The success of 4D dismantling USV: history, evolution and rules of the game

old yuppie

Original source: readthegeneralist

Original compilation:old yuppie

Actionable Insights:

If you only have a few minutes, here's what investors, operators, and founders should know about Union Square Ventures (USV).

Master of Consistency.USV may be the most stable venture capital firm in the past 20 years. All of the company's vintages were reported to be top-four in the industry, with several more extraordinary performances.

Methodology-driven thinker.Founders Brad Burnham and Fred Wilson are brilliant systems thinkers. USV's partners have used this ability to develop a theory that guides their investment practice.

Self-disciplined deployer.Given its track record, USV has no shortage of suitors. The firm has maintained a conservative fund size despite the genuinely fervent interest in it from LPs. This practice is different from the general market trend.

Build a network.For a web-obsessed venture capital firm, it's fitting that USV created its own network. The firm offers a private community and a range of events for portfolio companies and their founders.

Lefty Gomez once said that he"Rather than doing good things, do things that make you lucky". Many venture capitalists likely make the same tradeoffs as this eccentric Yankees pitcher. In the grand slam business of venture capital, one major investment can make up for a series of failed investments. Participating in an early funding round from Google, Facebook, Stripe, or Coinbase can eliminate a quarter of misses. Since it is not a simple matter to select a company with great potential from a large number of entrepreneurial projects, it is easy for people to hand over the choice to the "god". Why not close your eyes and "swing"?

Some people do. In fact, so many people, this"strategy of hope"There's a name for it: cast a net and pray. On a small scale, casting a net and praying can work well. Anyone who throws some money at a venture in the "cast net" probably looks like a guru for a while. Never mind the string of failures; in venture capital, you are remembered for your successes.

This posture can make it difficult to distinguish the identity of practitioners. If you can do so well with only one investment, how do you know which investor is lucky and which business is good? How do you tell the difference between a passionate investor and a mature entrepreneur?

The only sure solution is to wait. Either investors keep "hitting" or their luck is running out. Over a long enough time frame, skill and luck can diverge.

USV is probably the most reliable investor in startup investing. Since opening in 2003, few other funds have managed such high performance over such a long period. USV's performance in the industries it invests in has always been among the top four. It also broke records for some of the best performing vintages ever. Much of that success stems from the firm's genius for thinking deeply about the future and refining a methodology for investing in opportunities. This is equivalent to VC being able to guide the entire entrepreneurial track before investing, and has made a lot of necessary preparations for their own investment.

Like every successful investor, USV has been lucky. But more importantly, it's been very, very good. Today's article will explore the company's history, evolution and rules of the game. By reading this article you can learn:

Flatiron Partners。Before starting USV, Fred Wilson co-founded Flatiron Partners with Jerry Colonna. The firm has invested in hot startups such as Geocities and The Industry Standard. Much of its portfolio collapsed during the dot-com bubble.

A difficult financing.Despite their strong backgrounds, Wilson and Brad Burnham took 18 months to raise USV's first fund. The University of Texas plays a key role in fostering institutional interest.

two years.USV's first fund was very successful, returning 14 times the invested capital. The company's 2012 performance was even better.

Dark horse company.USV is known for investing in Twitter, Zynga, Coinbase, Tumblr, and Etsy. One lesser-known investment bright spot is recruiting platform Indeed.

Be disciplined.Despite their success, USVs have remained small in funding. Its early investment return was $275 million, which is a lot of money for an investment company of this size. This self-discipline has helped USV maximize returns.

origin

origin

first level title

meet lovely people

In 1996, Fred Wilson got his chance. After spending nine years rising through the ranks at Euclid Partners, the thirty-five-year-old financier is about to helm a firm of his own.

This opportunity arose under surprising circumstances. While working at Euclid, Fred Wilson bet $250,000 on a"no future"push"push"to the consumer's desktop. Rather than visiting a web page to see the latest news, it's better to call it uninvited. Headlines appear on your home screen, indistinguishable from a TV station. The entrepreneur behind the invention is Mark Pincus, whose venture is called Freeloader. Former AOL product manager Sunil Paul serves as co-founder.

