How do exchanges and investors respond to the Lehman moment?

The FTX incident can be called the "Lehman moment" of the encryption world. The development speed and scope of the incident have far exceeded previous imagination. And just last night, the U.S. Bureau of Labor Statistics released data showing that U.S. CPI in October rose 7.7% year-on-year, lower than market expectations of 7.9%, and a sharp drop from the previous value of 8.2%. The CPI rose by 0.4% month-on-month in October, which was also better than market expectations.

first level title

1. The overall crisis of the exchange

secondary title

1.1 Outflow of assets

The market has fallen severely, and capital flight is limited. Binance stabilizes, FTX gets gutted.

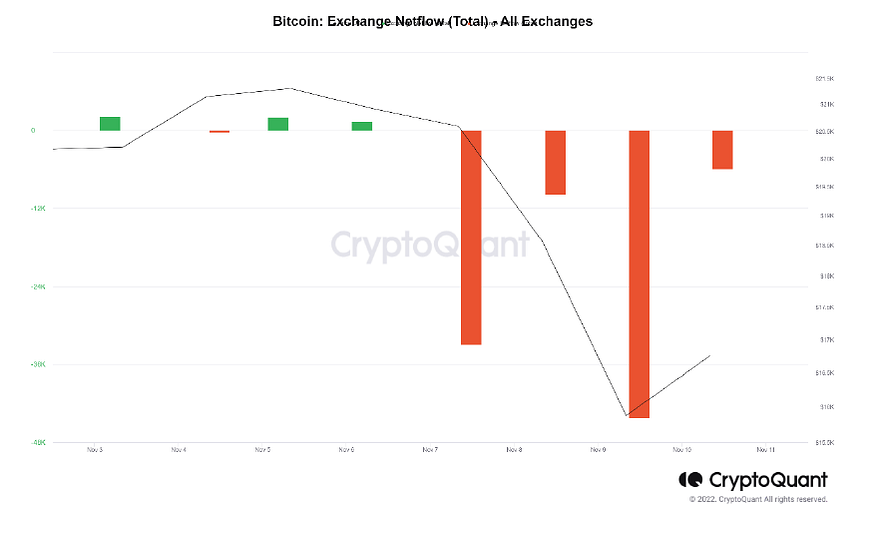

The figure below shows the BTC net inflow and outflow of mainstream exchanges in the past 7 days. Since November 7, the exchange has had a net outflow of 92.8 K BTC in the past four days, accounting for 4% of its total holdings. The situation is similar for stablecoins, with net outflows accounting for 3% of the total in the last 4 days. This is the third consecutive large net outflow of BTC this year. The previous two occurred on May 12-17 and June 15-17. The first of these was affected by the LUNA crash, and the second was affected by the Celsius thunderstorm and the Fed's first rate hike of 75 basis points. After the second large net outflow of BTC, the price of BTC dropped by 16%, but this time BTC has fallen by about 20%, and the market has not shown obvious signs of stabilization, which shows that this incident has a greater impact on the market.

Observing the BTC net outflow of mainstream exchanges, we found that except for the complete collapse of FTX, most exchanges did not experience a large outflow of assets. Binance only had a small outflow, while Huobi, Kucoin, and Bybit had net inflows. This shows that users have a relatively solid foundation of trust in these exchanges. Although there were rumors that Kucoin might have insufficient reserves, its CEO responded quickly and reassured users. Only OKX and Coinbase had large net asset outflows. This may be because Xu Mingxing supported SBF a few days ago. Coinbase has recently experienced a downtime. These incidents have aroused user concerns.

secondary title

1.2 Proof of reserves

Proof of reserves has become the touchstone, and the long-term mechanism is the key.

