Random talk about block space: the most precious commodity in the crypto world

Original author:Nate

Original compilation: Deep Chao TechFlow

Transactions, data storage and calculations on the blockchain are block space. Intuitively, the transactions included in a block are the block space.

In various articles, posts, and podcasts, blockspace is increasingly being referred to as “the best product” or “the most important commodity.” Understanding what blockspace is and how to create and value it can be confusing, especially since it is constantly evolving.

Not all block spaces are created equal, they actually vary quite a bit. Blockspace is a commodity that can be easily rated based on common characteristics such as security, flexibility, and decentralization. This article will detail each characteristic, give some examples, and then explore the market players for the most valuable digital goods that currently exist.

First, let’s briefly introduce the consensus mechanism for protecting block space:

Proof of Work (PoW) requires miners to solve complex mathematical problems to verify transactions and create new blocks. The first miner to solve the problem will be rewarded with newly minted tokens. The process of solving these problems requires a large amount of computing power, making it difficult for any one miner to control more than 50% of the networks computing power. If a miner can control more than 50%, they can launch a 51% attack. In a 51% attack, miners with the majority of computing power can manipulate transactions or even reverse them, potentially allowing them to double-spend coins. Today, almost all PoW production is done through mining pools.

Proof of Stake (PoS) is a newer consensus mechanism that requires users (called validators) to provide a certain amount of cryptocurrency as collateral in order to validate transactions and create new blocks. Validators are selected based on the number of tokens they stake and are incentivized to act in the best interest of the network.

quality

Blockspaces can be constructed and generated in many different ways, and can be used for a variety of different purposes. Each blockspace market has different levels of security, decentralization, and assurance, as well as different options for blockspace size, quantity, and verification methods. There are a few different qualities you may want to evaluate when deciding to participate in the blockspace economy.

safety

Perhaps the most important quality is the security of the blockchain. How much resources and effort is required to attack the chain? This is often referred to as a 51% attack, but there are other types of consensus mechanisms that only require 33% of producers to agree.

A common metric for measuring blockchain security is to look at the “cost of attack.” How many resources would be needed to rent and/or purchase computing power/stake in order to control 51% of the network?

Complete takeovers of the blockchain are very rare and have only happened a few times in history, one of which was the takeover of the steem blockchain by Justin Sun. Ive often thought about why blockchains like Dash, Bitcoin SV and even well-known blockchains like Zcash havent seen more complete takeovers yet, but if their security is so bad, its easy to infer that their other qualities are just as bad, if not worse. Oops.

A more common attack is a simple blockchain reorganization. This is often seen on blockchains like Polygon, which reorganizes frequently. It should be noted that given Polygons probabilistic consensus, its reorganizations are not necessarily malicious, but reorganizations may also be an attack in which producers reorganize transactions in previous blocks for their own benefit.

To better understand the problems posed by restructuring, consider the following example: A small company bids on a billboard on a popular highway. The companys bosses are paying 20% more than initially expected after fierce competition from rivals. Satisfied with the billboard, they send their design to the billboard company. A few weeks later, the small business owner drove to the highway to check out his ad, only to see a competitor appear on the billboard. This is similar to what happens in a reorganization, where your previously paid transactions are rolled back and reorganized.

Security is probably the most important feature for those consuming block space, who want to ensure that the transactions they pay for are secure and relatively immutable. This directly affects the value of block space, producers’ willingness to expend resources to produce block space, and ultimately traders’ interest in trading it.

Decentralization

The degree of decentralization of a blockchain is a very important quality on par with its security. Decentralization has several equally important parts:

Satoshi coefficient;

different operators;

geographical distribution;

client diversity;

Unique hardware.

The Nakamoto coefficient is undoubtedly the most commonly used indicator to measure the degree of decentralization of a blockchain. It’s a very simple formula: the number of validators or the percentage of computing power required for an attack, and it helps to understand the number of validators needed to collude together to conduct a successful attack to prevent any blockchain from functioning properly.

