CLARITY 法案如何重塑穩定幣收益經濟

- 核心觀點:美國CLARITY法案通過參議院銀行委員會,將穩定幣收益禁令擴展至所有數位資產服務提供商,並引入「被動收益vs活動性獎勵」的法律二分法,強制行業從「持有付息」轉向「使用付息」。華爾街資管巨頭(摩根士丹利、貝萊德、摩根大通)同步佈局代幣化貨幣市場基金,以此卡位成為新範式下最穩健的合規收益基礎設施。

- 關鍵要素:

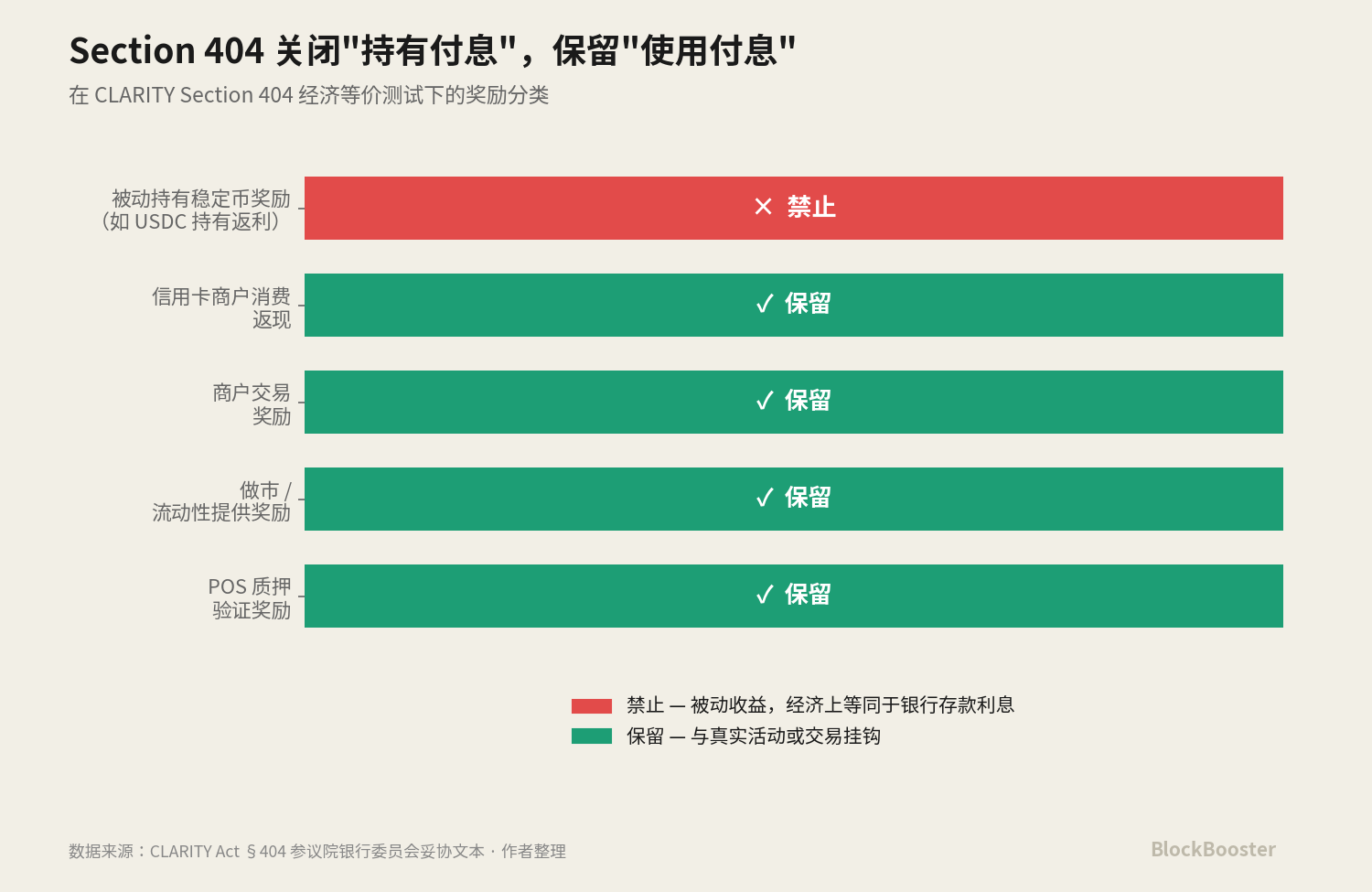

- CLARITY法案Section 404做了兩件關鍵事:將收益禁令從穩定幣發行人擴展至交易所、託管商等所有DASPs及其關聯方;引入「被動收益」與「活動性獎勵」的二分法,禁止僅基於持有的利息,但保留基於質押、交易等真實活動的獎勵。

