Tái cấu trúc nửa cuối: Vàng nhường chỗ, Bitcoin khi nào lên sàn?

- Quan điểm cốt lõi: Tỷ lệ Bitcoin/Vàng đã chạm đáy vào tháng 2 năm 2026, sau đó phục hồi 46% nhờ vàng điều chỉnh giảm. Golden Cross trên khung tuần dự kiến hình thành vào tháng 6, giúp Bitcoin vượt trội hơn vàng trong nửa cuối năm, nhưng bối cảnh vĩ mô phức tạp hơn do lạm phát cao, Fed diều hâu và xung đột địa chính trị.

- Các yếu tố chính:

- Tỷ lệ Bitcoin/Vàng phục hồi từ mức đáy 12,5 hồi tháng 2 lên 17,6, chủ yếu do vàng giảm 18% từ mức đỉnh lịch sử 5.589 USD, chứ không phải do Bitcoin tăng mạnh.

- Golden Cross trên khung tuần (EMA 9/21) dự kiến hình thành vào tuần đầu tiên của tháng 6 năm 2026. Dữ liệu lịch sử cho thấy sau Golden Cross, tỷ lệ có thể tăng từ 148% đến 641%.

- Lạm phát CPI của Mỹ đạt 3,8%, kỳ vọng cắt giảm lãi suất của Fed tan vỡ. Chủ tịch Fed mới, ông Warsh, nhậm chức vào tháng 5, thị trường chuyển sang định giá diều hâu, làm suy yếu hỗ trợ thanh khoản cho sự tăng giá của Bitcoin.

- Ngân hàng Trung ương Trung Quốc đã mua vàng trong 17 tháng liên tiếp, tổng lượng nắm giữ đạt 2.313 tấn, tỷ trọng mở rộng lên 9,6%. Các ngân hàng trung ương toàn cầu tiếp tục có nhu cầu mua vàng, tạo hỗ trợ đáy cho giá vàng.

- Bitcoin phục hồi ổn định từ 65.000 USD lên quanh 80.000 USD. Cấu trúc nắm giữ thị trường lành mạnh hơn, nhưng sự phục hồi vẫn phụ thuộc vào sự suy yếu của vàng, chưa chuyển sang giai đoạn tăng giá dẫn dắt bởi Bitcoin.

- Mâu thuẫn cốt lõi nửa cuối năm là cuộc đối đầu giữa chính sách diều hâu của Fed và nhu cầu tất yếu về nới lỏng tài khóa. Cuộc gặp thượng đỉnh Mỹ-Trung và khả năng hạ nhiệt căng thẳng Mỹ-Iran có thể là sự kiện xúc tác cho sự trở lại của khẩu vị rủi ro.

- Tỷ lệ hiện tại vẫn còn dư địa phục hồi rất lớn so với mức đỉnh 31,5 vào tháng 10 năm 2025. Trong kịch bản bảo thủ (Bitcoin 80.000-100.000 USD, vàng 4.200-4.700 USD), tỷ lệ có thể tăng lên 19 đến 21,3.

