WallStreetBets: 24/7 Trading คือรูปแบบสูงสุดของตลาดการเงิน

- มุมมองหลัก: สนามแข่งระดับซูเปอร์ต่อไปของอุตสาหกรรมคริปโตคือการแปลงสินทรัพย์ดั้งเดิม เช่น หุ้น พันธบัตรรัฐบาลสหรัฐฯ และสินค้าโภคภัณฑ์ ให้เป็นโทเค็นบนบล็อคเชน ใช้บล็อคเชนเพื่อให้สามารถซื้อขายได้ตลอด 24 ชั่วโมง ลดความเสียดทาน และเพิ่มมูลค่าการใช้ประโยชน์ของสินทรัพย์ เพื่อเปลี่ยนแปลงช่องทางการลงทุนและรูปแบบการซื้อขายของประชาชน

- องค์ประกอบสำคัญ:

- กระแสการทำโทเค็นไนเซชันได้เปลี่ยนจากแนวคิดสู่การปฏิบัติ สถาบันการเงินดั้งเดิมอย่าง BlackRock, Franklin Templeton และ Robinhood ได้เปิดตัวผลิตภัณฑ์จริงแล้ว ซึ่งผลักดันการย้ายสินทรัพย์ดั้งเดิมขึ้นสู่เชน

- โทเค็นหุ้น (เช่น rNVDA, rTSLA) อนุญาตให้ซื้อขายสินทรัพย์ภายในบัญชีคริปโตได้โดยตรง และใช้พูลเงินทุนร่วมกับสปอตและตราสารอนุพันธ์ ช่วยเพิ่มประสิทธิภาพของเงินทุน แพลตฟอร์มอย่าง Bitget และ Robinhood เป็นผู้นำในการปรับใช้

- ผลิตภัณฑ์โทเค็นของสินค้าโภคภัณฑ์อย่างทองคำ (เช่น GLDY) สร้างดอกเบี้ยผ่านธุรกิจให้เช่า ซึ่งให้ผลตอบแทนเพิ่มเติมแก่ผู้ถือ และช่วยแก้ปัญหาจุดอ่อนที่ทองคำดั้งเดิมไม่มีกระแสเงินสด

- ระบบนิเวศ RWA บน Solana (เช่น โปรโตคอล Sunrise) มียอดซื้อขายสะสมเกิน 3.5 พันล้านดอลลาร์สหรัฐ โดยผลิตภัณฑ์โทเค็น SPCX มียอดซื้อขายเกิน 50 ล้านดอลลาร์สหรัฐภายใน 24 ชั่วโมงหลังจากเปิดตัว

- ตลาดสัญญา perpetual ได้ยืนยันถึงความต้องการที่แข็งแกร่งของนักเทรดสำหรับการซื้อขายตลอด 24/7 แพลตฟอร์มอย่าง Hyperliquid กำลังผลักดันให้โครงสร้างตลาดอื่นๆ เช่น ออปชัน ย้ายขึ้นสู่เชนมากขึ้น

- ความท้าทายหลักของอุตสาหกรรมได้เปลี่ยนจาก "สามารถทำโทเค็นได้หรือไม่" เป็น "จะรักษาผู้ใช้ไว้ได้อย่างไร" ซึ่งจำเป็นต้องสร้างสภาพคล่องที่เพียงพอและสถานการณ์การเพิ่มมูลค่าที่หลากหลาย (เช่น การ抵押 (จำนอง) การกู้ยืม) เพื่อดึงดูดให้ถือครองระยะยาว

Author: WallStreetBets, Translation: Luffy, Foresight News

Over the past decade, the crypto industry has built a comprehensive trading system for native crypto assets: spot exchanges, perpetual contracts, stablecoins, lending protocols, and a full-fledged Meme coin ecosystem. This has also cultivated an entire generation of users who are accustomed to anytime entry, global liquidity, and a trading market unfettered by the 4 PM close of the US stock market.

As I see it, the next super cycle in the crypto industry is the migration of traditional real-world assets onto the blockchain. Stocks, Treasury bonds, mutual funds, gold, crude oil, and credit products will all move on-chain.

Assets like gold or Nvidia don't require extra explanation. The real transformative opportunity for the market lies in changing the public's access to asset trading channels, trading hours, and the various ways they can interact with assets after purchase.