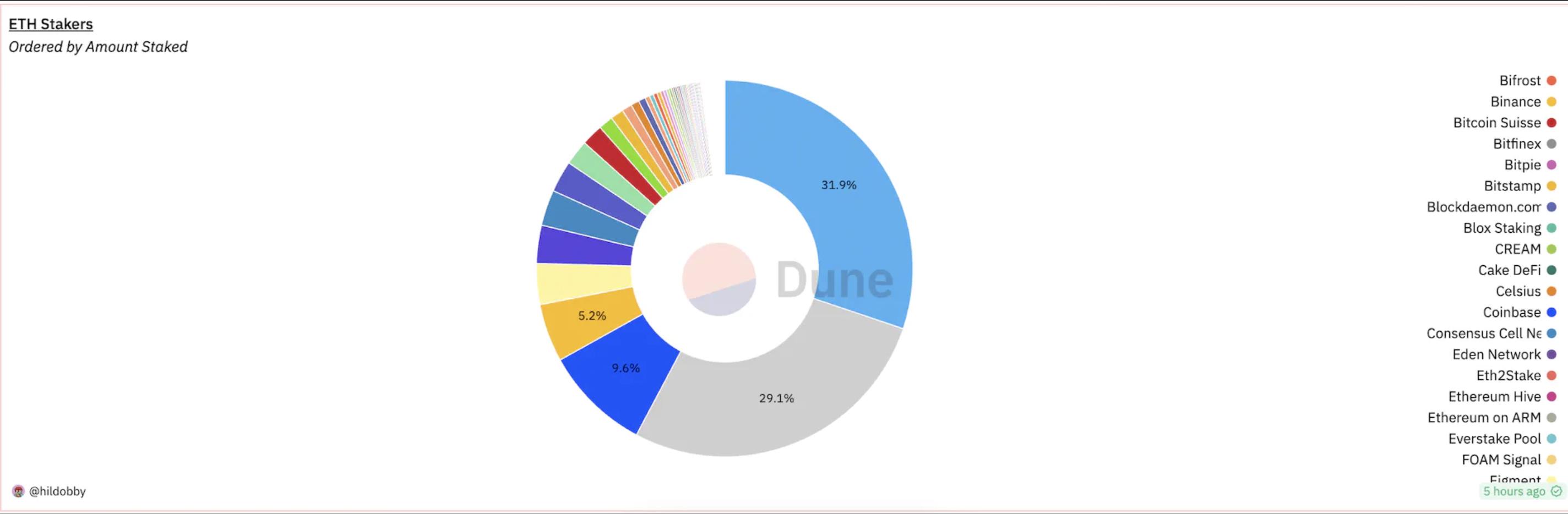

Just as important as the number of actors is the number of different actors required to collude. For example, Coinbase operates approximately 7% of Ethereum validators. Lido is a liquidity staking provider that currently accounts for approximately 33% of the validators on the Ethereum network. Lido is not a validator itself, but partners with trusted operators in the blockchain space such as Coinbase. Calculating the base share they represent for Lido operations plus the number of validators, Coinbase actually accounts for about 12% of the entire network.

