Saylor's Dubai Speech (Full Text): Why Bitcoin Will Become the Underlying Asset of Global Digital Capital

- 核心观点:比特币正演变为全球数字经济的基础资本。

- 关键要素:

- 美国政策转向,高层全面支持比特币。

- 传统银行及机构大规模接纳并开展比特币业务。

- 数字信贷工具(如STRC)提供高收益,重塑信贷市场。

- 市场影响:将推动传统金融体系向数字化加速转型。

- 时效性标注:长期影响

This article is from Binance Blockchain Week.

Compiled by Odaily Planet Daily ( @OdailyChina ); Translated by Ethan ( @ethanzhang_web3)

At Binance Blockchain Week on December 4, Michael Saylor, in his presentation titled "Why Bitcoin Is Still the Ultimate Asset: The Next Chapter for Bitcoin," reiterated his core predictions for Bitcoin over the next decade: Bitcoin is transitioning from an investment to the "foundational capital" of the global digital economy, and the rise of the digital credit system will reshape the traditional $300 trillion credit market.

From policy shifts and changing bank attitudes to the institutionalization of ETFs and the explosive growth of digital credit instruments, Saylor depicts a new financial order that is rapidly approaching: digital capital provides the energy, digital credit provides the structure, and Bitcoin will become the underlying asset supporting all of this.

The following is a summary of the key points of the speech compiled by Odaily Planet Daily. Enjoy!

Michael Saylor: Thank you for the invitation. Whether it's an honor or anticipation, this is indeed my first time attending Binance Blockchain Week. The atmosphere here has impressed me and excited me greatly. I noticed the yellow elements everywhere; it seems today belongs to the world of orange and yellow, and thanks to the organizers for making "Bitcoin Orange" stand out so prominently.

I'd like to start with what I consider to be the most exciting change of the past year: the rapid global embrace of digital capital, digital currency, digital finance, and digital lending. Binance plays a significant role in this process, and many of you here are among the driving forces behind it. I'll then share some trends I've observed, starting with a very direct phenomenon.

By the way, there was supposed to be a countdown timer, but it seems to be malfunctioning. It currently shows I have 12 hours and 40 minutes left to speak. If I really had that much time, I could probably talk for the whole thing, but let's get back to the main topic.

Macro Shift: From "Bitcoin President" to Full Wall Street Adoption

Capital markets are undergoing a structural reshaping. This transformation is impacting global currency markets and is also spreading to stock, credit, and derivatives markets. The core driving force behind these changes is largely the rise of Bitcoin and its acceptance by the global financial system. Bitcoin is becoming a new form of digital capital.

Why do we say this? Because US President Donald Trump has publicly positioned himself as the "Bitcoin President." He hopes to make the US the global crypto capital and establish leadership in areas such as digital assets, digital capital, digital finance, and digital intelligence. This is not just a campaign slogan. His cabinet lineup reveals this direction: Vice President, Treasury Secretary Scott Bessent, and SEC Chairman Paul Atkins are all explicit supporters of digital assets. This support extends beyond the financial regulatory system to other departments, including Tulsi Gabbard, Kelly Loeffler, Robert F. Kennedy, and even key officials in the intelligence and business systems.

In other words, Bitcoin, as an asset class, has received unprecedented endorsement from the highest levels of the US federal government. This is a major turning point, and all of this has happened in just 12 months.

US Treasury Secretary Scott Bessent is discussing Dogecoin, taxes, and the Federal Reserve. (Odaily Planet Daily note: Image source: Bloomberg)

For Bitcoin to truly become digital capital, the second key condition is full acceptance by the global banking system. Just a year ago, traditional financial institutions remained highly hostile to the crypto industry. Even in the early stages of the US government transition, the market remained skeptical about whether regulators would truly fulfill the promises of Trump's team.

However, this has proven to be true. Over the past year, the Treasury, OCC, FDIC, and the Federal Reserve have issued statements and joint guidance, the core message of which can be summarized in one sentence: cryptocurrencies are acceptable assets; Bitcoin is a high-quality asset; banks can conduct crypto business, use Bitcoin as collateral, and provide custody services. The previous administration's punitive approach to banks involved in crypto business has been completely reversed.

