Tiger Research:深入剖析 Circle 財報,加密貨幣下一階段將走向何方?

- 核心觀點:Circle 正從依賴 USDC 準備金利息的穩定幣發行商,轉型為以自有 L1 網絡 Arc、支付網絡 CPN 及 AI 支付棧 Agent Stack 為核心的綜合基礎設施營運商,旨在透過多元化收入來源降低對利率的依賴。

- 關鍵要素:

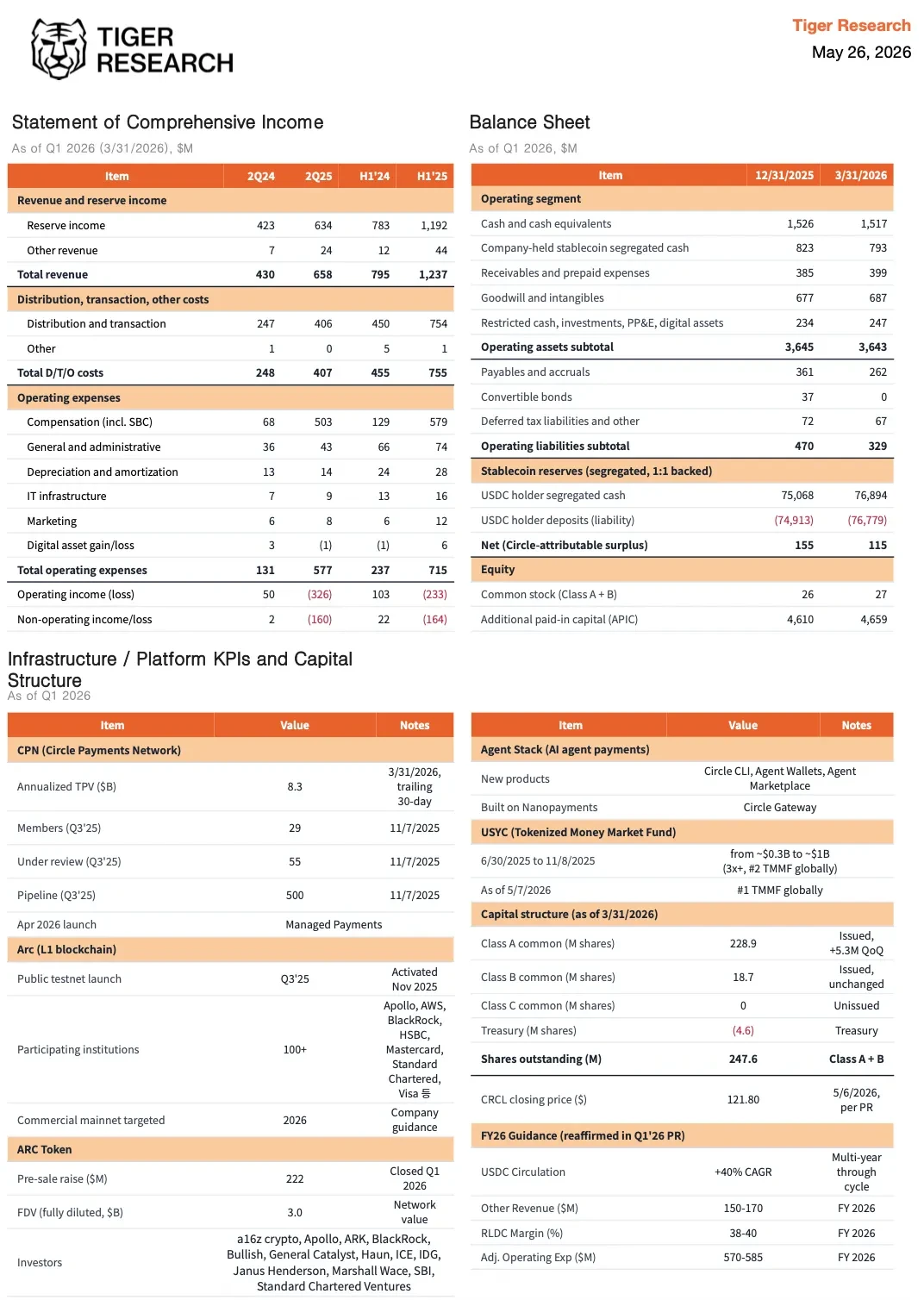

- 2026年Q1營收6.94億美元(年增+20%),RLDC利潤率創歷史新高41.4%,主因是USDC在自有平台使用佔比躍升至17.2%,降低了外部平台分成成本。