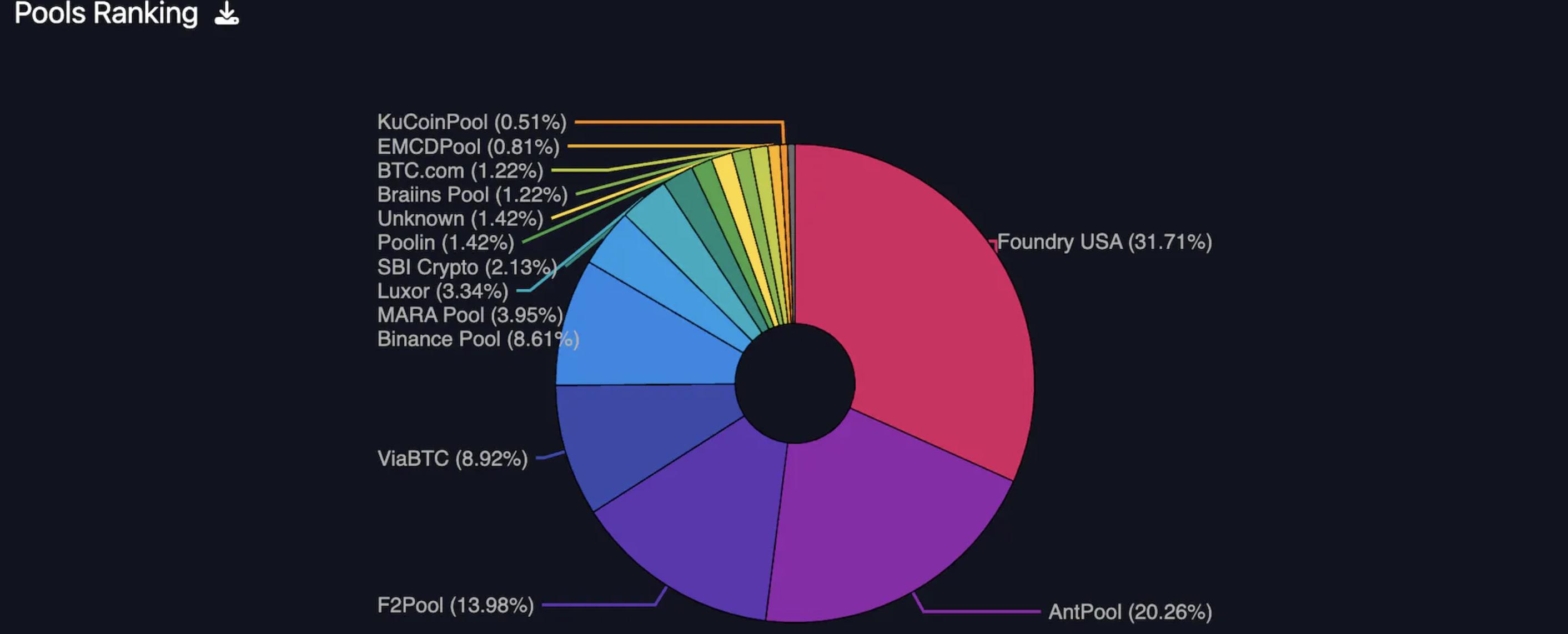

Bitcoin is often considered the leader in decentralization, but the Satoshi coefficient is only around 5. While it is true that there are many unique block-producing participants, Bitcoin mining pools have complete control over the ordering of transactions in blocks (until Stratum V2 is fully implemented and used).

For most of Bitcoins history, 1 or 2 mining pools controlled over 33% of the computing power and thus the order of transactions in a given block.

Some market participants are very concerned about the order of their transactions within a specific block, and having a single party completely control the order greatly reduces the quality of the block space for them. Note that this is also true for Rollups with a single orderer.

A single aspect ordering/structuring the majority of the block space would intuitively be very detrimental to decentralization, but could also have a significant impact on producers extracting additional value for themselves. This is often referred to as Maximum Extractable Value (MEV), and a producer can extract a significant amount of value. It is also important to note that MEV is helpful for the proper functioning of certain applications, such as liquidation, arbitrage to keep the market competitive, and even Squeeth rebalancing required searchers, are all good examples.