This is a 180-degree policy shift. Banks are typically among the most conservative, bureaucratic, and risk-averse institutions globally, and even when high-level positions change, implementation at the operational level often takes years. However, the changes over the past 12 months have far exceeded expectations. ( Odaily Planet Daily note: The content has been structured for easier reading .)

- Institutional investors have entered the fray: BNY Mellon, PNC Bank, Citi, JP Morgan, Wells Fargo, Bank of America, Vanguard, and other institutions have shifted from skepticism to support.

- Service rollout: Schwab announced it will offer Bitcoin custody and lending services, and Citi is also pushing forward with similar businesses.

Previously, I couldn't obtain Bitcoin-backed loans from any mainstream bank, but now, eight of the top ten banks in the US are involved in crypto lending projects, and almost all of these transitions have been completed within the last six months. Wall Street has accepted Bitcoin as collateral and a form of capital.

Looking back, we were the first publicly traded company to include Bitcoin on our balance sheet. At that time, we were the only one; later, it grew to a dozen, then twenty or thirty, then sixty—and today, the number far exceeds what we imagined back then. The first Bitcoin ETFs weren't approved until January 2024, and now there are 85 BTC ETFs globally, with BlackRock's IBIT becoming the fastest-growing ETF in history. Bitcoin has completely ignited the fund industry and has been adopted by hundreds of publicly traded companies. In the past year, this ecosystem has gone from being a "very small minority" to "massive," a growth curve that is extremely rare.

Bitcoin is the economic, moral, and technological cornerstone of today's financial system. There are several reasons for this ( Odaily Planet Daily note: The content has been structured for easier reading ):

