Tokenized Funds Open for Secondary Market Circulation! How is the Hong Kong SFC's New Policy Driving Global On-Chain Financial Development?

- Core Viewpoint: Through the "Stablecoin Ordinance" and the SFC's new framework, Hong Kong has taken the lead in providing compliant secondary circulation channels for RWA (Real World Asset Tokenization) products, promoting the implementation of on-chain financial markets. Its progress is ahead of major economies such as the U.S. and Europe in terms of speed and execution.

- Key Elements:

- On April 20, 2026, Hong Kong issued new regulations, allowing for the first time SFC-recognized tokenized investment products to be traded on the secondary market on licensed platforms, granting them financial product attributes.

- As of the end of March 2026, Hong Kong has offered 13 types of tokenized products to the public, with total assets under management reaching HK$10.7 billion, an increase of approximately seven times year-on-year.

- The Hong Kong Monetary Authority (HKMA) has issued stablecoin issuer licenses to Dingdian Fintech and HSBC, providing a compliant foundation for RWA settlement.

- The Digital Currency Institute of the People's Bank of China and the HKMA jointly tested real-time exchange between e-CNY and stablecoins, reducing cross-border transaction time from 2 hours to 3 minutes and lowering costs by over 20%.

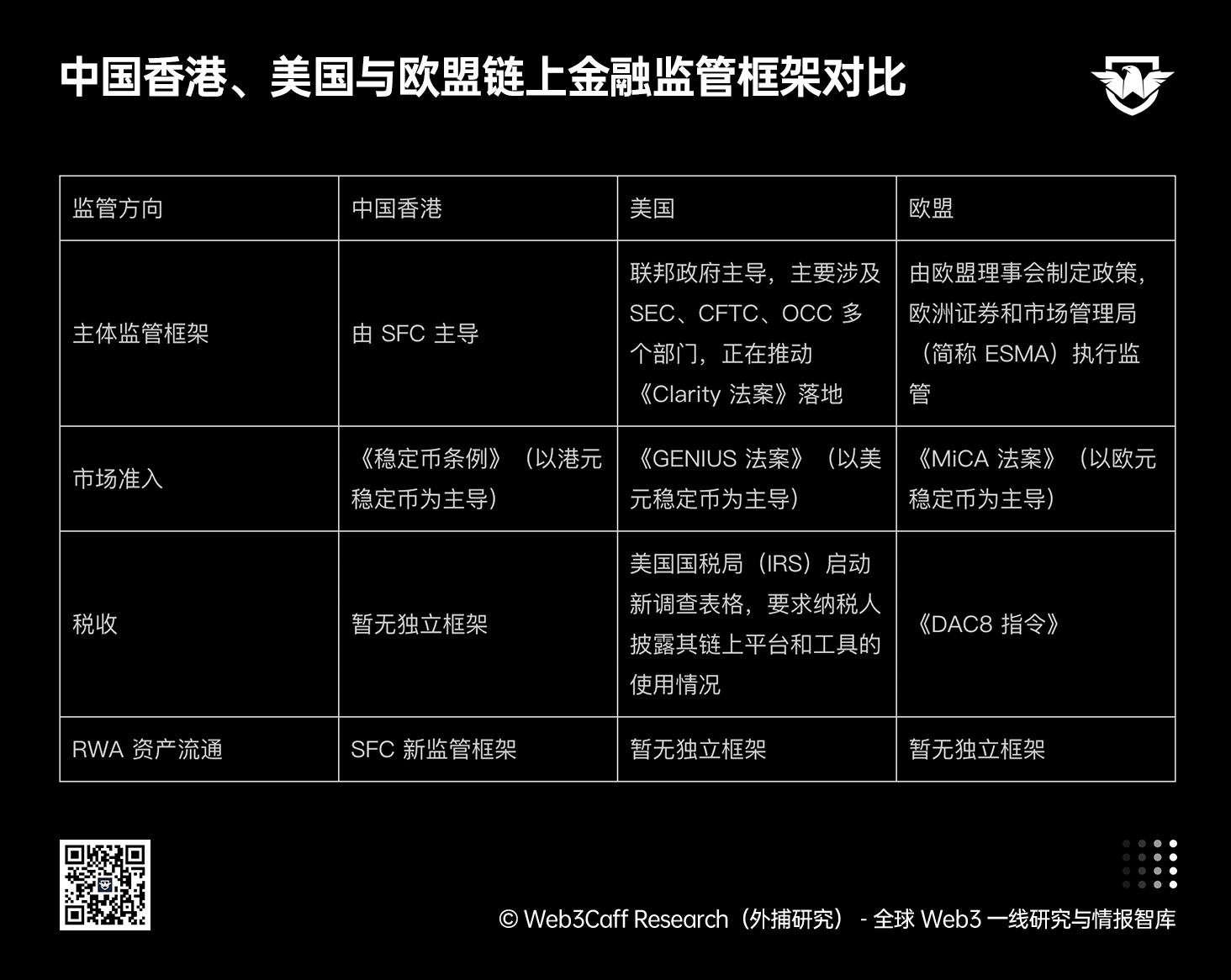

