泡沫之後,何去何從:2026 數位資產市場分析報告

- 核心觀點:加密市場當前處於泡沫破滅後的調整期,與網路泡沫(2000-2002年)的歷史週期高度相似,並非「已死」,而是經歷價值回歸與基礎設施重塑,為下一輪增長奠定基礎。

- 關鍵要素:

- 歷史週期規律:鐵路、無線電及網路等科技泡沫均經歷「萌芽-狂熱-崩盤-調整」四階段,調整期伴隨資本向頭部集中、監管完善及商業模式從「講故事」轉向「盈利」。

- 加密市場現狀:截至2026年3月,總市值約2.5萬億美元,BTC價格在6.5-7.6萬美元區間整理,BTC dominance穩定在58-60%,市場特徵與網路泡沫後的調整期(如2002-2004年)相似。

- 機構化進程:美國現貨BTC ETF自2024年獲批後累計淨流入超530億美元,機構投資者佔比超30%,顯示BTC正從投機資產轉型為機構級配置標的。

- 監管框架落地:SEC與CFTC於2026年3月聯合發布數位資產分類框架,將16種資產歸類為數位商品,結束長期監管不確定性,為機構入場提供制度保障。

- 資本集中與項目出清:2025年Crypto VC資金同比增長約50%,但交易量下降46%,資本高度集中於後期項目;超過70%的DeFi和Meme項目TVL跌幅超90%,流動性枯竭。

- 戰略建議:項目方應聚焦穩定幣支付與RWA代幣化;VC需轉向股權+代幣混合投資;投資者應優先配置BTC,對Altcoin保持審慎,關注可驗證收入來源。

Preface: Certainty and Uncertainty in Crypto

At the beginning of 2026, amidst a new cycle of bull and bear transitions, the entire market is fraught with anxiety. After the events of 1011, market liquidity began to dry up. In the following period, aside from a handful of leading projects and companies still surviving, more teams chose to shut down or pivot.

With the sudden emergence of Openclaw and the sweep of a new technological wave, immense uncertainty has further exacerbated the panic. As market liquidity contracted, countless crypto workers pivoted towards AI. Media outlets that once focused solely on Crypto inexplicably began featuring AI reports on their front pages. Even OGs who have navigated this space for over a decade are loudly proclaiming that "Crypto is dead."

The crypto bubble has burst. Is Crypto truly dead?

Tossing this question to AI yields countless answers. DeepSeek will tell you that the dividends of the crypto market have dissipated; it is now the domain of professional, compliant players, leaving little opportunity for ordinary people. If you ask Grok, it will tell you this is merely a bull-to-bear transition in Crypto, one that will eliminate some players but steer the industry in a better direction. Consulting Gemini, it will argue that the development of AI will drive the synchronous development of Crypto.

There is too much noise. So, we aim to find the answer to this question in our own way. There is nothing new under the sun. We have vague memories that when the internet bubble burst in 2001, the market said the same thing. In fact, it’s what the market says during every bubble.

Thus, this time, we choose to study bubbles.

Even if the answer might be wrong, it represents our own certainty.

1. Exploring Historical Cycles: How Tech Bubbles Recur, from Railways to the Internet

The Glory of Railways and the Radio: The Ups and Downs of Industrial Revolution Bubbles

On September 27, 1825, the world's first railway built in Britain, the Stockton and Darlington Railway, officially opened. Three years prior, despite opposition from feudal aristocrats and the church, capitalists saw the future value of this steel giant and chose to bet on it, eventually completing the project. They believed this technology would bring them returns, but they did not realize the full impact it would have on the entire era.

Although the first railway was merely built as a branch line for the canal transport system, thanks to its convenience and cost-effectiveness, the entire industry began to sprout and grow rapidly. Investors flocked to participate. Towards the end of the South American mining speculation bubble of 1824-1825, these risk-takers began shifting their investments to railway companies. During 1836-1837, as the overall stock market strengthened, railway company share prices doubled. Seeing the opportunity, the British Parliament approved 44 companies that year, and their total fundraising for the year easily surpassed all previous capital investments in the industry combined.

The Rise, Dissipation, and Re-emergence of Bubbles

Like countless bubbles that followed, when a new technology gains market acceptance, it rapidly develops, creates a bubble that quickly bursts. Then, as infrastructure gradually improves, a stronger new bubble emerges, eventually leading back to a stable track.

