Waterdrip Capital: How XCarnival Breaks the NFT Mortgage Lending Market

Original Author: Waterdrip Capital

The recent continuation of the NFT market does not seem to be affected by the entire encryption market, but has shown its unique local restlessness. Only Opeasea has 8 series with more than 100,000 ETH Volume, including CryptoPunks / BAYC / Decentraland / MAYC / Art Blocks / SandBox / Clone X / Azuki, etc., the market transaction volume of these 8 series of NFTs is close to 10 billion US dollars.

From the perspective of transaction data, in 2021, people traded NFTs worth more than 40 billion US dollars. Although most of them are punk avatars and "art form" collectible NFTs, the trading volume of NFTs has increased compared to previous years. With the growth of geometric multiples, the transaction category has also covered cyberpunk, music, paintings and other art collections, bills, bonds and other assets on the chain track, games, social, metaverse and other fields. NFT has become the most popular in the blockchain field. The fastest and strongest out-of-the-box tool.

However, in sharp contrast to the rapid growth momentum and huge transaction volume of NFT, there are currently only a few NFT mortgage lending platforms serving this market with huge potential, which makes us want to Find out.

Why has the NFT mortgage lending market with such huge potential not formed a scale?

Through preliminary research and analysis, we believe that the reason why the NFT mortgage lending market is still relatively small mainly comes from the following two factors:

Liquidity of NFTs

Price Discovery for NFTs

If you want to use NFT for mortgage lending, you need to treat NFT as a financial asset. For financial assets with insufficient liquidity or even lack of liquidity, the growth of the mortgage lending market derived from it needs to be based on the liquidity of its assets. superior.

Insufficient liquidity of NFT will lead to the following common phenomena:

The turnover rate of most NFTs is very low, and they mainly adopt peer-to-peer transactions. After the sellers list on platforms such as Opensea, they may wait for a long time without buyers buying, and finally fail to make a deal.

A small number of series of NFT are sought after by most people, but the price is high. After being purchased and collected by a few big households, they are no longer sold, and ordinary NFT users are turned away.

More generally, the proliferation of NFTs. Anyone can generate and create their own NFT on platforms such as Opensea. Now there are more than 29 million NFT projects launched only on Opensea. Although users can purchase NFT according to their own preferences, what is closer to reality is that users have no ability at all. Identify which NFTs have real value from tens of millions of NFTs. When a large number of NFTs are created, they also announce their demise and are submerged in the ever-increasing wave of NFTs.

price discoveryprice discovery

Price discovery is the result of the contact between the seller and the buyer. In other words, the price discovery of NFT is the result of the interaction between the NFT supply side and the demand side. This happens tens of millions of times a day in the traditional market and even in the Defi market. The behavior of the NFT market seems to be a bit out of order, and this is also a long-term problem that NFT needs to solve urgently:How to fairly price NFT。

In our portfolio, Pawnhouse is a comprehensive platform that provides price discovery for non-standard assets (Non-Standard Assets) including NFT. The Synchronized Multi-Round Auction (SMRA) system it advocates can help NFT market participants better obtain pricing services and encourage bidders to provide price information. The SMRA system is currently in the internal testing phase, and interested readers can stay tuned.

In the absence of a value consensus mechanism for NFT, it is difficult for borrowers and lenders to reach a basic consensus on the value evaluation of the target NFT. It is also easy to understand why a large number of NFTs can be actively traded on platforms such as Opensea, but cannot be supported by NFT mortgage lending The platform is included, and mortgage lending is no longer possible.

Since NFT has shown a deterministic growth trend, looking to the future, NFT mortgage lending is a major problem that must and must be solved.

The current mainstream solutions mainly include P2P mode and capital pool mode.

secondary title

P2P mode

The P2P model, because it is applicable to all NFTs and can also reflect the unique value attributes of NFTs such as scarcity, is currently the most familiar and most used solution.

For example, as early as half a year ago, the XCarnival1.0 version has operated the P2P lending method on the BSC. Relying on the project ecology, it successfully solved the pain point of the imbalance between borrowers and lenders.