- A joint statement by the U.S. SEC and CFTC clarified that tokenized assets fall under the category of securities and classified five types of assets; the EU's MiCA regulation came into effect in December 2024, providing unified licensing and market access rules.

- Regulatory practices in the U.S. and the EU (such as discontent from banks over the OCC's licensing, and the risk of regulatory arbitrage in cross-border operations under MiCA) serve as warnings for Hong Kong, which needs to balance inter-institutional compliance costs and risk monitoring.

Original Author: ShirleyLi, Researcher at Web3Caff Research

Compliance Note: The following content is solely an objective analysis of the latest regulatory strategies in Hong Kong SAR, China, and globally in areas such as RWA and stablecoins. It does not constitute any proposal or offer. Please be aware that issuing or participating in the investment of Tokens is subject to varying degrees of stringent regulatory requirements and restrictions in different countries and regions. In particular, issuing Tokens in Mainland China may constitute "illegal issuance of securities," and providing cryptocurrency trading services like token matching also falls under "illegal financial activities." (Mainland Chinese readers are strongly advised to read the Compilation and Key Points of Laws and Regulations Related to Blockchain and Virtual Currencies in Mainland China). Therefore, please do not use this information for any related decisions, strictly comply with the laws and regulations of your country and region, and refrain from participating in any illegal financial activities.