Original author: that1618guy, Analyst at Delphi Digital

Original compilation: Chopper, Foresight News

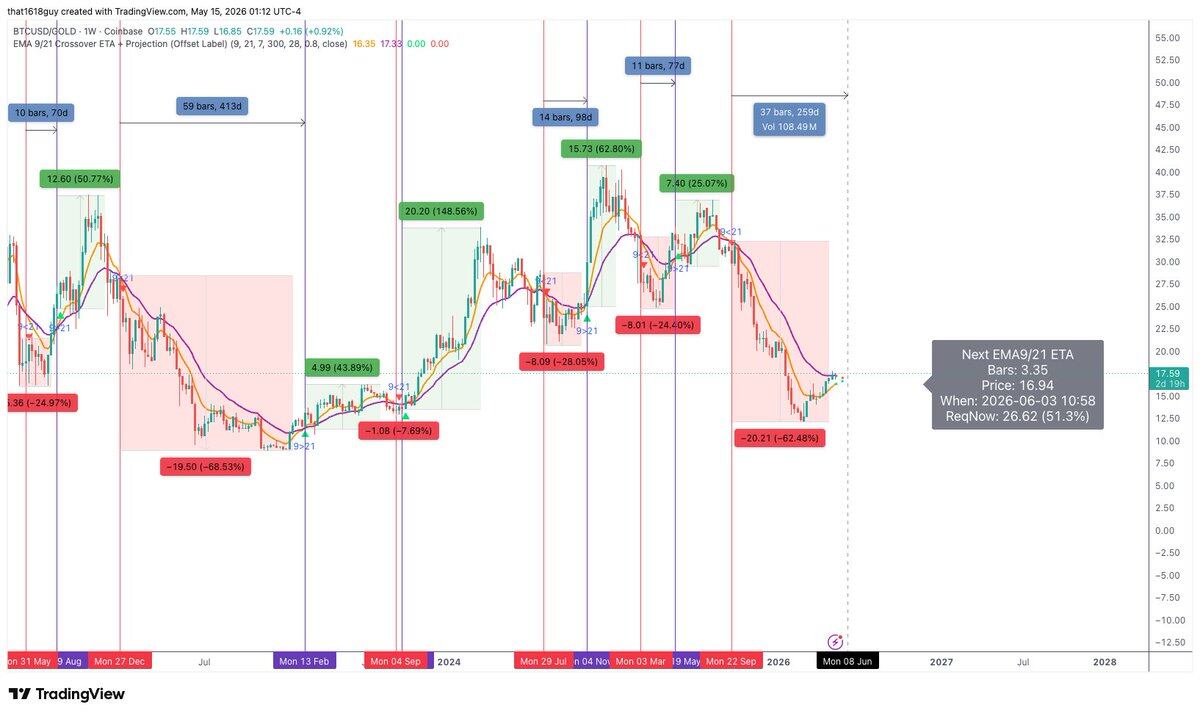

Three months ago, I published the article "Bitcoin vs. Gold: Positioning for the Next Relative Cycle" with a very clear core thesis: under the weekly 9/21 Exponential Moving Average (EMA) framework, the Bitcoin/Gold ratio had fallen into the second-largest retracement in history, suggesting a bottom was approaching based on the data. (Note: The weekly 9/21 EMA is a commonly used combination by trend traders to determine trends and identify reversal points.)

This judgment has now been validated. The ratio has recovered approximately 46% from its February low. Gold has corrected 18% from its all-time high of $5,589, while Bitcoin has steadily climbed from the $65,000 range back to around $80,000. The key confirmation signal, a bullish weekly 9/21 EMA golden cross, is currently projected to form in the first week of June. Historically, following a deep bearish death cross that transitions into a golden cross, subsequent ratio gains have been 148%, 641%, and 148%, respectively.

However, the macroeconomic environment has changed dramatically. Current inflation stands at 3.8%, completely dashing expectations for a Fed rate cut. The US-Iran conflict continues to escalate. Furthermore, Kevin Warsh officially assumed the role of Fed Chair on May 13. The market landscape for the second half of 2026 is far more complex than in February, but the overarching trend of Bitcoin strengthening relative to Gold remains unchanged.

This article will review the previous forecast for the Bitcoin/Gold ratio, assess how the views on Gold and the macro market from "2026 Annual Market Outlook" have played out, and update the analytical framework for the second half of the year.

Bitcoin/Gold Ratio Recovery Underway

When the article was published at the end of February, the Bitcoin/Gold ratio languished between 12.5 and 13, an extreme historical low. Bitcoin was trading around $65,000, while Gold had surged to $5,100 following a massive rally.

Today, the ratio has risen to 17.6, significantly up from its lows. This recovery has been entirely driven by the first scenario: Bitcoin hasn't seen a violent rally; instead, its relative strength comes from the price correction in Gold. This was the most overlooked market dynamic mentioned in my previous article. Few in the market realize that Bitcoin's recent outperformance of Gold is primarily fueled by Gold's weakness, which has been the reality since mid-February.

