Không nên định giá ETH dựa trên phí giao dịch nữa, "Logic Kho Báu" mới là tương lai?

- Quan điểm cốt lõi: Ethereum không nên được xem là một doanh nghiệp tạo doanh thu từ phí giao dịch, mà là một "kho báu" bảo vệ khoảng 250 tỷ USD tài sản tiền mã hóa. ETH là "ổ khóa" bảo vệ kho báu này, giá trị của nó trực tiếp quyết định cấp độ an toàn của kho báu. Vốn hóa thị trường hiện tại của ETH đang bị định giá thấp nghiêm trọng, giá hợp lý nên cao hơn nhiều so với giá thị trường.

- Các yếu tố then chốt:

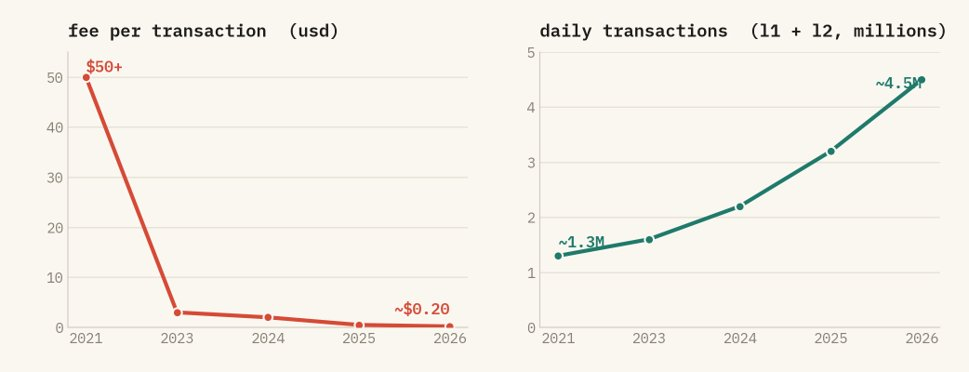

- Phí giao dịch là ma sát của mạng lưới chứ không phải doanh thu. Phí giao dịch đơn lẻ của Ethereum đã giảm từ hơn 50 USD xuống còn 0,2 USD, nhưng khối lượng giao dịch lại tăng gấp ba. Dấu hiệu của một mạng lưới thành công là đưa phí về 0.

- Sau khi chuyển sang Proof of Stake (Bằng chứng cổ phần), chi phí tấn công gắn liền với giá trị của ETH. Kiểm soát 33% và 66% ETH đang staking có thể làm tê liệt hoặc giả mạo mạng lưới. Chi phí cho hành vi xấu được tính bằng ETH và hành vi xấu đồng nghĩa với việc ETH bị tiêu hủy.

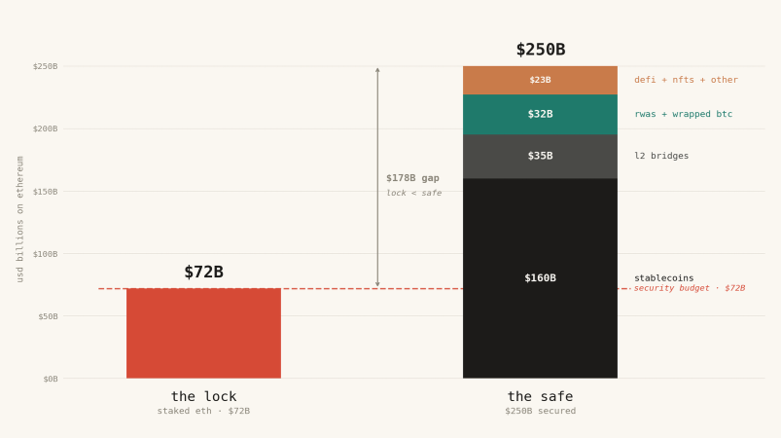

- Tài sản trên chuỗi Ethereum khoảng 250 tỷ USD, nhưng giá trị ETH được staking để bảo vệ tài sản đó chỉ là 72 tỷ USD. Tỷ lệ an toàn (khóa : két sắt) mất cân bằng nghiêm trọng, giống như dùng một ổ khóa hỏng để bảo vệ thỏi vàng.

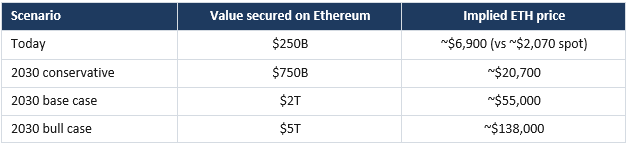

- Theo mô hình, để bảo vệ tài sản hiện tại, giá hợp lý của ETH phải là 6.900 USD (hiện tại khoảng 2.070 USD). Khi tài sản trên chuỗi tăng lên hàng nghìn tỷ USD, ETH sẽ cần tăng lên hàng chục nghìn USD.