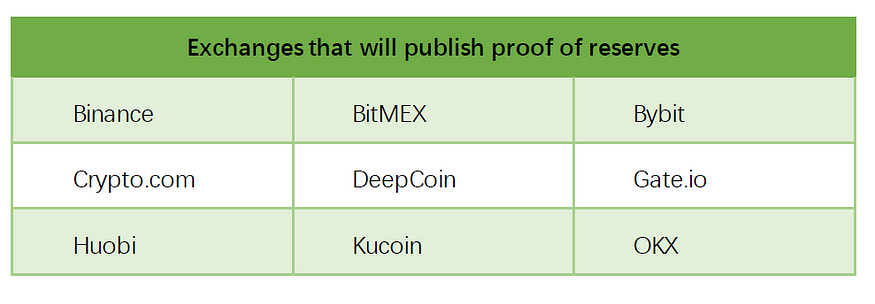

The most important thing for exchanges at the moment is to prove to users that they have not misappropriated users' assets. Since the outbreak of the FTX incident, several mainstream exchanges have issued announcements, saying that they will issue proof of reserve funds. Among them, Binance took the lead in announcing the cold/hot wallet addresses, and Huobi is also rapidly promoting the implementation of POR products, and because the acquisition has just been completed, the assets have been reviewed by multiple parties, and the credibility is relatively high.

Publishing the proof of reserves reflects the sense of responsibility of the exchange, which has a great effect on stabilizing the mood of users. The exchange that dared to announce this at the first time has a high probability of not misappropriating user assets. If there is no response to this, users will inevitably become more anxious and turn to competitors. Therefore, the reserve fund proves to be a touchstone, which can accelerate the clearing and reshuffle of the exchange industry.

This crisis has once again reminded the public that no platform can be trusted as long as it has a connection with finance. Only publicly verifiable data can be trusted, and only the strictest regulatory measures can protect the interests of investors. Due to the inconsistent policies of various countries, it takes a long time to form regulations. It is unrealistic to expect unified rules issued by regulatory agencies in multiple countries in the short term. A more feasible method is for many mainstream exchanges in the industry to jointly form a "rule" and stick to it: the misappropriation of user assets is regarded as a red line of operation and must not be touched; the reserve certificate is disclosed regularly. Such regulations have no legal effect, but users can freely decide whose services to use, so as to gradually eliminate violators and make the encryption market more mature through a long-term mechanism.

first level title

secondary title

text

2.1.1 Risk of serial liquidation

The market has witnessed a painful decline in recent days. Could there be a series of liquidation events? For this reason, we make an on-chain liquidation analysis of several mainstream currencies and currencies that are more closely related to FTX.

BTC and ETH are far away from the large-scale liquidation line, and the rest of the currencies are relatively safe, or have little impact on the market.

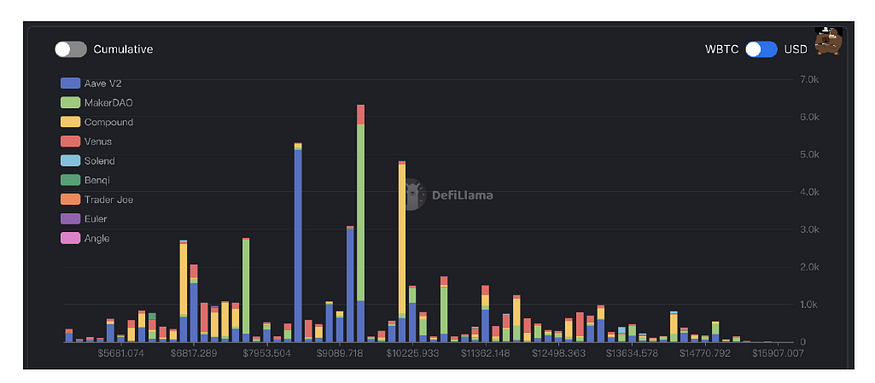

WBTC

WBTC has small settlements at 14933 and 14282, with a scale of 700-800 coins, mainly compound maker. The large amount of liquidation is between 8000-10000, about 5000 pieces, generally will not reach this price, and needs to be promoted by major events.

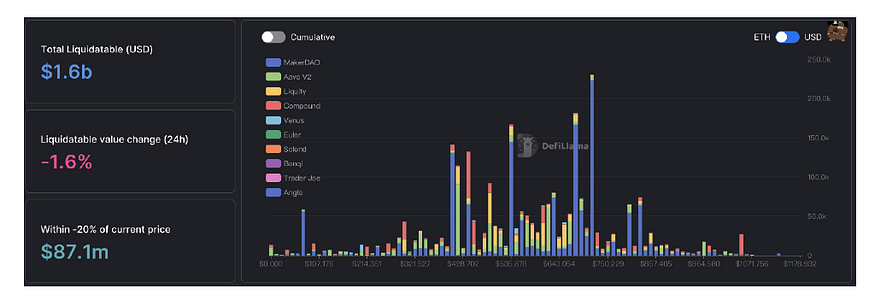

ETH

1050 has a small-scale forced liquidation risk (worth US$ 28M), mainly based on compound. There are two large-amount liquidation lines, which are around 800–820 (worth 100M) and around 700 (worth 300M), both of which are dominated by makerdao. This is generally not achieved here, unless a major event pushes it.