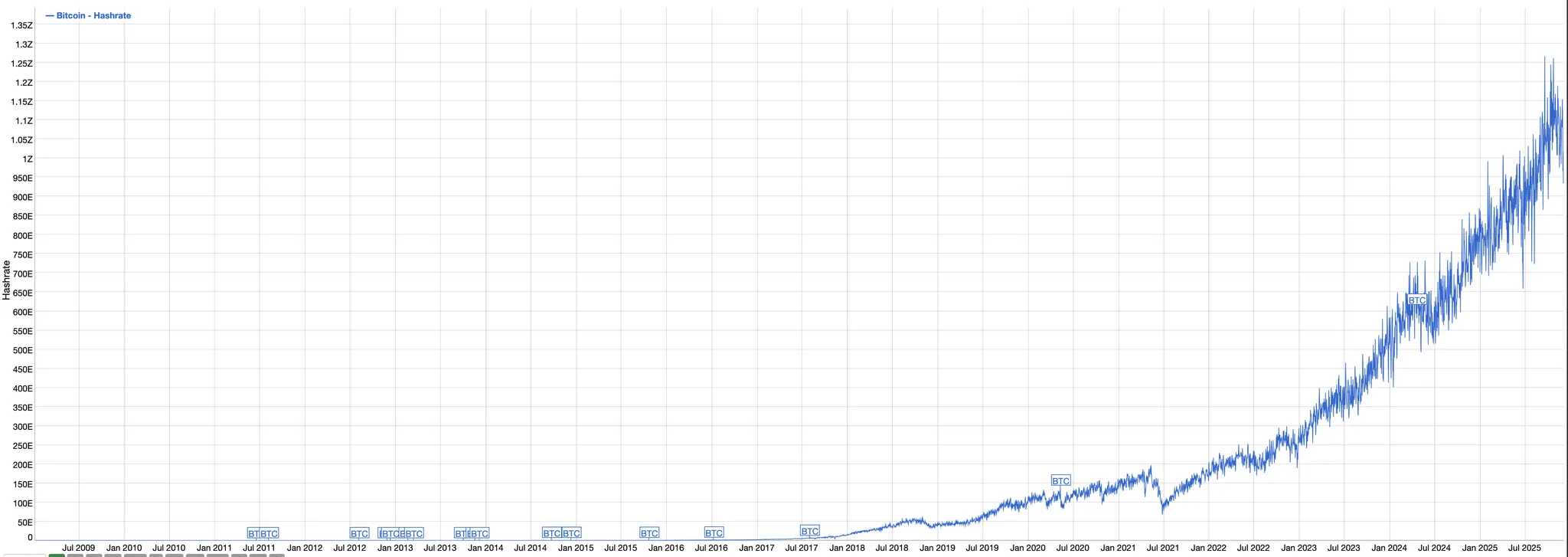

- Energy-wise: Bitcoin operates at a computing power consumption of approximately 24 gigawatts, equivalent to 24 full-power nuclear reactors, which is more energy-intensive than powering the entire U.S. Navy.

- In terms of computing power: the global network has a computing power of over 1,000 EH/s, which is more powerful than the combined computing power of all Microsoft and Google data centers.

- On the infrastructure front: Thousands of exchanges worldwide allow anyone to trade, hold, or transfer Bitcoin anytime, anywhere.

- Political influence: Hundreds of millions of crypto users worldwide and 30% of registered voters in the United States support cryptocurrencies.

- Real capital: More than one trillion dollars is being injected into the Bitcoin network.

Our company has invested approximately $48 billion, accumulating 3.1% of the circulating Bitcoin. You can extrapolate from this how much real capital is flowing into this network. Therefore, the first important conclusion is: we now possess "digital capital," a completely new store of value. And this is just the beginning. It will become the underlying cornerstone of the digital finance and digital lending industry, upon which all new financial innovations will be built.

Bitcoin hash rate history chart (Image source: bitinfocharts.com, Odaily Planet Daily note)

Strategy Decoded: A Digital Finance Department Constructing Micro-Strategies Based on "Positive Polarization"

You can reshape the insurance industry, banking, transaction models, and various capital structures. We've chosen to focus on the credit sector and are committed to becoming the first truly "digital treasury." What have we done? We've built a capital reserve system, currently holding approximately 650,000 bitcoins, the result of continuous accumulation over the past five years. In terms of reserve size, we rank fifth among S&P 500 stocks, and I believe we'll rise to second in a few years, and reach first place within four to eight years.

This stems from our "positive polarization" strategy. Traditional companies rely on the money market for capitalization, which only yields about 3% annually. When your cost of capital is 14% (the average S&P yield), using 3% of assets to support a 14% cost of capital is tantamount to continuously destroying shareholder value. However, if you use Bitcoin for capitalization, the historical annual return is 47%. This means that any company that uses Bitcoin as its capital base can consistently create shareholder value.

The meaning of "positive polarization" is that companies using digital capital can continuously grow stronger, while companies relying on fiat currency or traditional currency markets become more vulnerable the larger their capital size. Traditional wisdom leads to the "decapitalization" of companies, while digital wisdom leads to their "recapitalization."

Our model is simple: raise funds at a debt cost of 6%-12% or an equity cost of 14%, and then purchase an asset that appreciates at a rate of 47%. This results in an overall return of approximately 65%.

