offer cheaper transfer services. More importantly, they can control pricing power—no longer relying on others and can optimize network performance based on business needs.

Ecosystem Stickiness and Bargaining Power: In the crypto world, users follow wherever developers go. Solana's low transaction fees and fast speeds have attracted numerous projects, and users have flocked to it. If a stablecoin issuer owns its own public chain, they can proactively attract developers to build an ecosystem by providing specialized development tools, offering token incentives to new projects, or promising permanently low transaction fees. Once scale is achieved, a snowball effect will occur, transforming the stablecoin issuer from a mere "printing mill" into a platform-level enterprise. More importantly, their voice will be enhanced. Currently, partnerships between Circle or Tether and traditional banks are essentially "begging for favors." However, if a stablecoin issuer has a thriving public chain ecosystem with millions of users and thousands of applications, its negotiating position will be completely different, potentially even prompting traditional financial institutions to actively seek cooperation.

The direction and differentiation of the three major stablecoin public chains

Plasma: Leveraging Bitcoin for Security

A dedicated public chain for stablecoin payments. Plasma is a blockchain built specifically for stablecoin payments, and can be thought of as the "stablecoin version of Alipay." Its most significant feature is its deep integration with Bitcoin—users can directly participate in smart contracts with real Bitcoin, without the need for complex wrapped tokens. Even more conveniently, when transferring funds on Plasma, you can pay transaction fees directly with USDT or Bitcoin, without having to first purchase native tokens like on other public chains. The design philosophy of this chain is clear: to make stablecoin payments as easy as transferring money via WeChat. Teams developing payment applications can directly access Plasma's infrastructure without having to build complex underlying systems from scratch. Simply put, Plasma aims to make stablecoin payments faster, cheaper, and more secure, while lowering the barrier to entry for both ordinary users and developers, and promoting the widespread adoption of stablecoins in everyday payment scenarios.

Converge: A Clever Integration of Traditional Finance and DeFi Applications

Converge is an intriguing blockchain. Its defining characteristic is its duality—it can be both a completely open DeFi playground and a strictly compliant financial platform, allowing users to choose between different models based on their needs. Imagine: on the same public chain, retail investors can freely participate in various DeFi mining and trading activities, while institutions like banks and funds can conduct regulated digital asset operations within a compliant environment. The two approaches work independently, yet benefit from each other. Converge supports direct payment of fees in stablecoins like USDe and USDtb, ensuring completely manageable costs. This design is particularly well-suited for projects that aim to serve both retail and institutional clients: retail users can enjoy the high returns and innovative gameplay of DeFi, while institutional users can participate in digital asset investment while meeting regulatory requirements. Simply put, Converge aims to break down the barriers between traditional finance and DeFi, enabling the harmonious coexistence and mutual enhancement of these two worlds.

Stable: USDT L1 created for institutions

Stable is a blockchain built entirely around USDT, specifically designed to serve the transfer needs of hundreds of millions of USDT users worldwide. Its greatest innovation is making USDT the very lifeblood of the network—users don't need to pay any fees or prepare other tokens in advance when transferring funds; all transactions can be completed directly with USDT, just like using a bank transfer. For privacy-conscious users, Stable also offers encrypted transfers to ensure confidentiality of transaction information. More importantly, it offers a comprehensive payment solution designed specifically for businesses and institutions, including batch transfers, merchant acceptance, and debit card integration, allowing businesses to use USDT for daily operations, just like using traditional banking systems. Stable also maintains excellent compatibility with other major public blockchains, allowing users to easily transfer assets between networks. Simply put, Stable aims to make USDT the true dollar of the digital world—not just a transaction tool, but a complete payment infrastructure.

Arc: Built for Institutional Finance

Arc is a blockchain specifically designed by Circle for businesses and financial institutions, and can be considered a "Wall Street version of a public stablecoin blockchain." Its greatest advantage is its backing by Circle's deep roots in traditional finance, which naturally equips Arc with compliance advantages unmatched by other public chains. For businesses, conducting business on Arc is like operating in a regulated financial environment, with manageable risks and regulatory compliance. Technically, Arc allows businesses to pay all expenses directly in USDC, making financial accounting simple and transparent, eliminating the headache of complex token conversions. More importantly, Arc offers a variety of financial tools specifically designed for institutional needs. For example, businesses can easily tokenize traditional assets like real estate and equity, or build their own digital payment systems. For traditional businesses interested in embracing blockchain but concerned about compliance risks, Arc provides a relatively safe entry point.

Comparison of features and technical parameters

From the above introduction to the core concepts of each stablecoin public chain, it's clear that Ethena's Converge differs significantly from the other three. Plasma, Stable, and Arc all define themselves as payment infrastructure, focusing on making stablecoin transfers simpler and cheaper. Essentially, they're transforming the traditional payment experience with blockchain technology. Converge, on the other hand, explicitly positions itself as a DeFi innovation platform, a move that aligns with Ethena's DNA. Unlike traditional stablecoins like USDC and USDT, which are backed by cash and government bonds, USDe maintains price stability through a delta-neutral strategy. This innovative mechanism makes Converge a natural fit for users deeply involved in DeFi or interested in on-chain financial innovation.