- 核心業務仍高度集中:USDC準備金利息佔總營收94%。淨利潤年減15%至5500萬美元,主要受IPO後股權激勵攤銷及Arc研發支出增加影響。

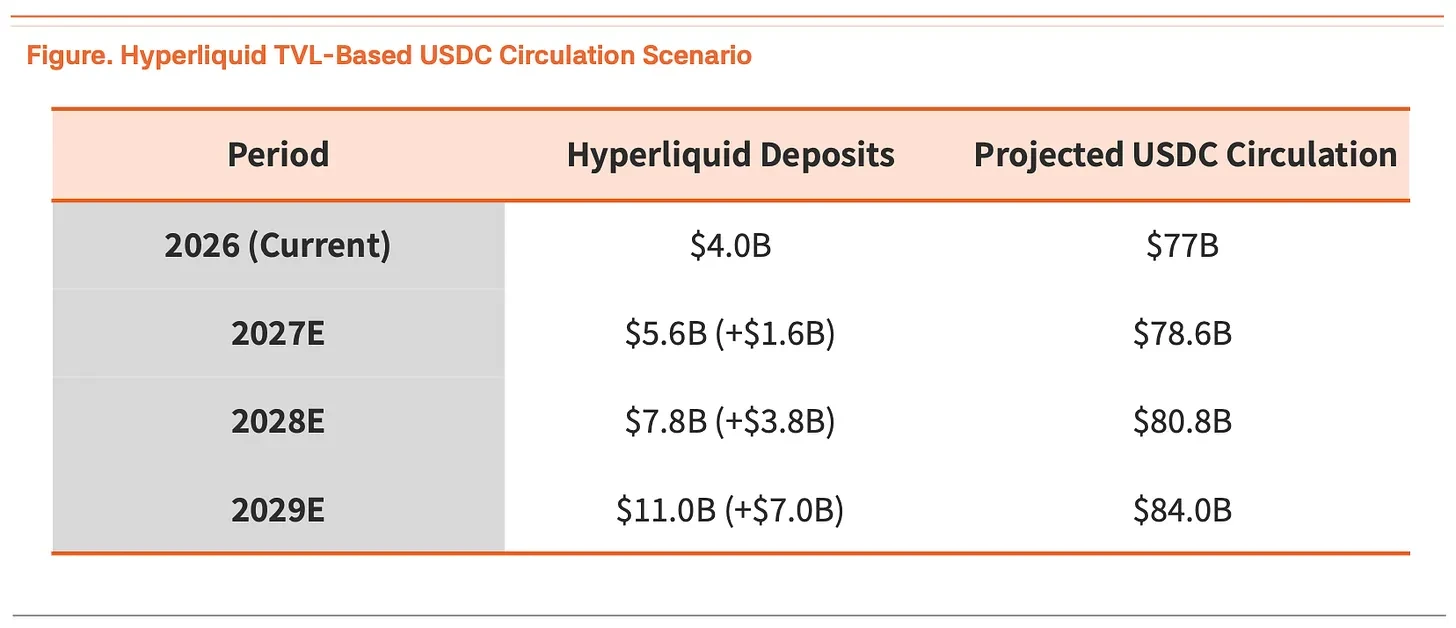

- 透過與DEX平台Hyperliquid合作,USDC被註冊為官方交易對。預計未來三年該平台能推動流通量從770億增至840億美元,犧牲利潤率換取規模。

- 自有L1網絡Arc主網計劃於今年夏季上線。其核心目標是基於CPN支付網絡和鏈上外匯引擎StableFX產生基礎設施手續費收入,切斷對利率的直接依賴。

- 針對AI智能體經濟推出Agent Stack,支援極小額支付(低至0.000001美元)和零Gas費結算。預計完全商業化需待2028年《GENIUS法案》生效後。

This report is written by Tiger Research. Circle has released its financial results for the first quarter of 2026. Interest income from USDC reserves still accounts for over 90% of total revenue. To break this highly concentrated structure, Circle is advancing several initiatives, including the Ark network. Where is the next stage heading?