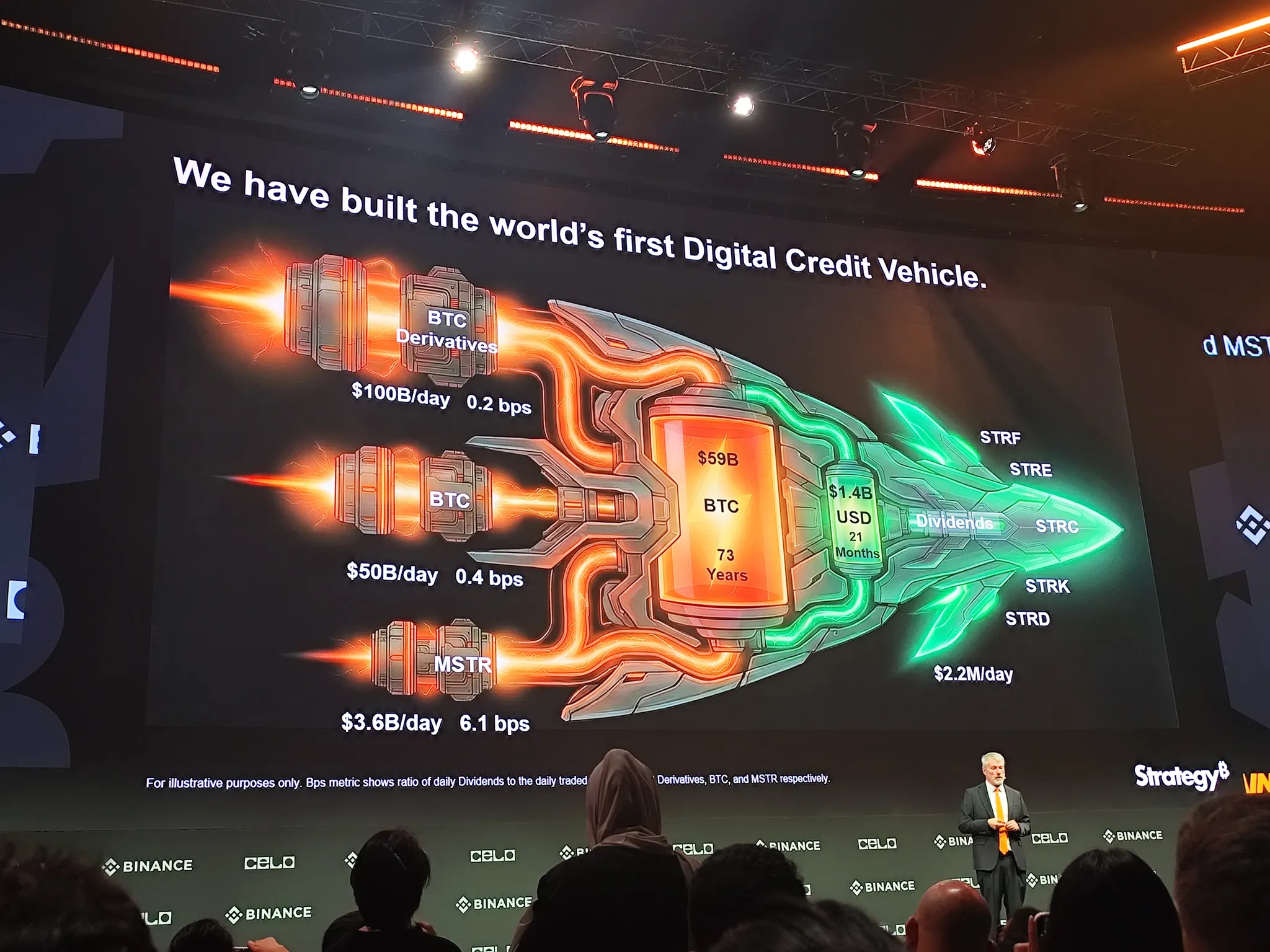

Last year we raised $22 billion, and this year another $22 billion, all flowing into the crypto economy. Funding methods include equity financing ($16 billion last year, $13 billion this year), approximately $7 billion in digital lending, and a range of public instruments and debt products such as STRF, STRK, STRD, and STRC. The company's mission is to continuously increase the "Bitcoin content per share." For long-term Bitcoin believers, they buy our stock because we increase the amount of Bitcoin per share every year; if they only want to hold the asset itself, they can choose an ETF, as the Bitcoin content per share in an ETF is fixed. Currently, our capital structure is roughly: approximately $60 billion in BTC reserves against approximately $8 billion in debt, with extremely low leverage. The reserve value is equivalent to 73 years of dividend payouts. The company pays approximately $800 million in dividends (or interest equivalents) annually.

To maintain net worth growth, Bitcoin only needs to rise at a rate of 1.36% per year to cover costs. This is our "cruising speed." In other words, we are betting on Bitcoin's long-term annualized growth exceeding 1.36%, and once that is achieved, the company and its shareholders will win.