More significant differences lie in growth strategies and understandings of "openness." Plasma emphasizes native Bitcoin integration, Stable pursues a zero-fee experience, and Arc leverages Circle's compliance advantages. These are all optimizations and improvements within the existing framework. The first three primarily attract traditional users by lowering barriers to entry—fee-free, simplified operations, and compliance assurances, employing a typical "build user base first" strategy. Converge, on the other hand, has chosen a completely different path: attracting crypto natives by offering higher returns and more innovative opportunities, then expanding the community with an optional compliance layer. This embodies a "deepen user value first" growth philosophy. Converge's most forward-thinking innovation lies in its "optional permissioning" model. By default, the network is completely open, allowing anyone to freely bridge assets, deploy applications, and participate in DeFi activities, fully preserving the innovative vitality of decentralized finance. However, when tokenizing RWAs or meeting Know Your Customer (KYC)/Know Your Business (KYB) requirements, applications can optionally enable the compliance layer. This design cleverly balances the open spirit of DeFi with the compliance requirements of traditional finance, neither stifling innovation through over-regulation nor deterring institutions through laissez-faire. Simply put, while the other three blockchains are using new technologies to accomplish traditional tasks, Converge is building the infrastructure for the future financial ecosystem.

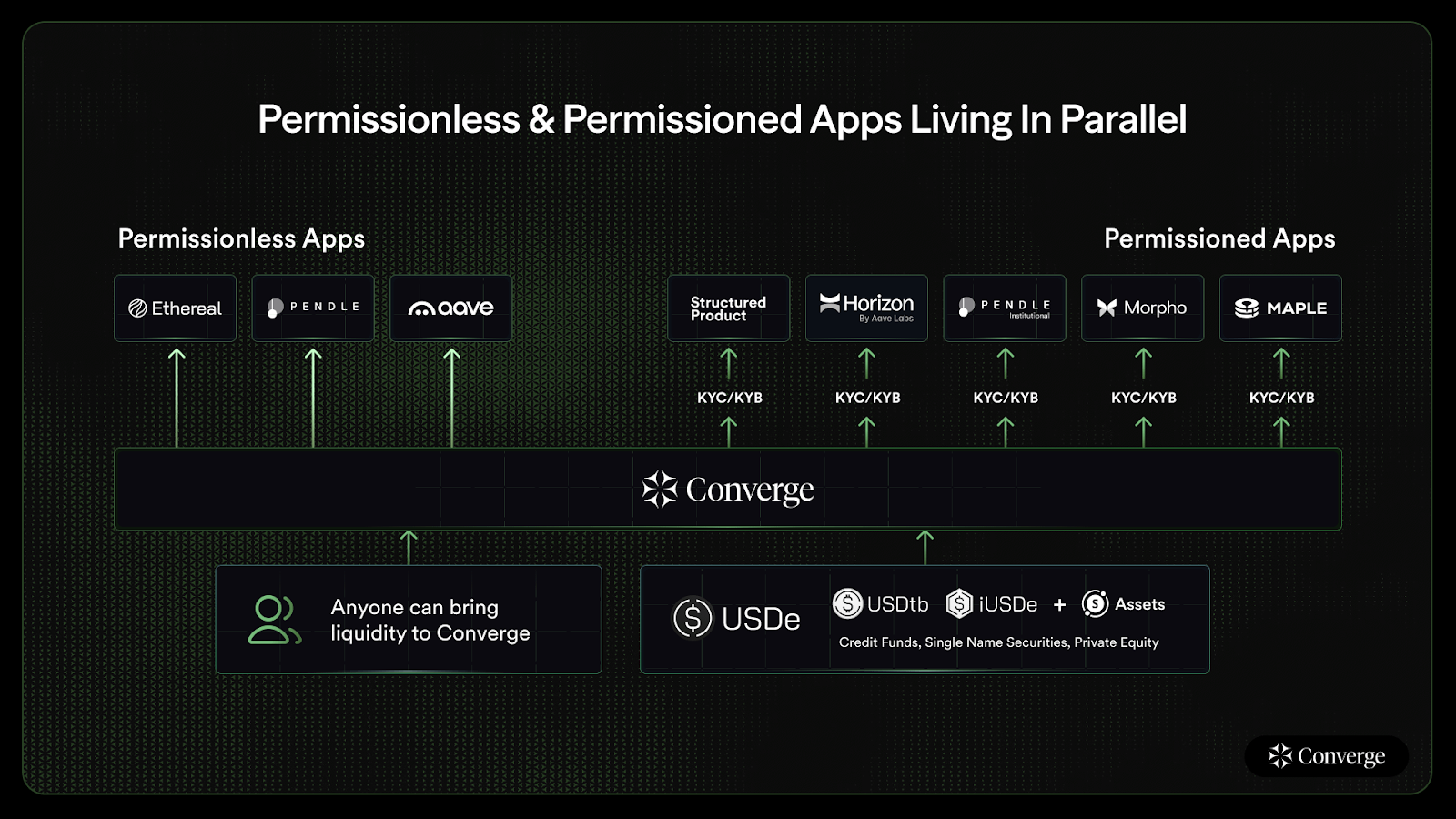

Converge's optional licensing architecture (Source: Converge)

Challenges and Future Outlook

Stablecoin public chains must support large-scale transfers, clearing, and payments, placing extremely high demands on stability and security. Any vulnerability or interruption would undermine the foundation of trust in the stablecoin. Furthermore, the ecosystem's cold start presents another significant challenge. Newcomers must rely on differentiated features and incentive mechanisms to counter the network effects of established public chains like Ethereum and Solana. In the future, the integration of stablecoins and public chains will blur the boundaries between "currency" and "infrastructure," evolving them from simple tokens into ecosystem operating systems. Projects that strike a balance between compliance and openness are most likely to become a bridge between traditional and crypto finance, securing a key position in the global competition for financial infrastructure.