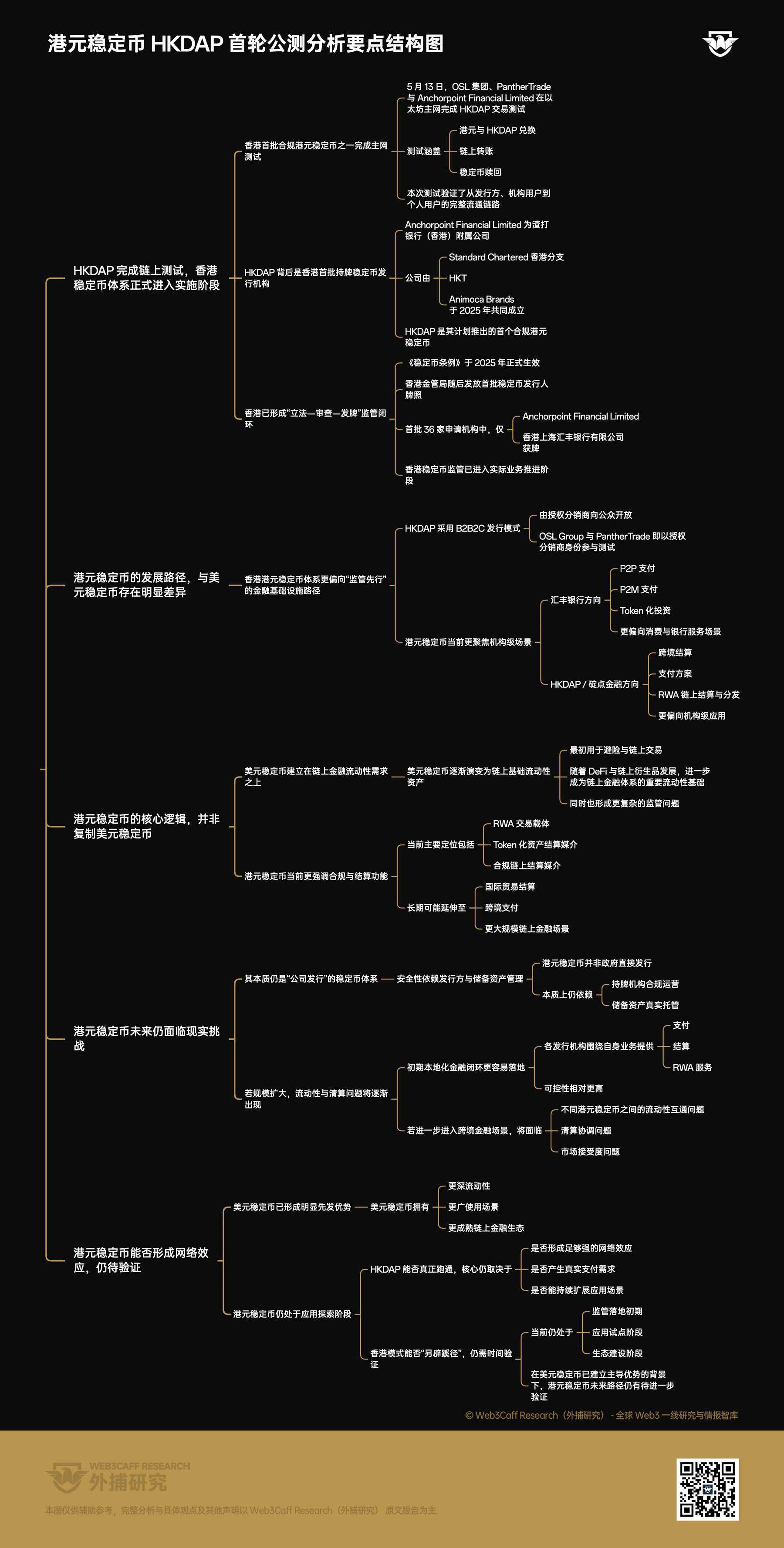

港元穩定幣 HKDAP 完成首輪公測,合規穩定幣能否在美元主導的賽道中另闢蹊徑?

