ArkStream Capital 2026年第一季報:地緣衝突與流動性退潮下的加密行業結構性出清

- 核心觀點:2026年第一季,加密市場在地緣衝突、貿易戰和鷹派聯準會政策的多重壓力下遭遇系統性拋售,比特幣從93,000美元跌至63,000美元,數位黃金敘事被證偽,山寨市場陷入流動性枯竭,AI行業的虹吸效應進一步加劇資金分化,市場出清遠未結束。

- 關鍵要素:

- 宏觀壓制:川普關稅政策、美伊軍事衝突和聯準會降息預期崩潰(從2次壓縮至近零)構成三重系統性風險,導致風險資產全面承壓及政策不確定性溢價。

- 比特幣敘事失效:數據顯示比特幣與那斯達克高度聯動,與黃金相關性極低,在極端風險事件中充當「流動性泄壓閥」而非避險工具,ETF投資者浮虧約23%加劇拋售。

- 山寨市場結構性萎縮:山寨幣較週期高點跌60%-80%,BTC Dominance維持高位(56%-59%),ETF和DAT資金全部鎖定BTC,中小山寨缺乏創新與資金流入,陷入價值回歸和投機枯竭。

- AI虹吸效應:AI行業已進入經濟性驅動階段(API成本降80%),其股票板塊收益率遠超Crypto+AI代幣,導致資金持續分流;Crypto+AI多數敘事還停留在炒作階段。

- VC投資困境:項目解鎖規則導致VC成為「劣後」方,一級投資虧損擴大,退出難度上升;交易所上幣策略加劇囚徒困境,做空中小山寨成為少數正期望對沖手段。

Preface

In the first quarter of 2026, the global financial markets entered their most severe risk repricing cycle since 2022. The continuous escalation of geopolitical conflicts, the full-scale return of trade protectionism, and the repeated wavering of major economies' monetary policies have collectively created a highly uncertain macro environment with low liquidity preference. The crypto market suffered a systemic sell-off during this quarter, with Bitcoin falling from around $93,000 at the beginning of the year to the $63,000 range, a maximum drawdown of over 38%; the altcoin market was even more severely impacted, with numerous tokens dropping 60%–80% from their cycle highs.

The deterioration of the market environment was not random but the result of multiple structural pressures叠加. On one hand, the Trump administration's aggressive tariff policies and the US-Iran military conflict pushed geopolitical risks to new heights, putting widespread pressure on risk assets; on the other hand, the crypto market's own narrative fatigue and fragile liquidity structure were fully exposed during the downtrend. Bitcoin's "digital gold" narrative failed to fulfill its safe-haven function in a wartime environment, instead behaving like a high-beta risk asset; altcoins, lacking new capital inflows and fundamental support, fell into a continuous value regression.

Meanwhile, the rapid evolution of the AI field is profoundly reshaping the intersection of technology and finance. The continuous iteration of large language models, the explosive growth of open-source AI Agent frameworks, and the initial integration of AI with crypto payment scenarios provide noteworthy new variables for the medium to long-term development of the industry.

The following analysis will dissect the core variables of Q1 from four dimensions: the macro environment, Bitcoin and capital structure, AI development trends, and altcoin market divergence, offering ArkStream Capital's framework assessment for the subsequent direction.