After these 44 companies were established, the railway network was still underdeveloped, making rail transport seemingly less convenient than traditional water transport. Consequently, the railway stock index began to decline during this period. However, by the early 1840s, valuations rebounded, approaching previous peaks. Before 1843, the average annual capital investment in railway companies was about £1 million (approximately $3.5 billion today). In 1844, this figure became £20 million (20x), in 1845 it approached £60 million (60x), and by 1846, it reached £132 million (equivalent to about $120 billion today). In the same year, the total length of new railways built hit a record 4,538 miles. Everything seemed prosperous.

Bubble Burst and Value Return

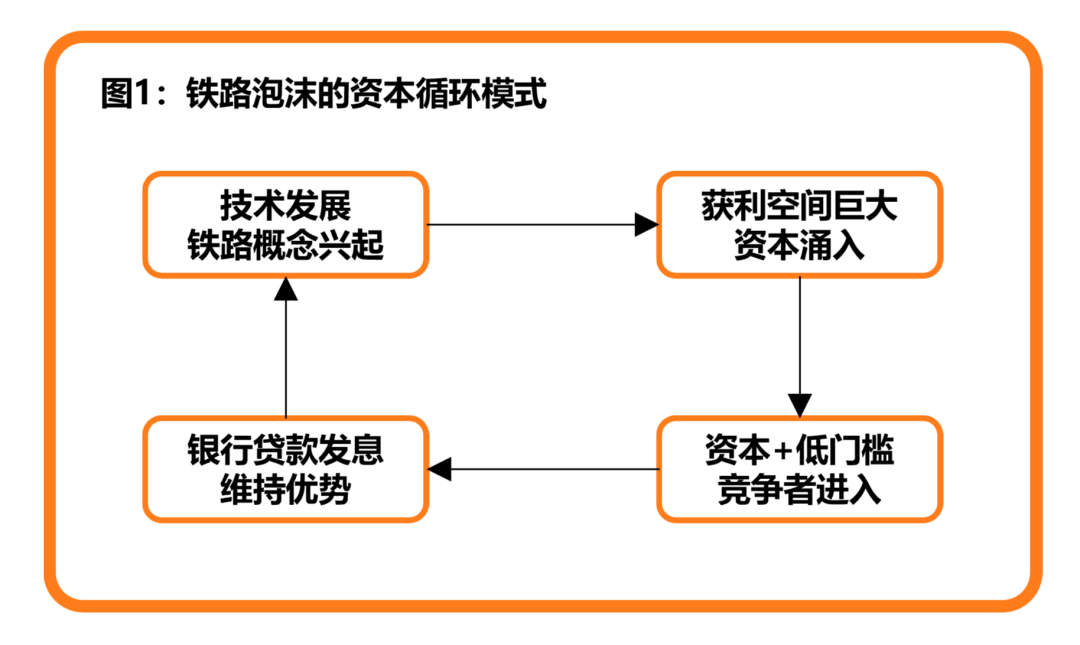

Undeniably, early railways were successful commercial projects. However, due to investor optimism, stock prices quickly far exceeded the maximum level a rational valuation of railway stocks could justify. The first railways had a first-mover advantage, but without barriers to entry, this advantage would disappear. Ample market capital, combined with relatively low technical/market barriers, presented an excellent opportunity for subsequent competitors. This, in turn, continuously squeezed the profit margins of existing companies, creating an environment of persistently declining industry-wide returns, commonly known as "involution."

For market investors at the time, the first sign that the boom was ending was the disappearance of huge premiums on newly issued stocks; only companies perceived as higher quality could maintain their share prices. For surviving railway companies, expanding and securing prime locations was undoubtedly the best option to maintain valuation and competitive advantage. Leveraging bank loans accelerated this advantage. To make matters worse, being in a nascent industry, most railway companies tended to underestimate the difficulty of railway construction, causing actual costs to far exceed the initial estimates in their prospectuses. Over time, these company stocks became purely financial games: railway dividends no longer came from company profits but from capital funds and bank borrowing.

Within this vicious flywheel, bank interest rates were continuously raised. At a certain critical point, railway companies could no longer sustain this capital cycle. The luster of technology-driven capital suddenly vanished. Overnight, countless investors went bankrupt, and public praise for railway companies turned into criticism.

Faced with this situation, the British government was forced to pass a Parliamentary Act allowing consolidation within the railway industry and abandoning nearly 20% of approved new railway constructions. As surviving companies regained profitability, a wave of mergers and acquisitions began. After this, the glory of British railways was no longer a glaring presence but more like the gentle, slow morning sunlight warming the land. Although the crazy capital bubbles were hard to replicate, this era truly nourished the growth of the Industrial Revolution.

Ultimately, the same story happened again, slightly later, on the American continent.

