讓市場本身鏈上化:Canton Network正悄然成為機構金融的新底層

- 核心觀點:全球支付巨頭Visa以最高權重加入Canton Network成為超級驗證人,標誌著傳統金融對隱私保護型區塊鏈基礎設施的認可從實驗階段進入生產準備期;Canton Network透過數據可見性控制等差異化設計,正成為受監管金融機構開展鏈上業務的核心基礎設施。

- 關鍵要素:

- Visa首次提交區塊鏈治理提案,3天內獲批並以最高10級權重加入Canton Network,體現傳統金融對該網路的深度信任與合規審核的完成。

- Canton Network核心差異化在於將數據可見性控制內建於L1協議層,僅交易參與方可見細節,解決銀行對隱私缺失的顧慮,使受監管機構能安全開展業務。

- 鏈上月處理量超過9兆美元,真實運作傳統金融業務(如代幣化回購、國債結算),而非虛假刷量;摩根大通JPM Coin、DTCC國債代幣化為旗艦用例。

- 代幣CC為零預挖、零團隊分配、零VC份額的「網路效用資產」,價值錨定於鏈上真實金融活動量,減少機構對籌碼不公平的顧慮。

- Canton Network驗證人名單包括高盛、摩根大通等「老錢」機構,由華爾街出身團隊Digital Asset打造,目標是在合規框架內複製傳統金融的成功。

- Visa加入旨在實現原子化結算:買方付款與資產交付同步完成,消除時間差與對手方風險;Canton在資本市場側已有布局,支付側獲機構錨點。

Original | Odaily Planet Daily (@OdailyChina)

Author|jk

1. A Proposal Approved in Three Days

On March 20, 2026, Visa, the globally renowned payment service provider whose logo appears on most bank cards, submitted a governance proposal to the Canton Network. According to a report from The Block, just three days later, the proposal was approved, and Visa officially became a Canton Super Validator with the highest weight level 10 (Super Validator Weight 10). This also marks the first time Visa has submitted a blockchain governance proposal.

In the crypto space, this might look like yet another incursion by traditional finance. But if you are sufficiently familiar with the legal and compliance processes within traditional institutions like Visa, you would find a three-day approval quite unusual. For Visa's compliance team to submit this document, it must have been approached with the caution and seriousness typical of the traditional financial world. Moreover, securing the highest weight level suggests that negotiations and due diligence were fully completed beforehand. The proposal the public saw should be the result of months of collaboration between traditional finance and the crypto world.

In a statement, Rubail Birwadker, Head of Global Growth Products and Strategic Partnerships at Visa, said: "Many banks believe the lack of privacy is the biggest obstacle to migrating meaningful business to the chain. By becoming a Super Validator on the Canton Network, we bring Visa-level trust, governance, and operational standards to this privacy-preserving blockchain infrastructure, allowing regulated financial institutions to move payment operations onto the chain without disrupting their current ways of working."

It's clear that Visa's entry is an endorsement of an already operational and mature institutional network, not a starting point.

Since 2017, each market cycle has seen a batch of traditional financial institutions loudly announce their "exploration of blockchain," but very few have resulted in actual business applications. This time, Visa chose to enter the governance layer of a blockchain, holding voting rights and participating in infrastructure decisions. Eric Saraniecki, Head of Network Strategy at Digital Asset, the co-founder of Canton Network, said in a statement: "Visa's joining confirms that this technology has moved from the experimental stage to a production-ready stage."

Driven by curiosity about this collaboration, Odaily Planet Daily interviewed the Canton Network team. What exactly led to this partnership? And why was Canton, a long-gestating project, chosen?

2. Not Just More Assets On-Chain, But the Market Itself

To understand why Canton attracted Visa, we need to first look at the core differences between Canton and other chains.

Ethereum and Solana solve the problem of how to get more people involved and how to get more assets on the chain. Canton solves the problem of how financial institutions can conduct business normally on the chain. The focus sounds different, but when it comes to specific design choices, the trade-offs are almost entirely opposite.

Ethereum's global transparency is an advantage for retail investors but a barrier for institutions. Take a concrete example: a bank's foreign exchange trading desk. If every buy or sell order for USD or EUR were visible in real-time, counterparties could immediately adjust their quotes based on this information, significantly increasing the bank's trading costs. If a market maker's positions and hedging operations were all public, competitors could directly reverse-trade them, squeezing out profit margins. Repurchase agreements between institutions involve the capital positions and collateral sizes of both parties. Leaking this data poses a risk to the liquidity management of the entire institution. These constraints are not directly related to regulation but are determined by basic business logic.

Even if wallet addresses are not directly linked to real-name institutions, transparent on-chain transactions would alter the logic of the entire secondary market. No traditional financial institution wants its trades to be front-run. Therefore, designs like Ethereum and Hyperliquid are not optimal for large institutions.