Elon Musk's SpaceX, from its financing to secondary market trends, has already demonstrated a new model for asset circulation. The same asset can generate liquidity simultaneously across traditional brokerages, private markets, and crypto platforms. Traditional brokerages receive IPO意向认购, private platforms offer early-stage shares to qualified investors, and the crypto sector lists SpaceX IPO perpetual contracts and tokenized related products, matching traders' expectations of the stock's opening price.

Early derivatives often failed to meet market demand due to insufficient circulation of the underlying assets. Traders had to hop between brokerages, private markets, perpetuals, and tokenized products just to gain exposure to a specific asset.

This is the core trend most people overlook. The source of an asset can be within the traditional financial system, but the boundaries of its trading and circulation will completely break free from traditional frameworks.

Stablecoins have already completed the on-chain migration of the US dollar, enabling capital to flow freely around the globe, with clearing and settlement possible even when banks are closed. Now, stocks, funds, and commodities are following the same path.

Why is the Tokenization Wave Happening Now?

For years, asset tokenization remained a concept. BlackRock CEO Larry Fink once compared the traditional financial system to sending letters by post, while tokenization is email. Shortly after, BlackRock launched the BUIDL fund, with underlying assets in cash, short-term US Treasury bills, and repurchase agreements. Investors hold tokens with a stable value of $1, with returns distributed in the form of new tokens. Compliant investors can transfer their holdings between on-chain wallets.

Franklin Templeton had already deployed its government money market fund infrastructure on-chain, under the product name BENJI. Now, BENJI is expanding its business, partnering with multiple banks and digital asset platforms for trading and collateral financing.

These underlying asset classes have existed for a long time. What tokenization changes is the method of recording asset ownership, the speed of transferring holdings, and the reusable financial scenarios available after issuance.

Robinhood has listed tokens for over 200 US stocks and ETFs for EU users, covering Nvidia, Apple, Microsoft, and others. These tokens support 24/7 trading, five days a week.

Plume Network focuses on the asset issuance side, providing asset management institutions with a one-stop infrastructure for building on-chain assets, eliminating the need for them to build an entire system from scratch.

TheoriqAI sits on top of the issuance layer, building various investment strategies and deploying tokenized assets into on-chain lending and treasury yield-enhancing scenarios.

A few years ago, the industry debated whether large traditional financial institutions would adopt public blockchains. Now, the answer is clear: major institutions are already putting it into practice.

Robinhood CEO Vlad Tenev recently stated that the biggest opportunity in crypto isn't creating more native cryptocurrencies, but becoming the underlying infrastructure for real-world assets. Tokenized stocks, futures, and private market assets represent the convergence point of traditional finance and crypto.

Robinhood's significant push into tokenization has also brought this topic out of the crypto echo chamber and into the public eye.

Airbnb CEO Brian Chesky mentioned he has been following the tokenization space for years: "The core highlight isn't the token itself, but the significant reduction in transaction friction."

This is the core reason the tokenization topic is heating up so quickly. The market isn't chasing the concept of "tokenization," but rather frictionless new financial products. The industry's focus has shifted from "can assets be tokenized?" to "which tokenized products can retain long-term users."

Asset tokenization has been technically feasible for a while. The real challenge is sustained user retention.