A few months after Wilson's initial investment, Euclid Partners increased their stake, deploying another $1 million investment. SoftBank Ventures also joined the round, with Charles Lax leading a $1.6 million round. Both companies are cashing in quickly, though perhaps not as richly as they first appear. Eight months after Freeloader was founded, it was sold to Individual Inc. in a mix of cash and stock at a valuation of $38 million. That price initially meant a return of more than 5x for SoftBank, and even more for Euclid, though a sharp drop in Individual Inc.'s stock price shortened the return.

Wilson impressed SoftBank's team. After the Freeloader deal closed, Lax proposed that he join the firm as an investment partner. While SoftBank was taking a very different tack at the time, it was ironic that one of the most disciplined investors in venture capital might end up in a company known for its big spenders.

Wilson feels it's time for a new chapter, but he's not sure SoftBank is the right next step. As he considered this option, another option came up.

Wilson met Jerry Colonna a few months ago through the Freeloader deal. Colonna's employer, CMG @Ventures (@Ventures), is considering investing. When Wilson arrived at Colonna's office, he was surprised to find his counterpart wearing a worn Yankee T-shirt and ripped jeans. Wilson reportedly thought at the time:"Well, it's really an internet guy". Despite their differences in appearance, the two quickly developed a good relationship.

Colonna seemed to inspire an affinity for everyone he met. While @Ventures declined to invest in Freeloader, Pincus counts Colonna as a confidant and advisor. So when Pincus learned that Wilson was considering a new position, he felt compelled to call Colonna and share the news. Pincus thinks his first disciple and close advocate would make a great team.

Turns out, Colonna didn't even need another meeting to be persuaded. When Wilson canceled their breakfast, remembering that it was his daughter's kindergarten graduation, Colonna realized the outgoing Euclid partner shared his values. When they finally met, Wilson agreed.

Instead of rejecting SoftBank outright, Wilson countered: What if SoftBank had invested in his and Colonna's latest fund instead of hiring him? Flatiron Partners will focus on the emerging New York City tech ecosystem, giving SoftBank an informal presence in a potentially important new market.

first level title

Partner at Flatiron

Wilson and Colonna's new endeavors coincided with the inflation of the dot-com bubble. As technology has grown in the public consciousness, Flatiron has attracted attention. In a closely watched report, New York magazine named the firm's partners as"prince of new york"。

Flatiron's early performance proves that title to be true. Indeed, the firm's partners proved to be a potent duo, with Wilson's high energy and analytical skills paired with Colonna's powerful charisma. Wilson said:"He's the guy that entrepreneurs always talk to, and entrepreneurs always say bring Jerry to meetings and investors will love us."These capabilities propelled Flatiron to select several early Internet winners, including Geocities, Mercado Libre, The Industry Standard, Kozmo.com, TheStreet.com, and Yoyodyne (run by a green entrepreneur named Seth Godin).

Geocities, in particular, looked like a landmark win. In 1996, Flatiron led an $8 million Series B round for the web directory project and a Series C round the following year. The first of those two investments was helped by young Brooklyn native Jason Calacanis, who Colonna had been interested in. Calacanis drafted the company’s memo that helped convince SoftBank and Chase to invest alongside Flatiron.

In 1999, Yahoo bought Geocities for $3.7 billion, an all-stock deal. That looks like a good result that will return Flatiron's fund, perhaps many times over. In fact, Flatiron has never realized such a large gain on a Geocities deal.

In 2000, the dot-com bubble burst, crippling the tech world and crippling Flatiron's portfolio. Once-proud companies like The Industry Standard and Kozmo.com went out of business. Yahoo, which traded at a high price of $118.75 per share in January 2000, fell to $9 by September of the following year, hit by post-September 11 instability. By then, Flatiron had closed its doors and JPMorgan absorbed the entity.

Wilson later said:"We made a fortune and lost it in the blink of an eye"first level title

Brad and Fred

Following the closure of Flatiron, Colonna left the venture capital industry to begin his reinvention journey as a founder coach. Today, he is one of the most sought-after advisors in the tech world. His business, Reboot, has established itself as an authority on leadership development.

When Colonna discovered his mission lay outside venture capital, Wilson's mission had to be built through perseverance. After the collapse of Flatiron, he spent two years"Licking his wounds and internalizing the lessons he's learned". While there is no fund to manage, Wilson has maintained his focus on the hard-hit risk sector through angel investing. A major opportunity to reconnect with an old relationship - Brad Burnham.

