你在CEX買到的真不是美股:拆解94%清算壟斷與五層管道下的權益蒸發

- 核心觀點:當前加密交易所的美股產品並非簡單的RWA資產革命,而是分化為傳統API、代幣化(Tokenized)與合成永續合約三條路徑。其中,代幣化模式高度依賴Alpaca的清算壟斷,存在鏈上即時交易與鏈下T+1結算的時間差風險,且用戶並不享有真實股東權益,而是持有離岸主體發行的債務憑證。

- 關鍵要素:

- 三條路徑分化:傳統API模式(如Binance與Alpaca合作)提供真實股東權益與SIPC保護;代幣化模式(如Backed、Ondo)犧牲所有權換取鏈上流通性;合成永續合約(如Hyperliquid)僅提供價格衍生品博弈,無真實資產交割。

- Alpaca壟斷與風險:Alpaca壟斷了94%的代幣化美股清算託管。其ITN系統雖實現鏈上秒級鑄造,但底層證券仍受限於傳統T+1結算週期,產生的「時間差」風險和流動性斷層最終由終端用戶承擔。

- 權益與法律風險:在五層中介架構中,用戶的投票權在發行方層面空轉;分紅演變為合同債權而非股東權利;SIPC保護無法穿透至鏈上持有者,一旦發行方破產,用戶代幣將無法追回底層資產。

- 市場增長與規模:鏈上美股代幣總規模在10個月內從不足1億美元擴張至15.6億美元(截至2026年6月),但仍遠低於傳統市場。同時,傳統API路線正快速分流部分尋求合規保障的資金。

- DeFi潛力初顯:Binance發行的bStocks已作為抵押品納入Venus Protocol借貸池,標誌著代幣化美股開始探索DeFi組合性,但該應用仍處早期實驗階段。

- 技術演進方向:DTCC計劃於2026年下半年啟動代幣化證券試點,若成功落地,將為代幣化資產注入傳統級別的法律權益與清算保障,可能重塑當前競爭格局。

Original authors: Ethan, Xinyang, IOSG

In 2026, CEXs intensively launched US stock trading products, creating a booming narrative at the industry's forefront about "seamlessly buying and selling NVIDIA with USDT." However, peeling back the smooth trading interface to examine the underlying legal relationships and clearing processes reveals that this is far from a simple "RWA asset revolution." It is a complex game of interests involving spot pricing, ownership attribution, and underlying custodial monopolies.

TL;DR

- Three diverging paths: Crypto exchange US stock products have diverged into three parallel paths: Traditional API, Tokenized, and Perpetual Contracts.

- Tokenized model heavily relies on Alpaca: Monopolizing 94% of tokenized US stock clearing, it presents a time-lag risk between on-chain real-time and off-chain T+1, ultimately leaving users to bear the hidden costs and black swan liquidity gaps.

- The Tokenized U.S. Stocks market is still in a blue ocean phase: Asset scale expanded approximately 15 times in 10 months, DeFi collateral potential is emerging, while the Traditional API route is rapidly diverting capital.

The Three Diverging Paths of US Stocks

In terms of capital flow, asset form, and most fundamentally, legal relationships, the US stock trading products offered by CEXs on the market are not a single category. Beneath the highly homogenized front-end trading interface, they have diverged into three completely different evolutionary paths based on differences in underlying assets and legal structures:

The coexistence of these three models is not the result of a short-term product design decision but a product of the continuous compromises and iterations within the on-chain ecosystem over the past few years as it navigated between liquidity efficiency and traditional compliance clearing friction.

Early Exploration and Liquidity Limitations of Offshore Tokenization

The starting point of this track dates back to the period between 2021 and 2024, marked by early attempts at on-chain asset tokenization (Tokenized Securities) led by projects like Backed Finance (xStocks) and Ondo Finance. The core business model at this stage involved setting up Special Purpose Vehicles (SPVs) in offshore jurisdictions, fully collateralizing real stocks off-chain, and minting corresponding tokenized certificates (e.g., AAPLx) on-chain as a mirror. These assets possess the native characteristics of crypto assets, allowing them to be withdrawn to Web3 wallets and transferred permissionlessly on-chain, successfully establishing a paradigm for moving assets from 0 to 1 on-chain.