Macro Environment: Geopolitical Conflicts and Trade Wars Form Systemic Pressure

Accelerated Fragmentation of the Global Trading System

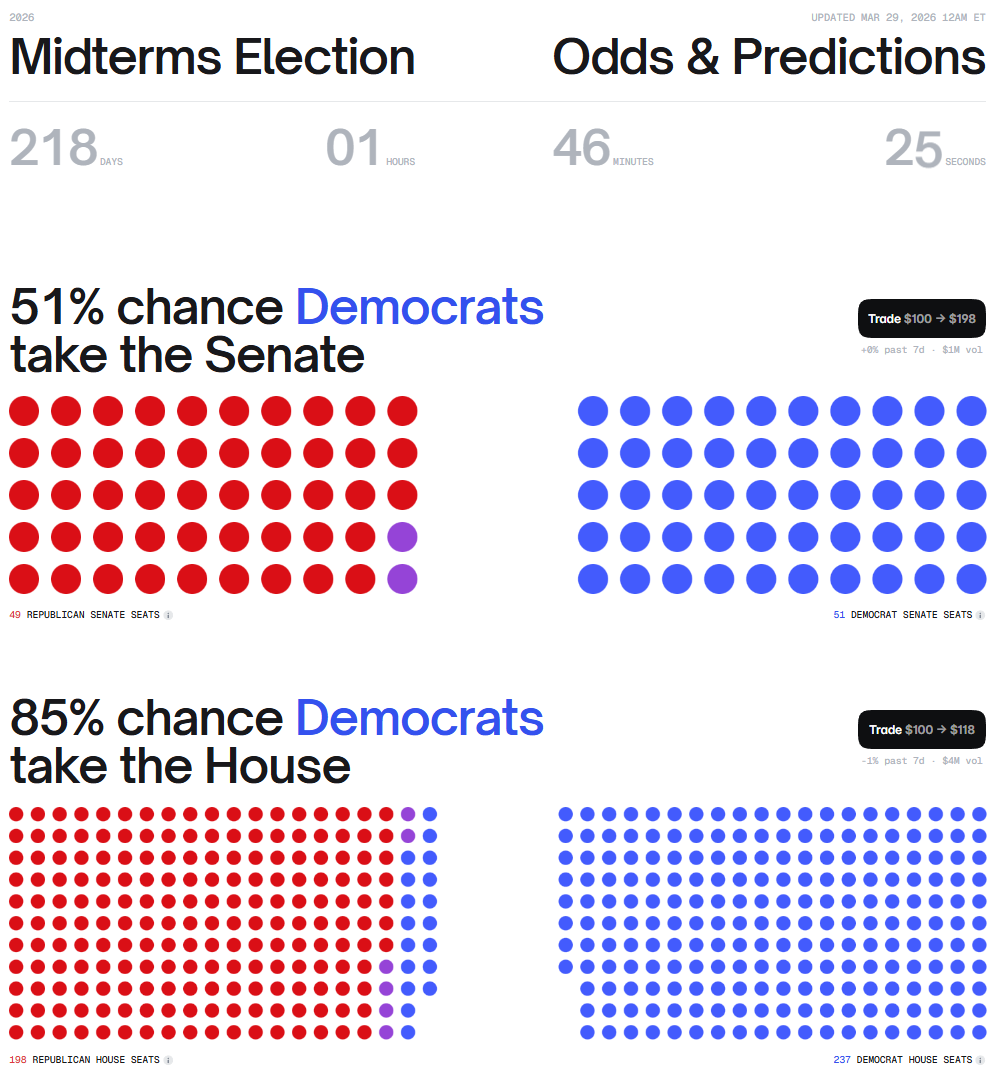

The primary analytical framework for understanding Q1 policy actions is the November 2026 US midterm elections. The Republican Party's slim majority in both the House and Senate faces a serious challenge; historically, the ruling party almost always loses seats in midterm elections. Under this pressure, the Trump administration's series of aggressive moves in Q1—including tough tariffs, the Greenland sovereignty narrative, and military strikes on Iraq—all serve a single political logic: consolidating the Republican base by adopting an assertive stance in foreign and economic policy, crafting a "strong president" narrative for the election year. This implies that, at least until the November vote, policy unpredictability and aggressiveness are unlikely to cool down substantially, and the premium for political uncertainty faced by risk assets will persist throughout the year.

