Tom Lee's latest podcast: We are witnessing ETH's "1971 moment", $60,000 is a reasonable valuation

- 核心观点:ETH财库公司成以太坊最强买盘力量。

- 关键要素:

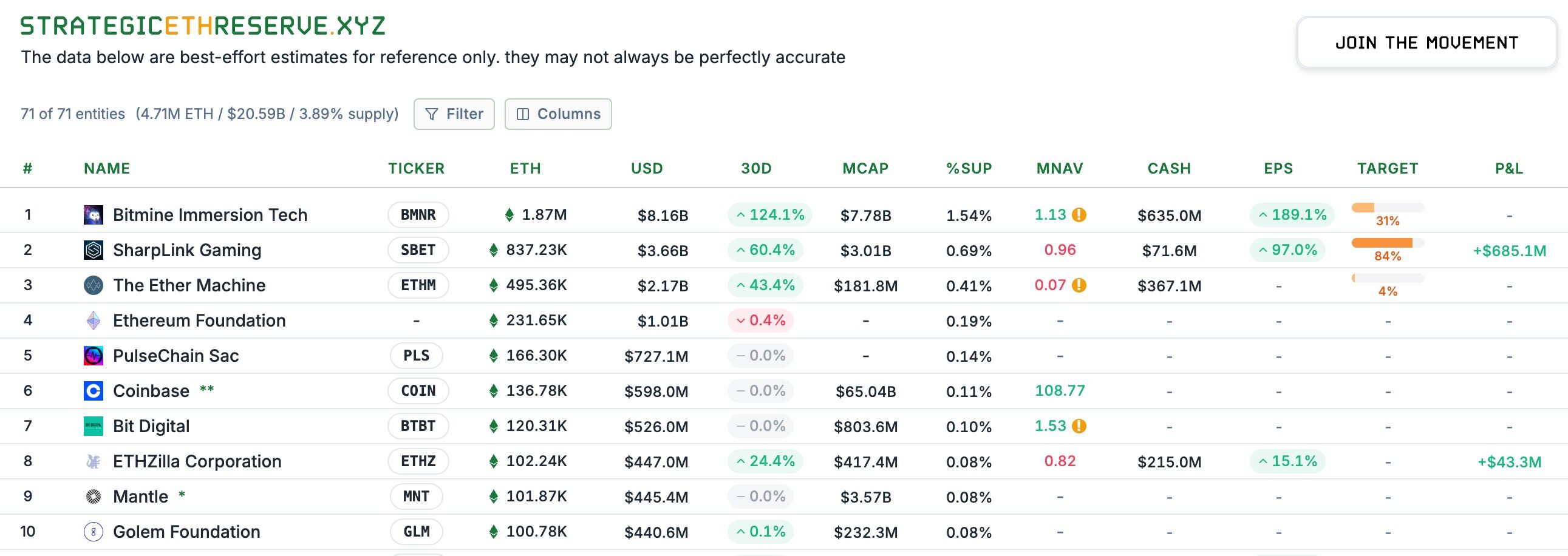

- BitMine持仓187万枚ETH,价值81.6亿美元。

- 华尔街资产代币化多基于以太坊进行。

- 财库公司策略可加速每股ETH持有量增长。

- 市场影响:推动ETH机构化进程加速。

- 时效性标注:中期影响。

This article comes from: Medici Network

Compiled by Odaily Planet Daily ( @OdailyChina ); Translated by Azuma ( @azuma_eth )

Editor's Note: What's driving the strongest buying force behind ETH's recent surge? The answer is undoubtedly ETH Treasury. With the continued increase in holdings by BitMine (BMNR) and Sharplink Gaming (SBET), the power of ETH's influence has quietly shifted. For more details, see " Unveiling the Two Key Players Behind ETH's Recent Surge: Tom Lee vs. Joseph Rubin ."

Strategic ETH Reserve data shows that as of September 4th, Beijing time, BItMine's ETH holdings have reached 1.87 million, worth approximately US$8.16 billion. BitMine's helmsman Tom Lee has long become the whale with the most say in the entire Ethereum ecosystem.

