Walsh’s debut: Dot plot remains, but the Fed may have already changed

- Key Takeaway: In his first FOMC meeting, new Fed Chair Walsh signaled a shift in communication framework towards a "data-dependent" decision-making approach by omitting his own dot plot and offering vague policy guidance. This led the market to reprice the rate path and triggered a downward adjustment in risk appetite.

- Key Elements:

- The rate decision held steady this time, but the focus was on Walsh's first policy communication, which the market had already fully priced in.

- Only 18 of the 19 FOMC members submitted dot plots; Walsh himself voluntarily abstained, aiming to diminish the significance of this mechanism as a forward guide.

- Walsh emphasized data dependency and meeting-by-meeting decision-making, opposing frequent signaling of future policy, thus altering the communication model of the Powell era known for its transparency.

- Following the decision, the market reassessed the policy reaction function. Some interest rate futures pricing began to discuss scenarios for the earliest possible rate hike again around October 2026.

- All three major US stock indices fell, with the S&P 500 (-1.2%) and Nasdaq (-1.3%) declining over 1%, indicating a significant cooling of risk appetite.

Original: Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

In the early hours of June 18, Beijing time, the Federal Reserve officially announced its latest interest rate decision. As expected, the federal funds rate remained unchanged within the established range, in line with market expectations.

Over the past few weeks, market pricing showed little dispute over the rate path, and the market had already fully priced this in. Therefore, the real focus of this rate decision was not "whether to cut rates," but rather how the new Fed Chair, Kevin Warsh, would conduct his first policy communication — This was Warsh’s first FOMC meeting as Chair, and the first opportunity for the market to observe how he will shape the monetary policy communication framework in the coming years.

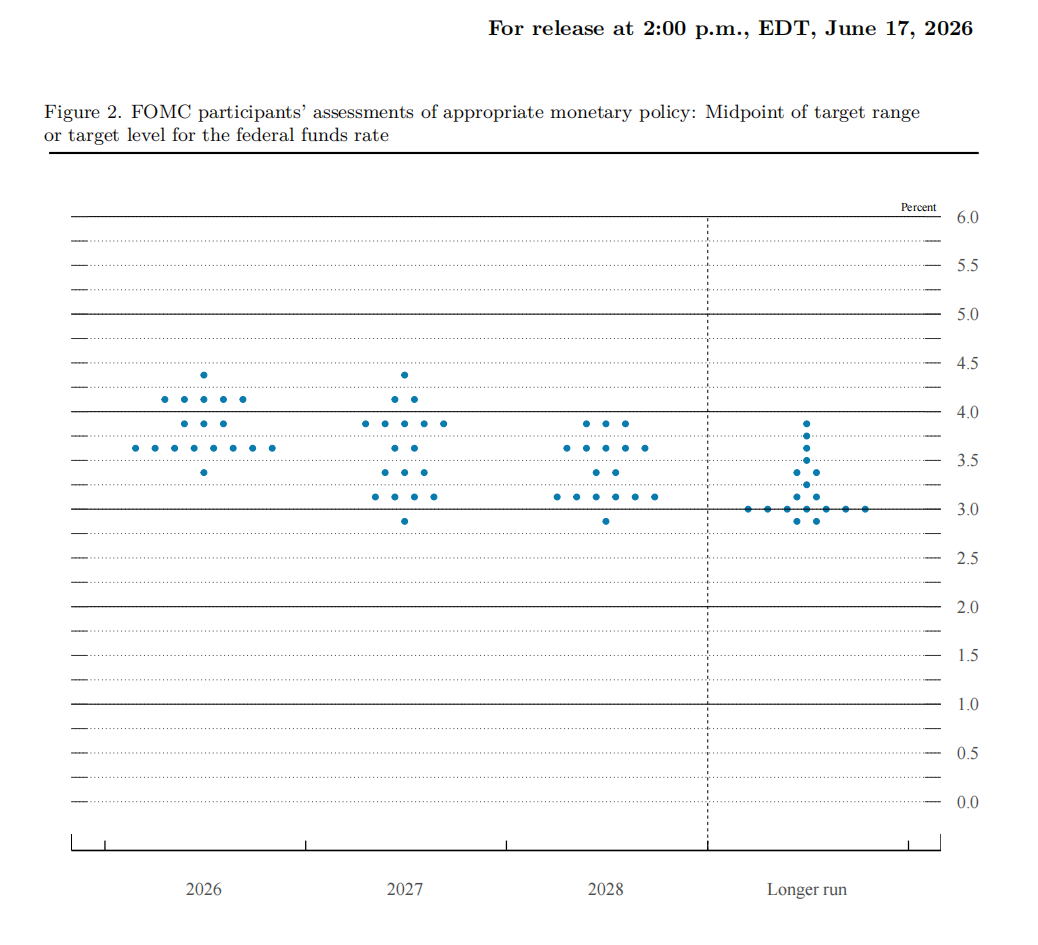

The Dot Plot Remains, But Warsh Himself is Absent

The most discussed change from this meeting came from the structure of the economic projections and the dot plot itself.