However, during the window period before traditional financial clearing giants substantially entered the crypto ecosystem, this model exhibited severe supply-side scarcity and scale limitations. Lacking underlying liquidity support from major centralized exchanges (CEXs), these tokenized assets could only circulate on a few decentralized protocols or second-tier platforms, causing the total value locked (TVL) of the entire track to languish at low levels. By August 2025, the total scale of on-chain US stocks across the network was less than $100 million. This characteristic of "having an asset mapping but lacking transaction friction efficiency" inevitably relegated early tokenized US stocks to low-liquidity settlements on-chain, failing to truly reach mainstream retail traders.

Synthetic Perpetual Contracts: Pure Derivative Price Speculation

To compensate for the liquidity shortcomings of spot tokenization, perpetual contracts for US stocks/ETFs quickly became the market's main focus. In September 2025, Bitget pioneered US stock perpetual futures, rapidly expanding its offering to over 40 products with cumulative trading volume exceeding $15 billion. However, the real catalyst that ignited the track was Hyperliquid's HIP-3 (Permissionless Perpetual Contract Deployment Mechanism) launched on October 13, 2025, which fully activated the 24/7 equity derivatives market. By June 2026, the total open interest (OI) in US stock-related perpetual contracts had surpassed $2.25 billion. Hyperliquid, leveraging HIP-3, holds a dominant share, with its Nasdaq-100 (XYZ100) and S&P 500 index perpetuals having OIs exceeding $310 million and $340 million respectively.

Binance also aggressively followed suit in early 2026, capturing over 56% of the CEX market share in the RWA perpetual sector. Notably, pre-IPO derivatives like SpaceX (SPCX) saw peak daily trading volumes reaching tens of billions of dollars. Furthermore, Binance's launch of Korean stock perpetual futures (Samsung, SK Hynix, Hyundai) in early June 2026 generated cumulative trading volume of approximately $470 million in its first week, with SK Hynix contributing over 90% and frequently exceeding $100 million in daily volume. This demonstrates the strong interest from retail leveraged traders in globally hot assets like AI semiconductors. This highlights a key advantage of crypto perpetual contract platforms: the ability to quickly integrate international hot assets that traditional brokers may find difficult or insufficient to service, providing global retail investors with timely leveraged trading channels.

These synthetic perpetual contracts do not involve any actual off-chain stock delivery. They rely entirely on oracle price feeds and facilitate long-short speculation within the crypto exchange ecosystem. This design offers high capital efficiency and continuity, especially providing efficient price discovery and liquidity during US stock market closed hours. In contrast, genuine tokenized spots, due to the need to interface with traditional T+1 clearing, custody, and underwriting processes, often exhibit significant liquidity gaps, larger slippage, and price distortions on-chain. This paradox, where "derivative pricing efficiency surpasses spot," has become a structural pain point that the current tokenized stock model struggles to avoid.

Traditional API Model: Exchanges Returning to Internet Brokerages

Entering 2026, despite the US Securities and Exchange Commission (SEC) promoting the "Project Crypto Innovation Exemption Framework" aimed at providing a regulatory sandbox for digital assets, mainstream exchanges began looking towards a more pragmatic path due to uncontrollable delays in the legal characterization and comprehensive compliance implementation of native on-chain securities (Tokenized Securities). In June 2026, Binance officially announced a deep partnership with Alpaca, a US-licensed self-clearing broker, to launch US stock and ETF trading services.

This "Traditional API Routing Model" is essentially an extension of the traditional retail brokerage architecture grafted onto the front end of a crypto exchange. Through its affiliated broker Nest Trading for routing, blockchain technology plays no role in the settlement of the product's entire lifecycle. The user's holdings are merely a data mapping within the exchange app; orders are ultimately executed on the NYSE or NASDAQ, and the underlying securities are held in the user's Alpaca account.

The cost of this model is sacrificing all native characteristics of crypto assets: stocks cannot be withdrawn to a Web3 wallet, cannot be transferred on-chain, and certainly cannot be moved across platforms. The user's "holdings" are just a line of digital mapping *inside* the exchange app. However, its underlying logic is the most robust. The user is legally the "Beneficial Owner" of the security, entitled not only to full dividends and nominal voting rights but also to the legal protection of the Securities Investor Protection Corporation (SIPC). This may appear as a compromise and regression for crypto exchanges, yet it is currently the only path that allows users to truly "own" the stock.