- 該法案關閉了Coinbase透過訂閱模式、Anchorage透過關聯實體等「間接付息」的合規繞道,迫使行業重構收益模型。

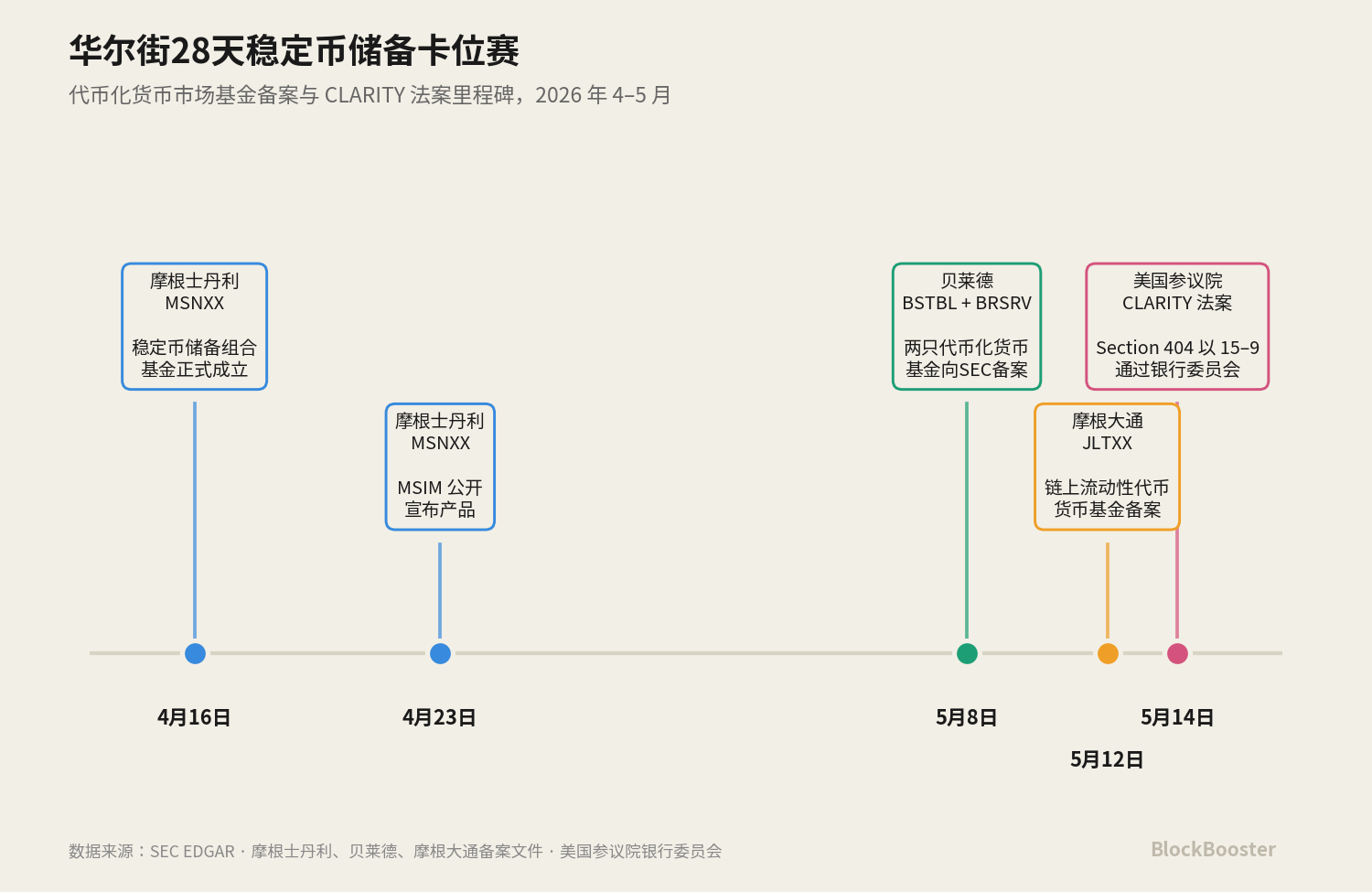

- 在法案通過前28天內,摩根士丹利(MSNXX)、貝萊德(BSTBL/BRSRV)、摩根大通(JLTXX)幾乎同步備案了專為穩定幣儲備需求設計的代幣化貨幣市場基金,表明市場預期已按新範式重組產業。