- Tính bảo mật của Ethereum là tự cung tự cấp, hoàn toàn khác biệt với Linux hay DTCC phụ thuộc vào luật pháp bên ngoài hoặc sự bảo lãnh của cộng đồng. ETH không thể có giá trị bằng 0, nếu không chuỗi sẽ không có bảo đảm an toàn.

Original Author: Tom Dunleavy, Venture Partner at Varys Capital

Original Translation: Yuliya, PANews

Editor's Note: The current market broadly treats Ethereum as a traditional enterprise, calculating its P/E ratio based on the fees it generates, and concluding that it is overvalued. However, Tom Dunleavy proposes a completely different framework: fees are not revenue, but network friction; Ethereum is not a company, but a "vault" protecting hundreds of billions of dollars in assets, and ETH itself is the lock. Below is a translation of the original article:

TLDR

- Stop valuing Ethereum based on fees. Fees are actually a hindrance; a successful network will inevitably try to reduce them to zero. ETH fees have dropped from over $50 at their peak in 2021 to around $0.20 today, yet transaction volume has more than tripled. The crash in fees indicates massive network success, not imminent decline.

- With the transition to Proof-of-Stake (PoS), ETH has become the lock protecting the asset vault. To attack Ethereum, you need to control the staked ETH. Controlling one-third can halt the network, controlling two-thirds can rewrite the ledger. Either way, the cost of malicious action is denominated in ETH, and if you act maliciously, your ETH is destroyed by the protocol. This inextricably links ETH's value to the network's security. No network operated this way before staking.

- Ethereum currently hosts approximately $250 billion in assets on-chain (including stablecoins, tokenized assets, cross-chain funds from L2 networks, etc.), but the staked ETH securing these assets is only worth about $72 billion. This is like using a cheap, flimsy lock to protect a safe full of gold bars. Logically, the fair price for ETH should be around $6,900 (currently $2,070). If on-chain assets grow to trillions in the future, ETH's price must rise to tens of thousands of dollars to justify its security responsibility.

- Saying "Ethereum is like a free Linux system" or "like the DTCC" is incorrect. This is because the security of Linux and the DTCC is borrowed from elsewhere (e.g., the open-source community's goodwill, or government and bank legal guarantees). But Ethereum buys its own security using its native token, ETH. Therefore, ETH must be valuable, while Linux does not need to be.

- If ETH fails, Crypto will likely fail too.

Fees Are Not Revenue, They Are Friction

Last week, Bankless founder David Hoffman announced he had sold all his ETH, causing a stir in the crypto community. While I respect David's decision, I believe the way most people evaluate ETH and other PoS public chains is outdated. I've discussed my new framework with many people on various shows, but it seems not to have resonated (perhaps due to my articulation), so today I'm laying it all out in one go.

New things require new perspectives. Let me introduce a brand new ETH valuation model.

Many people treat Ethereum as a company and the fees it collects as its revenue. Seeing fees decline, they conclude the "company" is failing and the token is overpriced. This completely reverses cause and effect. Once you understand this, you'll never see it the same way again.

In reality, fees are like taxes; the higher they are, the less people want to use the network. Lowering fees encourages more participation, leading to more on-chain applications and capital. The data doesn't lie: individual transaction fees have dropped from over $50 in 2021 to around $0.20 today, yet transaction volume has hit all-time highs, more than triple that of 2021, with L2s now handling roughly 85% of transactions. It's cheaper to use, so more people use it. A successful settlement network should naturally drive its toll fees towards zero.

Ethereum's fees have crashed while transaction volume hits new highs. It has become cheaper, and more people are using it. L2s now handle approximately 85% of the throughput.

So, if fees are the wrong metric, what is the right one?

Ethereum is a Giant Vault, ETH is the Lock

Stop thinking of Ethereum as a company. Think of it as a massive, super-secure vault. This vault holds roughly $160 billion in stablecoins, $20 billion in RWAs (like US Treasuries, money market funds, and private credit), and $35 billion in assets bridged to L2s, which inherit Ethereum's consensus by design. Additionally, there's about $12 billion in wrapped Bitcoin, and roughly $20 billion distributed across DeFi positions, NFTs, and on-chain treasuries. In total, on-chain assets amount to approximately $250 billion, and this figure is growing every quarter.

A vault's security depends entirely on its lock. And everyone seems to be miscalculating the value of this lock. On Ethereum, the lock is made of ETH.