Marconi and the Radio

As a footnote to the development of the era, the story of railways concludes for now. With the continuous development of transportation, the distance between the world and itself was gradually shrinking. People could travel farther using these vehicles, or use wired telephones and telegraphs to achieve information transmission without leaving home.

Of course, the speed limit of information transmission should not stop here.

In 1865, after Scottish physicist James Clerk Maxwell systematically proposed the theory of electromagnetic waves, some inventors began experimenting with various radio waves. Eventually, in 1895, fortune favored the Italian inventor Guglielmo Marconi. When he successfully made a receiver ring a bell from a distance of 10 yards using his self-developed signal transmitter, he believed this distance could be extended much further.

Marconi keenly perceived the future commercial value of this technology. He filed a patent in 1896 and began promoting his technology to government agencies. Soon after, he founded the Wireless Telegraph and Signal Company to develop and sell wireless telegraph equipment. As compensation for relinquishing his patent rights, Marconi received £15,000 in cash (equivalent to about $6 million today) and £60,000 in shares (equivalent to about $28 million today), freeing him from financial worries. That year, Marconi was only 22 years old.

From Wartime to the Marketplace

As a rising star, Marconi quickly attracted attention from all sectors of society. In the early days of his company, he recognized the communication needs of the British Navy, which had a global presence. In 1899, he provided wireless equipment sales and consulting services to both the British and Italian navies. The first order was worth £6,000 (about $2.5 million today), with subsequent annual revenues exceeding £3,000 (about $1.25 million today).

Despite securing national-level endorsements, the market remained skeptical about whether this technology could have conventional commercial value. After several years of trial and error, Marconi adjusted his business model, shifting his sales strategy from direct sales to leasing. The biggest feature of this approach, compared to traditional paths, was ecosystem building. Through this collaboration, he allowed any product or company to use radio products by paying only a portion of the rent. The only restriction was that all customers could only communicate with other customers of Marconi.

It was precisely this strategy that led to the birth of countless radio stations and similar competitors.