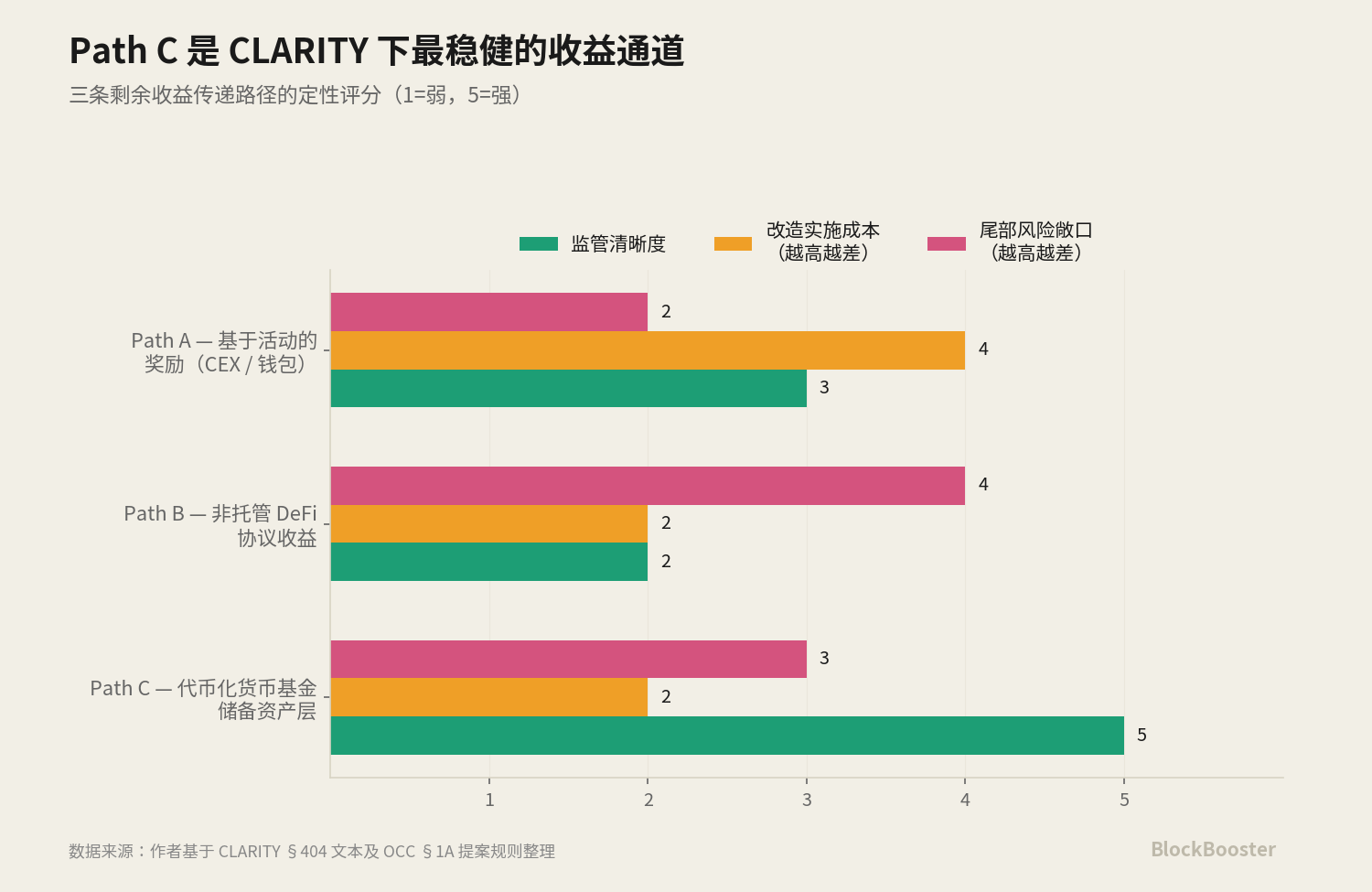

- 新範式下,收益傳遞有三條路徑:路徑A(交易所重新設計活動獎勵)、路徑B(DeFi協議層的非託管收益),以及路徑C(代幣化貨幣市場基金作為儲備資產付息),其中路徑C受監管直接威脅最小、風險調整後吸引力最強。

- OCC提出的「代幣化儲備資產占比20%上限」提案是決定路徑C能否規模化的關鍵博弈,CLARITY法案賦予代幣化證券法律地位,削弱了OCC的限制理由,上限可能被放寬。

- 貝萊德已建構三層次產品矩陣(BUIDL、BSTBL、BRSRV),覆蓋DeFi抵押品、傳統機構現金管理和穩定幣儲備資產,形成完整生態系統。

- BUIDL的集中度風險突出:其單一基金支撐了USDtb約90%儲備及JupUSD約81%儲備,若OCC上限放寬,此類單點故障風險將被放大,可能引發系統性風險。

Original Author: @BlazingKevin_, Blockbooster Researcher

On May 14, 2026, the U.S. Senate Banking Committee passed the CLARITY Act with a bipartisan vote of 15-9.

The most important content in this "legislative progress" is Section 404 of the bill text. This section, redrafted by Senators Thom Tillis and Angela Alsobrooks in a compromise text released on May 1, accomplishes two things that the GENIUS Act did not:

First, it expands the stablecoin yield prohibition to all Digital Asset Service Providers (DASPs) and their affiliates—including centralized exchanges, brokers, dealers, and custodians. When the GENIUS Act was signed in July 2025, it only applied to "stablecoin issuers" (PPSI/FPSI). All compliance workarounds by Coinbase, Anchorage Digital Neo Ltd., etc., which paid users 3.5%-5% yield via the "non-issuer interest payment" route, are closed off by Section 404.