MEV is such a large and important concept when discussing the blockchain space (the MEV supply chain is now a multi-billion dollar industry in its own right) that it probably deserves its own article. But here are a few things to know:

It is important to establish an independent MEV supply chain so as not to harm block space consumers. Many protocols are solving this problem:

Flashbots ;

Solana’s Jito;

Cosmos Skip;

Stratum V2 for Bitcoin;

(Still waiting for MEV solution from Polkadot and Near)

MEV also exists in Bitcoin, large mining pools have begun extracting it, and the amount of MEV that can be extracted is directly related to the value of a given block space.

size, quantity, verification

The actual size of the block space is also an important factor when judging quality. These are very simple and clearly defined:

How big is the block? How many transactions can a block hold? How much data can a block hold?

How often are blocks generated? How many blocks are produced in a day?

How does the network reach consensus on blocks?

Questions about the size and quantity of block space are often a quality that consumers or traders need to consider. If a consumer wishes to complete a transaction within 1 hour, how many blocks are available to bid for transaction space? As a trader, how scarce is block space?

Assessing how well the network reaches consensus on blocks may be a quality that an institutional consumer cares about, perhaps a fund or trading firm, but more likely an application built on top of a given block space, such as an exchange, custodial service or Tier 2. Exchanges may evaluate how the network forms consensus as it may impact user execution. Some examples of consensus among different network participants:

Rotation/responsible person election:

In a round-robin rotation, validators are periodically selected to construct, propose, and single-handedly include entire blocks.

Examples include Solana, Cosmos and Polygon.

General consensus:

In a general consensus network, the producer broadcasts the block to the network REST, and if it is consistent, the block is added.

Examples include Bitcoin.

Single sorter:

Most layer 2 networks implement a single sequencer, which sorts all transactions, forms them into blocks, and publishes them to layer 1 or the data available layer.

Examples include Arbitrum and Optimism.

The manner in which consensus is reached has slightly different effects on the execution of the relevant exchanges.

Rotating leader elections are typically very fast, but for networks that have not yet abstracted away the block building layer, exchange participants who are also validators have an advantage.

General consensus enforces fairest execution to exchange users, but currently has difficulty handling throughput. As of 2023, we haven’t really seen a fully functional and fast order book on a blockchain using general consensus.

Exchanges built on networks that currently use centralized orderers need to determine the likelihood that orderers operators will front-run or extract certain types of value in trade orders.

A fourth option for exchanges is to take certain parts of their infrastructure offline, such as their order books. This is also highlighted in the hybrid section of AMM and order book.

Availability

It is important to ensure that consumption, access, and production of block space are widely available and readily available.

Do you have easy access to block space? Is it always available or are there chain stops or downtime? How easy is it to run your own RPC node or access publicly available nodes? Are RPCs frequently overloaded, and do they have sustained uptime?

uptime

As a consumer, it is important that you have ready access to the Blockspace Marketplace. If a blockchain stops or goes down frequently, you cant use it reliably.

For example, you are a new liquidity provider looking to provide liquidity to a centralized liquidity AMM and are choosing between Solana and the Ethereum blockchain. Assessed solely on availability characteristics, the choice is simple, over the past year Solana and seemingly all layer 2 have experienced days of downtime, with the entire chain completely unavailable.

Chain state and storage

As a producer (and possibly as a consumer), it may be an important consideration to consider accessibility for downloading, validating, and storing the complete chain state.

As a blockspace producer, you want to ensure that you have extremely high uptime and minimal dependence on others in case they go down. Some blockchains like Solana or Near actually require you to download a snapshot of the chain data from AWS S 3, Google BigTable, or other validators, often with little or no way to synchronize and store the chain data yourself.

Chain state and storage is also a very important consideration for applications or protocols that require historical data. On Bitcoin or Ethereum, it only takes a few days to fully synchronize a node, with complete historical data. Solanas complete chain state, on the other hand, is primarily stored in the Google BigTable database, requiring petabytes of data, making synchronization and storage nearly impossible for any ordinary consumer.

costs and fees

Blockspace is valuable and has various costs and fees associated with its production and consumption.