Under the old Proof-of-Work (PoW) system, you secured the network with mining hardware. The lock was purchased externally, and its cost was unrelated to the token's value. But with staking (PoS), everything changed. To attack Ethereum now, you must buy and control the staked ETH. The lock is made of the token itself. This means the security level of the vault and the market price of the token are one and the same. You cannot separate them.

The Current State: Lock Cheaper Than the Safe

This is the issue the market is ignoring. Today, the total value of all staked ETH securing Ethereum is only about $72 billion. Yet, the assets it protects amount to $250 billion. The safe contains more than twice the value of the lock securing it.

This is dangerous. If what you are protecting is worth more than the cost to break in, your vault is inadequate. For Ethereum to securely protect this $250 billion, the defensive capital (staked ETH) must be greater than $250 billion, not less than one-third of it.

Currently, only about 30% of ETH is staked. So, just to make this 30% staked portion equal to the on-chain assets, the total market cap of ETH would need to be over three times the on-chain assets (1 divided by 0.30). Right now, ETH's market cap is roughly equal to (about 1x) the assets it protects. But according to my logic, it should be over 3x. Using the current $250 billion figure, the fair price for ETH should be around $6,900, not the current $2,070. This means, even without any capital inflows, based solely on the assets it currently protects, ETH's price should more than triple. This is very close to the directional model of BitMine Chairman Tom Lee.

"But Circle can freeze USDC, so it doesn't need ETH for protection."

Every time I make this argument, someone counters with this, but it's completely wrong. Here's why:

The idea is that if Ethereum were attacked, Circle, the issuer of USDC, could simply freeze the attacker's addresses and reissue the coins. Therefore, those hundreds of billions shouldn't be counted in Ethereum's security responsibility.

But consider this: Circle's freezing mechanism operates through a smart contract that executes on Ethereum and depends on Ethereum's ledger. If Ethereum's consensus is broken, there is no single canonical chain for the freeze mechanism to function on.

Furthermore, Circle could have chosen not to use Ethereum and built its own private database instead. They chose Ethereum for its neutrality, deep liquidity, and composability with other projects. The trade-off for these benefits is that USDC's fate is now intertwined with Ethereum's security. You can't enjoy the advantages without accepting the dependency risk.

Also, people often assume attackers want to steal USDC. That's not the point. If Ethereum collapses, that $150+ billion isn't stolen; it becomes trapped on a chain without consensus, unable to be redeemed, throwing all loans and transactions built on it into chaos. The value of these assets isn't taken by the attacker; it's destroyed. Destroyed value is a critical factor in security considerations.

An attacker doesn't even need to steal money to profit. They could short ETH, short the entire ecosystem, or be a hostile state that benefits from crippling the network. The more value held on-chain, the greater their incentive to disrupt it. Therefore, our security budget must scale with the total assets on-chain, not just the fraction a thief could plausibly steal.

If you place your money on Ethereum, you are consuming its security, regardless of whether you have a "freeze" button. All money must be accounted for.

"Ethereum is just Linux" or "Ethereum is the DTCC."

Here is another favorite counter-argument from smart people.

- First Argument: Ethereum is like Linux. It's the underlying infrastructure powering a vast network, but as an asset, it's worthless. Open-source infrastructure is a free public good. Value is captured by applications running on top, not by the base protocol. Therefore, ETH will be incredibly important but completely valueless.

- Second Argument: Ethereum is like the DTCC (Depository Trust & Clearing Corporation), the infrastructure behind almost all US securities trades. The DTCC processed $3.7 quadrillion in transactions in 2024, earning ~$2.5 billion in revenue, but profit was under $500 million. It's critical, regulated, but its value is a tiny fraction of the transactional value it handles. Infrastructure is a cost center. Even if you can't live without it, and even if Ethereum processes trillions, it will only capture a sliver of utility profit. That's it.

Both arguments fail for the same reason.

Linux and the DTCC both borrow their security from external sources. Linux relies on the open-source community, its reputation, and decades of code review. The DTCC relies on US law, federal regulators, and guarantees backed by major banks using US Dollars and Treasuries. Their security exists outside the system. This is precisely why the DTCC can settle immense wealth while capturing almost no value. It's a member-owned utility designed to run at cost. It doesn't need a valuable token because trust is provided by governments and banks.

Ethereum has no such external protection. No government enforces it. No member banks backstop it. No law can reverse a fraudulent settlement. The only barrier between Ethereum and an attacker is the market value of the staked ETH used to secure it. Ethereum must purchase security on the open market, with its own asset, for every single block.

