Explain the risk situation of stable currency in detail: Will USDT really crash?

Author: Matt Ranger

Original compilation: Block uniocrn

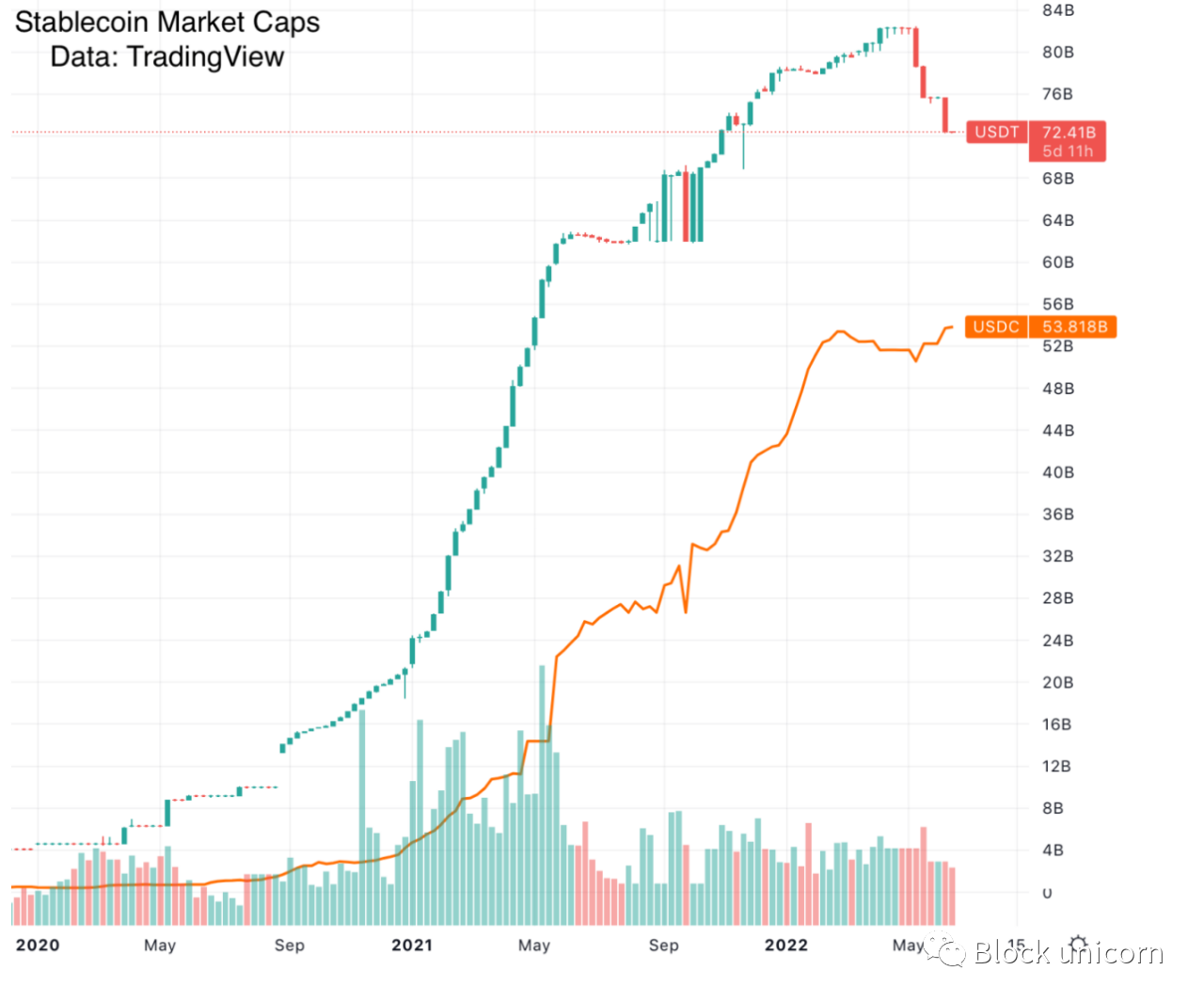

At the time of writing, the price of Bitcoin is around $22,000, and the total market capitalization of the cryptocurrency ecosystem is around $950B (95 billion). The dollar-backed stablecoin currently accounts for 16% of the total cryptocurrency market capitalization.