- 核心觀點:香港首批持牌穩定幣發行人碇點金融科技已完成港元穩定幣 HKDAP 在以太坊主網的交易測試,標誌香港穩定幣監管進入實施階段。HKDAP 定位於機構級應用,側重跨境結算與 RWA 交易,與美元穩定幣形成差異化發展路徑。

- 關鍵要素:

- 碇點金融由渣打香港、香港電訊及 Animoca Brands 合資成立,於 2025 年 4 月獲香港金管局首批穩定幣發行人牌照(共 2 張),計劃第二季度起分階段發行 HKDAP。

- 測試由 OSL 集團和 PantherTrade 作為授權分銷商參與,驗證了從發行商到機構用戶再到個人用戶的完整兌換、轉帳及贖回流動鏈路。

- HKDAP 採用「B2B2C」發行模式,即面向授權分銷商分銷後由後者向公眾開放,重點場景為跨境結算與支付及現實世界資產(RWA)鏈上結算。

- 另一獲牌方匯豐銀行計劃下半年推出港元穩定幣,初期聚焦個人對個人(P2P)付款、個人對商戶(P2M)支付及代幣化投資,偏向消費與銀行場景。

- 港元穩定幣與美元穩定幣定位差異明顯:後者源於鏈上金融避險與流動性需求,前者則更審慎地作為「監管先行」的金融基礎設施,主攻 RWA 交易與合規結算媒介。

- 港元穩定幣面臨挑戰:安全性高度依賴發行方合規運營與儲備託管,未來若進入國際貿易結算等大型場景,需解決不同穩定幣間流動性互通、清算協調及市場接受度問題。

Original Author: ShirleyLi, Researcher at Web3Caff Research

How to easily grasp the ongoing market hotspots, technological trends, ecosystem developments, and governance situations in the Web3 industry? The "Market Pulse Analysis" column launched by Web3Caff Research delves into the front lines to screen current hot events, providing value interpretation, commentary, and principle analysis. Seeing through the appearance to perceive the essence, follow us now to quickly capture the front-line market trends of Web3.

Compliance Reminder: The following content is solely an objective analysis of the formation characteristics and development status of the Hong Kong dollar stablecoin HKDAP, and does not constitute any proposal or offer. Please be aware that the issuance and investment in Tokens are subject to varying degrees of strict regulatory requirements and restrictions in different countries and regions. In particular, issuing Tokens in Mainland China may constitute "illegal issuance of securities," and providing services related to cryptocurrency transactions, such as token trading matching, is also considered "illegal financial activity" (Mainland Chinese readers are strongly advised to read "Compilation and Key Points of Laws and Regulations Related to Blockchain and Virtual Currencies in Mainland China"). Therefore, please do not make any decisions based on this information, and strictly comply with the laws and regulations of your country or region, refraining from any illegal financial activities.

On May 13, OSL Group, a stablecoin payment and trading platform, and PantherTrade, a virtual asset trading platform under Futu Holdings, together with Anchorpoint Financial Limited, a licensed stablecoin issuer in Hong Kong, successfully completed a transaction test on the Ethereum mainnet using the Hong Kong dollar stablecoin HKDAP as the settlement medium. This test covered the exchange between fiat HKD and HKDAP, on-chain transfers, and redemption processes.

Anchorpoint Financial Limited is a subsidiary of Standard Chartered Bank (Hong Kong) Limited, jointly established by Standard Chartered Hong Kong, Hong Kong Telecom, and Animoca Brands in February 2025. HKDAP (Hong Kong Dollar Anchor Point) is its planned first compliant Hong Kong dollar stablecoin.