This week, we raised another $1.44 billion in cash reserves, equivalent to our expenses for the next 21 months. This means we can continue operating reliably without selling equity, BTC, or derivatives. Even if the funding markets were completely shut down, we could "hold our breath" and survive for nearly two years. This is the "dollar battery" we've built.

To summarize the company's strategy: when the stock price is above net asset value (NAV), we sell equity to create incremental value; when the stock price is below NAV, we sell derivatives or Bitcoin to maintain value growth. The entire system is like a spaceship, revolving around a core driving force.

From Capital to Credit: Building a "Digital Bank Account" with an Annualized Return of 10%

Our ultimate goal is to create the world's best digital lending product: an account that offers users 10% interest, instead of the 4%, 3%, 2%, or lower rates offered by traditional banks. This is STRC (Digital Credit Carrier), structured around a "Bitcoin reactor" at its core, continuously charging the "dollar battery." As long as Bitcoin appreciates at an annualized rate exceeding 1.3%, the reactor can operate stably, keeping the battery charged for a long time. Even if Bitcoin doesn't appreciate at all, this system can sustain itself for up to 73 years.

Next, we will continuously fuel the entire system through the equity capital market, the BTC spot market, and the BTC derivatives market. Explaining this in detail would take a considerable amount of time, so I'll just emphasize one point here: we have published our complete credit model on our official website, updating it in real-time approximately every 15 seconds. You can insert almost any assumptions about token price or ARR volatility, and the model will simultaneously provide corresponding risk calculations.

We recently received a credit rating from S&P. Our goal is to become the first major Bitcoin holder to receive an "investment grade" rating, and the first crypto company to issue "investment grade" debt. Of course, this requires starting from the basics and building up step by step, so in the initial stages, we received a B or B- rating from S&P.

This rating was obtained before we raised that $1.4 billion in reserves. We hope the rating will gradually improve over time. But even at this stage, it has opened a significant door for us to sell credit products to specialized credit investors who must allocate "rated assets." Obtaining the rating has nearly doubled the potential market size for our credit products, which is crucial. So, what exactly are we doing with this capital?

In short, what we're doing is transforming "capital" into "credit." Imagine you have a five-year-old child. You can buy him an acre of land in New York City—that's capital. You tell him that in 10 to 30 years, the land will either be sold or refinanced, and until then, it will generate almost no cash flow—this is typical capital investment logic. Another approach is to buy him an annuity contract, promising to pay him $10,000 a month for life—that's credit. If you want him to receive a stable $10,000 a month, you choose credit; if you want him to have the opportunity to acquire a huge fortune in 30 years, you choose capital.

Bitcoin is capital. It's extremely volatile, but offers extremely high long-term returns. Many people are unwilling to bear this volatility. The underlying order of the world is driven by capital, while the world's daily operation relies on the credit system. Therefore, to transform capital into credit, we hold BTC—a form of "monetary capital"—while simultaneously converting it into US dollars, euros, or even issuing a Japanese yen-denominated version. In this process, we isolate risk through over-collateralization, compress volatility by setting par value and liquidation priority, and set the dividend yield through active management and "refining returns." You can set your target yield at 10% or other levels and adjust the duration through structural design.

For capital investors, if you ask me, "How long should I hold Bitcoin?", my answer is usually: at least 10 years. You'll become richer as a result, but during those 10 years, you might not receive any cash flow. For credit investors, we offer "instant gratification": monthly cash dividends starting next month. Both types of demand exist simultaneously in the market. In reality, most people actually need two allocations: one part of their funds for credit to generate cash flow; and the other part invested in capital assets to pursue long-term appreciation.

What we're doing is transforming digital capital into digital credit and systematizing and productizing it. We've already launched several digital credit instruments: STRK is a structured Bitcoin product that pays you interest while allowing for some appreciation, letting you share in some of the gains while you wait; if you want to further amplify your returns, STRD is a high-yield, long-term credit instrument with a current effective yield of approximately 12.9%; if you value safety margins and stable cash flow most, you'll prefer STRF, which is a super-priority credit instrument, located at the forefront of the capital structure, possessing the highest governance rights and liquidation priority.