Summary

- Taking the Q1 2026 results as a turning point, Circle is accelerating its paradigm shift—from a pure stablecoin issuer to a comprehensive infrastructure operator for the digital asset industry. Its forward-looking business strategy revolves around three core pillars.

- Maximizing USDC Profit Margins and Circulation: Reserve interest accumulates on both external and proprietary platforms. This quarter, increased usage of USDC on Circle's proprietary channels (CPN) drove the RLDC margin to a historic high of 41.4%. To expand issuance scale, Circle has partnered with the DEX platform Hyperliquid.

- Launching Its Own L1 Network "Arc" to Diversify Gas and Fee Revenue: Currently, 94% of Circle's revenue comes from USDC reserve interest. Once Arc expands Circle's platform business and generates platform fee income, the structural over-reliance on reserve interest will be fundamentally addressed.

- Securing the AI Payment Gateway through Agent Stack: Circle is vying for the standard-setting power for autonomous micropayments between AI agents. Based on infrastructure development progress and the expected enactment of the GENIUS Act, the target for full commercialization is set for 2028.

Overall, Circle's near-term focus is aggressively expanding USDC issuance volume through anchor platforms like Hyperliquid, while vertically integrating its financial stack around its own L1 (Arc), payment network (CPN), and AI nanopayments (Agent Stack). The key lies in the positive feedback loop where USDC circulation growth and infrastructure diversification reinforce each other.

Circle is transitioning from a pure interest income business to a platform business driven by traffic and transaction fees.