Second, it explicitly introduces a legal dichotomy of "passive yield vs. activity-based rewards." Section 404 prohibits rewards that are "functionally or economically equivalent to bank deposit interest"—i.e., automatically accrued yield solely based on holding—but preserves rewards "based on genuine activities or transactions," such as staking, market making, credit card cashback, and merchant transaction rewards.

Together, these two changes constitute a paradigm shift. The stablecoin industry is moving from a market where interest is paid for holding to a market where interest is paid for using.

Meanwhile, over the past month, Wall Street's three largest asset managers (Morgan Stanley, BlackRock, JPMorgan) have almost simultaneously launched money market fund products tailored for stablecoin reserve requirements. Morgan Stanley's MSNXX was established on April 16 and publicly announced on April 23; BlackRock filed registration statements for two tokenized funds, BSTBL and BRSRV, on May 8; JPMorgan filed for JLTXX on May 12. Three firms launched highly similar products within a 28-day window.

This timing is certainly no coincidence. We believe: The expectation that CLARITY Section 404 will pass is pushing the stablecoin yield economy towards a new paradigm—the hold-to-earn path is being narrowed, the use-to-earn path is preserved, and tokenized money market funds, serving as a compliant yield-bearing instrument for stablecoin reserves, become the most robustly benefiting compliant yield layer in this new paradigm.