Predicted distribution of seats in the US Senate and House for the 2026 midterm elections

https://polymarket.com/predictions/midterms

Driven by this political logic, the global trade order experienced its most severe shock in Q1 since the founding of the WTO. The Trump administration announced tiered tariffs of 10%–25% on eight countries—Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands, and Finland—in mid-January, using the Greenland sovereignty dispute as leverage; by the end of January, a bill for 500% punitive tariffs on countries purchasing Russian oil (directly targeting BRICS nations like China, India, and Brazil) gained bipartisan support and entered the voting process. On February 20, after the US Supreme Court struck down the legal basis for tariffs under IEEPA, Trump immediately invoked Section 122 of the Trade Act of 1974 to reimpose a 10% global temporary tariff (valid for 150 days).

The repeated shifts and escalations in tariff policy impacted markets from three dimensions: on the cost front, import tariffs directly pushed up commodity prices and inflation expectations, compressing the Fed's room for rate cuts; on the supply chain front, retaliatory measures from trading partners exacerbated global supply chain uncertainty, dampening corporate capital expenditure intentions; on the risk premium front, the policy's inherent unpredictability became the biggest pricing challenge, systematically raising implied volatility for various risk assets. ArkStream Capital believes that the suppressive effects of the latter two on the market are far harder to quantify than the tariff rates themselves and are even more difficult for the market to fully price in.

📊 [Chart Placeholder] Screenshots or maps related to the Greenland sovereignty dispute news

https://truthsocial.com/@realDonaldTrump/posts/115925897257210763

The essential difference between this round of trade conflict and past tariff disputes is that the scope has expanded from bilateral to multilateral, and the repeated changes in legal basis indicate that policy-making has strayed from the institutional track, entering a new phase of "instant executive power." Its suppressive effect on risk assets far exceeds the direct economic impact of tariff rates themselves.

Tail Risk of US-Iran Military Conflict

On February 28, the US and Israel launched coordinated military strikes on Iran. Oil prices surged within hours, and global financial markets shifted into risk-off mode. With traditional markets closed for the weekend, the crypto market, as the only 24/7 major asset class, bore the brunt of safe-haven selling pressure. Bitcoin dropped from $65,500 to $63,000 within an hour, liquidating over $515 million in leveraged positions.

This event once again confirmed a fact: Under the current institutional participation structure, crypto assets during extreme risk events play more of a 'liquidity relief valve' role than a safe-haven tool. When traditional markets are closed, the crypto market becomes the only operational risk-release channel for global capital, and its price action reflects liquidity structure more than fundamental logic.

Crude Oil Price Trend Q1

https://www.tradingview.com/chart/WZsS9J3A/?symbol=NYMEX%3ACL1!

The impact extended far beyond price levels. Within hours of the strikes, the Iranian leadership announced the closure of the Strait of Hormuz, one of the most critical arteries for global oil shipping, through which nearly 20% of the world's seaborne oil trade transits. This super-tail risk superimposed an energy supply shock onto already high global inflation, directly impacting European and Asian economies heavily dependent on imported photovoltaic energy. Even though a temporary ceasefire was reached through negotiations a few days later, the pricing of this tail risk has not been fully eliminated. Should the conflict escalate again, the market's reaction magnitude could far surpass the initial shock.

For the crypto market, this shock absorbed two pressures: first, rising oil prices pushed up inflation expectations, further compressing the Fed's room for rate cuts; second, investor anxiety before traditional market openings could only be released via the crypto market. Meanwhile, Iran's uncertain subsequent situation remains a core macro variable for geopolitical risk signals in Q2. If the conflict escalates further under the political logic of a midterm election year, the suppression of risk assets will not merely be a repeat of Q1.