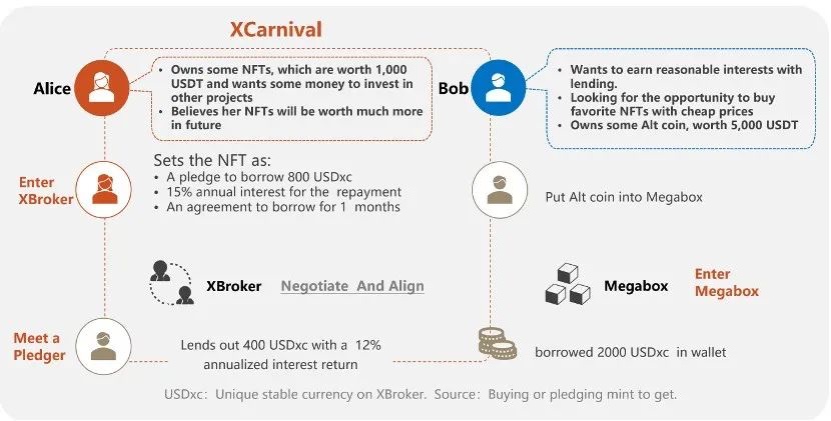

The P2P model of NFT mortgage lending probably works like this:

User Alice has some NFTs worth about $1,000, but she wants to mortgage them and borrow a sum of money to invest in other projects. She can set her own NFT on the XCarnival platform:

Loan amount: 800USDxc

Loan interest: Nianhua 15%

Borrowing time: one month

At the same time, user Bob wants to manage some tokens worth $5,000 in his hands, buy his favorite NFT, and obtain reasonable income. He can operate on the platform as follows:

Put the Token into the Megabox and Mint out 2000USDxc If you like Alice's NFT, you can bid, for example, 400USDxc, and get an annualized 12% borrowing income.

One month later, Alice repays the principal and pays interest, redeems her NFT, and Bob may get the corresponding borrower's income, or Alice does not repay the principal and interest, and the NFT worth $1,000 belongs to the borrower Bob.

Pros and cons of the P2P model

Although the P2P model can solve the problem of different NFT prices in actual use, especially for NFT types such as high-value and rarity attributes, and make separate quotations for NFTs with different attributes and scarcity, there are also Many problems, such as long transaction time (NFT owners can only wait for others to place orders or quotes, and need to check from time to time), low efficiency of fund use, and high interest, etc. For NFT owners who are in urgent need of money, this kind of The user's sense of uncertainty is also relatively poor.