The products filed by Wall Street asset management giants in April-May represent an industrial positioning for this paradigm shift. It's important to clarify: CLARITY has only passed the Senate Banking Committee and is still far from the President's signature, but market expectations are already reorganizing in this direction.

This article will start by reconstructing the timeline, deconstructing the relay legal structure of GENIUS and CLARITY, and analyzing why the tokenized reserve asset layer becomes the most robust compliant yield channel in the new paradigm.

1. Industrial Positioning in 30 Days

1.1 April 16: Morgan Stanley's Opening Move

Let's go back to the earliest event.

On April 16, 2026, Morgan Stanley's Stablecoin Reserves Portfolio (ticker: MSNXX) was officially established.

MSIM publicly announced this product on April 23.

The product positioning of MSNXX was very precise. The official statement read: "The Fund provides compliant stablecoin issuers with a qualified money market fund option for investing reserve assets backing their outstanding stablecoins."

MSNXX is a product tailored specifically for reserve asset requirements—investing in cash, U.S. Treasuries with maturities under 93 days, and overnight repurchase agreements collateralized by Treasuries.

However, MSNXX is not a tokenized product and does not trade on-chain. Morgan Stanley's product strategy was conservative—offering only a traditional MMF wrapper for stablecoin issuers to invest through traditional financial channels.

This was the first publicly announced product "specifically designed for stablecoin reserve needs" among Wall Street asset management giants. It wasn't revolutionary in itself, but it sent a clear signal: stablecoin reserve demand has grown large enough for asset managers to dedicate a specific fund to it.

1.2 May 8: BlackRock's "Dual Filing"

22 days later, BlackRock submitted two registration statements to the SEC simultaneously: the BlackRock Select Treasury Based Liquidity Fund tokenized version (BSTBL) and the BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV).

The design of these two products contrasts sharply with MSNXX. BSTBL is a tokenized share class of BlackRock's existing Select Treasury Based Liquidity Fund. It serves traditional institutional cash managers—clients who already invest in this fund, now with an additional on-chain distribution channel.

BRSRV is a newly created tokenized money market fund, distributed on multiple chains via Securitize, targeting a single customer group: stablecoin issuers.

The key difference between BlackRock and Morgan Stanley lies in tokenization. BlackRock chose to issue on-chain shares of the same underlying assets (short-term Treasuries + cash + overnight repos) to stablecoin issuers, granting the reserve assets themselves on-chain composability, 24/7 liquidity, and the potential for integration with DeFi protocols. This is a product form tailored for crypto-native clients like Ethena and Jupiter.

The BSTBL + BRSRV filing expands BlackRock's existing product matrix, extending the tokenization infrastructure from BUIDL's "DeFi collateral" use case to BRSRV's "stablecoin reserve asset" use case.

1.3 May 12: JPMorgan's Second Entry

Four days later, JPMorgan filed the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX) with the SEC.

The fund invests in U.S. Treasuries and overnight repos collateralized by Treasuries or cash, with underlying assets identical to BUIDL, BSTBL, and BRSRV. The Token Class Shares were dated May 13.

JLTXX is not JPMorgan's first on-chain MMF. As early as December 15, 2025, JPMorgan Asset Management launched the My OnChain Net Yield Fund (MONY) on Ethereum. MONY is a 506(c) private fund, only available to qualified investors.

This means JPMorgan has nearly 5 months of operational experience in the tokenized MMF space. JLTXX is not a catch-up product but the second step in JPMorgan's on-chain MMF strategy—expanding a product previously restricted to 506(c) qualified investors into a registered fund for a broader client base, specifically targeting the stablecoin reserve use case.

On one hand, JPMorgan, alongside Bank of America, Wells Fargo, and Citigroup, explored issuing a joint syndicated stablecoin in 2025. On the other hand, it deeply positioned itself in the tokenized reserve asset track through the MONY → JLTXX product matrix. Regardless of the OCC's final ruling, JPMorgan has a product in place—this "betting on both sides" represents the unique strategic space available to JPMorgan as both a GSIB bank and an asset management company.