The Birth of the Radio Concept Stock

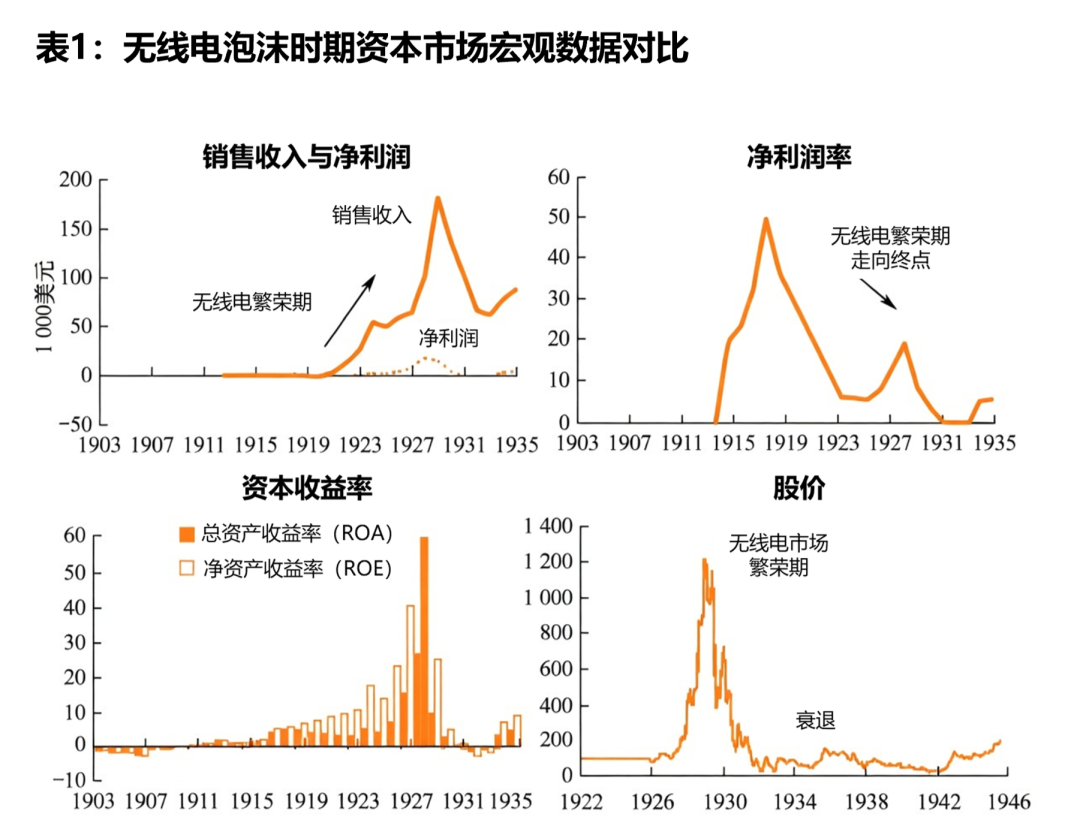

With the participation of Marconi and other technological competitors, the entire radio industry began to thrive, drawing in massive amounts of capital. In the early days of Marconi's company, despite reported losses, this did not dampen investor enthusiasm: technology and business models were still in early development, so losses were acceptable. Later, Marconi's company was renamed RCA, and the technical advantages and business networks built in the United States began to pay off. They consolidated the patents held by AT&T, GE, RCA, and Westinghouse Electric, forming an impregnable commercial fortress. This led to explosive growth in RCA's sales revenue and profits.

When one person gets to the top, all his friends and relations get there with him. Upstream and downstream companies associated with RCA also enjoyed this technological dividend. At the market's most extreme point, some people merely registered a company related to "radio" in the market and could easily raise funds and list their stocks. The story that followed was identical to the earlier railway boom: under the dividend, countless capital and companies flooded in; when the dividend began to dissipate, bank loans were used for dividends, ultimately leading to market collapse and the disappearance of the dividend. Unlike railways, the commercial value of radio technology was so epoch-making that this technological boom lasted nearly two decades. Once radio infrastructure was complete, from receivers, broadcast stations to televisions and radio media, the potential for imagination was vast enough to keep the market at a prosperous level for a long time.

Eventually, the Great Depression arrived. Capital games could no longer be sustained. People had to resort to more difficult but practical methods to improve the real sales revenue and net profit of companies and products.

At the Peak of the Internet Wave: A New Round of Technological Social Experiments

After IBM attempted to create personal computers and Apple propelled the trend, the penetration rate of personal computers in the mass market reached new heights. This also meant that certain technologies previously confined to research laboratories began to emerge – the Internet.

Coming from the Ivory Tower, Heading to the Commercial Field

The origin and birth of the Internet have become a cliché, so we won't dwell on it. Compared to its birth, the process of how the Internet became commercialized is certainly more worthy of our study.

In this transformation, the decisive factor was the U.S. National Science Foundation's (NSF) decision to relinquish control over the National Research and Education Network (NREN) and transition it to privatized, self-sustaining operations. During this process, numerous key elements emerged, making the widespread societal application of the Internet possible: Apple PCs provided the hardware foundation, the World Wide Web provided the framework, and Mosaic provided the entry point. Coupled with the commercialization of NREN, a giant industry began its magnificent journey.

In the early days of commercial open-source, not everyone saw this opportunity. More related companies opted for conservative approaches. On one hand, their knowledge and insights did not make them aware of the potential opportunities the Internet held. On the other hand, in the business environment of the time, industry giants generated revenue mainly through land grabbing and building their own ecosystems. Faced with this extremely open new environment, they were naturally repelled. Nevertheless, this was not necessarily bad for the industry's development: the resistance of giants provided ample market space and opportunities for new entrants.

Netscape: The First to Taste the Crab

As one of the earliest companies to feast on the crab, Netscape's peak indeed shook the entire market. In late 1994, Mosaic Communications faced legal issues due to its name similarity with Mosaic, eventually changing its name to Netscape Communications Corporation.

Although the company still had $12 million in the bank, its monthly cash outflow of $1 million forced Netscape to consider a business model pivot. After some maneuvers, it changed its previous service model, adopting a 30-day free trial followed by a $49 service fee. Coupled with the overwhelming performance advantage of its product, it quickly captured a large market share. Its initial intention was merely to make its market valuation look better, but this tactic proved highly effective. During its IPO in August 1995, Netscape publicly raised $140 million, propelling it to its peak.

However, what made it successful also led to its downfall. The success of this sales strategy went to Netscape's head. Basking in the joy of its IPO, it failed to consider how to build its moat next. It neither solidified its upstream and downstream moat through acquisitions, nor deepened its product to make it better. It even disdained commercial cooperation with peers, instead choosing the foolish option of inaction.

Its eventual outcome was clear – when the market discovered this massive cake and Netscape, as a pioneer, had proven its deliciousness, a flood of competitors rushed in. Netscape was finally acquired by America Online.