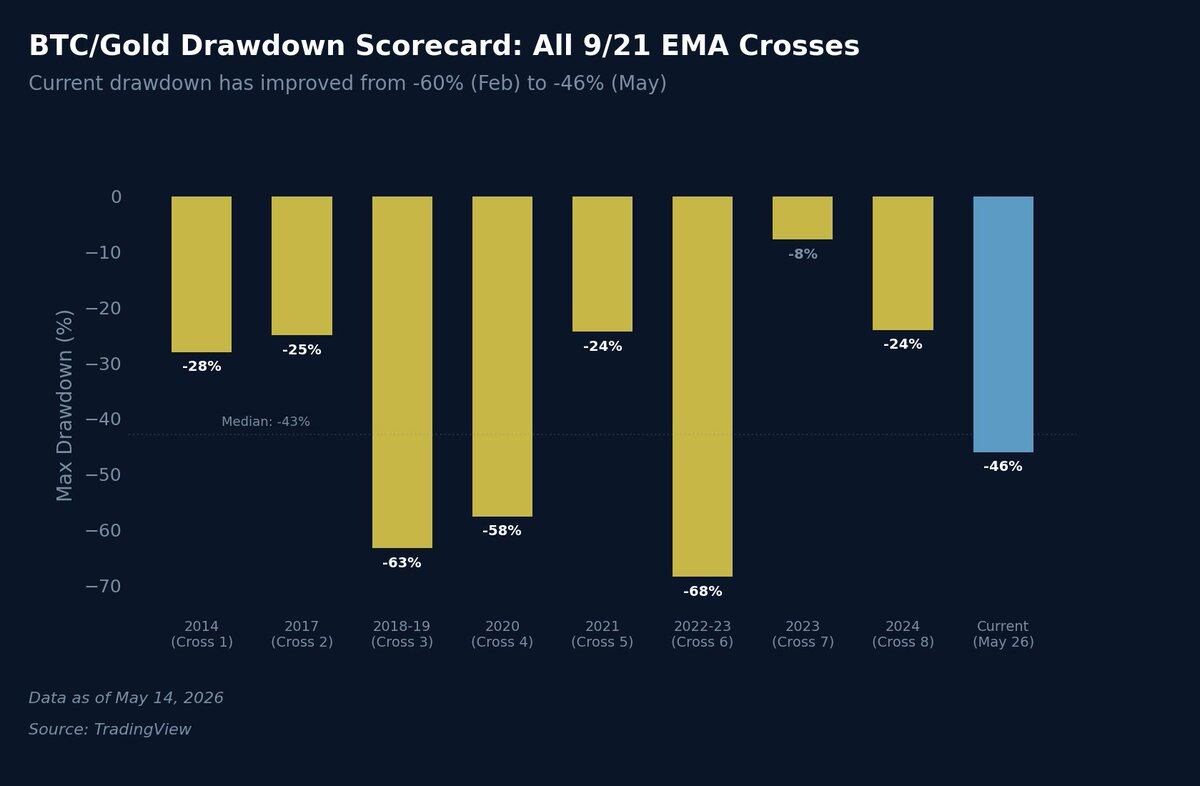

The retracement from the October 2025 high has narrowed from approximately 60% to 46%. While historically still deep, it has moved away from the extreme trough, falling from the second-largest historical retracement to a medium level.

Looking at eight historical downturns, only the 2018 bear market (63% retracement) and the 2022 bear market (69% retracement) saw deeper declines than the February lows. The current 46% retracement is now close to the historical median of 43%, showing significant market repair compared to the extreme lows three months ago.

The convergence of the 9/21 weekly EMAs, which I highlighted as a key point, hasn't fully materialized yet. Both moving averages are still in a bearish trend, but the gap between them is rapidly narrowing. Based on trading model projections, approximately 3.5 more weekly candles are needed for a bullish golden cross, landing around the first week of June 2026.

After the previous weekly death cross, the Bitcoin/Gold ratio plummeted 62%, closely mirroring the three historical deep death cross cycles (2018: -63%, 2020: -57%, 2022: -68%). This technical analysis framework holds true perfectly in downturns.