Canton's approach incorporates data visibility control into its design.

This method bakes selective disclosure of data into the protocol layer as a native L1 design, rather than relying on patches from upper-layer applications. Specifically, only the direct participants in a transaction can see the details; the network validates the transaction without exposing any sensitive data. Two banks can conduct cross-border settlements on the same shared infrastructure, with the transaction completely invisible to all unrelated parties. Competitors can interact on the same network without exposing their respective positions and strategies.

We also asked about the relevant technical details. Canton's response was: "Canton separates the coordination layer (shared across the network) from data visibility (limited to participants), achieved through isolated execution environments and selective synchronization. This allows institutions to trade securely, and competitors to interact without exposing their positions or strategies. This is the mechanism that allows a real market, not just assets, to operate natively on the chain."

The Canton Network told us the summary of this design logic is: data visibility control is foundational, not an add-on feature.

So, it's no wonder why Canton's validator list looks like a gathering of old money: Goldman Sachs, JPMorgan Chase, BNP Paribas, Citigroup, Bank of America, DTCC, Nasdaq, Broadridge, Tradeweb... These institutions joined because this infrastructure allows them to replicate the success of traditional finance on it, which is why liquidity will gradually flow in.

Canton's Super Validator List

3. Born on Wall Street, Slow and Steady Wins the Race

Canton's creator is Digital Asset Holdings, founded in 2014 by Blythe Masters. A former star executive at JPMorgan Chase and one of the key pioneers in the CDS space, Masters has deep connections and strong industry credibility on Wall Street. From day one, this company was not building a blockchain product for retail; its target clients were strictly regulated financial institutions with real balance sheets operating within legal frameworks.

Regarding its origins, we asked a pointed question: We saw Canton launch in 2023. Why did it take until this year for a full-scale launch?

Canton's answer was: slow and steady wins the race.

Its Wall Street heritage dictates the entire project's pace. Canton admitted in the interview that this chain took longer than other L1s to get where it is today because, from the start, it dealt with regulated financial systems, building institutional trust, and figuring out how to genuinely plug into markets with real business.

This pace is entirely opposite to the mainstream narrative of Web3. Most public chains pursue rapid launch, rapid ecosystem expansion, and rapid hype generation, followed by a TGE and then "the team doesn't really know what's next." Canton's path was step-by-step negotiation: first secure DTCC, then Goldman Sachs, then JPMorgan Chase, then Visa, using their endorsements to bring in real business.

2026 is a turning point, not because of project marketing or the crypto bear market shakeout, but because, beyond the narrative, the infrastructure has, for the first time, truly met institutional requirements: real balance sheet activity is running on it. This is why it's the best time to pay attention to the Canton Network.

"So how much business has been onboarded?" we asked further.

4. On-Chain Activity on Canton

Canton's current data is an outlier in the blockchain industry, and the nature of these numbers differs significantly from most public chains. Currently, the Canton Network processes over $9 trillion monthly, handles hundreds of thousands of daily transactions, and the number of ecosystem participants has grown by an order of magnitude over the past three years. These figures correspond to traditional financial operations: tokenized repos, treasury settlements, and cross-institutional collateral mobilization. This is not inflated volume but real operations occurring on institutional balance sheets.

We also asked which products are currently mainstream on the chain. Currently, there are several flagship products:

JPMorgan's JPM Coin: In January 2026, JPMorgan's Kinexys division announced the native deployment of JPM Coin on the Canton Network. Unlike USDT and USDC, JPM Coin is a deposit token representing a direct claim on a deposit at JPMorgan, operating within the existing banking regulatory framework. For example, if two institutions use JPM Coin on Canton to settle a cross-border transaction, it is essentially no different from what they do in the traditional system, just much faster, and operations are no longer limited to business days. Kinexys currently sees daily transaction volumes between $2-3 billion, with a cumulative total exceeding $1.5 trillion since 2019. This flow of funds is about to run on Canton.

DTCC's Tokenization of US Treasuries: In December 2025, the US securities depository DTCC announced a partnership with Digital Asset to tokenize a portion of its custodied US Treasuries on Canton, aiming for a controlled production environment version in the first half of 2026, with expansion based on market demand. DTCC, together with Euroclear, serves as the co-chair of the Canton Foundation, directly participating in network governance.

DTCC processes securities transactions worth over $2 quadrillion annually and is the core of the US capital market's clearing and settlement infrastructure. To provide an intuitive analogy: DTCC's role in traditional finance is somewhat like the central bank's role for the interbank system; no one deposits money with it, but all stock and bond trades must pass through its backend system. Traditional repo markets only operate on business days; activity stops from Friday afternoon until Monday. But on Canton, repo transactions can run 24/7, using on-chain US Treasuries as collateral, enabling real-time fund intermediation across institutions, time zones, and weekends.