Exchanges' Multi-Track Parallel Approach

Looking at the current mainstream US stock product lines, a deeper industry consensus emerges: most leading exchanges have not placed all their chips on a single path but have adopted a multi-model parallel product layout. For instance, platforms like Binance, Bitget, and Bybit often simultaneously operate multiple underlying systems, including Traditional API routing, tokenized assets, and synthetic perpetual contracts. This multi-track approach is not product redundancy. The core reason is that it caters to the actual needs of different user groups within the crypto ecosystem. High-frequency speculators value the high capital efficiency and leverage of synthetic contracts, while large long-term allocators (whales) prioritize the compliance assurance and SIPC legal protection offered by the Traditional API model.

This hybrid layout is also a hedging strategy for exchanges against regulatory uncertainty. The Traditional API model leverages and compromises with the existing Web2 securities compliance system. The Tokenized model pushes the boundaries of RWA innovation in offshore jurisdictions. Synthetic derivatives purely digest risk within the crypto network itself. By preparing multiple channels, exchanges can flexibly adjust their product focus based on the regulatory policies of different regions, thereby diversifying political risks.

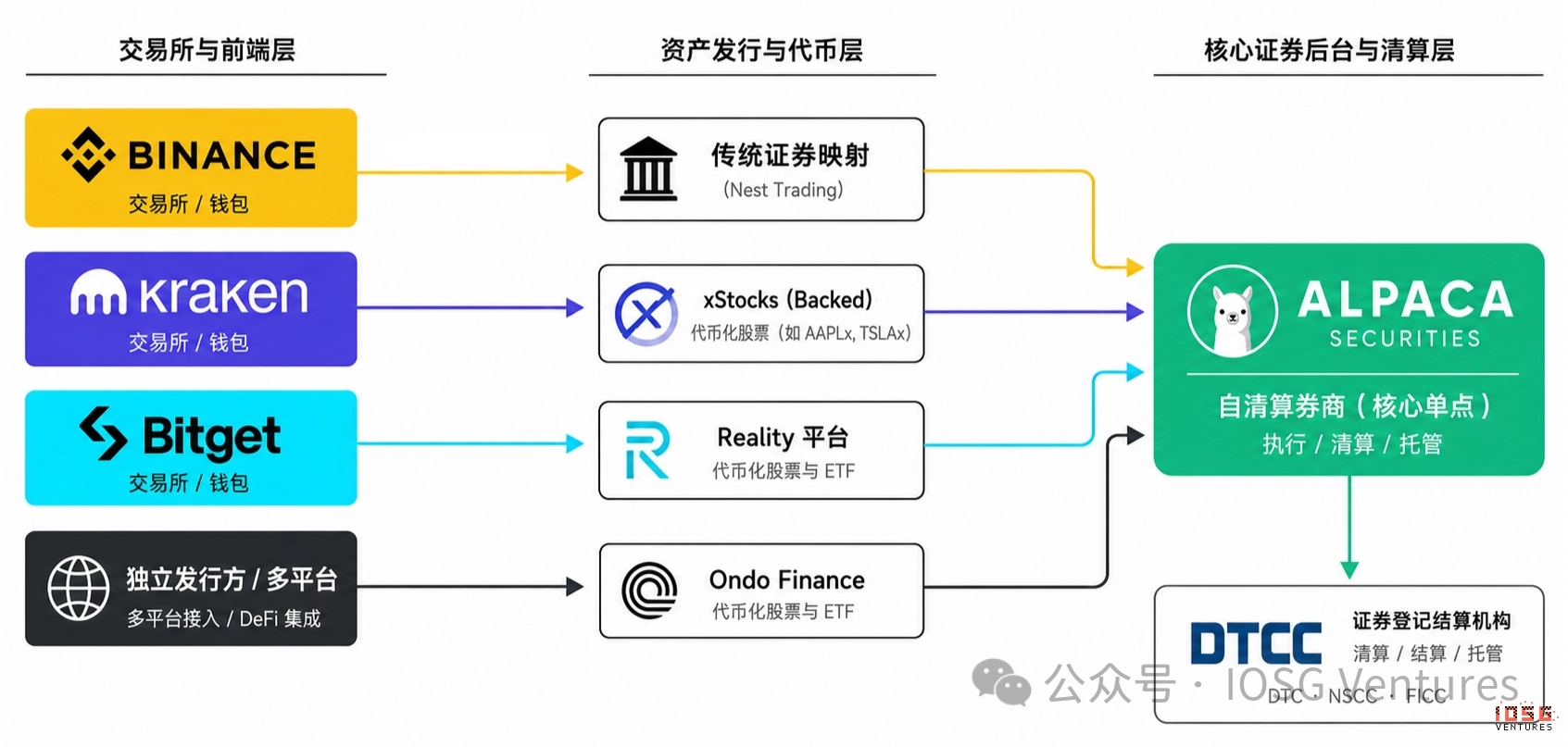

Architectural Layers: The Stripping of Rights Across Five Layers

To understand the essence of equity dilution in on-chain US stocks, one must look away from the smooth front-end experience and audit downwards along the data pipeline. The difference originates not from the token's name or on-chain narrative, but from how many intermediate layers exist between the end-user and the ultimate underlying asset.

The reason the Traditional API model can fully preserve shareholder rights is that it follows a very clean Web2 three-layer architecture:

User → Broker → Depository Trust & Clearing Corporation (DTCC)

In this pathway, the broker acts merely as a nominee pipeline. The law directly extends ownership protection through to the end-user, solidifying their legal status as the "Beneficial Owner."

However, to forcibly "bring stocks onto the chain," the Tokenized model introduces multiple intermediary layers. It is forced into a complex five-layer structure:

[End User] ──> [Crypto Exchange] ──> [Token Issuer] ──> [Intermediary Broker (Alpaca)] ──> [DTCC]

This increase in layers is not a harmless engineering cost; it represents a significant consumption of asset rights throughout the transmission chain. Within this structure, each layer intercepts or distorts the legal rights originally belonging to the shareholder.

Futile and Evaporated Voting Rights

At the foundation of the traditional securities system, the underlying stocks for all US equities are registered under the DTCC's nominee, Cede & Co. Firms like Alpaca or Apex, as DTCC participants, are the holders in terms of beneficial ownership. This means that corporate actions, such as shareholder meeting notices and voting guidelines, at the end of the traditional clearing network, are only sent to licensed brokers like Alpaca.