These designs aim to provide clear choices for investors with different risk appetites: if you prioritize higher protection, the return is approximately 9%; if you're willing to forgo some protection, the return can rise to 12.9%. Those who choose the former rarely opt for the latter, and vice versa. We intentionally use two product structures to cover two completely different investor profiles. STRC is our "highest level" tool.

When designing STRC, our goal was to create a "high-yield bank account-style product": the principal would fluctuate around $100, making it very stable, while paying dividends monthly. To achieve this, the interest rate had to be able to adjust monthly. STRC is the industry's first "treasury-level" digital credit instrument, and in fact, it is the first "variable-rate preferred stock" product issued in the entire capital market history. All of this is possible because we have digital capital at our disposal; without digital capital, this structure simply cannot exist. At the same time, we also possess digital intelligence; I relied on AI to complete the design of this product.

MicroStrategy Product Matrix Diagram (Image source: live demonstration, Odaily Planet Daily note)

Without AI, it would never have existed. The reason is simple: lawyers would say, "Nobody's ever done this before," investment banks would say, "We have no precedent," and everyone would repeat, "It's never been done before, it can't be done." But I asked, "Is it really impossible?" AI's answer was, "Absolutely, it's structurally very clear; you just need to build it according to a few steps." So we used AI's deduction and verification to persuade lawyers, investment banks, and market participants, using modern technology to truly bring this product to market. I'll show some results later. As for Stream, it's our fifth product, essentially a Euro-denominated version of STRF.

If you are a euro-denominated investor who doesn't want to bear exchange rate risk and prefers that both the asset value and cash flow be settled in euros, then this is the solution designed for you. Here is the performance of STRC over the past five months since its issuance on August 1st: the issuance price was around 90, and it has now stabilized at around 97, while we have also continuously increased the dividend level. I want to use this to visually illustrate the difference between capital and credit.

Let's say you had $100 and bought $100 worth of Bitcoin on August 1st. Over the past four to five months, you would have lost about $27 and received no dividends. However, if you had bought STRC at that time, you would now have earned about $7 and received an additional $3.70 in dividends. During this period, credit investors in STRC significantly outperformed capital investors in a bear market. So, why do people still choose to buy Bitcoin? The answer lies in the time dimension: over the past five years, Bitcoin's average annualized return has been close to 50%, while STRC's steady-state return is approximately 10.75%. To achieve this kind of capital appreciation, you must endure high volatility and deep drawdowns.

Therefore, if your investment horizon is 4 to 10 years or even longer, you should hold capital assets, such as Bitcoin; if your funds will be needed in the next four months, four weeks, four days, or even four years, or if you are extremely averse to volatility, you are better suited to credit instruments. To complete the transition from "highly volatile capital" to "predictable credit," the market needs a "treasury-like company" to design and operate the middle layer: stripping volatility and risk from capital and extracting robust cash flow. This is exactly what we are doing, and we will continue to do so in greater depth.

When we launched this digital lending line in January of this year, the category started from almost nothing; in just nine months, it has grown to nearly $8 billion. Liquidity is also very high, with transaction volumes for these digital lending instruments reaching hundreds of millions or even billions of dollars on certain trading days.

Let me explain this in a more intuitive way. Most common preferred stock is traded over-the-counter (OTC), with an average daily trading volume of about 100,000 shares. Even mainstream preferred stock that has successfully gone public typically has an average daily trading volume of around $1 million. Our initial digital securities, including STRF, STRK, and STRD, far outperformed traditional products from the outset: their average daily trading volume reached $30 million, about 30 times that of traditional preferred stock.

We then found the most successful architecture solution to date: STRC. This product addressed everyone's pain points, causing its daily transaction volume to jump rapidly to $140 million, a 100-fold increase compared to traditional products. In the financial sector, the true measure of an innovation's effectiveness is not a "slight improvement," but rather an order-of-magnitude leap in performance and adoption—something STRC achieved.