Similarly, the uptrend cycles offer strong reference points. Once a bullish golden cross is confirmed and holds, history shows a tendency for vigorous rallies. After the three deep death crosses, the subsequent golden crosses led to ratio gains of 148%, 641%, and 148%, respectively. Even in shallower correction cycles, golden crosses resulted in impressive gains of 25% to 62%.

A crucial caveat: not all moving average golden crosses are durable. A false breakout occurred in 2023, where the averages briefly crossed before quickly reversing, leading to a 7.69% decline in the ratio. This represents the smallest magnitude and shortest duration death cross in the data. Investors can use momentum indicators like MACD and RSI to gauge the strength of a golden cross and distinguish genuine signals from false ones.

I maintain my view that Bitcoin will continue to outperform Gold for the remainder of 2026, potentially extending into the first half of 2027. The core market question now is the magnitude of this upcoming rally, once the golden cross is confirmed and holds.

Reviewing the Annual Gold Outlook

In the "2026 Annual Market Outlook" report, when Gold was still trading in the $4,600 range, we flagged it as one of the asset classes most worthy of attention. We clearly identified solid structural tailwinds: continued central bank gold purchases (especially by the People's Bank of China), fiscal deficits exacerbating currency debasement, and the global trend of de-dollarization of foreign exchange reserves.

Gold subsequently surged, hitting an all-time high of $5,589 on January 28, 2026, a gain of over 26% from our forecast point. It has since corrected to around $4,700, a 16% decline from the peak. Three factors converged behind this reversal:

- In January, Kevin Warsh's nomination for Fed Chair quickly shifted market pricing towards hawkishness, triggering significant profit-taking after Gold's massive rally.

- The outbreak of US-Iran military conflict on February 28 pushed oil prices above $100/barrel, adding to inflationary pressures. The April US CPI inflation rate rose to 3.8%, the highest since May 2023, extinguishing hopes for Fed rate cuts. While Gold can hedge multiple risks, a prolonged period of high interest rates acts as a significant headwind for this non-yielding asset.

- Rising hawkish expectations drove a rebound in the US Dollar Index, further pressuring Gold prices.

As mentioned in the annual outlook, Gold's weekly RSI briefly exceeded 85, entering an extreme overbought zone rarely seen in modern history. We noted that short-term upward momentum would inevitably slow, likely giving way to a consolidation phase – a forecast that has fully materialized.

Gold's historic rally is now in a digestion and adjustment phase, but the underlying structural buying pressure hasn't collapsed. Short-term price action is merely being temporarily suppressed by shifting interest rate expectations and a stronger Dollar.

PBOC Continues Increasing Gold Reserves

The outlook regarding the PBOC's gold purchases from the annual report has also fully materialized. The report noted that the PBOC is one of the world's largest and most consistent gold buyers; China's continued accumulation is a key part of its national strategic layout, potentially using ample gold reserves to optimize its debt structure and build a cross-border RMB settlement system.

Since the annual report was published, the PBOC has increased its gold reserves for 17 consecutive months, reaching a total official reserve of 2,313 tons, accounting for 9.6% of total foreign exchange reserves (data from the World Gold Council). In March 2026 alone, the PBOC added approximately 5 tons of gold, marking the largest monthly increase in nearly a year.

Global central bank buying remains robust. In Q1 2026, net central bank gold purchases totaled 244 tons, higher than the previous quarter's volume and the five-year average. Goldman Sachs had previously forecast average monthly central bank purchases of 70 tons for 2026. The actual pace is slightly below that expectation (PBOC added just 1 and 1.2 tons in Jan-Feb), but the accelerated buying in March demonstrates that the central bank's purchase rhythm is dictated by actual market demand, not a gradual exit.

The most telling market signal is that the PBOC hasn't stopped buying even with Gold trading above $5,000. Historically, central banks often pause purchases or even sell after new highs. However, as we predicted, the aggressive buying continued through this price surge, proving this is a long-term structural strategic allocation, not short-term speculative hoarding.

This trend is deeply linked to the relative strength logic between Bitcoin and Gold. The PBOC's persistent large-scale gold purchases are essentially a statement on USD credit. Each ton of gold bought represents a ton of reserve assets moving away from the dollar asset system. The de-dollarization wave is accelerating.

