What exactly is ve(3,3) that AC is trying to advertise?

Recently, Andre cronje, the founder of Yearn Finance and Keep3r Network, tried his best to promote a mysterious new project of his own on social media - ve(3,3). But so far, although AC has released many details of the project, its real veil has not been lifted. After collecting relevant information, the editor of Rhythm sorted out the content of the following article.

AC's project will be in partnership with Daniele, who created such hits as Abracadabra. money, Popsicle Finance and Wonderland Finance. ve(3,3) will be established under the protocol-to-protocol service architecture and will not compete with existing projects. Generally speaking, ve(3,3) is more like a group version of Curve, but it is not controlled by the liquidity provider, but by the agreement, so that the agreement can better control the inflation and emission rate of its own Token.

The project's token is currently called ve(3,3), but it can be speculated from the review diagram below that it will be called "SOLID".

ve(3,3) How does the Token economy work?

ve(3,3) It will combine the "ve" voting escrow mechanism of protocols such as Curve and the (3,3) rebase mechanism of DeFi 2.0 protocols such as OlympusDAO. By locking Token for a longer period of time, users can obtain higher incentives and greater weight in protocol governance.

Like OHM, the actual value of the ve(3,3) agreement is less than its treasury book value, but the total price of Token transactions is higher than the treasury value. The higher the transaction price, the higher the APY of the protocol. The number of tokens pledged by holders will increase over time, but the value of tokens will also be diluted to a certain extent. In addition, the fees generated by the agreement will also be added to the treasury.

But compared to Curve and OHM, ve(3,3) has a very interesting unique mechanism.

For Curve holders, the locked veCurve cannot be sold, and they are "trapped" in the user's wallet most of the time. However, the "veToken" of ve(3,3) can be converted into NFT, which means that holders can use them for transactions. In this way, the locked governance token has its own secondary market and becomes A way to sell voting rights.

To sum up, the value of ve(3,3) native Token is mainly driven by the following factors:

1. The locked Token will be given the voting right to guide the distribution of mining pool incentives

2. The weekly emission of Token will be adjusted according to the proportion of circulating supply. As Token is continuously distributed, the pressure brought by emission will gradually decrease

3. The number of locked Tokens will increase proportionally with the weekly emissions

4. The locked Token can be converted into NFT

5. The smaller the proportion of locked-up Tokens to the circulating supply, the less emission allocations they get, which encourages more holders to lock their own Tokens

6. A longer lockup will also generate a higher APR, which incentivizes long-term lockups

KP3R:ve(3,3) Heavyweight helper

AC mentioned in the previous introduction article that ve(3,3) will not allocate fees in the form of native Tokens or stable coins, but will allocate "fee assets" that can continuously pass on the value of fees, so that the native Token The selling pressure is reduced.

KP3R (Keep3r Network) is currently the "fee asset" of Andre Cronje's project to accumulate fee value. It is a two-in-one ERC-20 Token, and its pledgers have two sources of income:

1. FixedForex platform fees: FixedForex is similar to Curve, but it is mainly aimed at the foreign exchange market with a potential scale of nearly one trillion US dollars. In 2022, as more and more international players join the crypto world, the demand for trading various currency-pegged stablecoins will also grow, bringing more platform fees to FixedForex.

2. Keep3r Network platform division: Keep3r Network mainly provides payment services for different protocols to help them entrust third parties to complete specific tasks.

Soon KP3R will be modified and based on the ve(3,3) model. Confirmed by AC, ve(3,3) is testing KP3R and will be released as early as this week.

Under the new ve(3,3) model, the number of vKP3R will no longer decrease over time. On the contrary, it will encourage more holders to continue locking positions. Users must lock KP3R if they want to get fee distribution. And receive vKP3R in return.

In the article "Curve War upgrades CVX battle, the wonderful power struggle continues", it is mentioned that Convex transformed Curve War into a war about Conevx by providing higher liquidity incentives, and attracted Protocols such as Frax Share have joined in. And KP3R, which is based on a unique revenue-generating model and ve(3,3) new Token economics, is also likely to join and win this war.