A disruptive force: How the "triple tax deferral" architecture is reshaping global yields

More importantly, we inadvertently triggered a significant discovery: demand truly is the source of innovation. We noticed that if companies pay dividends to investors by raising capital (whether from equity, derivatives, or BTC), these dividends are essentially "capital returns," not taxable income. This means investors don't need to pay taxes immediately, effectively receiving a "tax deferral," with an effective tax rate approaching zero, rather than 20%, 30%, or 50%. This is a highly structurally significant finding; we've identified a way to pay investors dividends with a near-zero tax rate.

Of course, the company will continue to sell credit products and use the proceeds to buy Bitcoin, creating an accelerating effect. This leads to an important question: why does equity have value? The answer is: because we can create credit. The more credit we issue, the higher the yield on BTC from the collateralized capital, and the higher the value of the equity.

I'd like to quickly break down this logic from several dimensions.

First, the credit market itself is undergoing a revolution; it's a global market worth a staggering $300 trillion. Why is digital credit more advantageous? The key lies in its foundation on a long-term appreciating asset, Bitcoin, rather than on depreciating assets or traditional collateral such as physical warehouses, production facilities, or service contracts.

Secondly, digital lending is highly transparent, liquid, and homogeneous. Our lending model is updated every 15 seconds, and risk assessments are visible in real time. It's not as complex as packaging 10,000 mortgages into a single MBS, nor does it possess the structural heterogeneity of corporate or sovereign lending. Essentially, it's more like equity than debt. Traditional bank lending is debt, corporate lending is debt, and bank deposits are also debt to banks; these debts amplify risk for the issuing institution. Equity, however, is different. Equity never matures, doesn't force the issuer to repay principal, and only pays dividends if it doesn't affect solvency. This "permanence" means we can permanently pay dividends to investors because we permanently invest our funds in the crypto economy. Furthermore, we bring credit securities to the public market, giving them global liquidity, brand recognition, and simplified structures. STRC is such a product, directly available to investors worldwide. Digital lending allows us unprecedented scale and speed: if you give me $500 million, I can complete a matching collateralized position within a day. Imagine that the financing-construction-asset generation cycle that traditional real estate companies need to complete takes five years, but we can complete it in a day.

More importantly, this entire architecture inherently possesses the characteristic of "deferred tax payment." You'll notice that, in comparison, traditional lending only offers returns of 2%–4%, while we can offer returns of 10%–12%. We can pay higher dividends because we've innovated on the underlying capital and credit structure, stemming from the business model of the Bitcoin Treasury.

What is a Bitcoin Treasury Corporation? Our model can be summarized in three things: we sell securities to obtain capital; we issue digital credits, putting them in a state of deferred taxation; and then we pay dividends in the form of "capital returns," while the underlying capital itself also grows under the premise of deferred taxation.

This creates a "triple tax deferral" structure, which is currently the most efficient and scalable fixed-income generation model globally. Traditional energy, real estate, and consumer goods companies cannot replicate this structure; it can only be driven by digital capital.

From this perspective, we are a "digital credit factory": we permanently exchange dollar yields for credit investors while continuously generating Bitcoin capital gains for equity investors. This system is compatible with multiple currencies, including the US dollar, euro, and Japanese yen.

The final result is very clear: the "capital return" structure allows investors to obtain a higher real rate of return. For example, in the United States, banks typically offer savings accounts with an interest rate of 0.4%, and the money market offers 0.4%–4%, but all of these are subject to taxation. The STRC offers a yield of approximately 10.8%, with a tax-equivalent return of nearly 17%, four times that of the money market and twenty times that of bank rates. This difference is so large that it cannot be ignored.

The same is true in Europe: money market rates are only 1.5%, while Stream's effective yield reaches 12.5%, a pre-tax equivalent of nearly 20%; for investors in Vienna or Brussels, this is equivalent to a bank account paying 27% interest. Its effect is revolutionary.

In short, we are digitally reshaping banking, money markets, and the credit system. And it's not just STRC; every digital credit instrument outperforms its corresponding traditional credit instrument. Junk bonds (“high-yield bonds”) give you 6%, while our products offer an after-tax equivalent of 14%–20%; private credit averages 7%, and its structure is opaque; money market yields in major developed markets range from 0% to 4%, while STRC's tax-equivalent yield is 17%.