1.4 May 14: The CLARITY Act Stamps the Entire Track

On May 14, the Senate Banking Committee passed the CLARITY Act with a bipartisan vote of 15-9.

It's worth noting carefully: Morgan Stanley's MSNXX, BlackRock's BSTBL/BRSRV, and JPMorgan's JLTXX—these products were all prepared before the compromise text of CLARITY Section 404 was made public.

In fact, since CLARITY was first shelved in January 2026, the asset management industry has been clear on two things: First, the "hold-to-earn" stablecoin reward path would eventually be closed. Second, stablecoin reserve assets must exist, must be compliant, and will inevitably yield interest.

Putting these two together: When the hold-to-earn path is narrowed, one of the most robust "indirect yield" transmission paths is through the reserve asset layer—the stablecoin issuer itself doesn't pay yield, but its reserve's tokenized money market fund legally pays yield to the issuer, who then decides how to pass this yield to users within the compliance framework.

The products from asset management giants are the infrastructure prepared for this "most robust compliant yield channel."

2. Why CLARITY is Much More Important Than GENIUS

2.1 The Limited Scope of the GENIUS Act

To understand the paradigm-shifting effect of Section 404, one must first precisely understand what it expands upon—GENIUS Act 4(a)(11).

The GENIUS Act, signed into law in July 2025, stipulates: A qualified stablecoin issuer or foreign stablecoin issuer shall not pay any form of interest or yield to stablecoin holders.

That is, the GENIUS Act itself does not distinguish between "passive yield" and "activity-based rewards"—any form of interest or yield paid by the issuer to the holder is prohibited.

Second, its binding target is only the issuer itself, not third parties like exchanges, wallets, custodians, or affiliates.

This second limitation created a regulatory loophole—the industry dubbed it "pass-through evasion." Throughout 2025-2026, the stablecoin industry essentially sought compliant innovation space within this loophole:

- Coinbase / Kraken Model: Exchanges distribute rewards. USDC is issued by Circle, but Coinbase pays approximately 4% rewards to USDC holders via the Coinbase One subscription model.

- Gemini Credit Card Model: Rewards triggered by external merchant transactions. GUSD is issued by Gemini Trust Company, but Gemini credit card holders receive GUSD cashback when spending at merchants.

- Anchorage Digital Neo Model: Payment via a separate affiliated legal entity. USDtb is issued by Anchorage Digital Bank, but Anchorage Digital Neo Ltd. (an independent legal entity) pays the rewards.

These three models collectively formed the "indirect yield" ecosystem of the GENIUS era.

However, the entire compliance basis for this was the limited scope of the GENIUS Act binding only the issuer.

2.2 The Substantive Expansion of CLARITY Section 404

CLARITY Act Section 404 does two things the GENIUS Act didn't.

First: Expanding to DASPs and Affiliates

The binding target of Section 404 is no longer limited to stablecoin issuers, extending to "covered digital asset service providers and their affiliates." This scope explicitly covers centralized exchanges, brokers, dealers, and custodians.

This expansion immediately closes all compliance paths like Coinbase, Kraken, Gemini, and Anchorage Digital Neo that used "non-issuer interest payments." Coinbase, as a DASP, can no longer distribute hold-only USDC rewards; Anchorage Digital Neo can no longer pay USDtb rewards.

Second: Introducing the "Passive vs. Active" Dichotomy

Section 404 prohibits DASPs from providing rewards that are "functionally or economically equivalent to bank deposit interest" but preserves rewards "based on genuine activities or transactions."

This means any reward linked to "consumption, trading, staking, or transfers" can survive, while any reward that grows linearly with idle balances cannot.

Together, these two things constitute a complete paradigm shift. All "indirect yield" templates of the GENIUS era are either closed or need redesign in the CLARITY era.

The stablecoin industry is moving from a market where interest is paid for holding to a market where interest is paid for using.

2.3 Winning Paths in the Paradigm Shift

Under the use-to-earn paradigm, there are three possible paths for passing yield to users.