Q1 2026 Review: Margins Are Improving

1. Revenue Growth and Margin Enhancement – Improved Profit Quality from Higher Proprietary Platform Share

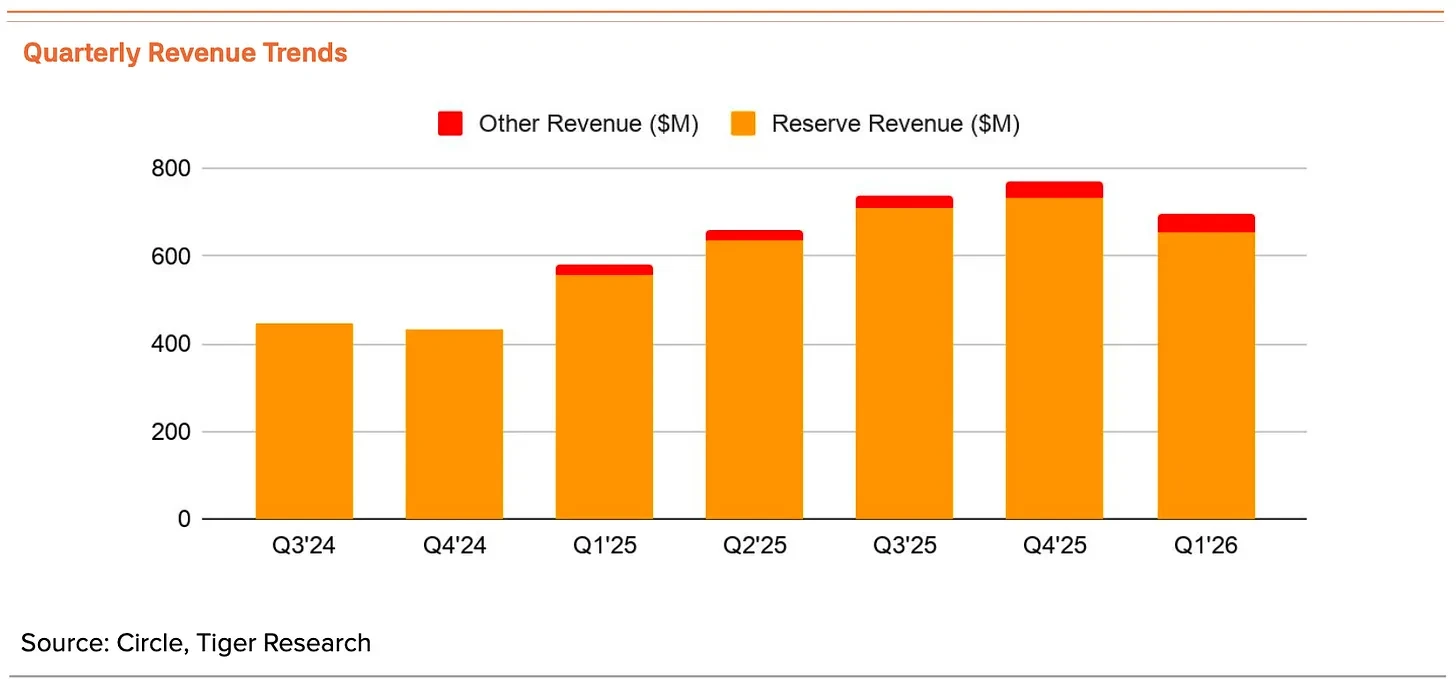

Q1 2026 revenue reached $694 million (YoY +20%), with adjusted EBITDA of $151 million (YoY +24%) and an adjusted EBITDA margin of 53%, indicating improved profitability. Currently, 94% of Circle's total revenue relies on reserve interest income.

The reserve yield fell 31 basis points QoQ (from 3.81% to 3.50%), putting direct pressure on revenue. Despite this, the RLDC margin rose for the third consecutive quarter, hitting a record high of 41.4%. Even as interest-dependent income faced headwinds, Circle successfully improved its core profitability.