As a producer, there are more traditional costs, such as the upfront purchase and/or ongoing cost of the various hardware and software that enable you to run on the network. In most cases, the initial capital outlay of issuing tokens as collateral is also required (which is the case in PoS networks). In return, you typically receive a block reward from the network, which may also include fees paid by consumers of the block space you produce.

As a consumer, you pay a fee to a block producer in order to use block space on a given network (this is in addition to the additional fees you may have to pay the protocol for interaction).

Costs and fees vary depending on the implementation of the blockchain and the design of the fee market. Typically the chain implements one of the following designs:

Priority Gas Auction (PGA): Consumers who want to utilize block space will submit their transactions with a given fee, and the transactions go into the mempool. Since producers capture fees in blocks, they (usually) order transactions by highest fee. This is a very simple fee market design and the most common.

EIP 1559: Consumers who want to use block space will pay a base fee (which is burned) and a priority fee (or tip) to the block producer. The purpose of introduction is to provide better consistency in estimating the fees that consumers need to pay.

The design of the fee market has a large impact on the amount and potential willingness of consumers to pay, as well as the rewards producers can expect to receive from block production.

flexibility

Blockspaces can be highly adaptable or very static. Most of the time, consumers may prefer a stable and predictable consumption space, but in some use cases, consumers (usually protocols) may want their space to be highly adaptable and flexible.

Flexible block space means blocks can be structured differently depending on various use cases. It could be adding pre- and post-processing instructions at the validator level, allowing block size to fluctuate, or being able to abstract block construction.

For example, you are a lending protocol and have begun to explore launching your own blockchain. They have several options to consider launching:

Application chain based on Cosmos;

Rollup based on Optimism or Arbitrum technology stack;

Build a parachain on Polkadot.

Each of these has different security, decentralization, and usage considerations.

The Cosmos AppChain requires you to build security yourself through an incentivized set of validators, but allows you great flexibility in consensus, block construction, and transaction execution.

Building a Rollup using the Optimism stack is (currently) more centralized due to the single sequencer, but allows you to have a very fast EVM compatible block space.

Polkadot parachains allow you to use Polkadots shared security model, but require you to bid a considerable amount of DOT in the auction to be included.

in short:

The Cosmos AppChain offers ultimate flexibility in block space creation, control, and security.

Rollup offers flexible block space creation, but control and security are currently limited to a single centralized orderer.

Parachains bootstrap security from Polkadot mainnet...but are expensive.

Bitcoin, Ethereum, Polkadot, etc. all generate common block spaces. Osmosis, Aevo, Lyra, Sentential use customization and dedicated block space to improve their products.

In recent months, products like Caldera and Conduit have made it easier to launch OpStack, Arbitrum or other Rollup/app chains.

market participants

The blockspace market is very complex, but can be broadly divided into producers and consumers.

producer

Blockspace producers are network participants who take a set of transactions to be included and actually build them into a block by ordering them. This is usually one of the roles of a validator, miner, or mining pool on a given chain. With the rise of the MEV protocol, this block construction has been largely outsourced to individual actors called builders. The MEV supply chain is now very complex, involving many different actors, as shown in the figure below.

In terms of proof-of-work, mining pools have complete autonomy over the ordering of transactions in blocks mined by miners in the pool. This will change with the release and adoption of stratum v2 and allow individual miners to express transaction ordering preferences to the mining pool.

Producers want to produce high-value block space, or expect to do so in the future. Here is a list of some of the big producers in various blockchains:

Coinbase Cloud;

Chorus One;

Jump Crypto;

Figment;

Marathon ;

Galaxy Digital;

Riot;

Foundry.

consumer

A consumer is any entity that uses the block space being produced. Practical uses can be a number of different things such as money transfers, exchanges/trades, other financial transactions, etc.