Cryptocurrency market cap is a ridiculous number backed by shared fiction. However, the market capitalization of stablecoins is not. No matter what happens in the crypto mania cycle, a dollar is a dollar.

The last time the total market capitalization of cryptocurrencies was $1T (one trillion) was in December 2020. Stablecoins account for about 2% of the market. Compared to 2020, the cryptocurrency market is now in a precarious position - 16% of the market is still waiting to be unleveraged.

So today, we will discuss the risks of USD-backed stablecoins, specifically USD Coin (USDC) and Tether USD (USDT).

first level title

USDC

USD Coin is the growth type of the two stablecoins, and it provides a programmable API to deposit and redeem USDC for USDC. This is frictionless compared to USDT, which has a redemption mechanism that Sam Bankman-Fried described as "chaotic."

USDC has grown tremendously since early 2021 due to its ease of use and lack of apparent fraud:

first level title

USDC is rich

secondary title

how do we know

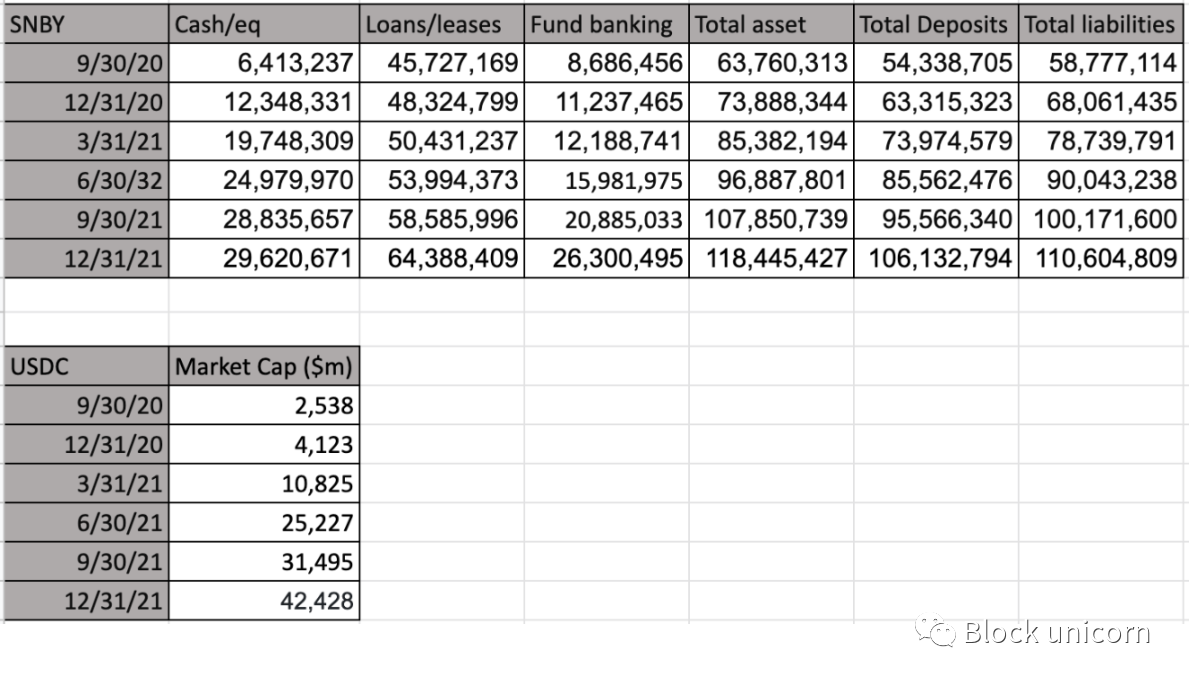

First, as pointed out in a previous post, USDC had an audit in December 2020 which confirmed they had $4 billion in coins. USDC has grown by $50 billion since then, but we can track the money.