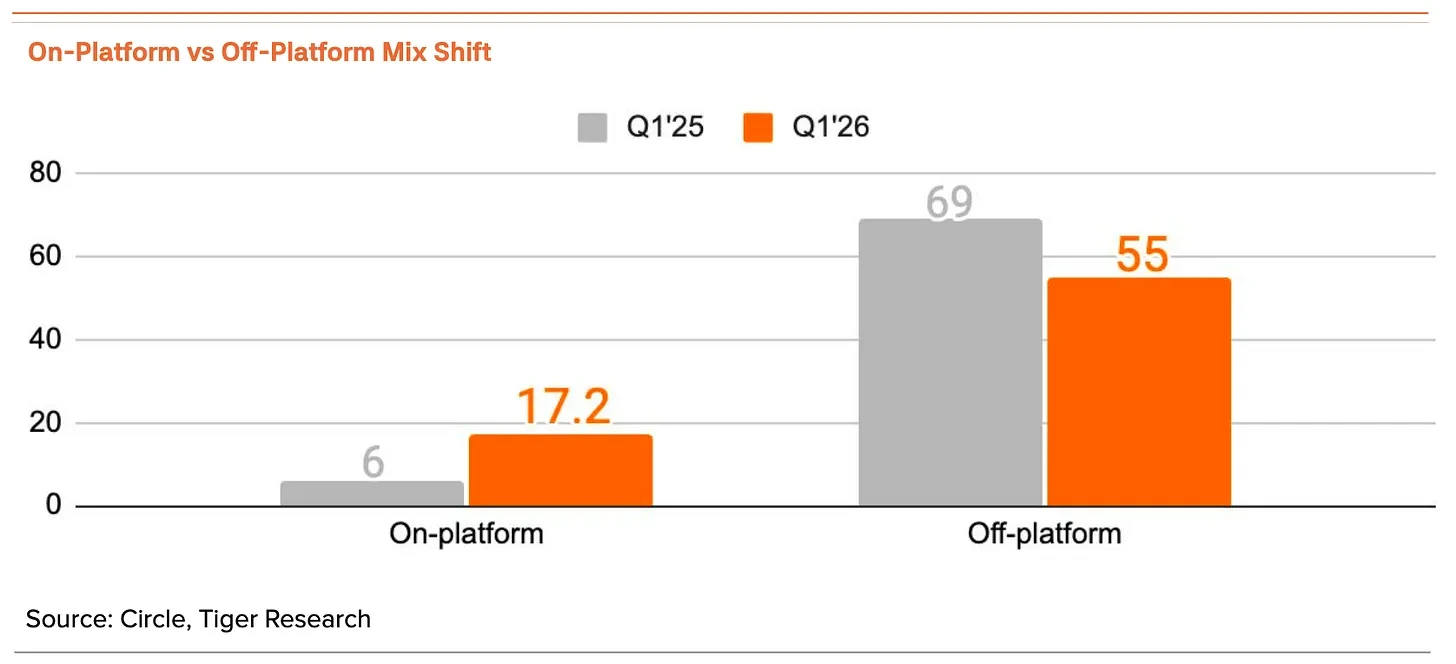

The key driver for the margin improvement was the rising share of USDC usage on Circle's own platforms. This quarter, the on-platform share jumped from 6% to 17.2% (YoY +1,149 basis points), while the off-platform share narrowed to 55%.

This change reflects the results of institutional client onboarding into Circle's proprietary payment network, CPN (Circle Payments Network). The number of member financial institutions grew to 136 in a single quarter (QoQ +36%), and annualized total payment volume (TPV) expanded to approximately $8.3 billion (QoQ +17%).

The phased rollout of the CPN payment product line supported this trend.

- Fiat Payments (Launched Q2 2025): Covers cross-border payments in over 50 countries, supporting local currency send and receive.

- Stablecoin Payments (Launched Q3 2025): Enables direct payment and settlement using regulated stablecoins (USDC, EURC) in over 180 countries.

- Custodial Payments (Q2 2026, launched in April): Circle provides licensing, custody, compliance, and USDC liquidity through a single integrated API. Partners only need to handle fiat currency, without the burden of digital asset custody, operations, and compliance.

This is critical for long-term profitability because the revenue attribution method differs entirely based on the deposit location. Balances held on external platforms like Coinbase require sharing reserve interest with the platform, while balances held on Circle's own platforms, such as Circle Mint and CPN, allow Circle to retain the full interest.

In other words, the higher the on-platform share, the lower the partner share cost, and the higher the RLDC margin. For the same revenue scale, Circle's actual profitability increases accordingly.

Of course, the usage fee income from CPN itself has not yet scaled. As CFO Jeremy Fox-Geen noted in last quarter's earnings call, the current priority is expanding the network's scale, not rapid monetization. CPN currently serves more as a channel to funnel funds into Circle's proprietary platforms rather than a direct fee channel. As a transitional strategy to defend against external distribution costs, the Q1 results confirm this path is effective.

2. The Signal of Declining Net Profit Hides Behind Growth

However, diverging significantly from revenue growth and margin improvement is the net profit trend. Net profit for Q1 was approximately $55 million, a 15% decline YoY.

The main reasons are the amortization of equity incentive expenses post-IPO and a sharp increase in infrastructure and R&D spending before the Arc launch. After excluding one-time and non-cash items, the adjusted data remains robust. Nonetheless, the net profit trend warrants continued attention.

Circle Moves Toward Full Vertical Integration

1. USDC: Strengthening the Core, Expanding Issuance

In Q1 2026, reserve interest income reached $653 million, accounting for 94% of total revenue. Circle's core business is highly concentrated on reserve interest, making revenue growth conditional on the continuous expansion of USDC issuance.

USDC's current circulation is approximately $77 billion. The core proposition for Circle's structural growth is how far this circulation cap can be pushed. USDT's previous rapid expansion was achieved by securing first-mover status on Binance trading pairs.

Circle plans to replicate this "preemptive grab" strategy on the DEX platform Hyperliquid. A recent typical example is Coinbase's acquisition of Hyperliquid's native stablecoin USDH – Hyperliquid did not deploy USDH as its platform's native trading pair but sold it and registered USDC as the official base trading pair.

Deposit growth on Hyperliquid directly drives USDC issuance. Hyperliquid's TVL grew from $2 billion in Q1 2025 to $4 billion in Q1 2026, peaking at $6 billion. Since Hyperliquid uses USDC as its base deposit asset, platform growth directly translates into new USDC issuance. The circulation outlook based on this is projected below.