On the evening of September 3rd, Tom Lee participated in an interview on Medici Network's podcast, Level Up. In the conversation, Tom Lee discussed ETH's position in global finance, BitMine's rise as a leading ETH treasury, and the macroeconomic environment surrounding digital assets. Tom Lee also shared his views on the long-term potential of cryptocurrencies, his vision for decentralization, and BitMine's plans to further increase its reserve size.

The following is the original content of the interview, translated by Odaily Planet Daily - for the sake of reading fluency, some content has been deleted.

- Host: Could you please briefly tell us your story? How did you get involved in the cryptocurrency market? (When introducing Tom Lee, the host called him "the man with the best hair on Wall Street" in addition to his regular title.)

Tom Lee: To put it simply, my entire career after graduating from Wharton has been essentially one job: market research. I first worked at Kidder, Peabody & Company, focusing on the technology industry, particularly wireless communications, from 1993 to 2007.

That experience taught me some important lessons. Wireless communications were still in their infancy—there were only 37 million mobile phones in the world at the time, compared to nearly 8 billion today. Growth was exponential. But I was surprised to learn how skeptical many of my customers were of wireless technology. They viewed the core of the telecom industry at the time as long-distance and local calling, and mobile phones as just a "supercharged wireless phone" that might eventually become free.

I realized then that fund managers in their 40s and 50s often don't truly understand technological disruption because they're essentially vested interests. I later became JPMorgan Chase's chief strategist, a position I held until 2014. I then founded Fundstrat. Our original goal was to establish the first Wall Street firm to attempt to democratize institutional research—to make research previously available only to hedge funds and large asset managers accessible to the broader public. We wanted to make the research services we previously provided to hedge funds and large institutions available to the public.

Then, around 2017, I started noticing news reports about Bitcoin breaking through $1,000. This reminded me of my time on the JPMorgan FX team, where we had discussed Bitcoin numerous times. Back then, the price was less than $100, and the core of the discussion was whether this digital currency could be recognized as a form of money.

At JPMorgan, however, the attitude was very negative, with people viewing Bitcoin as little more than a tool for drug dealers and smugglers. But in my 20-year career at the time, I had never seen an asset go from less than $100 to $1,000 and have a market capitalization exceeding $10 billion. This was definitely something I couldn't ignore; I had to research it.

So we started researching. Although I didn’t fully understand at the time why a “proof-of-work blockchain” could be a store of value, I discovered that just two variables could explain over 90% of Bitcoin’s growth from 2010 to 2017: the number of wallets and the activity within each wallet.

Based on these two variables, we can even model and deduce Bitcoin's possible future trends. This was my first real "journey" into the crypto space. So, when the price of Bitcoin was still below $1,000, we released our first white paper. We proposed that if Bitcoin were considered a gold substitute, and it only accounted for 5% of the gold market, then its reasonable price would be $25,000. This was our prediction for Bitcoin's price in 2022, and by 2022, the price was indeed around $25,000.

- Host: You just talked about BTC, but you're also doing some interesting things with ETH. Can we talk about the macro opportunities for ETH?

Tom Lee: For a long time, roughly from 2017 to 2025, our core view in the crypto space has been that Bitcoin occupies a very clear position in many people's portfolios because it has not only been proven in terms of scale and stability, but more importantly, it can serve as a means of storing value.

When we think about how investors should allocate their assets beyond Bitcoin, there are many projects on the market—such as Solana, Sui, and the various projects you often write about. But starting this year, we took a serious look at Ethereum.

Here's why: I think the regulatory environment in the US has been trending in a favorable direction this year, which has led Wall Street to take cryptocurrencies and blockchain more seriously. Of course, the real "killer app" or so-called ChatGPT moment here was the stablecoin and Circle IPO, followed by the Genius Act and the SEC's Project Crypto initiative.

I think there are a lot of positive factors for ETH here, but the main one is - when we look at the asset tokenization projects that are being advanced on Wall Street, whether it's the US dollar or other assets, the vast majority of them are being done on Ethereum.