USDC is primarily banked in two places: Silvergate Bank (SI) and Signature Bank of New York (SBNY). These are the only two U.S. banks that offer 24/7 API transactions to cryptocurrency companies, a requirement to operate similar to USDC. In a sense, USDC is a middleman between Signature and Silvergate banking services on the one hand, and blockchain transactions on the other.

Because SI and SBNY are public companies, we can track their quarterly balance sheets in their respective SEC filings (SI, SBNY). $50 billion is a lot of money, even for a bank, so we can track balance sheet changes as USDC grows. Correlating USDC to the balance sheet, we see that the majority of USDC is in SBNY Bank during the 2021 growth period:

first level title

bank run risk

There's a nuance to saying things like "I'm rich" when we're talking $50 billion. Who holds that money for you? How quickly can you get it if you want to transfer money?

The main problem with USDC is that USDC is primarily at the SBNY bank, and a large portion of SBNY's debt is dedicated to USDC.

Note that in the balance sheet above, SBNY is behaving like a normal bank: they have lent out a lot of this money!

Under normal circumstances, this isn't a problem: Individual depositors at banks are insured by the Federal Deposit Insurance Corporation (FDIC) to protect against bank runs. But in the USDC setup, there is only one individual depositor (USDC), and all their depositors have a claim on USDC, not SBNY Bank. This is a problem - if the banks run on USDC, USDC promises immediate redemption. But those redemptions immediately became a bank run on SBNY, who had most of the money lent out!

In the event of a USDC->SBNY bank run spreading, individual holders of USDC may not be eligible for FDIC's "pass-through insurance". So while USDC is largely doing it right, it still faces a significant risk of bank runs compared to traditional banks.

first level title

USDT

secondary title

Tether Ponzi

Despite my Ponzi hypothesis last year, USDT is only part of the Ponzi scheme.

secondary title

Stop caring what Tether's reserves are

A common trap that investigative journalists fall into is offering any credence to Tether’s claimed composition of reserves. For example, Patrick McKenzie analyzed Tether's reserves and found that they will be insolvent in May 2022, as their cryptocurrency holdings will lose more than their excess holdings of $160 million.

The problem here is that the $160 million in excess assets is entirely fictional. Tether announced that as its reserve size grew from $10 billion to $84 billion, the excess asset size over two years was exactly $162 million, which you can verify by visiting the web archive of tether's automated transparency pages.

Again, tether's certification is red herring. As far as I and other journalists know, the audit firm has only one relevant professional accountant.

This David J. Walker is apparently the only CPA in the world who is willing to sign a certificate for Tether. It is well documented that despite the apparent simplicity of the balance sheet, no company audits tether.

So when tethers claim they have tens of billions of dollars in commercial paper, trying to figure out what they are is like a red herring.

bankruptcy

bankruptcy

In order to find the truth about Tether, you need to look at it from another angle and see where USDT came from. The best news on this subject is Protos' Tether Papers, which breaks down where all the newly minted USDT goes.

Taking a closer look, Tether is highly likely to be insolvent, here are some of the ways it can lose money:

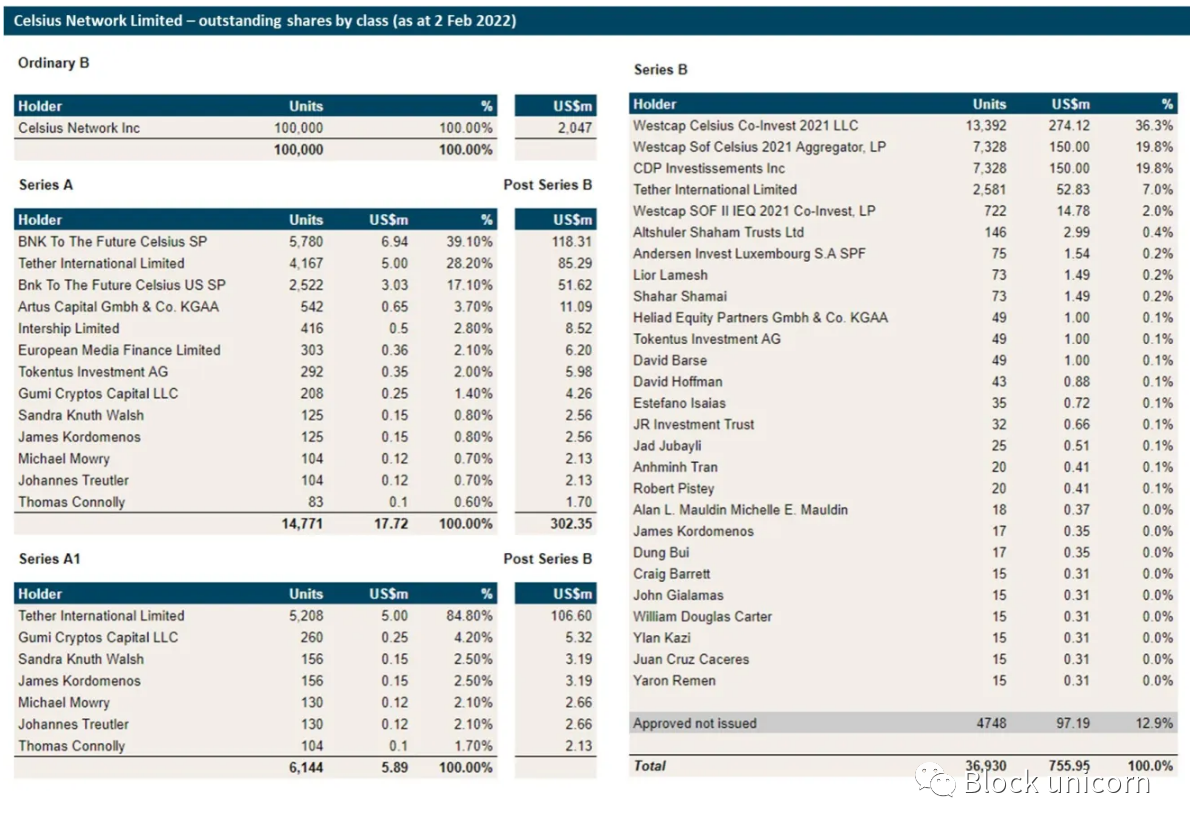

Tether is known to issue $1 billion in exchange for Bitcoin-collateralized loans from Celsius.

Note that this is specifically the "Tether Ponzi scheme" argument at play. BTC mortgages new USDT to buy new BTC, rises, washes, repeats. But also note that the Tether Ponzi scheme is likely only in the "Funds and other companies" section of the USDT issuance, so the Tether Ponzi scheme argument is at best partially true.

Of course, tether also invested $190 million in Celsius (source @intel_jackal):

Celsius is currently struggling financially, so I don't value equity on a cost basis, nor do I value loans at face value. Given that the loan was secured by BTC, which was twice as expensive at the time, Tether was in dire straits in the deal anyway.

But you don't have to believe me, you should never believe something until Tether explicitly denies it.

As Patrick McKenzie pointed out, tether itself claims to hold cryptocurrencies as reserves. These assets depreciated more than they claimed to be excess assets. Take tethers at their word - this is the best way tethers think they can present themselves, and even then they'll go broke.

It's hard to believe they hold dollar reserves. Deltec Bank from the Bahamas, the only bank with USD accounts, barely holds enough assets (overseas or local) to explain tether asset growth in 2020-2022. Tether’s data is at odds with a statistical report from the Central Bank of the Bahamas, which states that Deltec is Tether’s main bank.

If Tether held reserves denominated in a currency other than USD, possibly RMB, they would suffer exchange losses on USD-denominated debt during 2020-2022 and thus go bankrupt.

first level title

Insolvent Doesn't Mean Bankruptcy

Bankruptcy doesn't matter as long as you can continue to pay creditors. Hypothetically, the company lost $1 billion in reserves because they had to bail out their sister cryptocurrency exchange who was scammed by money launderers. It doesn't really matter unless the money is really needed to pay someone's salary, which may be years away.