SOL

SOL has a large liquidation risk of 0.37 M at 10.73, the current price is about 14 U, and the lowest point within 6 hours is 12.46. SOL has chips to be unlocked today, and market panic has always existed, which is more likely to be triggered. But in the short term, due to the extremely high open interest in perpetual contracts, the short-selling funding rate has reached as high as 30% a day. In the case of many short positions, it is difficult to go down smoothly, and there may be repeated rises and short positions. In addition, the Solana Foundation has postponed the unlocking of about 28.5 million SOL, so it is unlikely that SOL will drop sharply in the near future.

SUSHI

Although Alameda's xSUSHI holdings are high, the chain pledge is relatively healthy, because SUSHI is generally pledged in xsushi without leverage, so the risk of forced liquidation on the chain is small, and the subsequent additional pressure is small.

SRM

text

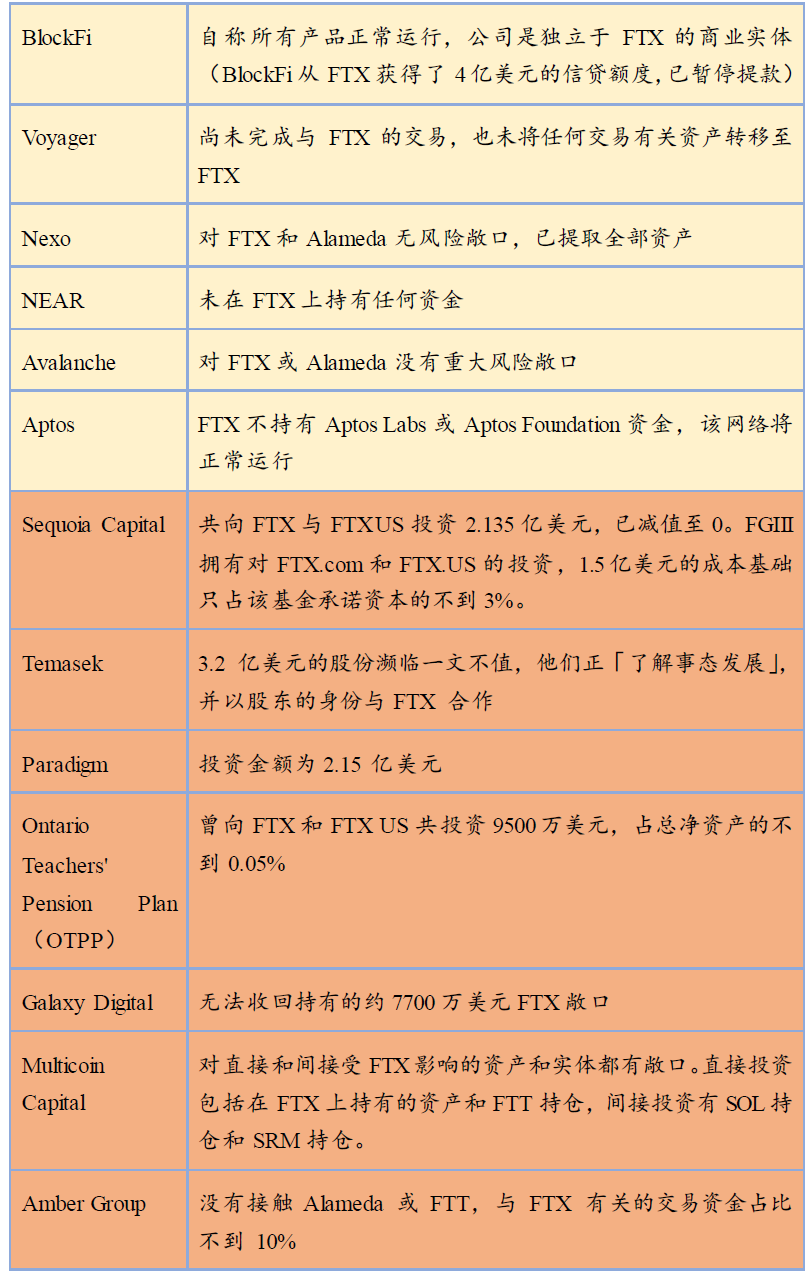

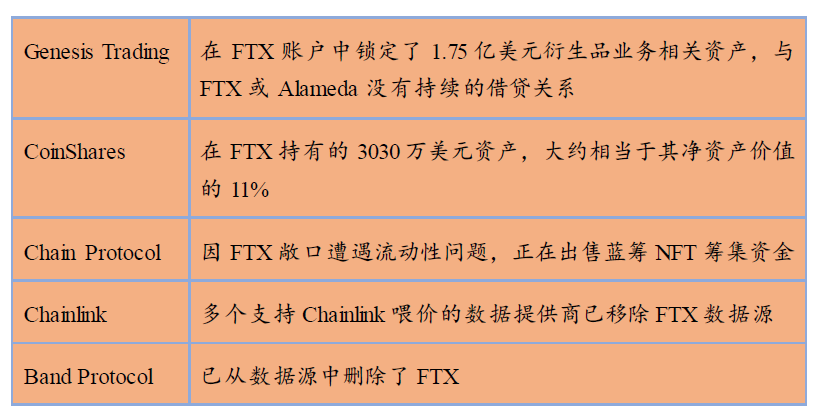

2.1.2 Joint Risks Between Institutions and Projects

secondary title

2.2 Market judgment and investment strategy

After the US CPI data for October was released, the market immediately rebounded strongly. As the US inflation shows signs of slowing down, the market expects the Fed’s monetary policy will also improve marginally, and the federal funds rate may peak in the first quarter of next year, when the market will see an inflection point of liquidity. So from a macroeconomic point of view, the bottom will not be too far away.

Let's combine several indicators to see if this is the bottom of the bear market in the cryptocurrency market, and give some investment strategies.

BTC MVRV Z-Score

The MVRV indicator is the ratio of Bitcoin's Market Value to Realized Value. RV rarely declines and is generally considered to have a strong supporting role. A larger MVRV value indicates that the current price of Bitcoin is overvalued, and the probability of price decline is higher; a lower value indicates that its price is undervalued, and the probability of price increase is higher. Compared with MVRV, MVRV Z-Score is flatter and can better reflect changes in long-term trends.

As shown in the figure below, Z-Score is a very practical indicator, which has the dual value of finding the top and finding the bottom. Whenever it reaches a negative value, it enters the green area in the graph, which is generally a periodic bottom. This round of bear market is different from the previous ones. MV and RV have been glued together since June, and Z-Score has been oscillating sideways. Until recently, affected by the FTX incident, there was a trend of digging down. This is a very valuable signal that the lowest point of the bottom has appeared, or is approaching.