One Whale Falls, Everything Flourishes

Netscape's story is regrettable, but overall, it was beneficial for market development. Countless profit-seekers and innovators joined this adventure, spawning a dazzling array of projects. Almost in the same year as Netscape's success, Jerry Yang and David Filo spent a lot of time researching browser needs and eventually created an extremely efficient information indexing system, which they named "Yahoo." Meanwhile, at Stanford University, Sergey Brin and Larry Page were exploring information search engines, trying to find ways to find desired information content faster on the Internet. When these ideas traveled across the ocean, a then-inspired Jack Ma began preparing for the development and construction of "China Pages."

The Pinnacle of Concept Bubbles

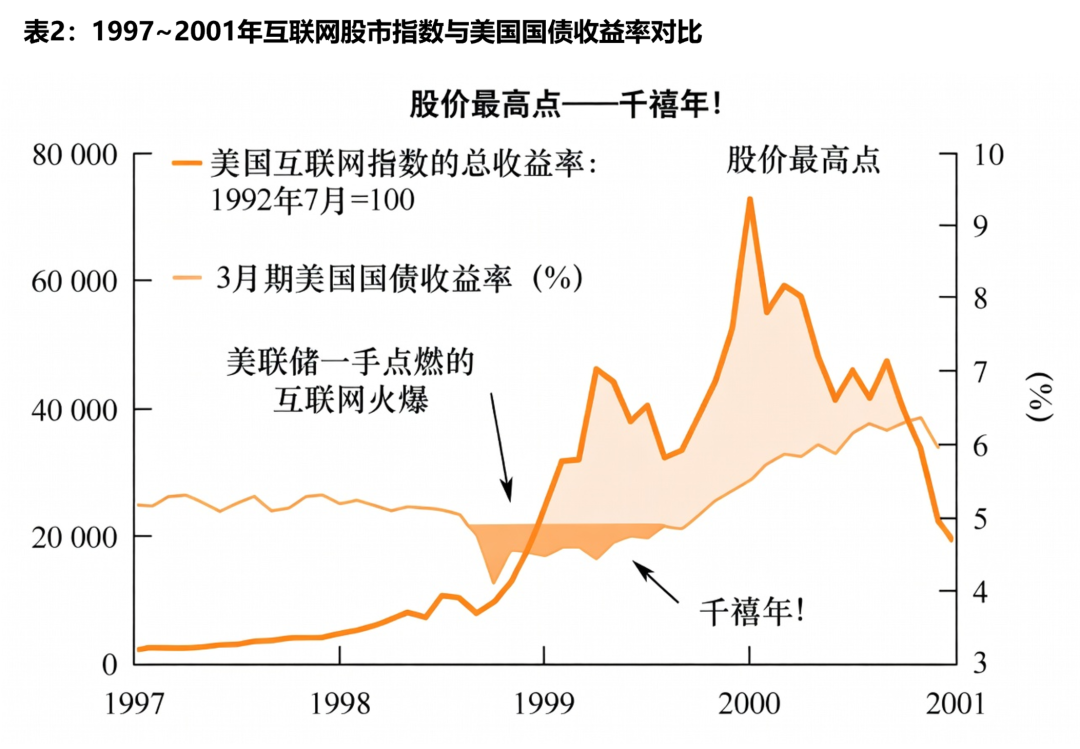

Compared to previous railway and radio technologies, the entry barrier for internet technology was significantly lower. It didn't require hiring workers to build railways or lay cables, nor did it require government permits. As long as you understood the relevant internet knowledge, you could do whatever you wanted. The massive wealth effect, combined with low entry barriers, kicked off a carnival in the capital markets.

At the very beginning of the bubble, the capital market maintained a certain level of caution. However, when they saw that rudimentary products born in "garages" like Yahoo and Google could also make a fortune through advanced business models, they realized that the old market valuation logic seemed to be failing. Coupled with the rapid price increase of various internet tech stocks, investors had long thrown their previous skepticism out the window. Ultimately, for fundamental investors, the valuations in the TMT sector were already artificially inflated without restraint or selection, and almost everyone thought this was perfectly fine.

As corporate valuations became bolder, professional analysis standards also began to warp. Typically, the higher the stock price, the higher the valuation analysts relying on profit statements tended to give. To ensure the rationality of the valuation, when the original profit anchor could no longer support the current price, the valuation benchmark gradually shifted from profitability to revenue, and then further broken down into concepts like "click-through rate" and "retention rate." Using these concepts, they analyzed a company's market prospects for the next few years. The entire logic seemed reasonable, but its most fatal flaw was, in the absence of historical precedent, how could one ensure the effectiveness of the business model analysis? The only prerequisite was to listen to the analysis of the founding team, i.e., "telling a story."

Eventually, people stopped paying for technological