Wilson met Burnham a few years ago from his investment in financial information company Multex. While working at Euclid Partners, Wilson attended lectures by ADP's Isaak Karaev. Karaev joined the compensation program giant in an entrepreneur-in-residence role after ADP acquired his startup. During Karaev's presentation, it was revealed that he was working on some new work. Wilson approached Karaev to fund his next venture, and soon became one of Multex's first investors. Euclid was also joined by AT&T Ventures, with Burnham representing the telecommunications company.

At that point, Burnham had been with AT&T for 14 years, with only one brief hiatus. In 1989, Burnham spun out a startup called Echo Logic from AT&T. The company's product is translation software that enables applications to be used on different computers. While AT&T is Echo Logic's sole investor and major shareholder, Burnham made sure he and his team had minority rights. The process of granting those protections was so daunting for AT&T Chief Financial Officer Bob Kavner that he created a separate venture fund to manage future incubations and invest in outside ventures. After Echo Logic ceased operating independently in 1993, Burnham joined AT&T Ventures, where he was promoted to general partner. The company has returned the sovereignty granted by its parent company with a stellar performance: From its founding to 1999, AT&T Ventures turned $350 million in seed capital into $1.2 billion. (Like Flatiron Partners, the firm suffered a brutal reversal during the dot-com bubble).

Multex's lively board meeting gave Wilson and Burnham a chance to get to know each other and exchange views on the future of the Internet. Those conversations would convince Karaev and the team to turn Multex into a primarily web-based business. In March 1999, Multex was listed on the public market at a valuation of $750 million. The company survived the dot-com bubble and was eventually sold to Reuters for $250 million.

While Multex may have introduced Wilson and Burnham, it was Tacoda that spurred their partnership. After leaving AT&T Ventures, Burnham helped entrepreneur Dave Morgan with his latest endeavor. The two met years ago when Morgan did an "elevator time" pitch at a Dallas hotel. Morgan said: "On the 14th floor, I interested him enough to have more conversations with him in the lobby. After that start-up, Real Media, merged with PubliGroupe, Morgan sought a second act. He returned to online advertising and started Tacoda with Burnham's advice.

Morgan's only problem is the small one of money. Like Flatiron, many venture capital firms went out of business during the crash. Those that survive are saving money because they know LPs are short on cash. Morgan says:"In 2001, no venture firm would invest in ad tech"。

Without institutional capital, Morgan and Burnham found angel investors in New York City, including Fred Wilson. Intrigued by Morgan's proposal, Wilson assembled a syndicate of venture capitalists willing to invest their own money. Venture capital legend Howard Morgan invested alongside longtime friend Jerry Colonna, Allen's Nancy Peretsman, and famed angel investor Jerry Rosenkranz.

Over the course of the investment, Wilson and Burnham grew closer and remained in touch over the ensuing months. The rotisserie is often the site of long-running discussions about the flaws and future of the venture capital industry. By early 2003, both were secretly asking Dave Morgan for his opinion on a potential partnership.

Morgan says:"It's kind of like dating in high school. each of them wants to talk about the other alone". For Morgan, it was an obvious fit. I told them you'd smash it.

first level title

Union Square Ventures

Despite Burnham and Wilson's credentials, raising new funds won't be easy. It took them 18 months to secure $125 million in funding for Union Square Ventures in 2004. Attracting the first $20 million in funding was particularly difficult, according to a person familiar with the early days. Dave Morgan said of that period:"There is no money everywhere in the market"。

Winning the backing of the University of Texas Investment Management Corporation (UTIMCO) proved to be a turning point. Senior investment officer Lindel Eakman committed to the fund and sparked a lot of interest from other LPs. Ultimately, about two dozen institutions joined USV’s first fund, according to one source. All will thank their lucky stars today.

Fittingly, one of USV's first investments was in Dave Morgan and Tacoda. A few years later, the company was sold to AOL for $275 million, giving the company a huge windfall. Though they didn't know it at the time, Burnham and Wilson nearly returned the fund with USV's first check.