Data from the World Gold Council's March 2026 survey shows that the proportion of central banks planning to increase their gold reserves within the year rose from 62% in 2025 to 68%. Against the backdrop of short-term bearish factors like the Fed's hawkish stance, a strong Dollar, and market fears of rate hikes suppressing Gold prices, structural central bank buying provides a solid floor for Gold. This limits Gold's downside, meaning further recovery in the Bitcoin/Gold ratio will increasingly depend on Bitcoin attracting capital inflows itself – the second scenario.

Year-to-Date Performance Review: Bitcoin vs. Gold

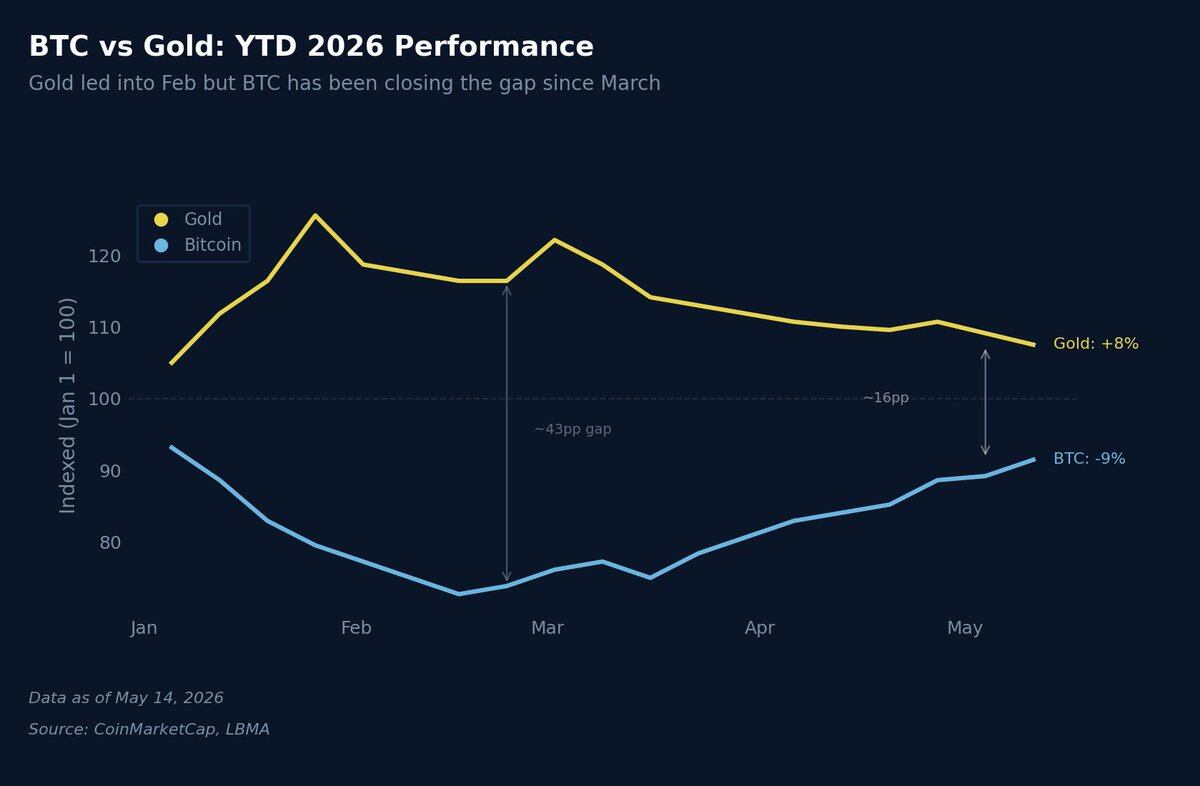

Measuring year-to-date (YTD) performance from January 1, 2026, the market moves are clear. Initially, Gold surged, with YTD gains reaching as high as 25% by the end of January. Over the same period, Bitcoin's YTD loss was around 25%. The divergence between the two assets reached an extreme, perfectly aligning with the time I predicted the ratio would bottom in February.