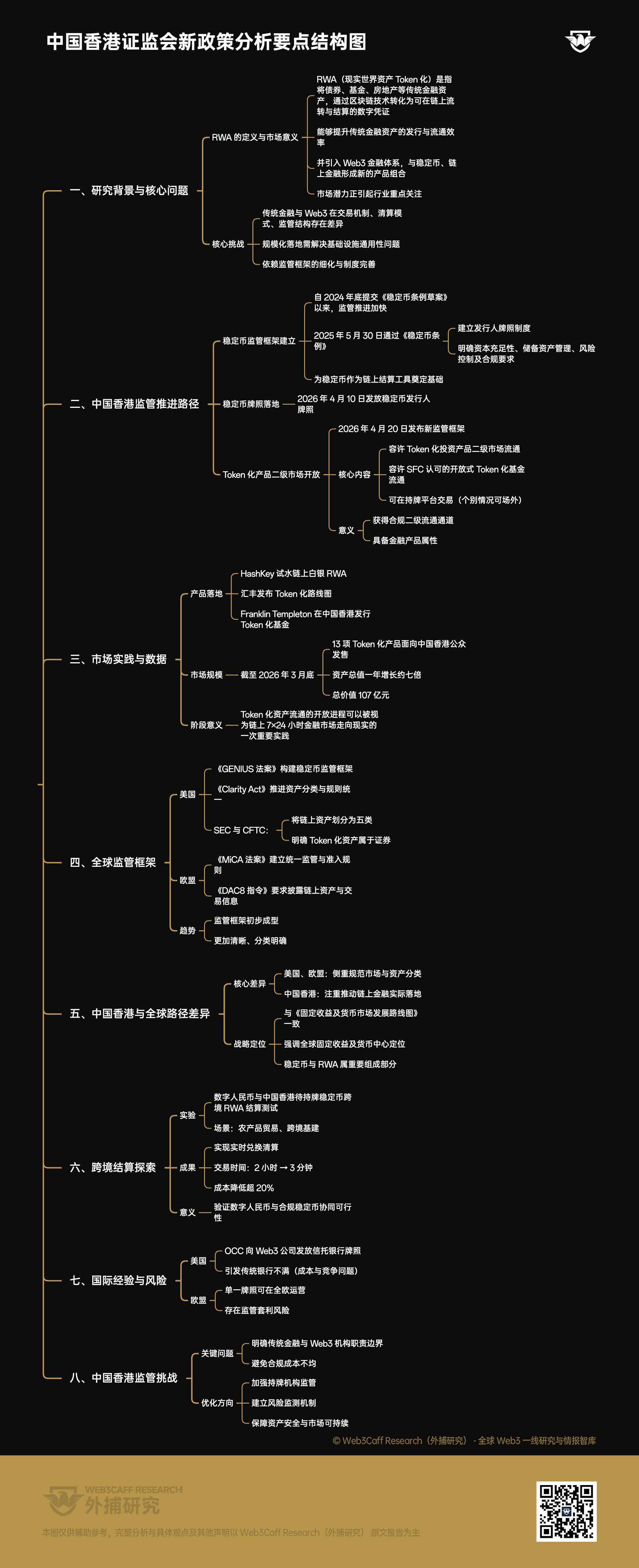

RWA (Real World Assets Tokenization) refers to the process of converting traditional financial assets such as bonds, funds, and real estate into digital certificates that can be circulated and settled on-chain using blockchain technology. This mechanism not only provides more efficient issuance and circulation paths for traditional financial assets but also introduces these assets into the Web3 financial system, forming new product combinations with stablecoins and on-chain finance. Consequently, the market potential inherent in the RWA track is attracting significant attention from industry participants.

However, significant differences exist between traditional and Web3 financial systems regarding trading mechanisms, clearing models, and regulatory structures. This implies that the large-scale implementation of RWA requires not only solving interoperability issues at the infrastructure level but also heavily depends on the refinement of regulatory frameworks and the improvement of institutional norms.

Against this backdrop, the overall pace of regulatory advancement in Hong Kong SAR, China, has been noticeably accelerating since the submission of the "Stablecoins Ordinance Bill" at the end of 2024.

On May 30, 2025, Hong Kong SAR, China, officially passed the "Stablecoins Ordinance," establishing a clear regulatory framework for the issuance and operation of stablecoins. This framework, on one hand, establishes a licensing system for stablecoin issuers, and on the other hand, imposes systematic requirements on licensed institutions regarding capital adequacy, reserve asset management, risk control, and operational compliance, laying the regulatory foundation for stablecoins to become credible settlement tools for on-chain transactions (Further reading: Hong Kong Passes the Stablecoins Ordinance Bill: What Impetus Will It Provide for Global Stablecoin Compliance and the Internationalization Strategy of the RMB?).

On April 10, 2026, the Hong Kong Monetary Authority (HKMA) granted stablecoin issuer licenses to Anchor Finance Technology Limited and The Hongkong and Shanghai Banking Corporation Limited under the Stablecoins Ordinance. [1]

On April 20, 2026, the Securities and Futures Commission of Hong Kong SAR, China (SFC) further released a new regulatory framework, explicitly allowing for the first time the secondary market circulation of tokenized investment products. The core direction of this framework is to permit the circulation of open-ended tokenized funds recognized by the SFC and allow related products to be traded on platforms licensed by the SFC (with over-the-counter forms potentially open in specific cases). This means that tokenized products recognized by the SFC have, for the first time, obtained a compliant secondary circulation channel, signifying they now possess the attributes of financial products.