- Odaily Note: The so-called "Dot Plot" is the Fed's quarterly published interest rate projection tool, where each dot represents an FOMC member's expectation for the future federal funds rate. Although these projections are not formal policy commitments, because they reflect the collective judgment of policymakers on the economic and inflation outlook, the dot plot has long been regarded by the market as a key reference for interpreting the direction of Fed policy.

In the latest FOMC economic projections, only 18 out of 19 Fed officials submitted dot plot projections. Among them, one official anticipated a cumulative rate hike of 75 basis points for the remainder of 2026, five anticipated a cumulative 50-basis-point hike, three anticipated a 25-basis-point hike, eight anticipated keeping rates unchanged, one anticipated a cumulative 25-basis-point cut, and one was absent.

Warsh later acknowledged during the press conference that it was he who did not submit a rate projection. Warsh explained: "I did not put forward any of my own projections. This is consistent with my long-held view, at least regarding its current structure."

In contrast to his predecessor Jerome Powell's highly transparent and frequent communication style, Warsh has long been a proponent of "saying less." He has repeatedly expressed skepticism about "the effectiveness of the dot plot," "excessive forward guidance," and "frequent signaling of policy intentions." In Warsh's view, the Fed does not need to tell the market every step of its future path but should make decisions based on real-time economic data.

Although the market once speculated that Warsh might push for reforming or even abolishing the dot plot mechanism, it was not directly eliminated at this meeting. However, Warsh's own absence still sent a clear signal — the Fed is downplaying the guiding significance of the dot plot.

A Subtle Shift in the Fed's Communication Framework

During the press conference, Warsh also stated that the Fed will implement a series of reforms in the future, including establishing multiple specialized task forces to explore more open data collection methods and study improvements to the Fed's existing statistical indicator system.

In the subsequent Q&A session, when pressed by reporters about whether the next step would be a rate hike and whether current rates are restrictive, Warsh repeatedly refused to provide clear guidance.

Over the past decade, a core capability of the Fed has been to continuously reduce market uncertainty through the dot plot, the Summary of Economic Projections (SEP), and press conferences. The market's intense focus on the Fed's every move essentially stems from the fact that it provides a "predictable path."

But Warsh's stance is changing this logic. Clearly, Warsh emphasizes data dependence, making decisions on a meeting-by-meeting basis and maintaining a more restrained expression regarding the future path.

If this tendency continues, the market will face a structural shift — The Fed will no longer attempt to "explain the future" but will only describe its "current assessment." This will directly weaken the certainty function of forward guidance.

Rate Hike Expectations Rise, Market Risk Appetite Declines

Following the rate decision, the market quickly repriced the policy path.

After Warsh emphasized that the "central bank will not tolerate high inflation," the market began to reassess the upper bound of the Fed's policy reaction function, i.e., whether there is a possibility of more aggressive tightening than previously anticipated if inflation does not fall significantly.

This change was first reflected in short-dated assets.

Traders began to bet again on a higher terminal rate path. Pricing in some interest rate futures contracts indicated that the market is already discussing the scenario of another rate hike as early as around October, without ruling out the tail risk of a more aggressive path. Polymarket probability data also rose in tandem, reflecting that market pricing for a "re-tightening window" is opening.

U.S. stocks fell sharply after the decision. All three major indices closed lower, with the S&P 500 (-1.2%) and Nasdaq (-1.3%) both falling over 1%. Tech stocks led the decline, and market risk appetite cooled significantly.

Structurally, this adjustment was not a single-factor-driven "rate hike shock," but a more typical triple repricing:

- Short-term rates rising: The path for rate hikes was reopened;

- Risk asset pullback: Valuation sensitivity to interest rates amplified;

- Dollar strengthening + yield curve volatility: Reflecting increased policy uncertainty.

Importantly, the market is not simply trading "economic weakness" or "the disappearance of rate cut expectations," but rather a more complex logic: Under Warsh's new communication framework, the inflation constraint has been re-elevated, and the "upside tail risk" of the policy path is becoming more real.

In other words, if inflation does not fall quickly, will the Fed pivot back to tightening sooner and faster than the market originally expected?

Warsh's Pivot May Just Be Beginning

In summary, if one only looks at the outcome of this meeting, the Fed did not make a drastic pivot. Rates remain unchanged, the dot plot still exists, and the system continues to operate. However, if the focus shifts from the "policy path" to the "communication style," change is already evident.

Warsh's debut was more like a signal test. He did not scrap old tools, but he also did not rely on them entirely. He chose to "weaken their effect and reduce their weight."

Looking at the longer-term implications, the biggest question left by this debut is not "whether the Fed will raise rates next," but "when the Fed stops spoiling the market path, how will the market reprice the world?"