Take Profit or Open a Position: How to Observe Recent Market Changes from a Macro Perspective in Plain Language

- 核心观点:美联储降息预期主导加密市场短期走势。

- 关键要素:

- 鲍威尔转向关注就业而非通胀。

- 特朗普政府施压降息缓解债务压力。

- 非农数据将决定9月降息概率。

- 市场影响:加密市场波动加剧,政策敏感性提升。

- 时效性标注:短期影响。

By @Web 3 Mario

The market seems to have recently entered an unpredictable phase. Blue-chip cryptocurrencies remain volatile at high levels, with their overall direction uncertain. The altcoin market has not yet experienced the anticipated full-scale bull run, while DAT assets or crypto-to-equity stocks have dominated the traditional financial markets. Prior to this, many voices on social media have characterized this bull market as driven by traditional capital. I strongly agree with this assessment, and this sector of capital exhibits several distinct characteristics compared to previous market cycles, such as a strong influence on macroeconomic factors, lower risk appetite, greater concentration of capital, weaker wealth spillovers, and less pronounced sector rotation. Therefore, during this period of significant macroeconomic changes, re-examining these developments will help us make informed decisions. Overall, I believe that as Powell adjusts the Fed's decision-making logic, the performance of the US job market will, in the short term, determine market confidence in the September rate cut, thereby influencing the prices of risky assets.

What did Powell's speech change?

We know that in the months leading up to this, the core market debate surrounding the macroeconomic situation has been whether the Federal Reserve under Powell's leadership can deliver on the Trump administration's desire to significantly cut interest rates this year. First, why is the Trump administration so eager to pressure the Fed to cut rates, even risking the Fed's independence and, by extension, the dollar's credibility, by using administrative power to influence the Fed's decisions? In previous articles, we've analyzed the Trump administration's goal of "reshoreing manufacturing" in US economic policy, but how this goal has encountered two obstacles in its implementation:

- Internal costs are too high to cope with competition from international competitors;

- Government debt is too high, and there is no sufficient budget to encourage industrial relocation;