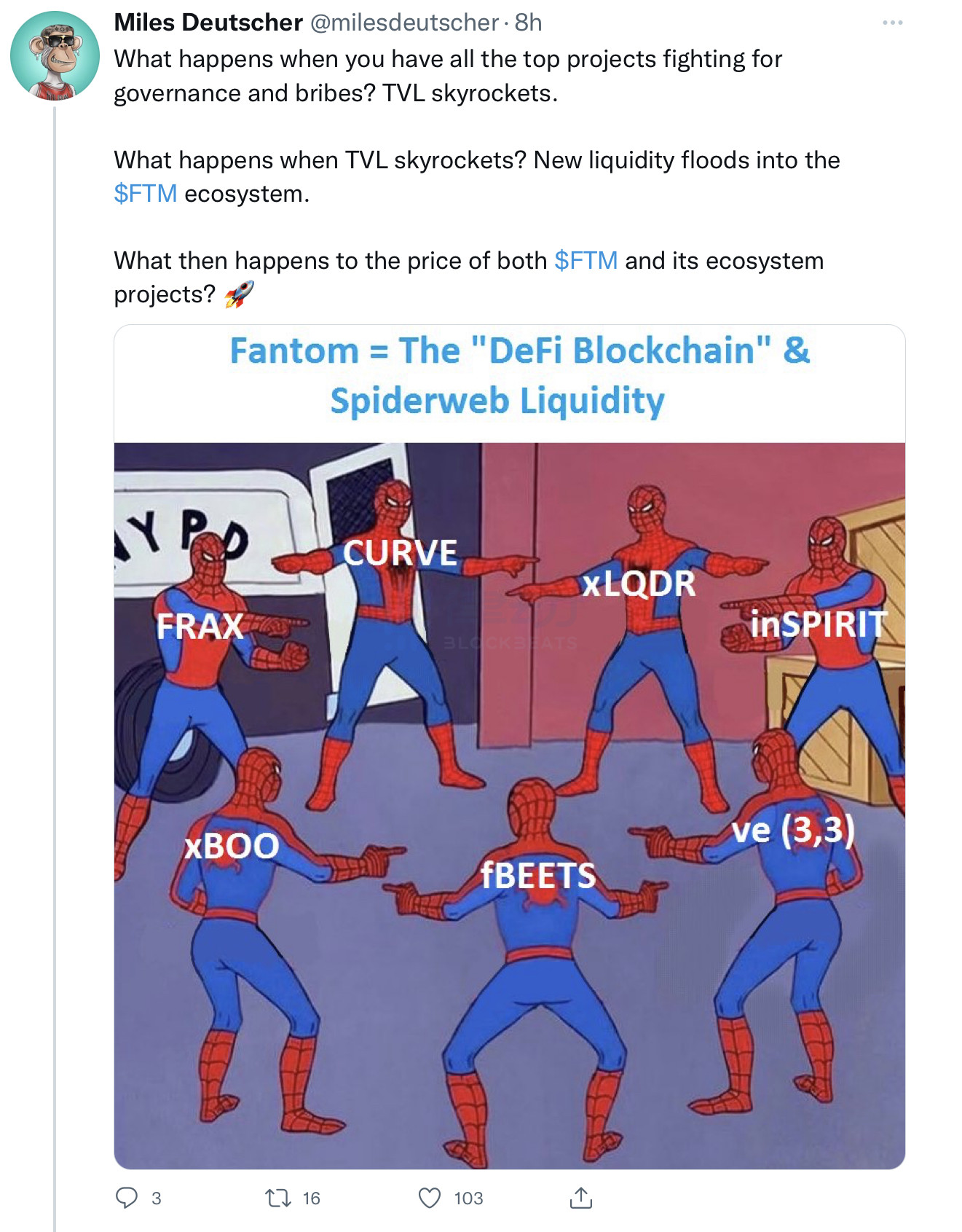

Drainage for FTM and KP3R

According to the latest article in AC, the native Token of ve(3,3) will not be available for purchase in the open market, and it will be allocated to the top 20 protocols based on the TVL on the Fantom public chain.

In this way, ordinary users who want to capture the value produced by ve(3,3) have only two options:

1. Tokens holding FTM and the top 20 agreements on FTM

2. Holding KP3R

As Miles Deutscher said, when all the top projects in a public chain ecosystem start to compete for governance rights, TVL will soar. And new projects will be attracted by this, and further bring more liquidity to the ecology. Undoubtedly, the Token allocation strategy formulated by ve(3,3) will bring more attention to FTM and KP3R, and the future performance of the Fatom ecosystem is also worthy of attention.