From a macro perspective, the transformation brought about by digital credit is a systemic rewriting of "how money works," "how banks operate," and "how the credit system supports the economy." The world relies on credit, but how do you leave a lifetime annuity for your children in Switzerland or Japan when banks don't offer any returns? How do you obtain a 10% return in Swiss francs or Japanese yen? The answer is digital credit. In the future, Bitcoin treasury companies like MetaPlanet will enter Japan, Switzerland, and South Korea. If we don't achieve it, local companies will. Because every country in the world has the same need: people want a "bank account that pays out 10% returns."

Finally, I want to emphasize a simple reality. If you ask 100 ordinary people, "Would you be willing to accept 40% volatility for a potential 30% or 40% annualized return?" their answers will vary. Some will be willing to take the risk, but more will choose to avoid it. But if you ask them, "Would you want an account that pays 10% annually and is in a tax-deferred state?" the answer will be almost unanimous: everyone would.

This is the significance of STRC. If you think about the next stage of the digital economy, it means that, based on the digital capital formed by Bitcoin, digital credit will permeate every market sector, repairing the banking system, restructuring the money market, and resetting the cost of capital for corporate credit, private credit, and other debt instruments.

Ultimately, the beneficiaries are investors, the digital economy itself, and Bitcoin holders and the community. The losers are the bureaucratic, outdated oligarchic institutions that take your money without giving you anything in return. The entire system is being restructured for the benefit of humanity, and you are witnessing this transformation and moving forward with us. Thank you.

Conclusion: Fluctuations are energy; don't run away from the "fire".

Q: There's a question in the community: you've explained Bitcoin's durability quite thoroughly. If you were to leave one last piece of advice for viewers around the world, why Bitcoin? And why now?

Saylor: Yes, the core message I really want to convey is that digitalization is reshaping the world, and that's undeniable. Digital intelligence will be deeply embedded in your car, the robots in your factory, your phone, and every system in your daily life. In the future, we will face an era of "billions of AIs," with self-driving cars and robots handling most of the manufacturing processes.

If you want to continue creating new things and achieving previously unimaginable goals through action, you must think digitally. Digital assets will also reshape the world; whether it's digital currency, digital equity, digital credit, digital financial instruments, or digital securities, everything is being redefined.

Regarding digitalization, there's a very simple yet often underestimated fact: almost everything can be done better through digitalization. Digital photography, digital video, digital education, and digital entertainment provide clear examples. Now, this wave of digitalization is beginning to directly impact capital markets and the banking system. My advice to you is: quickly figure out how to leverage digital technology to digitize and structure your goods, services, and products to create better returns for investors, while simultaneously better serving your citizens, your customers, and even your families.

Of course, markets fluctuate, but this logic is self-consistent. With any technological change, there will always be voices of doubt. People have questioned electricity, cars, and airplanes. For the past 50 years, people have even hesitated to accept nuclear energy. From 1973 to 2023, we almost pressed the "pause button" on nuclear energy development, but now people are recognizing that this near-infinite clean energy source may not be a bad idea. Therefore, skepticism towards new things is normal, but it doesn't bother me.

I am not afraid of volatility. On the contrary, volatility often means that it is one of the most dynamic, energetic, and useful assets in the entire capital market. It is precisely because it gathers enormous energy that prices fluctuate wildly. If you learn not to be intimidated by this volatility, you can learn to navigate it. Don't instinctively flee from the "fire," but learn how to move forward in the fire—that's the attitude I want to convey. If you find yourself unable to withstand 50% price volatility, unable to bear the ups and downs of capital, there is actually a very direct solution: turn to credit. If you are a builder, you can create credit instruments; if you are an investor, you can buy credit products. By purchasing digital credit, you can participate in the growth of the crypto economy while significantly reducing your exposure to volatility. If you don't want to participate in this way, you can also choose to become a creator of credit. And if what you crave is this "raw growth engine," then directly integrate digital capital into your country, your business, your family's asset allocation, and your product system.

I believe this is one of the most extraordinary opportunities our generation will ever have.