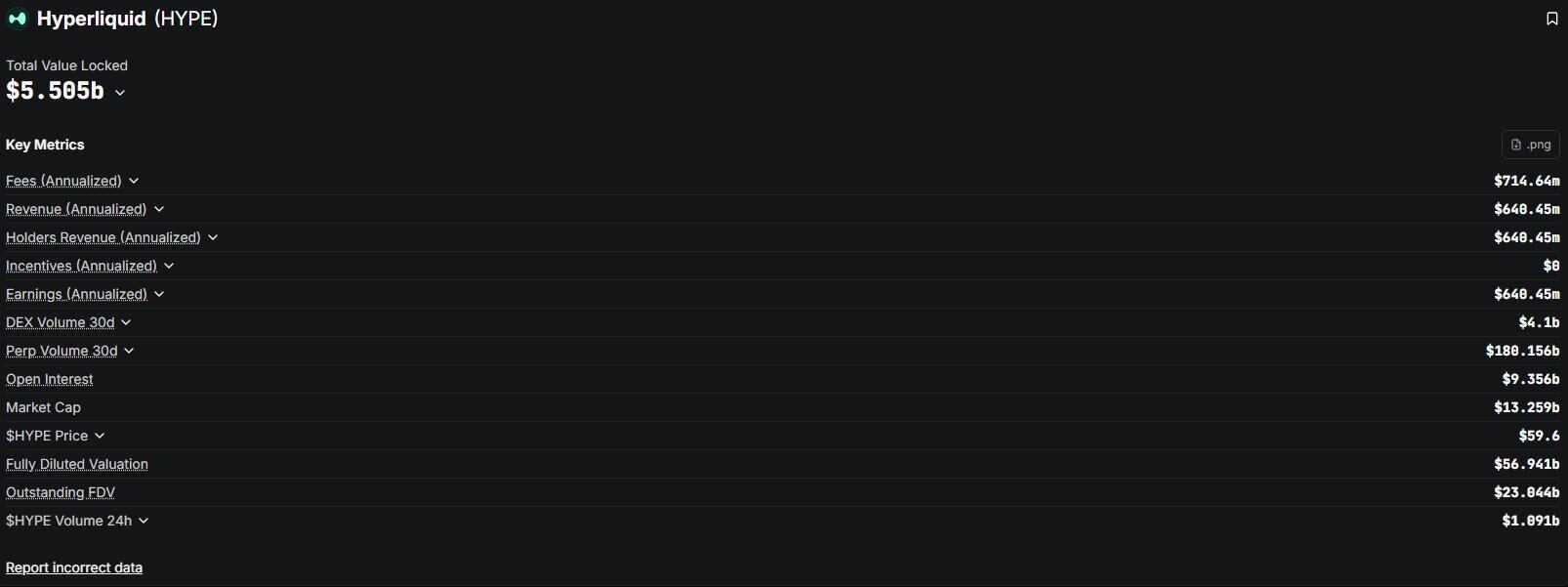

Hyperliquid Proves 24/7 Trading is a Market Necessity

HyperliquidX confirms that traders will naturally gravitate towards efficient, high-liquidity platforms that never close.

Perpetual contracts were the first category to take off because they are synthetic assets. They allow listing assets quickly without having to solve all custody, clearing, and various compliance/legal hurdles at once.

The process for moving real-world assets on-chain is more complex, requiring matching custody, clearing, and regulations from various countries.

The perpetual contract market has already validated the strong demand for 24/7 trading. Consequently, the industry is exploring more market structures that can be migrated on-chain.