QuadrigaCX, for example, had liabilities nine times assets for more than a year before its collapse. By the time Madoff's Ponzi scheme collapsed, his assets were $17 billion and his liabilities were $65 billion, a situation he had maintained for more than a decade.

first level title

Tether (probably) has a lot of money

We know USDC has money. We also know that nearly half of USDT is minted by two algorithmic trading firms, Alameda Research and Cumberland Global. Alameda also made a lot of USDC in particular, as we can see here:

Since Alameda and Cumberland are clearly capable of paying for the new USDC, we have to assume that it is possible for Tether to get a lot of real money from USDT Alameda and Cumberland.

first level title

Tether appears to be offering customers redemption services through bitfinex customer funds

The people who run tether and bitfinex are apparently happy to treat all assets they control as a slush fund. They have used tether funds in the past to cover bitfinex losses.

So it’s no surprise to learn that tether uses bitfinex funds for redemption services. Note that bitfinex is a large portion of the USDT redemption. That’s because many USDT redemption services use bitfinex as the last point of contact — something Alameda himself admits.

Recently, many wallet addresses like this exchanged hundreds of millions of USDT to bitfinex. Every few days bitfinex sends these data back to the tether vault, taking them out of the market.

As far as we knew at the time, Tether redemptions were considered bitfinex withdrawals: either bitfinex customer funds were used to service USDT redemptions, or redeemers received “merchant credit” in exchange for their USDT.

If you keep an eye on Tether redemptions, you should check out the Bitfinex Tron and ETH wallets and Tether treasury addresses (Tron, ETH).

first level title

Liquidate Stablecoins

As the total market capitalization of crypto falls, the market capitalization of stablecoins will have to decrease. In the crypto bubble of 2020-2022, stablecoins will be used mainly for two reasons:

1. Market liquidity. As we saw in our article on market manipulation, USDT is the denominator of most crypto transactions. As market size and trading volumes decrease, there is less need for large stablecoin liquidity pools and thus fewer stablecoins.

2. Systemic leverage. This is the basic scheme we see in DeFi, crypto P̶o̶n̶z̶i̶̶s̶c̶h̶e̶m̶e̶s̶ (Ponzi scheme) “lending schemes” such as Celsius, BlockFi and other high-yield products.

The gist of it is that you mint a stablecoin, lend it out to people looking to trade on margin. Because the entire cryptocurrency ecosystem is really just a casino of interconnected poker tables, the only thing a margin loan has to do is "trade with it."

More often than not, this is complicated. If Celsius pays 18% for the USDT lent, but AAVE charges 8% for borrowing, why don't you leverage more on this trade? Traders think they are playing a dodgy arbitrage game when in reality they are moving stable assets from a pile of Defi dynamite into the bonfire of a Ponzi scheme.

This is why the best metric to look for when hunting for fraud is a ridiculous risk reward (Sharpe) ratio. If you invest in a market index, you might get a 5% return. But that comes with volatility that prevents you from using too much leverage. Occasionally, the index will lose 50-70% of its value in a decline. If your leverage exceeds 2-3 times, you will be eliminated.

Funds like Madoff's Ponzi scheme not only promised a 15% return, but also risk-free. The Madoff-Ponzi regression plot is a straight line, sloping 45 degrees upward and to the right. This means you can use 10x or 40x leverage and get a return of 150% or 600%.

Of course, when a Ponzi scheme collapses, you are devastated, but the same is true if you don't use leverage.

As cryptocurrency prices fall, the effective demand for both uses of stablecoins decreases.

How will this end?

In short, when Tethers cannot be redeemed, the music stops. We probably need to see $20 billion in redemptions, or $50 billion, before that happens.

I used to think that USDC would be mostly redeemed before Tether, because USDC is easier to redeem and more secure. If you need to liquidate a stablecoin, why do it in a messy way that will anger the dragon of doom?

On the contrary, before and after the collapse of the LUNA-UST stablecoin system in May 2022, the DeFi lending agreement seems to exert pressure on USDT to anchor the US dollar.