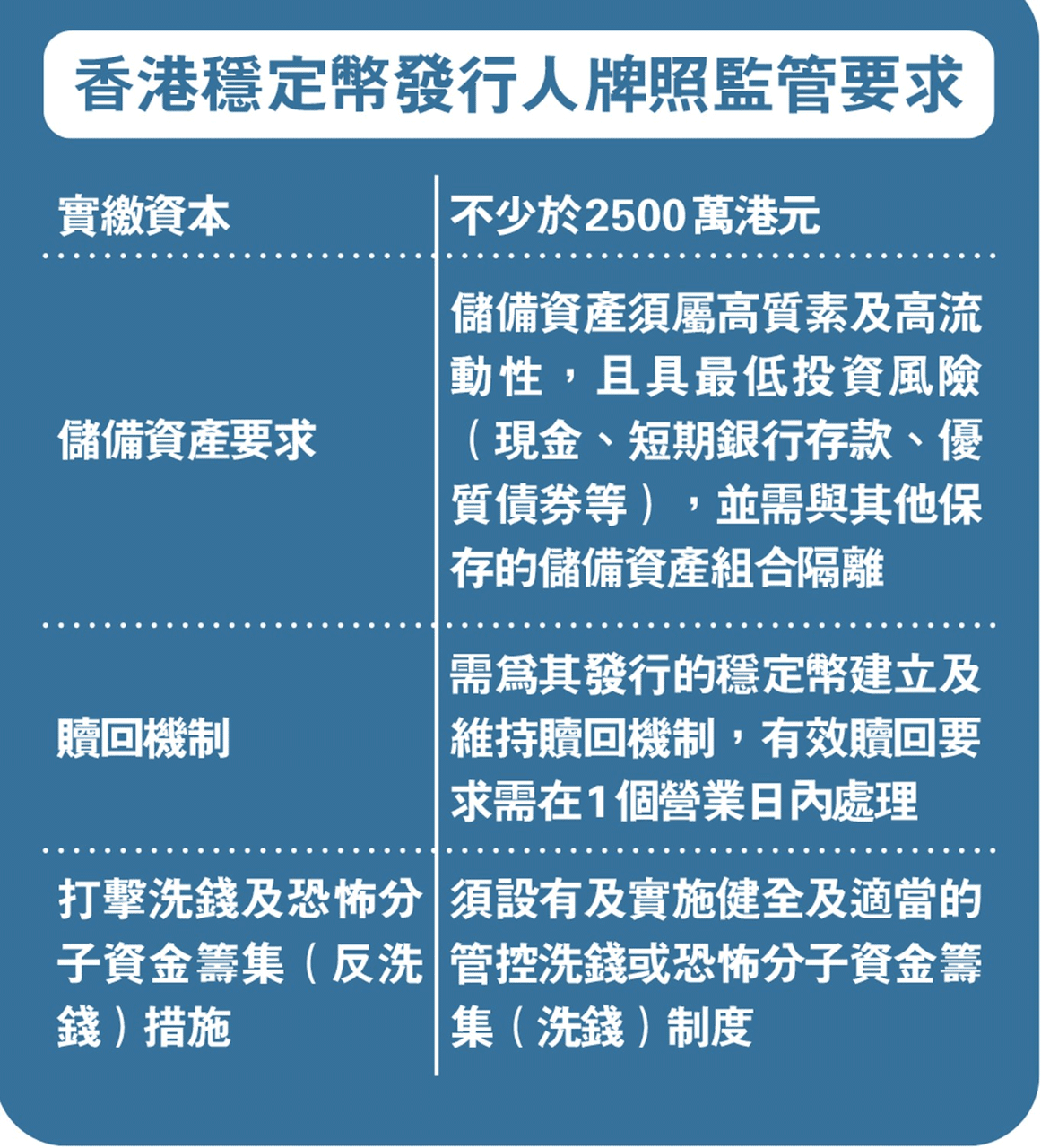

On August 1, 2025, Hong Kong's "Stablecoin Ordinance" officially came into effect, providing a relatively clear regulatory framework for the issuance and operation of stablecoins (Extended reading: "Hong Kong Passes the Stablecoin Ordinance Bill: What Impetus Will It Provide for Global Stablecoin Compliance and the RMB Internationalization Strategy?"). In April this year, the Hong Kong Monetary Authority, based on this ordinance, officially granted the first batch of 2 stablecoin issuer licenses. It is reported that a total of 36 institutions submitted applications in the first batch, but only Anchorpoint Financial Limited and The Hongkong and Shanghai Banking Corporation Limited (HSBC) were granted licenses. This licensing action is considered to have completed the "legislation-review-licensing" regulatory loop, pushing stablecoin regulation into the implementation and business preparation phase. [1]

Image Source: HSBC and Standard Chartered Affiliates Licensed, First to Launch Hong Kong Dollar Stablecoin

Among them, Anchorpoint Financial plans to issue the Hong Kong dollar-pegged stablecoin "HKDAP" in phases starting from the second quarter of this year, adopting a "B2B2C (Business to Business to Consumer)" distribution model. This involves distributing to designated authorized distributors, who then make it available to the public. In the test mentioned at the beginning of this article, OSL Group and PantherTrade, acting as authorized distributors of HKDAP, verified the complete circulation chain from the issuer to institutional users and then to individual users.

HSBC, on the other hand, plans to launch its own Hong Kong dollar stablecoin in the second half of this year and integrate it into its PayMe platform and HSBC Hong Kong mobile banking application.