Path A: Redesign Rewards as Activity-Based Rewards

Applicable to: Exchanges, wallets, credit cards. Coinbase could change USDC rewards from "yield for holding" to "based on trading frequency/spending amount." Gemini is already using the credit card cashback model.

The key issue with Path A is not whether it can retain users, but its design costs—Coinbase would need to restructure the entire legal framework and product UI of its reward system. Every active design would need to pass the SEC/CFTC's factual test. This restructuring could take 6-12 months, during which user churn is a real risk. However, in the medium term, Path A could potentially recover and even surpass the appeal of the hold-to-earn era.

Path B: Keep Yield at the Protocol Layer, Pass it to Users via Activity-Based Operations

Applicable to: DeFi protocols. The "covered digital asset service provider" definition in Section 404 is clearly built around centralized intermediaries—yield generated by non-custodial smart contracts, e.g., supplying USDC to Aave for variable rate lending, falls outside this definition according to its design.

This means users depositing USDC into the Aave lending pool to earn variable interest is, under most legal scholars' current interpretations, compliant—CLARITY seemingly unintentionally leaves a yield channel open for non-custodial DeFi.

However, this exemption carries significant uncertainty. If final rules extend the "economically equivalent" concept to non-custodial DeFi, or define DeFi frontends as affiliates, the exemption for Path B could be substantially narrowed.

Path C: Pay Yield Through the Reserve Asset Layer

This is the path Wall Street asset management giants are betting on. Specific mechanism: The stablecoin issuer itself doesn't pay yield, DASPs don't pay yield, but the stablecoin's reserve assets are tokenized money market funds that legally pay yield to their holders (i.e., the stablecoin issuer). The stablecoin issuer then retains the distributed yield as company profit—or partially passes it to users via designed active behavior rewards.

The key compliance advantage of this path: Its yield layer is not at the stablecoin layer or the DASP layer, but at the underlying fund layer—unrelated to the stablecoin regulatory framework.

These three paths are not mutually exclusive; they will evolve simultaneously.

Path A may find new life in the hands of players like Coinbase with retail brands and distribution channels;

Path B may receive an unexpected tailwind for protocols like Aave and Pendle (albeit with tail risk of regulatory tightening over the next 12 months);

Path C is the path least directly threatened by Section 404, but requires the OCC's 20% cap not being passed as a prerequisite.

Path C is the "most robustly benefiting" compliant yield layer, but not the "only benefiting" one.

This is precisely why Wall Street asset management giants filed for tokenized money market funds in April-May. They are preparing one piece of compliant yield infrastructure for the use-to-earn paradigm that CLARITY Section 404 is set to define. Considering the implementation costs and regulatory uncertainties of Paths A and B, Path C offers the strongest risk-adjusted appeal—this is the industrial judgment of firms like BlackRock.

2.4 The Collaborative Relationship Between Path B and Path C

There seems to be potential for collaboration between Path B and Path C. A complete on-chain yield system could utilize both paths simultaneously:

- The reserve asset layer uses BUIDL—ensuring a source of compliant yield

- The user layer uses Aave lending or Pendle yield splitting—ensuring the "yield" users perceive comes from active operations

This dual-layer structure of "BUIDL at the base, DeFi protocols on the surface" could theoretically build a use-to-earn system that is both compliant and user-friendly. BlackRock likely didn't specifically foresee Section 404 when launching BUIDL, but this product perfectly positions itself as the best underlying layer for a use-to-earn system under the new paradigm.

3. BlackRock's Three-Layer Product Matrix—Infrastructure Built for the New Paradigm

3.1 Three Products, Three Customer Bases

To understand BlackRock's strategy, one must compare its three tokenized fund products simultaneously:

BUIDL: Launched March 2024, natively built on Ethereum. Legal structure is a BVI fund, custody provided by Securitize.

Target Customer: DeFi protocols, crypto-native institutions, on-chain scenarios needing BUIDL as collateral. Accepted as qualified collateral on lending protocols like Aave, with a minimum investment of $5 million.

BST