In this scenario, just from the Hyperliquid platform alone, total USDC circulation could be pushed from $77 billion to $84 billion within three years. A single platform would contribute over 10% of total circulation, becoming a crucial issuance channel.

Conceding 90% of reserve interest income to the platform does compress near-term margins. But the reward is an irreplaceable scale—roughly $110 billion in daily trading volume and a 17% share of the DEX derivatives market. This deal is almost acceptable.

If Hyperliquid's derivatives product line further materializes, this positive cycle will become even more robust. For Circle, which prioritizes circulation expansion over margins, Hyperliquid, despite needing to share profits, is a strategic stronghold worth securing.

2. Arc: How Circle Breaks Free from Interest Rate Dependence

As mentioned, Circle's revenue is heavily concentrated in reserve interest, making its business structure structurally vulnerable during interest rate cut cycles. Arc is still in the testnet phase and has not generated visible revenue. With recent institutional funding of approximately $222 million, Arc has emerged as the core infrastructure to fundamentally sever this interest rate dependence.

Arc's primary target market is global cross-border payments. According to the World Bank report (RPW Issue 54), the global average remittance cost is 6.36%, with bank remittance costs as high as 14.99%. The high-cost structure stems from SWIFT's multi-level intermediation, opaque forex spreads, and weekend settlement delays.

Targeting these inefficiencies in traditional financial rails, Circle aims to build platform business revenue on Arc. The infrastructure fee income that reduces interest rate dependence rests on two pillars.

Circle Payments Network (CPN): Connects global institutions and enterprises to Arc for cross-border payments and settlements, charging processing fees on the traffic. Q1's institutional onboarding is laying the foundation for transaction revenue after the Arc mainnet launch.

On-Chain Forex Engine (StableFX): Supports on-chain stablecoin swaps, replacing the high intermediary spreads of traditional forex. Upon execution, smart contracts charge a preset fee from the transacted currency.

StableFX uses an RFQ (Request for Quote) model, unlike SWIFT's fixed cost structure. Market makers compete in real-time to offer the best wholesale spread. Large transfers can settle 24/7, with no SWIFT fixed fees and no slippage.

The greater the CPN traffic and StableFX trading volume on Arc, the higher the direct infrastructure and fee income. This creates a closed loop for non-interest income structure.