So, what will Visa do on the Canton Network?

A core goal described by Canton in the interview is atomic settlement: the buyer's payment and the seller's delivery of assets are completed within a single operation, without needing two steps or relying on intermediary institutions to bridge them. For example, currently, when an institution buys a batch of bonds, the transfer of assets and the settlement of cash are often separate processes with a time lag, counterparty risk, and the cost of manual reconciliation. Canton's goal is for these two things to happen simultaneously, locked in instantly with no time lag. To achieve this, capital market infrastructure and payment infrastructure must both be on-chain. Canton has a solid foundation on the capital market side; Visa's entry provides a true institutional anchor for the payment side.

Other things include real-time cross-border capital flows and embedding programmable logic into financial transactions, areas where blockchain excels.

Canton believes 2026 is the first cycle where infrastructure truly meets institutional requirements, which is why institutions like Visa are choosing to engage with blockchain infrastructure now.

Other Use Cases Already Running

Tokenized repos are currently the most mature scenario. Repurchase agreements (repos) are the most common short-term financing tool between financial institutions. Simply put, Institution A sells bonds to Institution B for cash, with an agreement to buy the bonds back in a few days. Traditionally, this process can only occur during business hours, and fund availability has delays. Tokenized repos on Canton are already available 24/7 with instant settlement. Several top-tier institutions have conducted real cross-institutional repo transactions covering weekends on Canton.

Collateral mobilization is another scenario with real demand. Large financial institutions often need to move collateral from one account or institution to another, e.g., moving bonds held at institution A to institution B to meet margin requirements for a derivatives trade. Traditionally, this process takes days, during which the assets are locked and unavailable for other uses. Canton's settlement model allows this process to occur nearly in real-time.

Digital bond issuance is another area where Canton has an advantage. Canton mentioned in the interview that it currently holds over half of the global digital bond issuance market share. The reason is that Canton can provide complete Delivery versus Payment (DvP), full bond lifecycle management, and multi-party coordination. The entire process from issuance to settlement can be closed on-chain, without needing to tokenize the asset and then rely on off-chain processes to finalize.

Stablecoin settlement is a direction accelerating with Visa's involvement. The goal is to enable stablecoin payments between institutions on the same compliant infrastructure with data visibility control, rather than routing through public chains.

Simply put, RWA wasn't explicitly mentioned, but every sentence spoke to the need for it.

Canton also gave a general outlook on the upcoming roadmap in the interview: In the medium term, corporate bonds, private credit, and trade finance will follow; in the longer term, equities are also on this path. The logic is consistent from current use cases to this roadmap: asset classes with higher liquidity and more mature regulatory frameworks are adopted earlier.