A familiar face helms another early-stage portfolio company. After directing the acquisition of Multex in 2003, Isaak Karaev started another business, Instant Information. The company will also be acquired (absorbed by EPAM in 2010).

first level title

achievement

first level title

consistency

An institutional investor who has been in venture capital funds for a long time shared their views on USV. While their firms did not back Wilson and Burnham's funds, they were filled with admiration. they said:"It's a perfect VC firm for my taste"。

This review was inspired by the USV's reliability, which stands above all else. The veteran investor said:"Consistency is the hardest thing. Each of USV's funds returns far above the industry average."According to this person, all of USV's funds have returned at least 5x. some funds return"greatly exceeded this figure". To the best of this investor's knowledge, there is no other fund quite like USV (except perhaps Sequoia that has produced such reliably exceptional returns). The Information previously reported that USV’s fund returns in 2004, 2012, 2014 and 2016 were among the top four in the industry. In total, USV has raised 8 early-stage funds and 4 late-stage opportunity funds. (Presumably the fivefold return is reserved for vintages that have had a certain amount of time to mature).

first level title

2004 vintage

USV's first fund proved to be one of the greatest in venture history. According to reports, as of 2018, the company's return on total invested capital in 2004 was about 14 times. This performance was driven by a portfolio that includes Zynga, Twitter, Tumblr, Indeed and Etsy.

According to Fred Wilson, Zynga is the first USV"high exit"project. The social gaming company, founded by Mark Pincus, who brought Wilson and Colonna together, was a breakout success. Former USV analyst and current Spero Ventures GP Andrew Parker said:"I don't think anyone has ever seen a company's revenue grow so rapidly. it's really amazing". Zynga went public at a $7 billion valuation, delivering a 65x return for USV.

Twitter remains the most notable of the bunch. According to Burnham, there was little competition for the deal. Part of it is a quirk of Twitter's founder. Jack Dorsey, Ev Williams, Noah Glass and Biz Stone are not traditionally strong entrepreneurs. A source pointed out"You'd never say Twitter is a great team. USV's willingness to invest reveals something profound about the company: Ideas matter more than founders. If a concept is compelling enough, Burnham and Wilson are willing to overlook potential character flaws or "rough edges." Some sources point to the founders of Tumblr and Etsy as other examples. One investor noted:"VC firms in New York usually don't invest in these guys"。

The market's silence is good for USV. The fund led a $5 million Series A funding round, taking a roughly 33 percent stake in the process. Twitter later IPO'd at a $14.2 billion valuation.

If Twitter is the fund's most famous investment, Indeed is the least appreciated. According to reports, Burnham knew founders Rony Kahan and Paul Forster before starting USV, and made it one of the company's first investments. Like Twitter, the job platform represents a clear example of a business with network effects -- a key investment case for USVs in this day and age. Indeed had only raised a single round of funding of $5 million before acquiring it for $1 billion.

Etsy is a notable case (for how it returns and why). The investment was provided by Albert Wenger, an operator who will be a big part of the USV story. Wenger had known Burnham for several years when he joined USV's portfolio company Delicious. The social bookmarking startup was in the same building as its financial backers, and they needed an experienced executive to help guide their green founding team. A source said of Wenger's work at Delicious:"Albert is the adult responsible for managing the USV"。

After Delicious was sold to Yahoo, Wenger joined USV as a venture partner (while tracking other investments). Wenger ended up finding two deals in the first fund — Clickable, which didn’t generate revenue, and Etsy, which went public in 2015 (the latter went public at a $3.5 billion valuation in 2015).

Wenger became a general partner in 2008. Wenger, who is trained as a computer scientist, adds a different perspective to Wilson and Burnham. He was an early partner who identified opportunities in developer tools and productivity."As an engineer, he can pick up a product and use it to program. A source said,"He has an edge on these things."Subsequent investments in MongoDB and Twilio represent the output of this strength. As one source said of MongoDB’s financing:"first level title

Looking back on 2012

Eight years later, the USV is in full swing. According to the institutional investors I interviewed, the company's 2012 offering was its best yet. That's thanks in large part to its stake in Coinbase.