When the architecture stretches to five layers, the chain of rights transmission breaks here. Alpaca, as a standard broker, has legal obligations and system interfaces that only connect to its direct clients – which are the token issuers like Backed Finance or Ondo Finance. Alpaca has no legal obligation to develop a complex voting rights penetration system for these crypto entities.

Meanwhile, the issuer layer also faces a systemic vacuum in both technology and compliance: they fundamentally lack the infrastructure to map the daily voting decisions from potentially thousands of underlying stocks to their on-chain token holders in real-time and securely. Consequently, voting rights stop their transmission at the bridge broker layer and become futile and evaporate at the issuer layer.

Dividend Redistribution and Contractualization

Unlike the complete disappearance of voting rights, dividends – the most attractive economic benefit – evolve into an indirect, repackaged distribution mechanism within the complex five-layer architecture.

When Apple or Nvidia pays a cash dividend, the dollars first flow into Alpaca's account. Alpaca deducts relevant taxes and fees and then disburses the funds to the account's nominal owner – the token issuer. From this moment, the funds leave the jurisdiction of securities law and become part of the issuer's corporate assets. Whether on-chain token holders receive money, and in what form, depends entirely on the contractual agreements and operational processes signed by the issuer in their offshore jurisdiction.

In practice, to avoid the complex cross-border clearing and securities regulatory risks associated with directly distributing dollars, mainstream projects like xStocks and Ondo commonly adopt an "automatic reinvestment" mechanism. Upon receiving cash dividends off-chain, they automatically reinvest them in the secondary market to purchase more underlying stocks. Then, by adjusting the multiplier in the on-chain smart contract or the Net Asset Value (NAV) price of the token, this income is reflected non-visually in the user's token balance or token price.

Currently, only a very few platforms like Bitget Reality attempt to distribute dividends directly on-chain in the form of USDT. However, both models are, in essence, not the shareholder dividends granted to you by securities law. They are a contractual claim you have against the offshore token issuer, dependent on the proper functioning of their technical nodes.

SIPC Protection Failure

The most critical hidden danger in the five-layer architecture is the legal vacuum during extreme risk events. In the traditional US securities market, the SIPC provides broker clients with a bankruptcy protection net of up to $500,000. This is the cornerstone of trust that allows retail investors to entrust their assets to emerging brokerages.

However, in the Tokenized model, Alpaca's direct clients on its books are SPVs registered in the Cayman Islands or Seychelles by Backed, Ondo, or Bitget, not the individual users on the chain. This means the SIPC protection net can, at best, cover the "token issuer" layer.