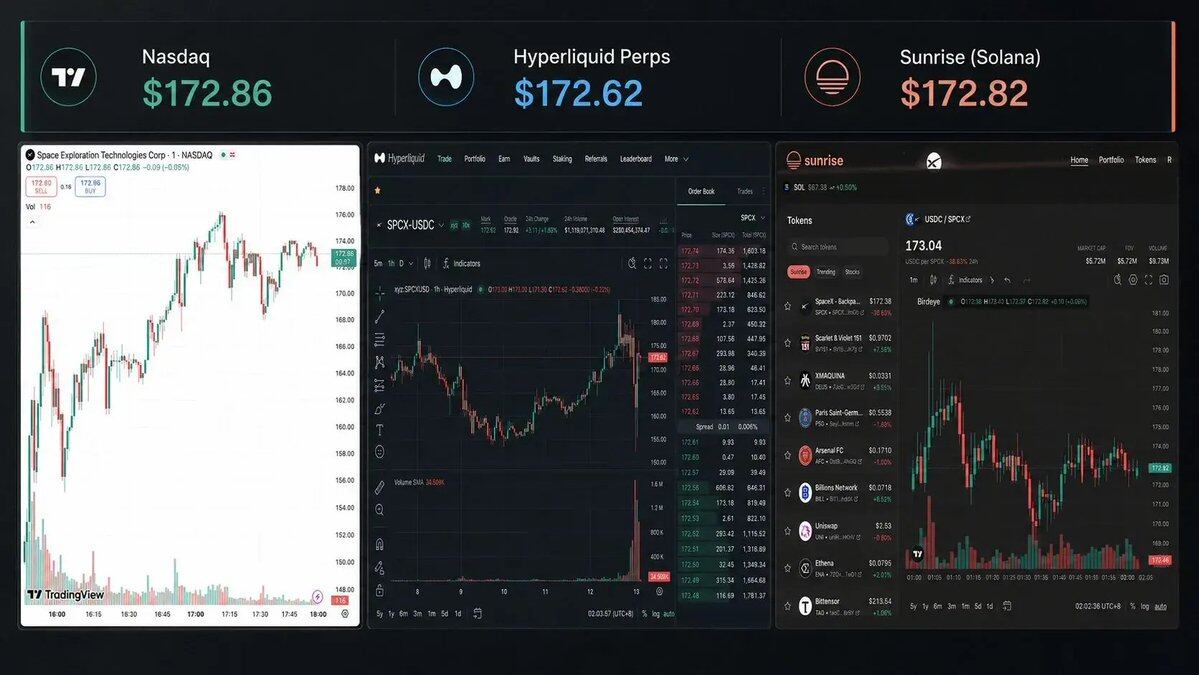

Synapse Protocol is building the underlying infrastructure for options trading. Its portfolio margin system allows market makers to use Hyperliquid perpetual contract positions as margin for option selling, hedging against the price volatility of the underlying asset. This mechanism is particularly friendly to emerging assets. Hypercall has listed SPCX options supporting intraday and same-day expiry contracts, providing trading exposure not available on the Nasdaq exchange floor.

Ondo Finance is extending this model to public markets. Ondo Global Markets integrates tokenized US stocks and ETFs into crypto wallets, using stablecoins as the medium of exchange. Ondo Perps offers traders 24/7 leveraged exposure, built on the Ondo ONE system.

Crypto users are already familiar with this operational logic: deposit stablecoins, select the asset, and complete the trade. The current challenge for the industry is, once tokenized assets are in a wallet, sufficient liquidity and diverse value-add scenarios need to be built to retain users.

Stocks: The Easiest Tokenized Asset for Consumer Adoption

SpaceX, Nvidia, Tesla, Apple, Microsoft, Coinbase, Robinhood, the S&P 500 index – these are all well-known assets to the public. This is the core reason why major exchanges are prioritizing the tokenization of stocks.

Robinhood first launched US stock and ETF tokens for EU users, and subsequently even developed its own dedicated public chain. Its business evolved from trading stock tokens within its app to becoming the underlying network carrying various on-chain asset flows. Robinhood successfully pushed stock tokens to a vast number of retail investors outside the crypto circle.

Before stock tokenization became a core narrative in crypto, projects like Streamex were already deeply involved in this track.

Bitget serves as a representative case, intuitively demonstrating the complete ecosystem of integrating tokenized stocks into a crypto exchange account. Bitget launched "Stocks 2.0," issuing rToken tokens via its compliant RWA protocol, Reality. The platform states that rToken solves several industry pain points: direct connection to Nasdaq and NYSE liquidity, 1:1 peg to the underlying asset, synchronization of corporate dividends, and the entire clearing process completed within the Bitget ecosystem.

rNVDA and rTSLA are the most straightforward examples: stocks like Nvidia and Tesla, well-known to traders, are no longer held solely in traditional brokerage accounts but are incorporated into crypto trading accounts.

Regular investors can also buy Nvidia and Tesla through traditional apps. The main change lies in where the asset is held after purchase. In a traditional brokerage account, stocks are isolated within the brokerage's proprietary system. In a crypto exchange account, compliant stock tokens can share a single pool of funds with spot, margin, grid trading, copy trading, and wealth management products. Dividends are automatically converted to USDT and credited to the account balance.

Holdings are directly calculated as available trading funds, rather than being isolated in a separate brokerage account.

Bitget believes that when stock tokens coexist in the same account as crypto spot, collateral, and various derivatives, the utility of the assets increases significantly.

Gracy, an executive at Bitget, stated that while traditional brokerage direct connection channels can solve liquidity and dividend issues, Bitget achieves equivalent advantages through tokenization while retaining the full suite of use cases for assets within the crypto account.

Crypto trading app Fomo is closer to the average user, integrating crypto assets and exposure to real-world assets into a single mobile trading interface. Its core function is product distribution and asset exposure; it does not participate in asset issuance or underlying trading infrastructure.