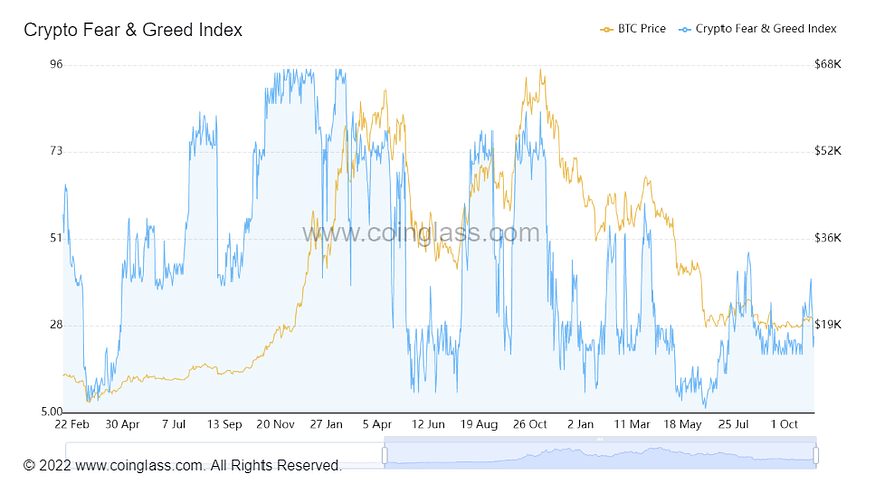

Greed and Fear Index FGI

The investment market is a game played by people, and human greed and fear are the influencing factors that can never be shaken off. The figure below shows the relationship between FGI and BTC prices in the past two years. Two conclusions can be drawn from the figure. First, the phased bottom is often accompanied by a sharp drop in FGI to around 10. Second, FGI bottoms tend to precede or synchronize with price bottoms rather than lag behind them.

Even though the FTX incident triggered market panic, the recent FGIs are above 20, which shows that the market sentiment is relatively stable. And due to rising expectations of easing inflation in the United States, market sentiment is unlikely to drop sharply in the short term. If there are not a large number of institutional thunderstorms in the later period, it can be judged that the bottom may be nearby.

The above are all personal judgments on the market, and judgments may be wrong. In particular, the FTX incident has a wider impact, and it is not ruled out that there will be thunderstorms by institutions in the future and the possibility that the market will continue to drop. So it is more important to develop a strategy that suits you.

Aggressive strategy: If you start to make regular investment before, you will continue to make regular investment. If the decline increases, the fixed investment amount also increases. If the position is still low, you can build a position at this time. According to market conditions, you can do more mainstream currencies under the premise of controlling risks.

Safe strategy: start building/adding positions after the following two conditions are met at the same time. First, Z-Score has formed an upward trend in the green area; second, the price of BTC has not hit a new low for 7 or 15 consecutive days. Set aside at least 20% cash to cover possible unexpected dips in the future. Temporarily do not do contract transactions.

In addition, the platform tokens of most exchanges have fallen by more than 10% during this crisis, but according to the above asset flow and the announced reserves, there may be wrong killings. A more aggressive strategy can invest in platform tokens that are undervalued.

4. The information, opinions and speculations contained in this report only reflect the judgment of the researchers on the date of finalizing this report. In the future, based on industry changes and updates of data information, there is a possibility of updating opinions and judgments.

About Huobi Research

Huobi Blockchain Application Research Institute (referred to as "Huobi Research Institute") was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain, with a view to pan-blockchain As the research object, the research objectives are to accelerate the research and development of blockchain technology, promote the application of blockchain industry, and promote the ecological optimization of blockchain industry. The main research contents include industry trends, technical paths, application innovation, Pattern Exploration, etc. In line with the principles of public welfare, rigor, and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms, and build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical foundation and trend judgment to promote the healthy and sustainable development of the entire blockchain industry.

contact us:

Consulting email: research@huobi.com

Official website:https://research.huobi.com/

Twitter: Huobi_Research

https://twitter.com/Huobi_Research

Medium: Huobi Research

https://medium.com/huobi-research

Telegram: Huobi Research

https://t.me/HuobiResearchOfficial

disclaimer

1. Huobi Blockchain Research Institute does not have any relationship with the projects or other third parties involved in this report that may affect the objectivity, independence, and impartiality of the report.

2. The materials and data cited in this report are all from compliant channels. The sources of the materials and data are considered reliable by Huobi Blockchain Research Institute, and necessary verifications have been carried out for their authenticity, accuracy and completeness , but Huobi Blockchain Research Institute does not make any guarantees about its authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the conclusions and opinions in the report do not constitute any investment advice on relevant digital assets. Huobi Blockchain Research Institute shall not be liable for any losses arising from the use of the contents of this report, unless expressly stipulated by laws and regulations. Readers should not make investment decisions solely based on this report, nor should they lose the ability to make independent judgments based on this report.

4. The information, opinions and speculations contained in this report only reflect the judgment of the researchers on the date of finalizing this report. In the future, based on industry changes and updates of data information, there is a possibility of updating opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you want to quote the content of this report, please indicate the source. Please let me know in advance if you need to quote a lot, and use it within the scope of permission. Under no circumstances shall any quotation, abridgement and modification contrary to the original intention be made to this report.