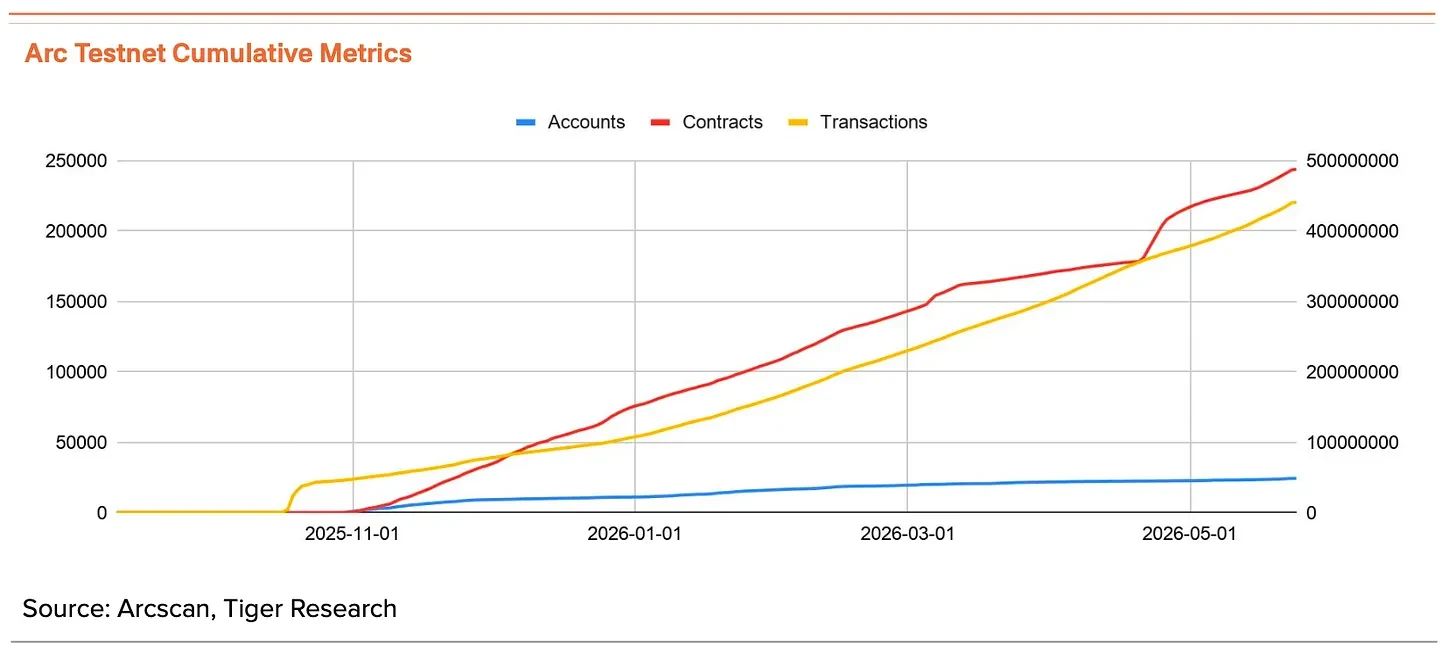

This transformation has already been validated through the testnet and participating enterprises. According to Arcscan data, the public testnet has accumulated approximately 430 million transactions since its launch, with about 3.26 million in the last 24 hours. Over 100 global institutions have participated, including BlackRock, HSBC, Visa, and AWS.

Beyond traditional financial institutions, the blockchain prediction market Polymarket has also joined the ecosystem.

This is not just a pilot for products and platforms. Arc is attracting real enterprises and driving real transaction traffic. If Arc operates as expected, Circle's revenue structure will expand from USDC reserve interest to include infrastructure operation income. Arc is the first step in uncoupling from interest rates.

According to the roadmap, the Arc mainnet is scheduled to launch this summer. Meaningful revenue from Arc is expected to gradually materialize after the mainnet goes live.

3. Agent Stack: A Blueprint for Autonomous AI Payments

An "agent economy" where AI agents make decisions and complete transactions autonomously on behalf of humans is approaching. Global tech giants like Google and OpenAI have begun actively deploying such autonomous systems.

The bottleneck lies in payment infrastructure. Fees generated by AI agents calling APIs are priced at micro (sub-cent) levels, which traditional payment systems cannot handle. Routing such micropayments through credit card networks results in fees higher than the principal—every transaction incurs a loss. Agent payments are structurally incompatible with existing card rails.

Circle is targeting this gap by launching the "Circle Agent Stack," which uses USDC as the settlement asset, along with a toolkit for building the supporting environment.

- Agent Wallets: AI autonomously holds and sends USDC within rules set by humans (e.g., spending limits).

- Agent Marketplace: A store where AI purchases API services and settles based on call count.

- Agent Nanopayments: Instant USDC settlement for as low as ~$0.000001, with zero gas fees.

- Circle CLI: A command-line tool for creating wallets and connecting agents.

- Circle Skills: Functional modules allowing AI agents to directly invoke Circle's financial product modules.

Currently, this revenue stream is also not yet in a visible stage. The path to market adoption and revenue recognition is expected to follow this phased roadmap.

2026 (Infrastructure Phase): Building the technical foundation to stably handle large-scale nanopayments. Arc mainnet activation this summer, anchoring partner integrations with Circle CLI and financial modules.

2027 (Regulatory Anchoring Phase): The GENIUS Act comes into effect, providing institutional guarantees for enterprise entry. Stablecoin securities exemptions and 100% safe asset backing are established legally, allowing even conservative corporate legal teams to trial the USDC payment system internally without risk.

2028 (Commercialization and Monetization Phase): The technical foundation and regulatory legitimacy are fully aligned. The agent economy becomes fully commercialized. Enterprises grant AI agents real spending authority, large-scale transactions emerge, and the contribution from Agent Stack is formally reflected in financial statement revenue.

Therefore, until traffic-driven revenue fully materializes in 2028, Agent Stack will mostly be reflected in the stock price as an "expected premium"—this is the capital market's valuation of future market position, not the realization of current revenue.