At the product level, Hong Kong SAR Legislative Council Member Duncan Chiu mentioned in his speech at the 2026 Hong Kong Web3 Carnival that HashKey has piloted on-chain silver RWA tokens, HSBC has released a tokenization business roadmap, and institutions like Franklin Templeton have also issued tokenized funds in Hong Kong. [2] Furthermore, according to SFC disclosures, as of the end of March 2026, 13 tokenized products had been offered to the public in Hong Kong. The total value of assets managed by these tokenized products grew approximately sevenfold over the past year, reaching a total value of HKD 10.7 billion, indicating rapidly increasing market acceptance. [3] Judging from these data changes, the opening of circulation for tokenized assets can also be seen as a significant practical step towards realizing a 24/7 on-chain financial market.

Globally, relevant regulatory systems in the United States and the European Union are also gradually becoming clearer.

In the United States, the "Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025" (GENIUS Act) was officially signed in July 2025. This act aims to establish a comprehensive framework for stablecoin issuance and regulation, clearly defining requirements for issuer qualifications, asset reserves, and compliance standards. Meanwhile, the "Digital Asset Market Clarity Act" (Clarity Act) is currently under Senate review, aiming to provide standardized market guidance through unified on-chain asset classification and regulatory rules. (Further reading: 'GENIUS Stablecoin Act' Passes US Senate: What Major Changes Await Web3 and RWA?, US 'CLARITY Act' Under Review: Are DeFi-Friendly Policies, Asset Classification, and SEC-CFTC Power-Sharing Becoming a Turning Point for Crypto Regulatory Clarity?)

In March 2026, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) issued a joint statement classifying on-chain assets into five types: Digital Commodities (Cryptocommodities), Digital Collectibles (NFTs), Utility Tokens, Payment Tokens (Stablecoins), and Digital Securities. The statement explicitly classifies tokenized assets under the securities category. This provides a reference for further defining the regulatory boundaries of various asset types.

In the European Union, the "Markets in Crypto-Assets Regulation" (MiCA) came into effect in December 2024. By establishing a unified regulatory framework, MiCA provides clear licensing systems and market access rules for businesses such as trading platforms, custodial services, and stablecoin issuers. The latest Digital Asset Tax Transparency Act (DAC8 Directive) also took effect on January 1, 2026, requiring on-chain asset service providers to disclose detailed user asset and transaction information to tax authorities of individual member states and share it. This means tax authorities can oversee the holding, trading, and transfer of Web3 assets in an open and transparent manner, similar to how they treat traditional Web2 bank accounts.

Thus, the regulatory frameworks for on-chain assets in major global economies have taken preliminary shape, showing a trend towards greater clarity and more specific classification.

Comparison of on-chain financial regulatory frameworks in Hong Kong SAR, China, the US, and the EU. Source: Self-made by ShirleyLi, Researcher at Web3Caff Research.

However, overall, the regulatory frameworks in the US and EU primarily focus on regulating the operation of on-chain financial markets, clarifying asset nature and classification, whereas Hong Kong SAR, China, places more emphasis on promoting the practical implementation of on-chain financial markets. This direction is highly consistent with the "Fixed Income and Currency Market Development Roadmap" previously released by the SFC and the HKMA. This roadmap emphasizes Hong Kong's strategic positioning as a "global fixed income and currency center," and the regulatory strategies related to stablecoin licenses, RWA asset issuance, and circulation naturally constitute a crucial part of Hong Kong's asset regulatory framework.