Since then, the trajectories have converged: Gold has given back most of its YTD gains, now holding only an 8% increase. Bitcoin has narrowed its YTD loss from a peak of 27% down to 9%. The performance gap between them has shrunk from 50 percentage points to 17 percentage points, a direct reflection of the ongoing real-time recovery in the Bitcoin/Gold ratio.

This trend has been achieved almost entirely through Gold weakening, not Bitcoin forcefully rallying. This carries significant implications for asset allocation strategy. The current market is dominated by the first scenario (Gold correction, Bitcoin sideways consolidation). The key suspense for the second half of the year is whether the market can transition to the second scenario (Bitcoin attracting capital for a rally) or will fall into a prolonged range-bound trading pattern.

Let's add a historical correlation observation: Past data suggests that Gold's movements and global M2 money supply changes tend to lead Bitcoin by 3 to 4 months. When Gold broke out in mid-2025, global M2 was also hitting new highs. According to this lag, Bitcoin should have followed higher in late 2025 or early 2026. But it didn't. The lag cycle extended to 5 or 6 months. This is not unprecedented; the 2020 pandemic shock also elongated the correlation cycle. Historically, such delays are often followed by violent price swings when correlation reasserts itself.

Currently, the US-Iran geopolitical conflict is playing a role similar to the pandemic, introducing a new round of inflationary pressure that directly delayed the Bitcoin rally that looser liquidity signals should have triggered.

What Has Changed Since February

Three months have passed since the previous report, and the market environment has materially changed. Here's a review of our previous forecasts:

Outcomes That Materialized

- The Bitcoin/Gold ratio bottomed as predicted within the forecast range, beginning its recovery fueled by Gold's correction.

- Gold's deep correction after its peak materialized as reality.

- The trend of global central banks continuously increasing gold reserves remained unchanged.

- The convergence pace of the weekly 9/21 EMAs largely aligned with our initial calculations.