USV recognized the disruptive potential of blockchain early on. Dave Morgan recalled that the company spoke about its importance long before it was outside the blockchain market. He said:"They told us in 2010 that cryptocurrencies are the future". The company used a portfolio meeting at the time to explain cryptocurrencies to its founders, using slips of paper with numbers on them to demonstrate how bitcoin was mined.

Cryptocurrencies represent a natural evolution of USV's interest in networked businesses. The company sees this revolution as another stage in technology adoption. Dave Morgan says:"They always see cryptocurrency as a game of the next generation Internet operating system, not an asset appreciation game"。

Coinbase represents a neat package of this interest. USV led the exchange’s $5 million Series A funding round and has followed through with subsequent funding rounds. Among traditional investments, the company has excelled at growing or protecting its stake in winners, often with a 15-20% stake at exit. Even after selling its 28% stake in Coinbase, USV reached the DPO with a 7.3% stake. After the first day of trading, USV’s stake was reportedly worth $4.6 billion.

Notably, at the time of USV’s first Coinbase investment, the partnership had already added several other talents, including John Buttrick and Andy Weissman. Buttrick brings his legal expertise from working at Davis Polk & Wardwell, while Weissman adds significant early-stage experience and charisma from building Betaworks. A source described Weissman as"startup whisperer", his arrival represents a"cultural shift". Andrew Parker said:"He adds a lot of extroversion to the team"。

first level title

game manual

How do you create the kind of performance that USV manages? While no summary can summarize the operations of a company approaching its third decade, certain characteristics appear to be particularly important to USV's approach.

design a topic

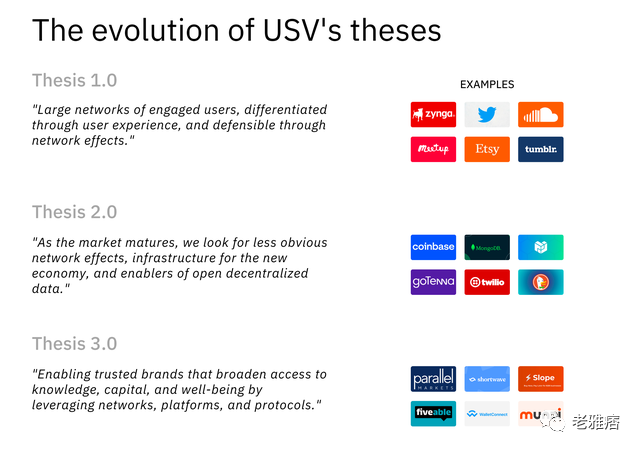

Venture capital can be broadly divided into methodology-driven and opportunistic investors. USV is perhaps the most prominent example of one that has a clear view of the market and invests on its merits. So far, USV has drawn up three topics in succession, as follows.

Methodology 1.0. Huge user network, differentiated through user experience and defended through network effects.

Methodology 2.0. As the market matures, we look for less obvious network effects, new economy infrastructure, and enablers of open decentralized data.

image description

USV

The first of these projects has achieved near-legendary status. In hindsight, USVs were astute at reading the market in the mid to late 2000s and led to investments in Twitter, Zynga, Tumblr, and Etsy, among others.

Methodology 1.0 specifically reflects Burnham's thinking. Several sources point to Burnham's excellence in systems-level thinking, with one describing him as the framework's"architect". another called him"very smart",have"figure out where the world is headed"talent.

Wilson compliments Burnham's ability with his own wit, financial acumen, and knack for distilling complex topics into accessible language. According to one source, the ultimate manifestation of these qualities is a big part of the strength of their partnership. Burnham devised a general theorem, which was honed and elaborated by Wilson. While oversimplified for my benefit, this description captures a core dynamic within the USV.

Actions based on one theory change the entire configuration of a venture fund. Adoption is more targeted rather than diffuse. Evaluation comes from a firm framework, not an ever-changing yardstick. Recommendations are based on working with similarly structured businesses rather than a mix of models. On top of that, funds can also take greater risk on founder profiles, as USVs do, by relying heavily on the methodology itself.

first level title

share your thoughts

For a fund with a track record, USV prefers to stay out of the spotlight and focus on its portfolio. One commentator highlighted the company’s position ahead of the Coinbase DPO as an example of its reserves. As other investors tried to gain credit, USV remained silent. The source said:"Wilson didn't go around bragging, and the USV didn't say anything. It's just silent. because the data speaks for itself"。

While the USV has shown unusual restraint in congratulating itself, that doesn't mean it's staying silent. In fact, the company has an established writing culture that stems from Wilson. He started his blog AVC at the same time as starting USV and has had articles published almost daily since then. The rest of the company may not be able to match Wilson's pace, but the writing is also taken seriously.