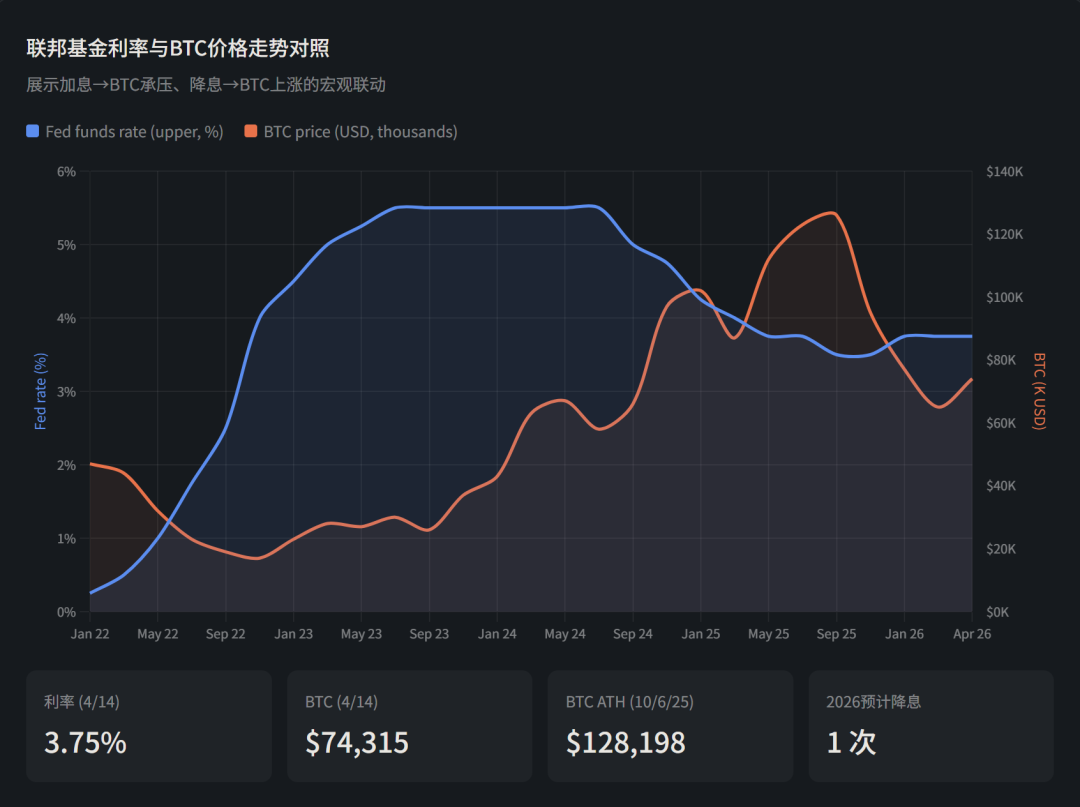

Federal Reserve: Reversal of the Rate Cut Path and Delay of the Liquidity Inflection Point

On a macro level, BTC, as a peripheral market within the financial industry, has shown significant correlation with the Fed's interest rate policies.

Fed Interest Rate vs BTC Price (2022–2026)

Starting from 2022, there have been roughly 4 distinct cycles.

2022-2023: Rate Hike Cycle → BTC Under Pressure

The Fed began aggressive rate hikes from early 2022, raising from near zero to 5.5%. During the same period, BTC plummeted from ~$47K to ~$16K. High interest rates increased the opportunity cost of holding non-yielding risk assets like BTC, leading to capital outflows.

H2 2023 - Early 2024: Rate Hike Pause → BTC Bottomed Out and Rebounded

While rates were held in the 5.25%-5.50% range, the market began pricing in rate cut expectations. BTC recovered from ~$16K to over $60K. Additionally, in January 2024, the SEC approved 11 spot BTC ETFs, marking BTC's official entry into the mainstream financial system.

September 2024 - October 2025: Rate Cut Cycle → BTC Soared

The Fed cut rates by 50 basis points for the first time in September 2024, followed by three consecutive cuts totaling 100 basis points for the year. In 2025, three more rate cuts were completed, bringing the cumulative cut to 1.75%. During this period, BTC surged from ~$66K to an all-time high of $128,198.