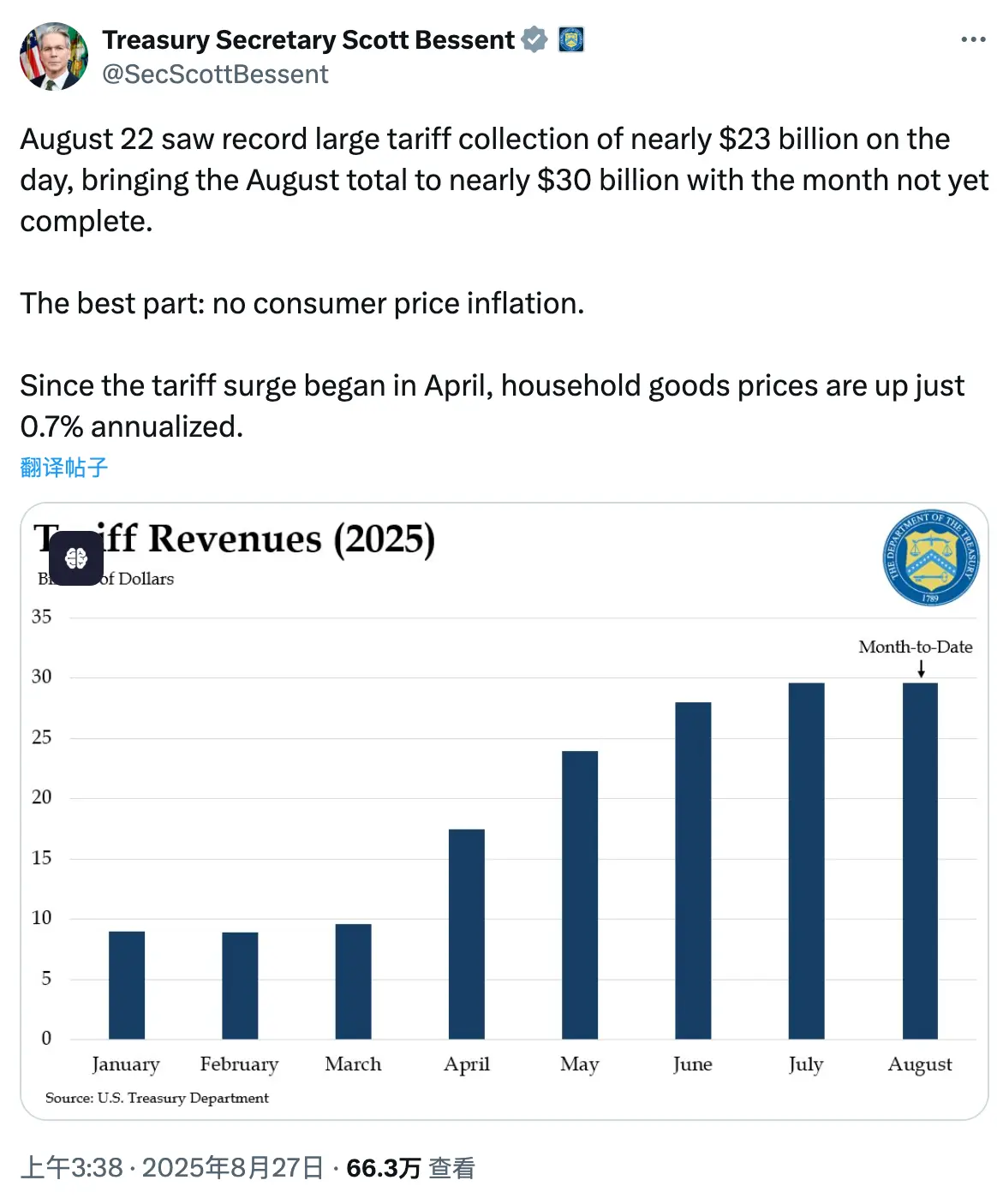

Over the past six months of the Trump administration, its policy implementation can be roughly divided into two steps. First, upon its election, it fulfilled its campaign promises as much as possible to strengthen its authority, such as granting DOGE extensive rights and shifting cryptocurrency policy. After consolidating its base, the Trump administration began implementing drastic tariff measures. The reason for this post-solidification push is that raising tariffs would raise market concerns about imported inflation, thereby increasing internal resistance. Having secured strong authority, and after months of negotiations, Trump's tariff policy framework has been initially established and is showing results. According to US Treasury Secretary Benson, as of August 22nd, tariffs have generated a nearly $100 billion fiscal surplus for the United States over the past six months, with an expected $300 billion surplus this year. Furthermore, the administration has secured investment promises from numerous countries, including $550 billion from Japan and $600 billion and $750 billion in energy orders from the European Union.

It can be said that although internal costs cannot be reduced immediately in a short period of time, such as labor costs and logistics costs, because these costs require the United States to reset the costs of various factors through a market clearing like a great depression, the Trump administration has changed the domestic market competition structure and capital structure to a certain extent through tariffs. Therefore, the time is right to start the next policy layout, that is, the FED interest rate cut.

So what can a rate cut change? There are two main points. First, it will ease debt pressure. As we know, during the tenure of previous Treasury Secretary Janet Yellen, the US Treasury increased its issuance of short-term debt, a decision Bensent maintained. The advantage of this approach is that short-term debt interest rates are regulated by the Federal Reserve, reducing the drag of long-term debt on the fiscal budget. Currently, market demand for short-term US Treasury bonds is strong, which helps lower financing costs. However, the obvious downside is that shortening debt duration increases short-term repayment pressure, which is why recent negotiations on the debt ceiling have become more intense. Rate cuts, on the other hand, mean less pressure on short-term debt payments. Second, rate cuts will reduce financing costs for small and medium-sized enterprises (SMEs), facilitating the development of industrial chains. Compared to large enterprises, SMEs typically rely more heavily on bank debt financing for their operations. Therefore, in a high-interest environment, SMEs' willingness to expand financing will be dampened. Furthermore, after tariffs have altered the competitive structure of the domestic market, it is imperative to incentivize SMEs to expand production and help them quickly fill supply gaps in the market to prevent inflation. Therefore, to sum up, the Trump administration will spare no effort to pressure the Federal Reserve to cut interest rates at this time, rather than just using smokescreens.

Whether it's actively intervening in the renovation of the Federal Reserve headquarters or relentlessly attacking the far-left, progressive, and hawkish Governor Cook, these measures demonstrate the Trump administration's active promotion. These tactics appeared to be working effectively in Powell's speech at Jackson Hole, the annual gathering of global central banks, last week. The market was most surprised by Powell's speech, which consistently defends the independence of the Federal Reserve, but he seemed to succumb to Trump's strong pressure. Several key points in his speech highlight his stance:

1. It is clear that the risks in the US economy have shifted from inflation to the job market;

2. The impact of tariffs on inflation takes time to manifest and is not a factor that triggers an inflationary spiral;

3. An update to the monetary policy framework, which interestingly reduces the emphasis on the effective lower bound on interest rates as a “characteristic of normal economic conditions.”

In layman's terms, the Federal Reserve is no longer concerned about inflation caused by tariffs, but is now more concerned about the collapse of the job market caused by an economic recession. At the same time, the level of interest rate cuts can be considered unlimited. The description of the effective interest rate should be expanded upon. The so-called effective interest rate refers to the level at which, when a central bank uses conventional monetary policy (primarily adjusting short-term policy interest rates), further cuts will have no impact on the economy. This shift aligns with the core of Trump's policies, as this "two-pronged approach" has sparked market expectations for further liquidity easing.

Impact on the cryptocurrency market

We know that the cryptocurrency market is often seen as a canary in the sand for speculative sentiment in the global risk asset market. Therefore, cryptocurrencies all saw a surge after the announcement of the speech. The subsequent pullback shows that the market had already priced in an interest rate cut this year to a certain extent. After the new trading logic was determined, the market shifted from the initial emotional expectations to rational expectations. Therefore, sufficient evidence is still needed to assess the extent of the interest rate cut.

As for how deep the pullback will be, I believe the performance of ETH, which has been the hottest cryptocurrency of the recent period, is worth watching. As long as the price doesn't fall below this rising channel in the short term, I believe investor sentiment hasn't significantly reversed, and therefore the risk is manageable. Over the coming week, indicators related to the job market will significantly influence cryptocurrency trends, particularly next Friday's non-farm payroll data, which will bring significant market volatility. If the employment data falls short of expectations, the probability of a September Fed rate cut will increase significantly. If it exceeds expectations, it will demonstrate the resilience of the US job market, and pressure for rate cuts will be felt, potentially leading to a further market correction. Regardless, the recent policy market situation reminds me of the CPI-dominated market in 2023.