Forecasts That Did Not Materialize

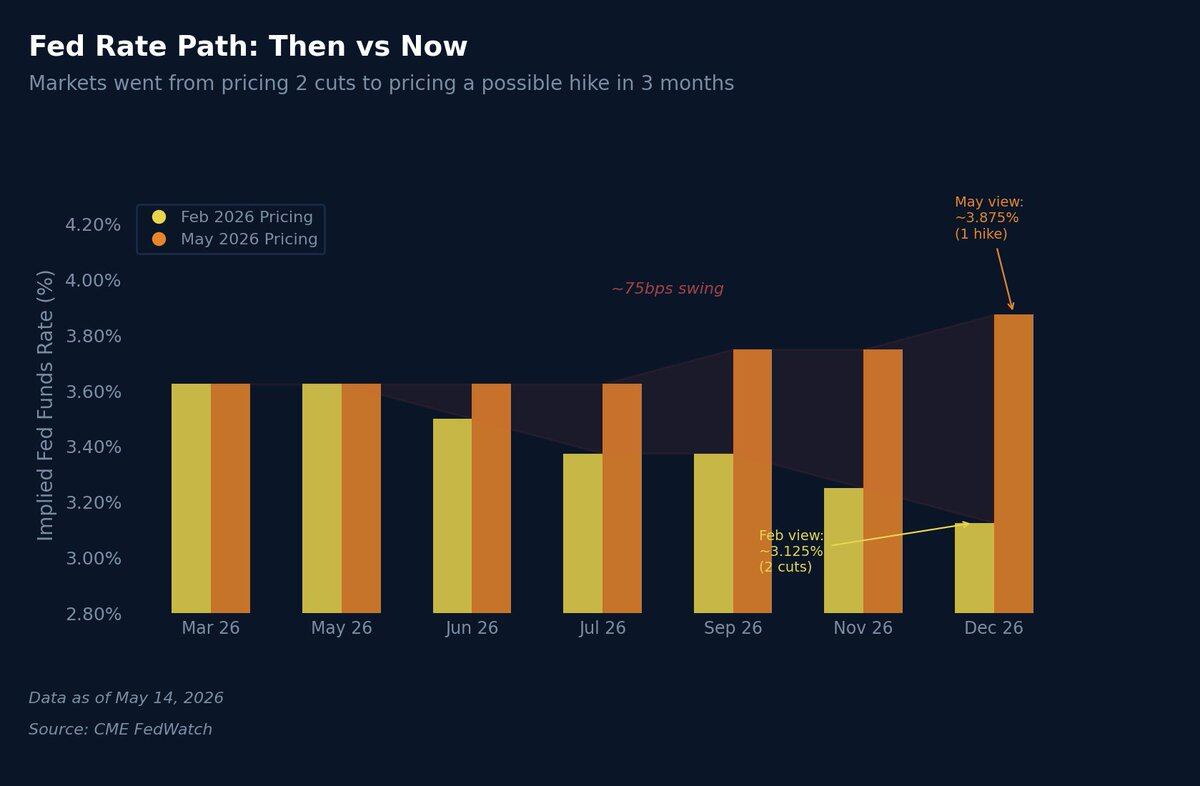

Expectations for Fed rate cuts have been completely dashed. In February, my base case was for 1-2 rate cuts in the second half of 2026, a view widely shared by the market at the time. This logic is now entirely invalid. With US CPI inflation at 3.8%, rising Producer Price Index (PPI), oil prices holding above $100, and the US-Iran conflict sustaining supply-side inflation, the market has not only abandoned rate cut expectations but is now pricing in the possibility of rate hikes by year-end. This is the biggest logical deviation in my thesis compared to before.

Interest rate market expectations have undergone a dramatic reversal. In February, the market projected the December 2026 Fed Funds Rate would fall to 3.125%, implying two cuts. Now, market pricing suggests rates will be flat or higher by year-end, with the implied rate near 3.875%. In just three months, the expected rate path has shifted by a staggering 75 basis points, driven primarily by the energy inflation shock from geopolitical conflict.