secondary title

Fund pool model

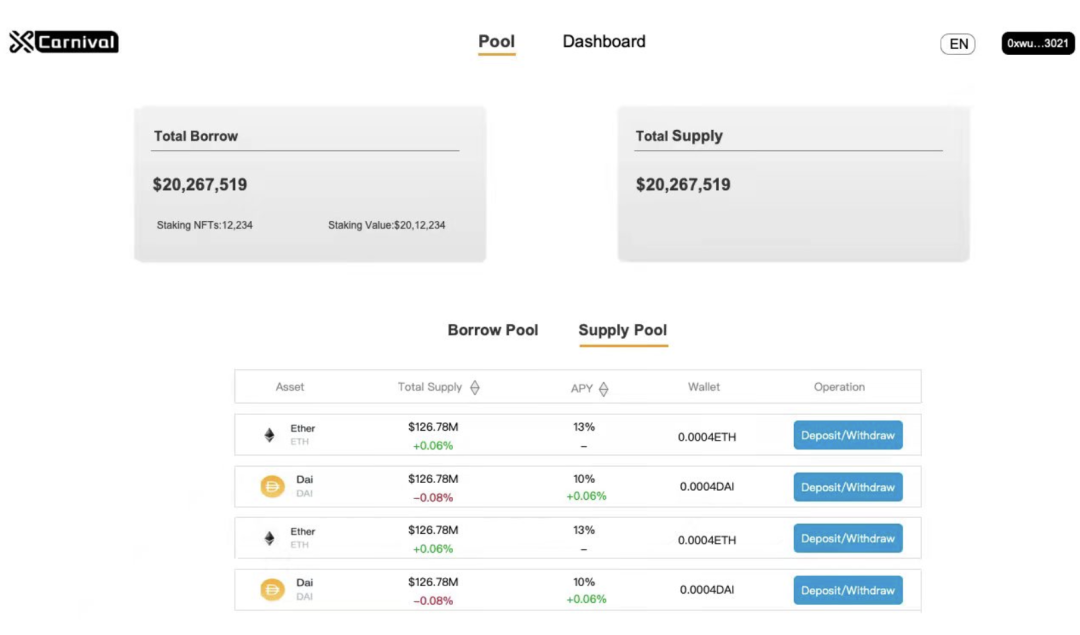

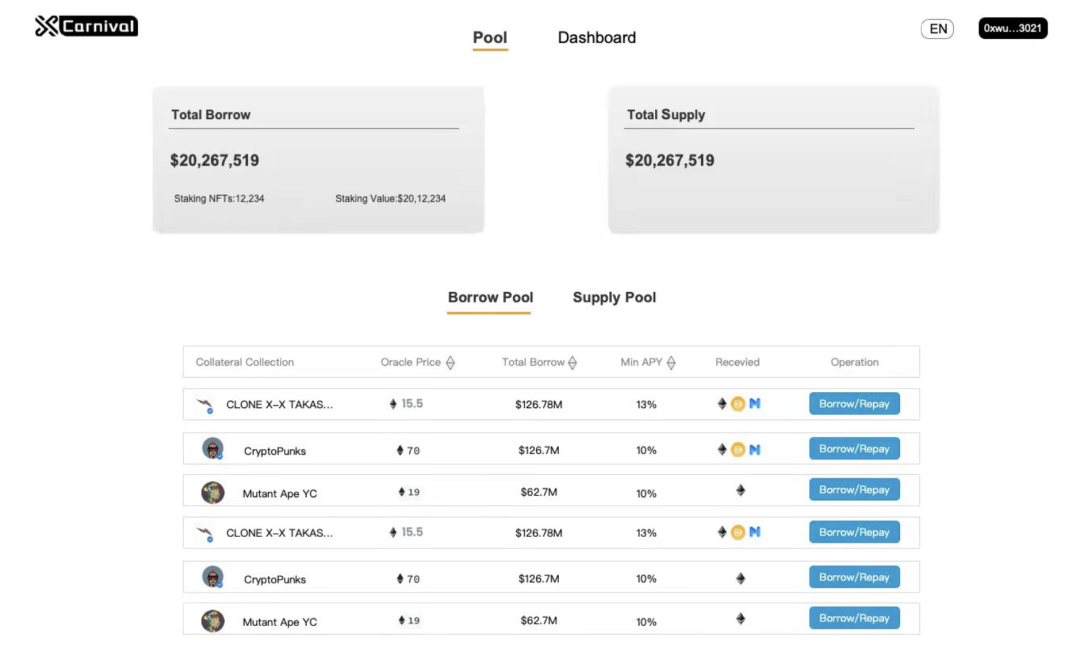

The fund pool model of NFT mortgage lending refers to the fund pool model of Defi. NFT owners can lend loans immediately after over-mortgaging NFT to the pool. The whole process is like using AAVE/Compound. This is also a mainstream exploration direction for the combination of NFT and DeFi at present, and some projects are making exploration attempts in this area, and the boundary between NFT and DeFi will become increasingly blurred.

In the fund pool mode, the lending process of NFT is similar to that of Defi. The fund provider can put its Stablecoin or ETH and other tokens into the fund pool to earn interest and earn stable interest. The amount of interest paid by the NFT owner depends on the The amount of loan funds in the pool and the supply of NFT. If the NFT owner does not pay or the price of the NFT falls to the liquidation line, the NFT will be placed on a trading platform such as Operasea for auction, and the funds will be returned to the fund provider.

Compared with the P2P model, the capital pool model has the following advantages:

The transaction process is rapid and the cycle is short

The loan amount is clear

The loan scale is relatively large, and the threshold for participation is lowered

Loan interest is stable and relatively low

Users who hold large blue-chip NFTs, such as Punks/ BYAC and other NFTs, as long as they have a loan demand, under the fund pool mode, they can mortgage NFTs and immediately obtain a loan of a clear amount, without waiting for price discovery, and almost no need to worry about NFTs Losses caused by price manipulation. Because the benefits obtained through price manipulation may be far less than the costs that need to be paid.

Taking CryptoPunks as an example, as shown in the figure above, the average transaction price of Punks in the last 30 days is 109ETH, and the floor price is about 68.5ETH. We assume that the proportion of Punks participating in the mortgage is only 20%, and the floor price of 68ETH can lend 20 ETH (assuming that the loan is provided at 30% of 68ETH). If you want to make a profit by raising the floor price of borrowing, even if the big players collude with each other, you still need to raise it to more than 204ETH to make a profit. A 20% mortgage rate requires a transaction volume of 408,000 ETH. If the mortgage rate is 30% , it requires a transaction volume of more than 600,000 ETH. At the same time, this is based on the premise that the intrinsic value of Punks is 68 ETH and will not rise, so the cost is much higher than the benefit.

The fund pool model also has certain shortcomings, and it cannot match all NFT series. For example, for NFTs with specific rare attributes, it is impossible to give a more fair loan amount exceeding the floor price. There are relatively few NFT series suitable for the fund pool model. Concentrate on the CrytpoPunks/BYAC big blue-chip NFT series, and for the long-tail NFT series, the risk of the capital pool model is relatively high, and the price of NFT may be manipulated by large funds, which will lead to the inability to sell NFT in time after being liquidated, causing borrowers loss of funds. In addition, the capital pool model is more complicated after all. Even if most of the logic is similar to AAVE, there are still risks of smart contracts.