That is the fundamental difference. Linux is software; no one is required to own a scarce asset to run it. The DTCC posts collateral in USD, external to itself. Ethereum's collateral is ETH, internal to itself. You cannot commoditize it to zero because security is not a line of code; it is a quantity of value that must be locked and placed at risk. Strip away ETH's value, and you haven't built a leaner Linux. You have built a chain with no collateral, and no one will trust a single dollar to it.

So, stop comparing Ethereum to Linux or the DTCC. Compare it instead to the dollars and Treasuries sitting behind the DTCC. No one values the US Dollar based on the fees the DTCC charges. You evaluate the clearinghouse's fees separately, and value the Dollars and Treasuries acting as the system's collateral as a monetary base worth trillions. ETH is not the clearinghouse. ETH is the collateral building the clearinghouse. That is the asset you are buying.

Linux never needed a treasury. Ethereum's security budget is a treasury, and it is denominated in ETH.

Looking Ahead and Market Dynamics

Follow this line of thinking. This model ignores fees or market hype entirely. It focuses on one core question: How much money will settle on Ethereum in the future? And to protect that money, how valuable must ETH be?

Stablecoins are poised to break $1 trillion in the coming years. RWA tokenization is projected to reach several trillion by 2030. Coupled with various on-chain applications, the assets Ethereum needs to protect will skyrocket from the current $250 billion to trillions. As long as that "more than 3x" security ratio is maintained, you can calculate how high ETH's price must rise as capital flows in.

Even if you're pessimistic and lower the security ratio, it doesn't matter. On-chain capital is growing (the variable), and the security ratio (the leverage) – no matter how you calculate it, the direction is consistently upward.

"This is blind optimism. The market will never price it this way."

This is the most reasonable counter-argument. Indeed, I'm talking about what ETH should be worth, not what the market will price it at right now. There's no forced arbitrage mechanism to close the gap. And frankly, my "ETH should go up" thesis has been wrong for the past few years in terms of price action. Let's address each point.

- On what bridges the gap: Ethereum isn't about arbitrage; it's about demand for the system's reserve asset. As value settles on Ethereum, ETH is used as collateral, as a trading pair asset, and is staked to earn the network's base yield. This demand grows with the activity it supports. Reserve assets are not priced on earnings; they are priced on how urgently the surrounding system needs to hold them. Gold is worth over $18 trillion and produces zero cash flow. ETH is the reserve asset for on-chain finance, and this framework merely measures how large that reserve must be.

- On the staking multiple: My mental model treats the staking multiple as a range, not a fixed target. At current staking rates, parity (staked ETH equals protected value) requires about a 3.3x multiple. A reasonable range spans from a loose end of 1.7x to a strict end of 5x, where the cost of an attack via a two-thirds staking share must equal the entire protected value. The price tracks protected value at some multiple within this corridor. Pinning it to one specific number destroys nuance, which is where reasonable people can disagree without breaking the model.

- On reflexivity: The model does have more than one equilibrium point, and nothing decisively selects the highest one. Today, Ethereum is secure enough below the coverage floor because acquiring one-third of the staked share is highly illiquid, slashing conditions are brutally severe, and the social layer can fork out an attacker. These are real defenses, but they determine whether an attack succeeds, not whether the coverage is sufficient as risk escalates. Thin coverage is tolerable at $250 billion. When it involves two or five trillion in regulated institutional capital, coverage is no longer an academic question. The gradient for closing the gap increases monotonically as adoption rises.

Finally, the most damning point is ETH's price over the last 5 years. Logically it should rise, but in reality, it has been declining. I think the main reason is: previously, the value on-chain wasn't large enough for people to see security as a major problem. With only $50 billion on-chain, nobody cared; at $175 billion, people started to feel something was off; by the time it reaches $1 trillion, the first question major institutions will ask before entering is: "Is this chain secure?" And the answer to that question is entirely dependent on the price of ETH. My model can't predict when the price will rise, but it tells you that as on-chain capital grows, the pressure for this rise intensifies, and the fact that "on-chain capital is growing" is something even the bears can't deny.

Some use Bitcoin as a counter-argument, pointing out that its security budget is tiny compared to its market cap. But Bitcoin primarily protects itself. Ethereum protects other people's dollars and various assets; that's a much heavier responsibility! And the trends are already clear: more and more ETH is being staked, compliant products are constantly buying ETH, and the burn mechanism is continuously destroying ETH as the network activity increases. These all confirm the demand growth I'm describing.

Those who only focus on fees and cash flow will continue to claim ETH is overvalued. They have the cause and effect completely backward. On-chain activity comes first, creating the need for security. ETH must be valuable to safeguard the entire ecosystem's security. Fees are a hindrance you should strive to eliminate, not a metric to use for valuing ETH.