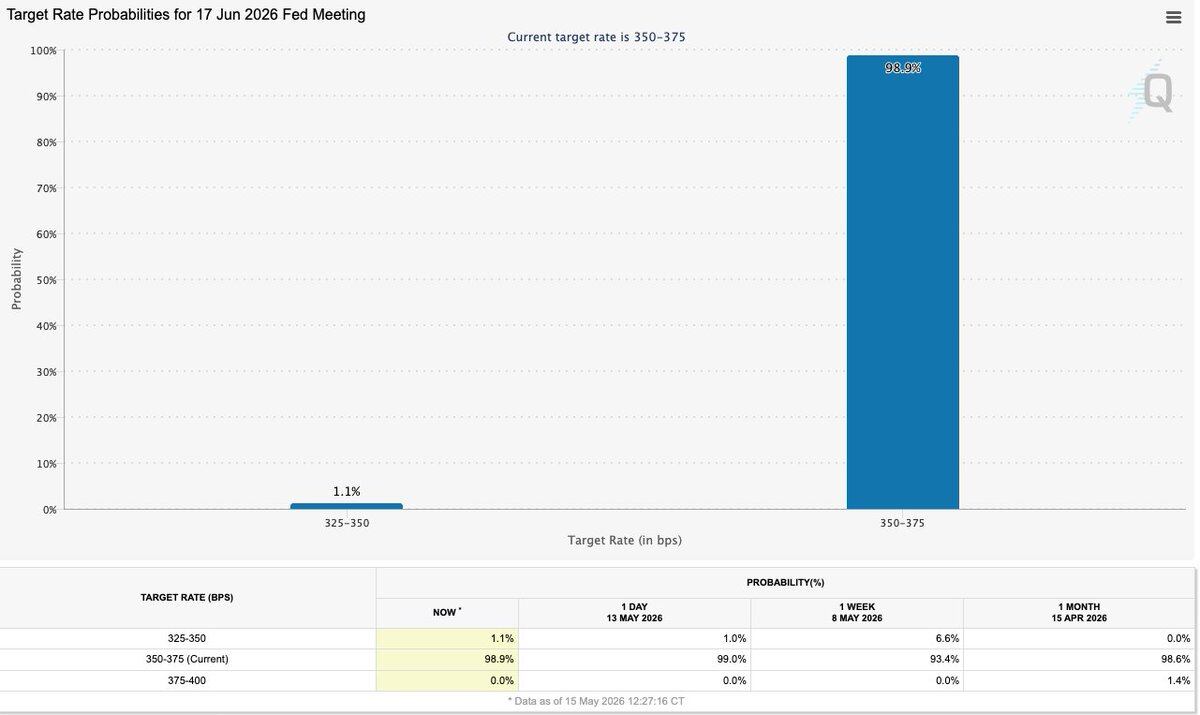

The Fed chair transition has also shattered the previous dovish expectations. The market assumed a new chair would lean dovish after Powell stepped down. Instead, Kevin Warsh is now in office, and his policy stance appears far more hawkish than Powell's. His first FOMC meeting is scheduled for June 16-17. Under his leadership, even if economic growth slows, the Fed is unlikely to embark on aggressive rate cuts, directly changing my previous thesis regarding a risk-on asset rotation in H2 2026. Current market models estimate the probability of a rate cut at this meeting is near zero.

However, the previously proposed fiscal dominance logic remains intact. The US continues to pursue debt monetization through the banking system. The annual fiscal deficit remains between $1.5 and $2 trillion. Regardless of the Fed's monetary policy stance, the sheer weight of fiscal pressure will eventually force more liquidity into the market.

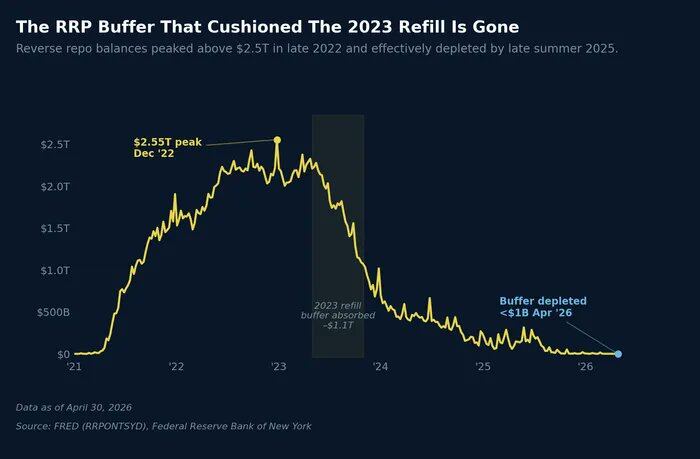

Total US national debt has now exceeded $39 trillion. The Treasury still needs the market to absorb a flood of new bond issuance. Hedge fund basis trades continue to provide support for the long end of the yield curve, and the Overnight Reverse Repo Facility (ON RRP) balance remains low.

Even if Warsh projects a hawkish tightening stance, the underlying operation of financial markets depends on liquidity support. The core contradiction to watch in the second half of the year is the tug-of-war between the Fed's hawkish monetary policy stance and the fiscal side's inherent demand for easy liquidity.

Overall Market Landscape for H2 2026

My core thesis remains unchanged: the Bitcoin/Gold ratio is recovering from extreme historical lows, and the overall trend is positively determined. The key drivers for the second half of the year are outlined below:

Gold Side

Gold's 18% correction from its all-time high has already provided ample room for the ratio's recovery. Even if Gold doesn't fall further and merely consolidates horizontally to digest its prior gains, the emergence of a positive catalyst could still drive the ratio higher, given Bitcoin's higher price elasticity. Combined with continued global central bank buying providing a solid floor, Gold's price bottom range is locked in between $4,200 and $4,500. This relative strength cycle does not require a sharp crash in Gold; it only needs Gold's rally to end.

Bitcoin Side

Compared to February, Bitcoin's market positioning is healthier. Since rallying from its low near $64,000, it has steadily climbed to around $80,000 over a dozen weeks. During this period, it successfully absorbed multiple bearish shocks including the US-Iran conflict, the Fed chair transition, and adjustments to inflation expectations, without making new lows.

I am closely watching the core catalyst of a potential meeting between US and Chinese leaders. Substantial progress on trade truce, coupled with de-escalation of the US-Iran situation, could quickly improve risk appetite. Current Bitcoin market positioning is low. If risk sentiment heats up, Bitcoin could see gains far outpacing other assets.