The disadvantages of the funding model can be summarized in the following aspects:

Not applicable to all NFTs, only applicable to mainstream series of NFTs

Long-tail NFT assets have price manipulation risks

secondary title

Summary of P2P model and capital pool model

The P2P model is theoretically applicable to all NFTs. Users place an order for their own NFT on the lending website, and both the borrower and the lender choose independently. The disadvantage of this method is that users cannot measure whether the NFT price deviates from the market price, and both borrowers and lenders have to bear higher risks. If the borrower does not repay the loan, the NFT liquidation link will also be unclear, and it is difficult to guarantee the rights and interests of the lender.

The target of the fund pool model is concentrated in the mainstream NFT lending market. The key to the NFT mortgage loan project using this model lies in the ability to integrate mainstream NFT resources. Because the mainstream/blue-chip NFT series is a stock market, if you can get more supply of mainstream/blue-chip NFT series, you can quickly occupy market share, attract and drive the inflow of loan funds, form a positive cycle, and then establish advantages to truly attract Blue-chip NFT and funding supply enter the NFT mortgage lending market.

XCarnival - How to Break the NFT Mortgage Lending Market

Officially seeing this, XCarnival is about to launch its own NFT lending pool on the ETH chain after half a year of running the P2P model on the BSC, and plans to officially land on the ETH chain in the middle and late March of this year. It is believed that the launch and launch of the NFT lending pool on the Ethereum chain will give a boost to the NFT mortgage lending track.

image description

(picture from internal beta)

image description

(picture from internal beta)

The second is the NFT holder. Users who hold NFT can directly obtain Stablecoin by putting NFT assets into the lending pool. Users can directly use the lending pool to quickly mortgage their mainstream NFTs to different pools, and lend corresponding mainstream tokens such as ETH, USDT, etc., and users can borrow and repay at any time.

The last is to guarantee the rights and interests of both borrowers and lenders. How to ensure that the lender's Stablecoin will not be swept away, and at the same time ensure that the borrower can repay the money? XCarnival uses the oracle mechanism to ensure the safety and smooth completion of transactions to the greatest extent.

image description

(picture from internal beta)

Regarding the oracle mechanism, the project party has not yet disclosed it. The current solution is basically to use the data on the chain to make TWAP (time-weighted average price). TWAP uses multiple time dimensions as data sampling sources, and eliminates extreme values at the same time. According to the comprehensive floor price, the same NFT can only be judged once for multiple transactions within a period of time to avoid being attacked, and at the same time prevent the price from being manipulated in this way.

Competitive Analysis

Competitive Analysis

Stani Kulechov, founder of the decentralized lending protocol Aave, tweeted last July that Aave is experimenting with using NFT as collateral and hopes that the protocol will be suitable for various NFT use cases when it is released. Today, half a year later, Aave's lending pool for NFT has not yet officially launched, so you can stay tuned.

There are still very few projects that use the fund pool model to support NFT mortgage lending. In addition to Xcarnival, which is about to launch this model in March this year, Drops has also said that it will launch the fund pool model, but at present, Lending Pool is also waiting to be launched (coming soon) ) stage, you can keep paying attention.

market outlook

It can be seen that the current use of the fund pool model to support NFT mortgage lending is still in a very early stage. In addition to having a keen sense of business, it also requires strong resource integration capabilities and product development capabilities.

XCarnival will land on Ethereum in March this year. In addition to the existing P2P mode, the officially launched Pool to C mode,secondary title

text

Community

Twitter: follow 52002 people

Telegram: 41,294 people in the international telegram group, 46,108 people in the Chinese telegram group

platform data

Mortgage NFT: 26746 pieces

Loan size: $20,659,142

Currency holding address: 13519

XCarnival Milestones

1. Win the BSC Hackathon Championship and pass the security audit of Certik and PieDun

2. Jointly launched XCarnival Genesis NFT with Galaxy.Project

3. Launch the BSC main network and launch the P2P model of NFT mortgage lending: the first batch of projects such as XCarnival, BabySwap and Pancake are supported, and liquidity rewards are launched

4. List CMC and CoinGeCko and get CMC traffic support

5. Simultaneously launched two well-known trading platforms, Sesame and Matcha, and officially launched the syrup pool incentive with Pancake

6. Start the Gamefi launch platform - XIGO: successfully completed the launch of the two major Gamefi projects Bino and Dracoo

7. Completed the first show of the Binance NFT market project: 9,000 XCarnival Combo Cards were sold out in 2 seconds

8. The scale of BSC loans exceeded $20,000,000, and the total number of mortgage loans exceeded 20,000

【references】

[Related interests] WaterdripCapital participated in the early investment of XCarnival. This article does not constitute any investment advice and is for reference only.