However, the biggest consumers are often overlooked. Asset issuers, exchanges, and protocols built on top of blockchains are often some of the largest consumers. Below is a list of some of the major consumer agreements/companies:

Asset issuers such as Circle, Tether, and Paxos;

Centralized exchanges such as Coinbase and Binance;

Layer 2 such as Arbitrum, Optimism, etc. (more and more such environments as many application teams deploy their own Rollups);

And of course there are big users/traders.

Valuation

Block space requirements can vary widely. Data Always provides a good overview of block space requirements in 2022. Below is the block space fee schedule for the major protocols:

It is worth noting that most of the fees paid in the native protocol are block subsidies. A valuable metric to focus on true demand and growth is user transaction fees as a percentage of total block rewards. For example, on Bitcoin this averages around 2-4%, but on Ethereum it is similar during periods of low activity but can spike to over 60%. When tracking agreements with mature MEV supply chains, tips should also be included.

Some chains have taken the time to develop unique fee markets, one is Ethereum’s EIP 1559. This upgrade has multiple goals, such as reducing fee volatility, but also has the important long-term goal of preventing blockchain instability in a world without ongoing native token issuance. 1559 causes the base fee to be burned and the priority fee to go to the validator, which reduces the importance/proportion of the block subsidy in the overall block reward.

To maintain its promise of cheap fees, Solana created a native fee market where transaction fees interact natively with each different contract. Jupiters transaction fees will not increase if there is high demand NFT minting on Magic Eden. This change is very consumer-focused as it actually reduces the fees that validators can expect to receive. However, given that Solana has a well-established MEV supply chain, nativeization fees may bring in more users and thus more fees through MEV tips.

Valuation of the block space is still in the very early stages, with the majority of block rewards on a given chain coming from predictable block subsidies, without much change in rewards and corresponding valuations. However, as halvings, increased demand, the creation of MEV supply chains, etc., transaction fees/tips become a larger and larger proportion of total block rewards, valuations will become more unpredictable and introduce unique trading opportunities.

trade

The pricing of block space is appalling. In many cases, blockchains misprice their payments to producers as they continue to print more inflation for terrible quality block space. Most block space is cheap and abundant, and only a small amount of block space is valuable.

This is where I look forward to new implementations of block reward and fee markets. Currently, most blockchains propose static block subsidies in white papers, perhaps consistent with some kind of de-inflation schedule. How do they determine how to accurately price their block space before their blockchain goes live? I look forward to finalizing the new implementation of block subsidies.

Considering these markets are so nascent, you may just be a producer or consumer and not even consider that you can trade block space. Currently, these transactions are typically expressed in the form of swaps, forwards, and futures, but there are also more unique instruments such as royalties, block inclusion reservations, and gas tokens.

The main places where block space is currently traded are:

Luxor, you can trade Bitcoins non-deliverable forward contract Hashprice.

Alkimiya, a more flexible exchange marketplace where you can trade Bitcoin and Ethereum block space swaps and possibly gas swaps.

Some projects with great potential:

Overlay, a perpetual futures platform that allows you to trade native data feeds, has various blockspace components explicitly mentioned in the documentation.

Oiler, has multiple products, one is Pitchlake where you can trade Ethereum for base fees.

Volmex, a volatility trading platform, I could see it eventually launching something like fees or validator rewards for the Volatility Index.

An interesting product idea is to form a block space quality index based on the above characteristics and form a block space exchange market between blockchains, such as the exchange between the block space requirements of Bitcoin and Ethereum.

In addition to the speculative markets that are being established such as Luxor, Alkimiya, etc., these markets are extremely important for transferring risk between block space producers and those who are willing to bear the risk. As public companies and energy companies enter the Bitcoin production space, they will want to reduce the volatility of their cash flows. As layer 2 becomes more complex, they will want to hedge layer 1 transaction fees. As exchanges and asset issuers seek to operate more efficiently, hedging their variable transaction costs becomes important.

Overall, Im extremely excited about the introduction of stronger capital markets around blockspace consumption and production, and interested in seeing how it develops.