In terms of pilot direction, the focus of the two institutions differs slightly. HSBC plans to initially launch services such as peer-to-peer (P2P) payments, person-to-merchant (P2M) payments, and tokenized investments. In other words, HSBC will lean towards scenarios related to general consumer and banking services. Anchorpoint Financial's focus will include cross-border settlement and payment solutions, as well as on-chain settlement and distribution of RWA (Real World Assets), primarily targeting institutional-grade application scenarios.

From a macro perspective, although both belong to the stablecoin system, Hong Kong dollar stablecoins and the currently dominant US dollar stablecoins exhibit significant differences in their development paths and potential positioning. The underlying reason lies in the different market environments and core needs from which they emerged.

In the early stages of Web3 industry development, the core function of US dollar stablecoins was to provide a safe-haven tool for highly volatile assets and serve as a medium for on-chain transactions. Subsequently, with the development of decentralized finance, on-chain derivatives, and other markets, US dollar stablecoins further became the foundational liquidity asset within the entire on-chain financial system. This highly financialized and globalized liquidity structure has also made the regulatory landscape for the US dollar stablecoin system more complex.

In contrast, Hong Kong's current positioning for Hong Kong dollar stablecoins is noticeably more prudent, leaning towards a "regulation-first" financial infrastructure path. Currently, Hong Kong dollar stablecoins are primarily positioned as carriers for RWA transactions, serving as a trustworthy, stable, and compliant on-chain settlement medium for tokenized assets. From a longer-term perspective, the potential future direction for Hong Kong dollar stablecoins may not be limited to the ongoing pilot areas like RWA transactions and merchant settlement, but could extend to more challenging fields such as international trade settlement and cross-border payments.

However, unlike fiat currency systems backed by governments, Hong Kong dollar stablecoins are essentially stablecoin systems issued by licensed companies and pegged to the fiat Hong Kong dollar. Therefore, their security is highly dependent on the compliant operations of the issuer and the true custodial status of the reserve assets.

If individual licensed issuers only launch payment, settlement, and RWA services around their own business, this relatively localized small financial loop is more controllable and feasible in the early stages. However, if Hong Kong dollar stablecoins further enter international trade settlement, cross-border payments, and larger-scale on-chain financial scenarios in the future, issues such as liquidity interoperability between different Hong Kong dollar stablecoins, clearing coordination, and market acceptance will gradually emerge.

Furthermore, as mentioned earlier, Hong Kong dollar stablecoins and US dollar stablecoins differ in positioning. Although US dollar stablecoins face complex regulatory issues, they have consequently accumulated deeper liquidity and broader use cases, while Hong Kong dollar stablecoins are still in the phase of exploring practical application scenarios. This means that whether the Hong Kong dollar stablecoin system, including HKDAP, can truly succeed ultimately depends on whether it can form sufficiently strong network effects and generate enough real payment demand. Given the clear first-mover advantage established by US dollar stablecoins, time will tell whether the Hong Kong model can carve a new path.

Key Points Structure Diagram:

References

[2] HSBC and Standard Chartered Affiliates Licensed, First to Launch Hong Kong Dollar Stablecoin

[5] 3 Licensed Firms Test Hong Kong's HKDAP Stablecoin on Ethereum

Disclaimer

This report is prepared by Web3Caff Research. The information contained herein is for reference purposes only and does not constitute any forecast, investment advice, proposal, or offer. Investors should not rely on such information to purchase or sell any securities, cryptocurrencies, or adopt any investment strategies. The terminology used and the views expressed in this report are intended to help understand industry trends and promote the responsible development of Web3, including the blockchain industry. They should not be interpreted as definitive legal opinions or the views of Web3Caff Research. The views in this report reflect the personal opinions of the author as of the stated date, are independent of the position of Web3Caff Research, and may change with subsequent circumstances. The information and views contained in this report are derived from proprietary and non-proprietary sources deemed reliable by Web3Caff Research, but do not necessarily encompass all data, and their accuracy is not guaranteed. Therefore, Web3Caff Research makes no representation or warranty of any kind regarding their accuracy or reliability and assumes no responsibility for errors or omissions arising in any other manner (including liability to any person for negligence). This report may contain "forward-looking" information, which may include predictions and forecasts. This text does not constitute a guarantee of any forecast. Whether to rely on the information contained in this report is entirely at the reader's own discretion. This report is for reference only and does not constitute investment advice, a proposal, or an offer to buy or sell any securities, cryptocurrencies, or adopt any investment strategies. Please strictly comply with the relevant laws and regulations of your country or region.