More importantly, I think people need to step back and consider this: What's happening on Wall Street in 2025 is very similar to the historical moment of 1971. In 1971, the US dollar was decoupled from gold, abandoning the gold standard. While gold certainly benefited, and many people bought into it, the real benefit wasn't gold itself, but rather the financial innovation that unfolded on Wall Street. Suddenly, the dollar became fiat currency, no longer backed by gold, and people had to build new "rails" for dollar transactions. Therefore, the real winner was Wall Street.

By 2025, blockchain innovations will be solving numerous problems, and Wall Street will be migrating to crypto. This, in my view, will be Ethereum's "1971 moment." This will create enormous opportunities, migrating a vast array of assets and transactions to the blockchain. Ethereum won't be the only winner, but it will be one of the primary winners.

From an institutional adoption perspective, I'm hearing a lot of discussion about it. Bitcoin is already very institutional. When I meet with investors, they all understand how to model and think about the future value of Bitcoin. As a result, Bitcoin has entered many portfolios. In comparison, ETH holdings are still very low, more like Bitcoin in 2017.

I think ETH is not really considered an “institutional asset” today, so it’s still very early days, which is why I think ETH has a bigger opportunity.

- Host: I know you set a target price for Ethereum, which is about $60,000. How did you make this prediction?

Tom Lee: Yes, that's right. But I have to clarify that ($60,000) is not a short-term target. So don't come to me on December 31st and say "it didn't go up that much." This is not a prediction that will be fulfilled next week.

In fact, I was referencing an analysis we did for Ethereum, done by Mosaics and other researchers. Their approach was to view the present as a turning point similar to 1971. They considered Ethereum's value from two perspectives: as a payment rail, and as a potential market share for Ethereum. I believe these two concepts overlap.

Their hypothesis is that if you look at the market covered by the banking system and assume half of it will move to the blockchain, Ethereum could capture approximately $3.88 trillion in value. Then, if you look at Swift and Visa, which process approximately $450 billion in payments annually, and assume that every transaction charges a gas fee and converts that into network revenue, and then give it a relatively conservative 30x P/E ratio, you get a valuation of around $3 trillion. Adding these two components together, Ethereum's fair valuation should be around $60,000, meaning it still has about 18 times the potential to grow from here.

- Host: The recent positive news for ETH is largely due to continued buying by digital asset treasury companies. As the chairman of BitMine, how do you think investors should view different investment avenues, such as choosing between ETFs, spot trading, and treasury company stocks?

Tom Lee: First of all, if someone wants to get ETH exposure through an ETF, that's totally fine because it allows you to invest directly in ETH without a big price difference, just like the BTC ETF, which gives you direct BTC exposure.

But if you look at BTC's treasury companies, MicroStrategy is larger than the largest BTC ETF. In other words, more investors are willing to hold BTC indirectly through MicroStrategy than through ETFs. The reason is very simple. Treasury companies do not give you a static ETH holding, they are actually helping you increase the amount of ETH corresponding to each share. MicroStrategy is an example: when they switched to a BTC strategy in August 2020, the stock price was about $13. Now it has risen to $400, an increase of about 30 times in five years. During the same period, BTC itself has increased from 11,000 to 120,000, an increase of about 11 times. This shows that MicroStrategy has successfully increased its holdings of BTC per share, while the BTC ETF has remained unchanged during this period.

In other words, an ETF might earn you 11x your investment over five years, but MicroStrategy's treasury strategy allows investors to earn even more. They leverage the liquidity and volatility of stocks to continuously increase their BTC holdings. Michael Saylor's strategy is similar, initially trading at $1 or $2 per share in BTC, to $227 today—a significant increase.

- Host: You just mentioned that traditional investors are showing increasing interest in Ethereum. I'm curious about how your attitudes have changed over the past few months when you've been talking to some of your non-crypto-native institutional clients about Treasury.

Tom Lee: Frankly, most people view crypto treasuries with skepticism . While many people have made good money investing in MicroStrategy, its holdings aren't as widespread as you might think, as there are still a large number of institutions that simply don't believe in crypto. For example, a recent Bank of America survey showed that 75% of institutional investors have zero exposure to crypto. In other words, three-quarters of them have never touched crypto assets. So when they see treasury companies, their immediate reaction is, "I might as well just buy the tokens."