End of 2025 to Present: Rate Cut Pause + Geopolitical Conflict → BTC Correction

The Fed maintained rates at 3.50%-3.75% in both its January and March 2026 meetings, due to oil price increases pushing up inflation expectations. PCE and core PCE forecasts were both raised to 2.7%. Coupled with heightened tensions in the Middle East, BTC fell back from ~$126K to its current level around ~$74K.

Current Rate Cut Expectations

Rate cuts reduce the opportunity cost of holding BTC and increase market liquidity, historically strongly correlated with BTC price increases. The Fed's dot plot indicates one rate cut expected in 2026, which is not positive news for BTC's price.

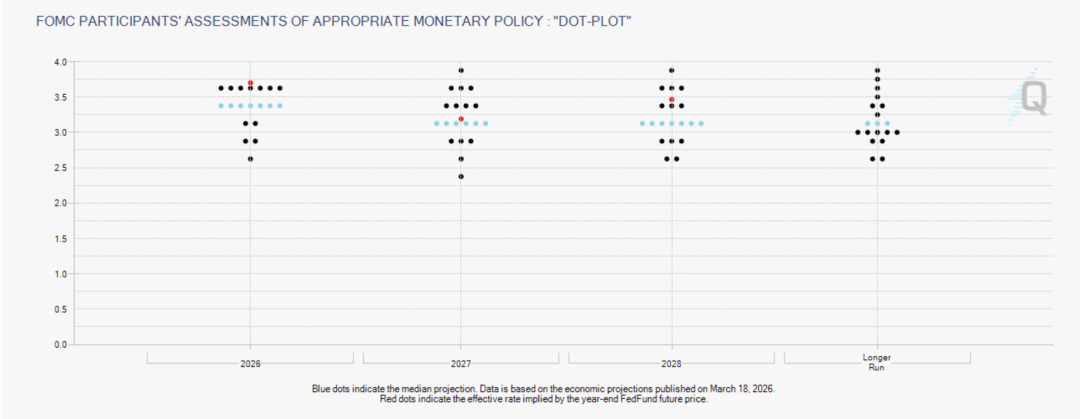

During Q1, the Fed's policy path underwent a gradual hawkish shift, with rate cut expectations being progressively compressed from 2 cuts at the start of the year to near zero.

Dot Plot

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

The January 28 FOMC meeting kept the federal funds rate unchanged at 3.5%–3.75%, the first pause after three consecutive rate cuts in 2025. Powell reiterated the need for "more data to confirm inflation is sustainably declining," a cautious but neutral tone. However, the minutes released on February 18 revealed internal divisions far deeper than the statement suggested. Several officials explicitly mentioned the possibility of a rate hike scenario, the first such language in the minutes since 2023, beginning to crack market confidence in rate cuts.

On January 30, Trump announced his nomination of former Fed Governor Kevin Warsh to replace Powell as Chair (formally submitting nomination documents to the Senate on March 4, with a potential start in May). As a Fed governor from 2006–2011, Warsh was one of the youngest and most hawkish members, having resigned in opposition to QE2. Notably, his public stance has softened in recent years, advocating for the idea that AI-driven productivity gains have a structural deflationary effect, thus supporting lower interest rates. However, his most prominent label remains "balance sheet reduction before rate cuts." Warsh has frequently criticized the Fed for maintaining an oversized balance sheet that blurs the line between monetary and fiscal policy, advocating for significant balance sheet reduction before discussing rate cuts; even if nominal rates drop slightly, liquidity tightening from aggressive balance sheet reduction could offset the effects of a cut (some analysts estimate that shrinking the balance sheet by ~$1 trillion is equivalent to roughly a 50bp rate hike). Market interpretation of his nomination was generally hawkish, with some institutions labeling him "an intriguing choice for a president wanting low rates." Following the nomination news, precious metals fell first (gold dropped 1.9% in a single week), the dollar strengthened, and the market began repricing what a Fed led by such a chair would mean.