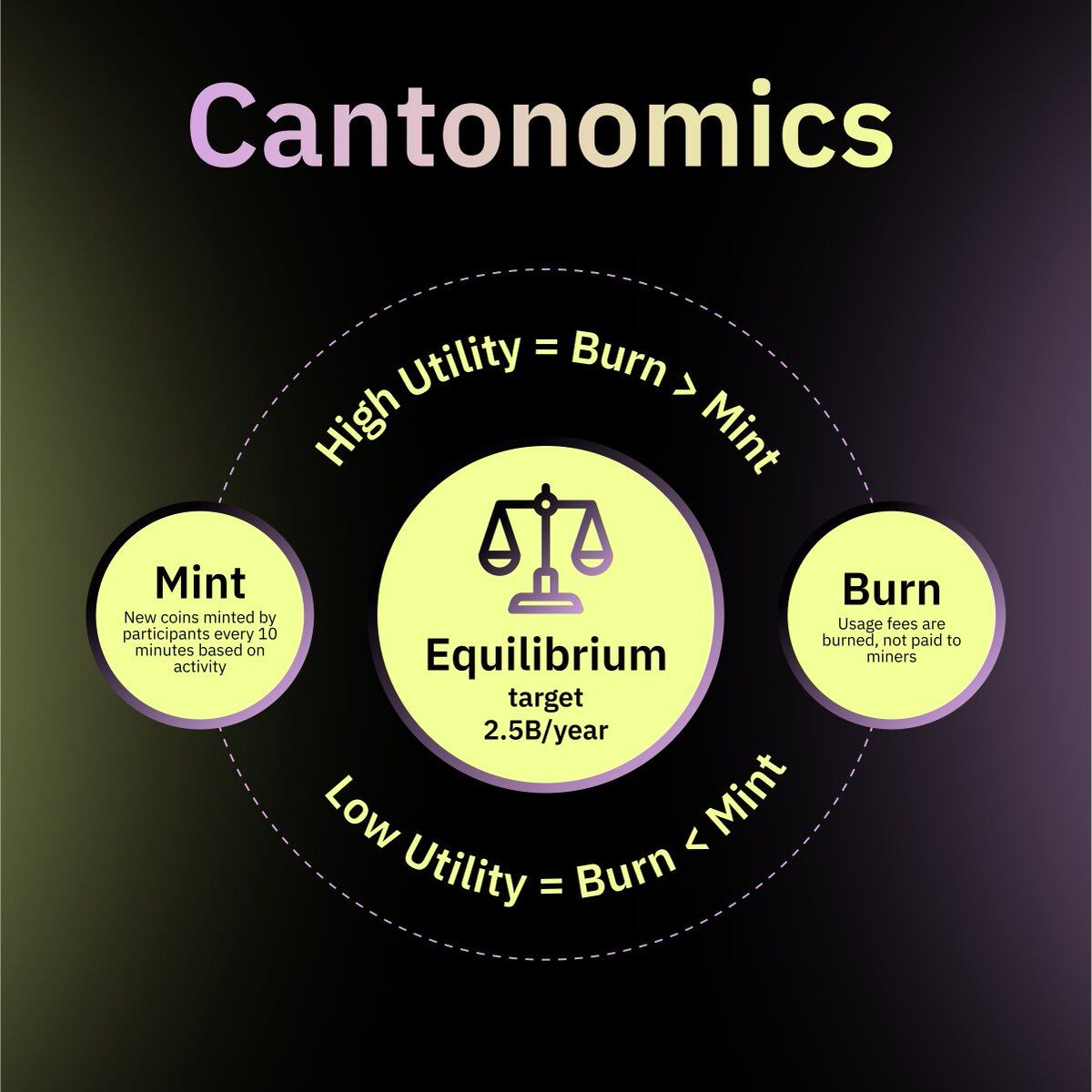

5. What Does the Token CC Represent?

For broader market participants, what exactly the CC token is remains an unavoidable question.

Canton's characterization in the interview was quite direct: CC is a "network utility asset," whose value is anchored to the volume of real financial activity occurring on the network.

This means demand comes from actual usage. The more transaction volume institutions generate on Canton, the more CC the network consumes. The long-term drivers for the token include institutional transaction flow, stablecoin settlement volume, total on-chain assets, and the depth of interoperability between Canton and other networks.

CC has a token distribution feature that is quite rare in the Web3 space: zero pre-mine, zero team allocation, zero VC allocation. All tokens enter the market through a fair distribution mechanism. For institutional participants, this design reduces concerns about "someone holding tokens with ultra-low cost basis ready to exit in the secondary market." The rules are transparent and equal for all participants.

For ordinary market participants, Canton exists more as backend infrastructure. The average person is more likely to interact with it through exchanges, wallets, or financial platforms, rather than directly interacting with the protocol. The improvements it brings, such as faster settlement speeds, tighter bid-ask spreads, and better financial product terms enabled by reduced operational costs, will gradually flow down to end-users through the product layer, rather than being directly perceivable.

6. The Next Steps

Canton's 3-to-5 year goals outlined in the interview are not measured by on-chain TVL or token price. Based on several specific goals listed by Canton: for stablecoins to become the standard means of inter-institutional settlement, much like SWIFT wire transfers are today; for major financial institutions to operate lending, deposits, bond issuance, and product packaging directly on-chain; for cross-border capital to move at near-real-time speeds instead of the multi-day settlement cycles typical in traditional systems; for multiple asset classes to be natively issued and settled on Canton, rather than being issued off-chain and then manually synchronized to the chain.

Canton uses the term "invisible" to describe itself in this state: At that point, Canton would just be one of the foundational protocols silently driving global finance, much like TCP/IP is for the internet or SWIFT is for cross-border remittances. Users wouldn't perceive its existence, but nothing would work without it.

Of course, there is still a long way to go. Regulation is highly fragmented across jurisdictions; what is compliant in Europe is completely different in Asia. Integrating with existing legacy systems is extremely difficult; banks cannot migrate core systems they've used for decades overnight. Interoperability between different blockchain networks remains an unresolved technical challenge. Coordinating institutions on the same infrastructure involves very complex interest dynamics. The Canton team did not shy away from these issues in the interview, telling us: Technological bottlenecks are no longer the biggest problem; the real challenge is how to truly achieve global adoption.

It's clear that changes in financial infrastructure never happen overnight. SWIFT was founded in 1973 and took nearly two decades to become the true standard for cross-border settlement. People use it today without thinking about where it came from. Canton's current position is probably that "no one has realized what it will become" stage. But for something that truly aspires to be infrastructure, being forgotten might be precisely what success looks like.