So we spent a lot of time educating them in meetings. Taking BitMine's data as an example, the difference lies in the fact that treasury companies can help you increase the amount of ETH per share. For example, when we transitioned to an ETH treasury on July 8th, each share was worth only $4 in ETH. By the time we updated on July 27th, each share was worth $23 in ETH, a nearly sixfold increase in just one month. This significant difference illustrates the "accelerated ETH per share effect" of the treasury strategy.

- Host: There are many ETH treasury companies on the market, but BitMine is obviously the fastest. How did you do it?

Tom Lee: I think MicroStrategy provides a great template. Overstock was actually the first Bitcoin treasury company, but it didn't really sell to investors, and its stock price didn't benefit. Saylor was the first to achieve this with a more scalable and systematic approach, which really inspired us. Therefore, our strategy at BitMine is to maintain an extremely clear and concise path, relying entirely on common stock, without complex derivative structures, so that investors can understand it at a glance. We may expand strategies that leverage volatility or market capitalization in the future, but the first step is to have a clear strategy that convinces shareholders.

Why is this important? Investors need to believe they're buying more than just ETH, but a long-term macro trade opportunity. Companies like Palantir command premium valuations not only because of their product, but also because shareholders believe they own something meaningful. We need to convince investors that Ethereum is one of the biggest macro trade trends of the next 10-15 years.

- Host: Regarding the premiums for treasury companies, Michael Saylor has said that he's more aggressive in using ATM (issuing new shares in the public market) at premiums between 2.5 and 4 times. I presume that of all the treasury companies, you've been more aggressive in increasing your net asset value (NAV) through ATM, correct? Even at lower premiums, but that's enabled you to achieve consistent and strong NAV growth. How do you think about the appropriate premium multiple? As Saylor said, he's at one extreme, arguing that anything below 4 times isn't worth aggressively pursuing. What are your thoughts?

Tom Lee: I think there's a weird math problem here.

In theory, every financial instrument has certain trade-offs - and this may be a little technical for some of you listening - but common stock is actually a great financing tool because it gives everyone an equal opportunity to rise and there are no conflicts of interest - both new and old shareholders are betting on the future success of the company.

But when you raise capital with convertible bonds, the situation is different. Buyers aren't just interested in the stock price; they're also concerned about capturing volatility and potentially even eliminating it through hedging. Preferred stock and debt are essentially liabilities—while the ETH Treasury can pay its debts with staking proceeds, that capital is still debt. Debt holders don't care about the company's success, only the interest payments.

So, if you introduce conflicting motivations and different incentives when you change the capital structure, it can actually hurt the company - too many convertible bonds suppress volatility, which hinders the flywheel effect (volatility is the basis of stock liquidity).

Therefore, it's difficult to accurately calculate the range of tiered operations. Another important thing to keep in mind is that in the next crypto winter (which is inevitable), the companies with the cleanest balance sheets will win . This way, you won't be forced to raise capital at a discount to cover your payment obligations, nor will you create a natural short position due to derivative structures—when the stock price falls, the coverage requirements will trigger more short selling, creating a death spiral. This is why Bitmine keeps its structure simple.

If Treasury's premium to NAV is only 10%, it's hard to justify the ATM operation. Mathematically, selling shares at a 1.1x premium would require selling 100% of outstanding shares (doubling the total share capital) to have a positive impact on ETH per share, but at a 4x premium, only 25% would be needed to double ETH per share. I suspect Saylor's logic is there, but I have a different approach. I think a more strategic approach might be better.

- Host: You mentioned the inevitability of a down cycle. We've experienced several crypto winters. How do you think this will affect treasury companies?

Tom Lee: It's hard to say, but the best analogy is probably the oil services industry. The simplest analogy for a cryptocurrency treasury company is an oil company. Investors can buy oil, buy oil contracts (or even take physical delivery), but many people buy oil company stocks, like ExxonMobil or Chevron, which always trade at a premium to their proven reserves because these companies are actively acquiring more oil.

When capital markets become unfriendly, companies with more complex capital structures can collapse. During a crypto winter, valuation discrepancies can widen, and companies with the cleanest balance sheets can acquire assets, potentially even trading at a discount to net asset value.