Entering February, the situation became more complex. On February 28, the US and Israel launched military strikes on Iran (see Section 1.2), causing oil prices to jump over $100/barrel, fundamentally altering the inflation landscape. Before the cost-push inflation from tariffs could be absorbed, a supply-side shock from energy prices was added, creating dual inflation pressure. The policy space for rate cuts was severely compressed, and the market began to seriously discuss a previously absurd possibility: the next move might not be a cut, but a hike.

The March 18 FOMC meeting put this discussion in black and white. The committee voted 11:1 to hold rates steady (the January meeting was 10:2, with Miran and Waller dissenting; in March, Waller switched to favor, leaving only Miran dissenting—a noteworthy hawkish convergence signal). The post-meeting statement specifically added language about "uncertainty regarding the impact of developments in the Middle East on the US economy," formally incorporating war factors into the Fed's decision-making framework. The updated Summary of Economic Projections (SEP) and dot plot released a clear hawkish signal: the 2026 inflation forecast was raised to 2.7%, and the median dot plot maintained one rate cut for the year (unchanged from December, with Powell explicitly stating "the median has not changed"). However, 14 of the 19 committee members expect only 0-1 rate cuts this year, a clear hawkish shift in distribution. CME FedWatch showed market expectations for 2026 rate cuts compressed from 2 at the start of the year to at most 1, with the probability of zero cuts rising significantly.

With the unemployment forecast maintained at 4.4% and GDP growth slightly upgraded, the overall picture takes on a stagflationary shape of growth resilience + inflation stickiness. Bitcoin immediately fell from $74,000 to $70,900, with ETF net outflows of $129 million on the day. Some market analysts pointed out that Warsh's first move after taking office might not be a cut, but a hike.

Looking back over the entire quarter, the collapse of rate cut expectations was not an event but a process, from the discussion of hikes in the January minutes, to the hawkish personnel expectation from Warsh's nomination, to the second inflation shock from the Iran war, to the March dot plot compressing the year's expected cuts to one. The market's initial pricing of 2 rate cuts at the start of the year was stripped away layer by layer, and the "Higher for Longer" narrative re-established dominance. The market widely believed that "the inflection point for interest rates was established; the liquidity inflection point was just a matter of time." However, the Q1 evolution offered a more extreme answer: not only is the liquidity inflection point distant, but the rate cut inflection point itself faces the risk of being overturned. If Warsh's advocated combination of rate cuts and balance sheet reduction materializes, it would mean that even if nominal rates decline, the actual liquidity environment could become tighter, and its suppressive effect on risk assets should not be underestimated.

Against this macro backdrop, global risk assets faced comprehensive pressure: the S&P 500 is down over 5% year-to-date, with the Nasdaq falling even more; gold ETFs absorbed over $160 billion; and Bitcoin ETFs saw net outflows of $38 billion in February alone. The signal of capital moving from digital gold to physical gold was extremely clear. ArkStream Capital will continue to monitor the evolution of rate cut expectations and geopolitical situations, as these are core variables for judging the subsequent timing of the liquidity inflection point.

Bitcoin and Capital Structure: Narrative Invalidation, ETF Divergence, and Institutionalization Progress

Stress Test for Digital Gold

One of the most noteworthy structural changes in Q1 was the significantly increased correlation between Bitcoin and the Nasdaq index during periods of stress. During the market stress test, Bitcoin not only failed to provide a hedging function but showed an almost synchronous downward trajectory with tech stocks.

From a behavioral finance perspective, this is not surprising. Since the approval of ETFs, institutional investors have included Bitcoin within the same risk budgeting framework as tech growth stocks. When macro risk appetite contracts, deleveraging and position reduction are systematic and do not differentiate by asset class. This jump in correlation signals that Bitcoin's identity transformation within the institutionalization process has entered a new phase: it is evolving from an independent alternative asset into a high-beta subset of the global risk asset portfolio.