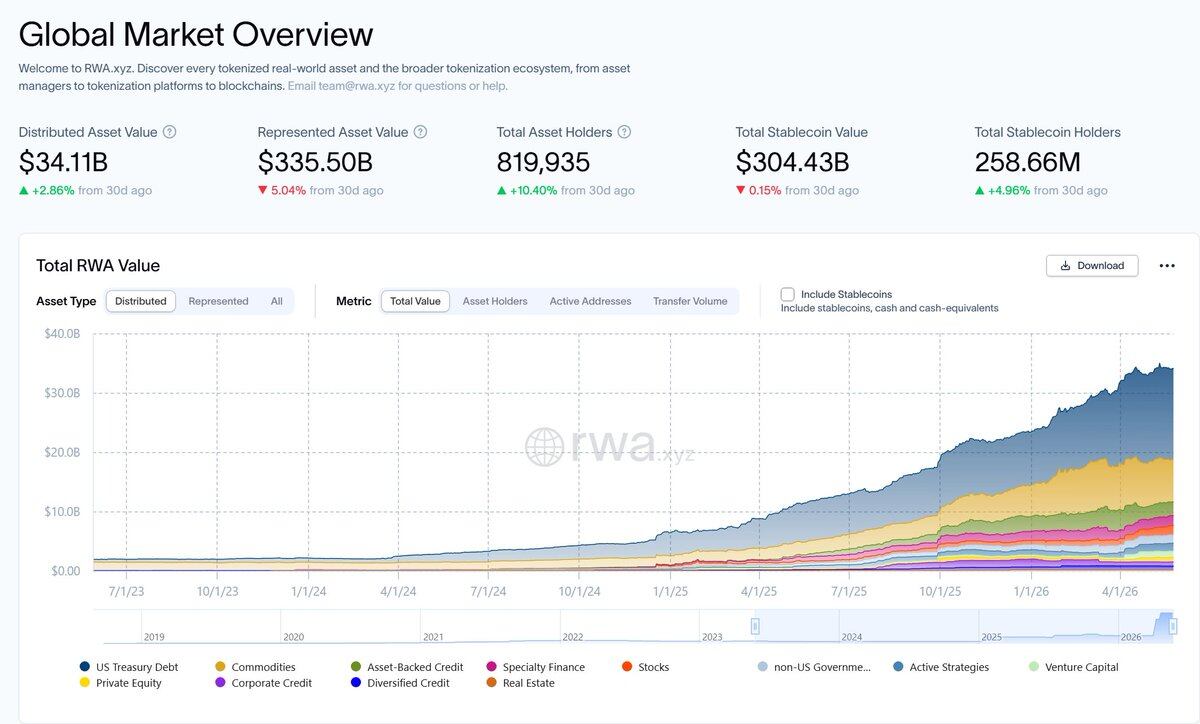

The RWA Ecosystem on Solana

Within six months, real-world assets launched on Solana via the Sunrise protocol have accumulated total trading volume exceeding $3.5 billion, across 14 million transactions, covering approximately 221,000 wallet addresses.

Sunrise utilizes Wormhole's native token transfer framework to deploy issuer-specified assets onto Solana. Wallets, aggregators, and liquidity platforms can interface with a single asset address, eliminating the need for multiple wrapped versions that fragment liquidity.

The SPCX tokenized product perfectly demonstrates this operational logic. Backpack Securities handled the securities compliance issuance. On the day of SpaceX's Nasdaq listing, Sunrise simultaneously deployed its token on the Solana chain. Within the first 24 hours, this asset traded over $50 million across 51 trading markets on Solana, surpassing $100 million in trading volume within four days.

Backpack manages securities compliance and user asset access; Sunrise connects Solana ecosystem traders, liquidity, and cross-chain routing. The cycle from asset issuance to listing trading is significantly shortened. However, whether the asset can sustain trading volume ultimately depends on market demand.

Commodities: A Bridge Between Institutions and Retail

US Treasuries are the most successful RWA category on the institutional side, with the core advantage of generating stable yields on-chain. Stocks are the best assets for retail, with Apple, Tesla, Nvidia, and the S&P 500 having broad appeal. Commodities fall somewhere in between. Institutions use them for hedging, collateral reserves, industrial sector exposure, and macro asset allocation.

Gold, crude oil, silver, copper, natural gas, and mining royalty rights all fall under the commodity category. The traditional commodity trading market is already mature. The persistent challenge has always been convenient access for ordinary investors.