USV appears to use this practice to test new ideas and hone its thinking. Wilson's blog, in particular, has helped him build good relationships with entrepreneurs. Speaking of Wilson, Andrew Parker said that the founder"first level title"。

become a true partner

From a founder's perspective, USV seems to fall into the soft zone of venture capital. The company is neither too hands-on nor conspicuously absent. One founder said:"They understand that they are investors, not operators. Most investors don't understand this". The company is there to provide straightforward, high-quality advice without intervention. It works by staying in close contact with the founding team to ensure it understands the state of affairs. Fredrik Haga, CEO of Dune, emphasized this advantage:

USV has established a very close relationship with the invested companies. They have remained small in terms of fund size and team. They understand us pretty well as founders, as a company, as a community, etc. Other companies have more services, but USV has a lot of background... The advice they give is often very general, and unless you have a good background and understanding, it is not that useful.

The team at USV is also "very human, with a lot of empathy," Haga added.

USVs do get their hands dirty when necessary. Albert Wenger is helping Twitter solve its"fail whale"issues and rationalize their engineering teams. A 2008 New York Times article described a potential feature that Wilson scratched off Etsy's roadmap. But the fund has shown an understanding of the beginning and end of its role.

USV also seems to go out of its way to help founders in dark times. Dave Morgan says:"They do things that other funds don't. This includes funding companies to close their doors the right way, helping employees out as much as possible. Truth be told, this act of service pays off in the iterative game of venture capital - founders who close companies often come back king". USV has funded many entrepreneurs several times, including Morgan himself.

A final notable way USV works with startups is through its wider community. It's only fitting that a company so obsessed with network effects built its own. Employees of investee companies have access to a Slack group that appears to serve a similar purpose to Y Combinator's Bookface. It is a place to exchange ideas and receive advice from peers. USV also offers"manager training camp"、"and"and"first level title"。

Management timing

USV is a master of timing. The company has shown a deft ability to pick the right moment to invest and exit."Timing is not something people are usually good at, says Charlie O'Donnell."it's very rare". O'Donnell was USV's first analyst before founding his own firm, Brooklyn Bridge Investments. As mentioned earlier, USV has seized on social media and cryptocurrency, finding big winners in both markets. (USV is also actively investing in leading cryptocurrency funds, including Multicoin Capital. Given Multicoin’s returns, this represents another major win).

Also critically, USV appears to have effectively exited many of its largest positions. The fund sold its Tumblr stake long before its value dropped to just $3 million as part of a $1 billion acquisition. A less obvious version of this story happened with Zynga, where USV reportedly sold its stake in the game before its decline. This also seems to offer good timing for Coinbase.

The USV trick is more than just luck. The company has a playbook for managing its winners. As Wilson writes:"In these pre-list liquidity trades we typically seek to liquidate 10% to 30% of the position"first level title

maintain self-discipline

In April, USV announced that it had raised two new funds: a $275 million early-stage investment fund and a $350 million"opportunity fund". These are modest numbers for a company of this stature and success, but they are consistent with USV's extreme discipline in terms of size. The firm has never raised a fund larger than these latest incarnations because they believe overly large funds affect returns.

USV's approach in this regard goes against industry trends. Many high-profile funds have used the past few years to rapidly expand assets under management. The aforementioned institutional investor said:"People don't say no to money. Especially when they are successful. USV is an exception. They are a special fund in my opinion". According to the same source,"They are one of the very few fund managers who are disciplined in fund size"

The success of USV shows that venture capital can be a game of skill. Even a seemingly fluke gamble in early-stage investing can become a practice, a model, if you're willing to think, work, and maintain discipline.

Benjamin Graham once said:"Successful investment professionals are disciplined, consistent, and put a lot of thought into what they do and how they do it". If he were alive today, the so-called Dean of Wall Street wouldn't have to travel far to find someone who agreed with him.