If Alpaca itself faces a clearing crisis, the issuer might file a claim with SIPC as a client. However, if the token issuer itself goes bankrupt, absconds with funds, or suffers a hacker attack, the protection umbrella of traditional securities law completely fails. Under current bankruptcy and securities law systems, there is no clear legal precedent supporting the "penetration" of SIPC protection to benefit an on-chain end-holder who holds a Solana SPL token in one hand but has no record in the securities system in the other.

This harsh legal reality is frankly disclosed in the official compliance documents of major issuers. Ondo Finance's legal terms are very explicit: the token provides "Economic Exposure" to the performance of the underlying assets. The holder does not possess the right to hold or receive the underlying asset.

This clearly defines the ultimate physical reality of on-chain US stocks: you are not the owner of the stock. You are merely the holder of a digital IOU issued by an offshore entity that tracks the price of the US stock.

Potential Risks Under US SEC Regulatory Compliance

Under the nested five-layer architecture, the outbreak of risk does not follow the compensation path of traditional securities law. Instead, it is directly constrained by the compliance game between the offshore SPV and the upstream clearing broker. When regulatory bodies like the SEC conduct a penetrating enforcement action on cross-border securities tokenization, the potential default and risk transmission path typically exhibits three distinct stages:

First, to mitigate compliance and reputational risks, the upstream licensed self-clearing broker will typically choose to cut off the API routing to the offshore SPV. Since the offshore issuer loses its actual clearing and settlement channel off-chain, its on-chain smart contracts will be forced to cease all minting and redemption functions.

Second, because anonymous on-chain addresses lack compliant confirmation records within the traditional securities settlement system (DTCC), the SIPC's bankruptcy protection umbrella wholly stops at the issuer entity and cannot penetrate downwards to exempt terminal holders. If the issuer goes bankrupt, the tokens held by users face the default risk of being unable to reclaim the underlying assets.

Facing this legal gap, the current path for on-chain US stock tokenized spots is gradually evolving towards contractual trusts. Platforms like Ondo Finance are moving away from the initial form of pure SPV mapping, leaning towards embracing a more rigorously structured off-chain compliant trust fund architecture. By formalizing dividends and liquidation rights through contractual realization, this design, while unable to bypass regulatory friction, maximally preserves a legal claim for holders within traditional financial courts. It is currently the best solution for this model to counter the legal vacuum.

On-Chain Financial Clearing Giant: Alpaca's Single-Point Monopoly and Liquidity Gaps

In the current five-layer architecture, if one were to dissect all the pipes of Tokenized US stocks and Traditional API trading products, a startling fact emerges: almost the entire crypto industry's underground network access to US stocks converges at a single point in the core execution and custody layer – Alpaca.

Whether it's the on-chain RWA-focused Ondo Finance, Backed Finance (xStocks), the exchange-backed Bitget Reality, or even Binance's traditional US stock trading launched in June, the underlying asset buying, clearing, and securities custody are all independently handled by Alpaca. According to an official announcement by Alpaca on December 4, 2025, Alpaca actually monopolizes over 94% of the clearing and custody market share for tokenized US stocks and ETFs (Source: Alpaca Official).

Why Alpaca: Self-Clearing Qualifications and Traditional Brokers' "Risk Aversion"

This highly concentrated single-point monopoly is not because Alpaca provides absolutely irreplaceable cutting-edge Web3 technology. It is determined by the extreme scarcity in the traditional financial supply and the inherent compliance gap.

Within the US securities system, brokers have a very strict hierarchy. One category is the large number of "Introducing Brokers," which can only take orders and must outsource clearing, settlement, and custody to third parties. The other category is the very few "Self-Clearing Brokers." Alpaca belongs to the latter. It is a formal member of DTCC, OCC, and FICC and can independently complete the entire chain from order execution to final asset registration. For crypto asset issuers, accessing Alpaca means they don't need to separately connect to different execution, clearing, and custody institutions; one broker provides the full-service chain.

Alpaca's core barrier lies in the unwillingness of other traditional large licensed institutions to cooperate with offshore crypto exchanges due to compliance and reputational risk concerns. Giants like Interactive Brokers, with market capitalizations in the tens of billions and immense reputational capital, would never risk regulatory backlash for a small API access fee by partnering with an exchange registered