Physical commodity holding barriers are extremely high. ETFs simplified the purchase process via brokerages, while futures are open to professional traders. Tokenization adds a third path: assets can circulate outside traditional trading hours, clear faster, and be directly used in various on-chain financial markets.

Not all commodities are suitable for tokenization. Crude oil has different benchmarks, storage locations, delivery contracts, and quality standards. Copper and natural gas also present physical delivery coordination challenges. Gold has the lowest barrier: global circulation, ample liquidity, a unified pricing system, is already widely traded via ETFs and futures, and PAXG/XAUT have proven user willingness to hold gold on-chain.

Currently, the dominant force in the on-chain RWA market remains US Treasuries. This product's logic is simple and clear: hold short-term Treasuries, distribute the yield to token holders.

The on-chain commodity market scale is still small, but the off-chain spot market size is enormous.

Gold is an excellent test case to verify if tokenization can optimize the trading, circulation, and yield distribution model for commodities, rather than just creating another digital certificate for the underlying asset.

GLDY: A Tokenized Gold Product with Yield

Gold has served as a store of value for millennia, yet most holding forms generate no cash flow yield. GLDY's design directly addresses this pain point: hold gold tokens and earn additional gold yield.

Each token corresponds to 1 troy ounce of standard physical gold reserves. Streamex states that expected dividends are paid in incremental gold, with the yield originating from gold leasing activities. Data on the Streamex website shows current total gold reserves of 3,096.6072 ounces.

Custodied gold can be leased to compliant enterprises in the gold supply chain, including refiners, mints, and jewelry manufacturers. Lessees pay leasing fees in the form of gold, which is then distributed to token holders.

Most tokenized gold products only offer digital custody. GLDY adds a gold leasing value layer, creating a fundamentally different yield model compared to simply holding tokens in a wallet.

Like all tokenized assets, the product's survival depends on a complete supporting trading ecosystem: holders need reserve verification, regular dividends, compliant trading channels, and a clear understanding of the yield source.

The platform's Q1 2026 financial report shows GLDY had an AUM of approximately $14 million at quarter end, with gold reserves of 3,096 ounces. The first two monthly dividend rounds distributed a total of 10.48 ounces of gold to users. Orca and Wintermute are its underlying infrastructure partners.

The platform has partnered with Siebert Financial and tZERO to access traditional brokerage channels. Siebert's wealth management and institutional clients can participate in GLDY through their existing brokerage accounts, while tZERO provides custody services via its compliant digital securities platform. With Siebert managing over $20 billion in assets, this creates a vast distribution channel outside the crypto ecosystem.

The parent company, Streamex, is listed on the Nasdaq under the ticker STEX, allowing secondary market investors to hold equity in the platform directly. In July of this year, the company's board approved a share buyback program of up to 10 million shares, with a maximum buyback price of $2, indicating management believes the current stock price significantly undervalues the business.

This ecosystem is comprehensive: Orca provides the secondary trading market, Wintermute offers market-making liquidity, Chainlink's reserve data oracle verifies gold inventory, Aurum handles the data layer, and Siebert connects traditional wealth management client channels.

I continuously track three core metrics: the scale of gold reserves, total monthly dividends, and whether secondary market trading volume can steadily grow in tandem. This is the ultimate litmus test for all tokenized assets.

The token itself is not the product; the complete trading and value-added market built around the token is the core value.

Key Points for Long-Term Observation

I don't view real-world asset tokenization as a one-way bullish market. I'm more focused on innovative products that fundamentally change how underlying assets are used.

For stocks, I want to see if traders will continue to use tokenized versions when traditional markets are closed, and whether these positions will play a role in their other portfolios.

For funds, I'm observing whether they will move beyond the issuance stage to be used as collateral or incorporated into other financial products.

Commodities are the testing ground I'm most focused on. Holding a gold token in a wallet is easy to understand. The real challenge is providing sufficient reason for users to abandon ETFs and traditional futures in favor of on-chain gold tokens.

Will users still be trading it a month from now? Can the asset be freely transferred across platforms? Will dividend yields grow in line with the underlying reserves? If the answers to all these are yes, then a truly new, mature market will have formed.

Five years ago, the industry debated whether traditional financial institutions would embrace public blockchains. Today, financial markets are gradually adopting crypto technology as underlying infrastructure.

If this trend continues, then one day, all assets will be tokenized.

Traditional markets have fixed closing times, but the crypto market is open 24/7.