Notably, at the end of February this year, the Digital Currency Institute of the People's Bank of China and the Hong Kong Monetary Authority jointly launched a special test for cross-border RWA settlement using the digital RMB (e-CNY). This test, using agricultural trade and cross-border infrastructure as a vehicle, verified the real-time exchange and clearing capability between the digital RMB and Hong Kong's pending licensed stablecoins (two companies have now received official licenses). It successfully reduced the time for traditional cross-border transactions from 2 hours to 3 minutes, achieving a cost reduction of over 20%. [4] This breakthrough further reveals the feasibility of the synergistic operation between the digital RMB and compliant stablecoins. (Further reading: Market Pulse Analysis: Decoding the 'Digital RMB International Operations Center' Signal for Cross-Strait Integration—Mainland Provides the Foundation, Hong Kong Provides the Market)

However, the regulatory practices in the US and EU also offer valuable lessons for Hong Kong. For example, the U.S. Office of the Comptroller of the Currency (OCC) granted trust bank charters to five Web3 companies, including Circle, Ripple, and BitGo, at the end of last year, allowing them to legally participate in on-chain financial activities. This move, however, sparked dissatisfaction within the traditional banking industry. [5] Traditional banks argued that the compliance responsibilities and costs they bear are unequal to those of licensed Web3 institutions, and they also compete in business. Meanwhile, the EU's MiCA regulation stipulates that an on-chain asset service provider licensed in one member state can operate across the entire EU. This cross-border passability could potentially lead to issues like license abuse or regulatory arbitrage.

These cases provide important references and cautionary tales for Hong Kong SAR, China. On one hand, while vigorously promoting the implementation of the on-chain financial system, Hong Kong needs to clearly define the boundary of responsibilities between traditional financial institutions and Web3 entities to avoid issues of unbalanced compliance obligations and costs. On the other hand, it needs to strengthen the supervision of the actual operations of licensed institutions and establish effective risk monitoring mechanisms to ensure the safety of user assets and achieve sustainable market development. Nevertheless, overall, the global regulatory system for on-chain finance is still in an exploratory phase, and its integration process with traditional finance will require long-term observation.

Key Points Diagram:

References

[1] Hong Kong Monetary Authority Issues Two Stablecoin Issuer Licenses

[4] Hong Kong Stablecoins + Digital RMB: A 'Fast Lane' for Mainland Assets Going Global?

[5] Bankers' Cake Tampered With? US Banking Industry Plans to Sue OCC over Crypto Charters

[6] Understanding the SEC's New Rules in One Article: Tokenized Funds Can Now Be Traded Like Stocks

[7] Circular on the Secondary Market Trading of Tokenized SFC-Authorized Investment Products

Disclaimer

This report is prepared by Web3Caff Research. The information contained herein is for informational purposes only and does not constitute any prediction, investment advice, proposal, or offer. Investors should not rely on such information to buy or sell any securities, cryptocurrencies, or adopt any investment strategy. The terminology used and opinions expressed are intended to help understand industry trends and promote the responsible development of the Web3, including the blockchain industry, and should not be construed as definitive legal positions or the views of Web3Caff Research. The views expressed in this report reflect only the personal opinions of the author as of the date stated and are independent of the position of Web3Caff Research; they are subject to change with subsequent circumstances. The information and opinions contained in this report are derived from proprietary and non-proprietary sources deemed reliable by Web3Caff Research, but do not purport to be comprehensive and its accuracy is not guaranteed. Therefore, Web3Caff Research makes no representation, warranty, or undertaking regarding its accuracy or reliability, nor does it accept liability for any errors or omissions arising in any other way (including liability to any person by reason of negligence). This report may contain "forward-looking" information, which may include projections and forecasts; this text does not constitute a guarantee of any forecast. Whether to rely on the information contained in this report is entirely at the reader's own discretion. This report is for informational purposes only and does not constitute investment advice, a proposal, or an offer to buy or sell any securities, cryptocurrencies, or adopt any investment strategy. Please strictly comply with the relevant laws and regulations of your country or region.