- Host: Do you mean there will be some mergers/integrations between treasury companies?

Tom Lee: Yes, the Bankless folks made a great point. They said that while MicroStrategy is clearly a distant leader in the Bitcoin treasury space, there's no clear leader in the Ethereum treasury space. For now, everyone seems to be able to access funding, so consolidation isn't necessary just yet.

If consolidation were to occur, I think it would be more likely to occur in the Bitcoin treasury market , as Bitcoin has already seen a significant surge (although I remain bullish and believe it can reach $1 million), while Ethereum is still at a much earlier stage in terms of value realization. Therefore, the scenario you just described seems more likely to occur in Bitcoin.

- Host: You mentioned earlier that you want to maintain a clean balance sheet. During a crypto winter, if your company's stock price is trading at a discount, would you consider buying back shares? Would you do so through a bond issue, or would you maintain additional cash reserves in addition to your ETH holdings?

Tom Lee: That's a good question, but we can only discuss it theoretically. First, I don't believe a crypto winter is coming anytime soon. To be clear, we remain bullish on the market, so I don't foresee a winter anytime soon. Of course, it will happen at some point in the future, and by then, BitMine will have several sources of cash flow:

First, it comes from our traditional core business;

Second, staking rewards come from staking, as staking income can be converted into fiat currency when necessary and used to execute repurchases. In theory, the repurchase scale can even reach 3%, which is actually very large.

Third, consider whether to use the capital market to support repurchases.

At that time, companies with the cleanest balance sheets could do a lot. For example, they could borrow money using ETH as collateral. The market interest rate was known, so there were many ways to do it, but the practical implementation varied from company to company. If the balance sheet was complex, it would be virtually impossible to protect against a discount.

- Host: To keep BitMine's stock price above its NAV, would you consider an acquisition? Because that would be accretive per ETH. At what discount do you think an acquisition would make sense?

Tom Lee: I think every company has its own algorithm. If a company's stock price fails to rise above NAV despite ETH's significant upside potential, then it's simply following ETH's beta exposure. Companies that can command a premium must make alpha choices. In other words, you can buy more ETH to gain beta exposure, but to surpass it, you need an alpha strategy.

The reasons for discounts for each company may be different, such as poor liquidity, high debt, complex business, etc., which will lead to a reasonable premium or discount.

- Host: Let's change the topic. Although it is not directly related to BitMine, I would like to ask, do you think MicroStrategy will be included in the S&P 500 in September?

Tom Lee: The S&P 500 committee's work is confidential, but they do a great job. If you look at historical data, every 10 years, over 20% of the index's returns come from companies that weren't included in the index a decade earlier. In other words, they (the S&P 500) are actively selecting stocks, not just mechanically picking them based on rules.

In fact, their performance is significantly better than the Wilshire 5000, a broad market index, and even the Russell 1000 (weighted by market capitalization). This suggests they aren't just selecting the largest companies, but rather applying a thematic approach. AI is certainly a key focus, as is cryptocurrencies. They are also considering reducing weightings in commodities-sensitive sectors.

- Host: Speaking of indexes, BitMine is growing very fast. Is it possible for it to be included in some indexes?

Tom Lee: The S&P series isn't currently possible because it requires positive net profit, which can only be achieved after we start native staking. The Russell index is quantitative, looking only at trading volume and free float market capitalization. The threshold for the Russell 1000 is approximately $5 billion, and it is reconstituted every June. Starting in 2026, it will be reconstituted semi-annually. By this standard, BitMine has already far exceeded the threshold.

- Moderator: I think we've pretty much concluded our discussion today. This has been a great conversation. Do you have any final thoughts or takeaways for the audience?

Tom Lee: Let me summarize: We are witnessing a historic moment in the financial industry. Blockchain solves numerous problems, democratizes finance, and breaks down the gatekeeper structures that previously controlled resources. Even when discussing universal basic income, blockchain and cryptocurrency offer solutions. Therefore, I believe we should not only remain optimistic about the short-term prices of Bitcoin and Ethereum, but also recognize their profound and positive impact on society.