业绩巨压之下,Coinbase向中国用户低头开放注册

- 核心观点:Coinbase 于 2026 年 7 月 14 日首次真正开放中国大陆身份证注册,旨在应对连续亏损的业绩压力,拓展全球最大的加密交易市场之一华语市场,但该平台目前存在合规隐患且产品对中国用户缺乏吸引力。

- 关键要素:

- 注册开放:无需海外地址证明,用户使用中国大陆身份证和手机号即可在 1 分钟内完成注册,截至撰稿通道未关闭。

- 业绩压力:Coinbase 连续两个季度净亏损(Q4 亏损 6.667 亿美元,Q1 亏损 3.941 亿美元),散户交易收入 Q1 同比下滑 48.2% 至 5.67 亿美元。

- 市场竞争:美国市场竞争加剧,超 10 家合规交易所(如 Robinhood、Kraken)提供更低手续费,导致 Coinbase 用户流失。

- 合规风险:中国用户与 Coinbase 发生纠纷时,可能面临中美法律均无法保护的风险;美国法律允许,但中国加密交易本身处于灰色地带。

- 产品劣势:Coinbase 无法支持中国用户法币出入金,且上币效应消失,在 Meme、衍生品(如代币化美股)等领域竞争力不足。

Original by Odaily (@OdailyChina)

Author: Golem (@web3_golem)

On July 14, community users discovered that Coinbase had quietly opened registration for users in the Chinese-speaking region—without requiring proof of overseas address. Users could successfully register using only a Chinese Mainland ID card and phone number, and the entire verification process took less than a minute. As of the time of writing, the registration channel has not been closed.

According to its Q1 2026 earnings report, Coinbase held 8.6% of the global crypto trading market share (excluding the Chinese-speaking market). Coinbase had previously restricted KYC for Chinese users. In April 2025, it briefly opened registration for Chinese users, where those using a Chinese passport plus overseas proof like a Hong Kong address had a chance to register successfully, but those accounts were soon broadly banned.

Therefore, July 14 can be seen as the first time Coinbase meaningfully opened registration to Mainland Chinese users. Coinbase has yet to make any official statement or explanation, but the market has interpreted this as a significant signal of Coinbase's accelerated push into the international market. According to Gate US stock data, Coinbase (COIN) shares closed up 2.62% on July 14 and rose 0.74% in pre-market trading today.

Under Earnings Pressure, Coinbase Targets Chinese Users

According to the US National Cryptocurrency Association (NCA), the US is the largest regional market by crypto trading market share. As of 2026, approximately 67 million American adults hold cryptocurrency, representing about 25% of the US adult population. Although precise statistics are unavailable, the Chinese user base and Chinese-speaking market certainly rank among the top three global crypto trading markets, with major exchanges like Binance and OKX treating the Chinese-speaking region as a primary market.

Once "aloof" Coinbase is now quietly opening its doors to Chinese users. This shift is not sudden; the reasons have long been evident in every past earnings report.

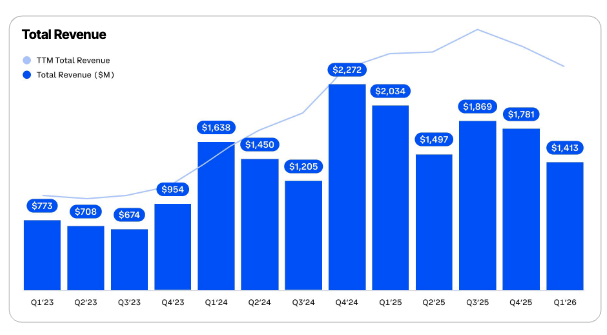

Coinbase has recorded net losses for two consecutive quarters, with a net loss of $666.7 million in Q4 2025 and $394.1 million in Q1 2026. Coinbase attributed the Q1 2026 losses primarily to a weak crypto market, but looking at the longer trend, Coinbase's revenue has actually been declining since the start of 2025.

Coinbase Quarterly Revenue

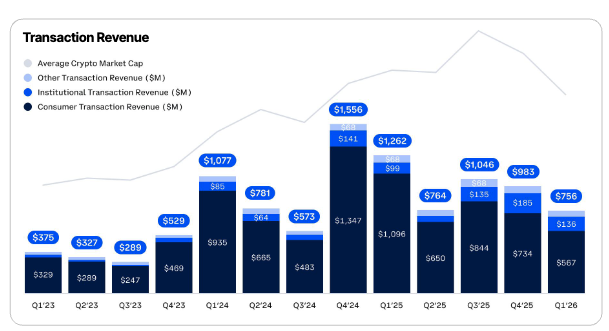

Coinbase's main revenue source remains its transaction brokerage business, with retail traders contributing 80% of total transaction revenue. Since 2025, Coinbase's transaction brokerage revenue has been on a general downward trend, with retail transaction revenue—accounting for the bulk of income—declining significantly: $1.096 billion in Q1 2025 compared to just $567 million in Q1 2026, a year-over-year decrease of 48.2%.

Coinbase Quarterly Transaction Revenue

The downtrend in the crypto market and sluggish user trading volume are only part of the reason for the decline in Coinbase's retail transaction revenue. Another reason is increased competition in its domestic market and user attrition.

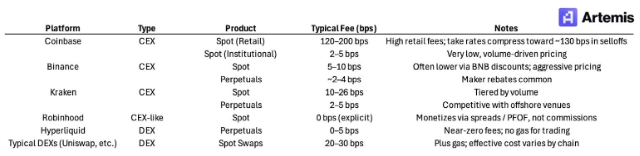

Coinbase's monopoly position in the US market, built early on its "compliance reputation," has long disappeared as US regulation has matured. Over ten exchanges have obtained licenses to offer crypto trading services to US users, including Robinhood, Kraken, and Binance.US. Without exception, these exchanges charge lower fees than Coinbase. Now that security and trust are no longer barriers to entry, retail traders naturally choose platforms with lower fees.

Fee Percentage Charged by Different Exchanges

Facing these challenges, Coinbase has begun heavily developing other businesses beyond spot crypto trading, such as derivatives trading, prediction markets, and tokenized stocks, attempting to brand itself as an "exchange for everything." Whether these combined businesses can challenge the dominance of spot crypto trading in Coinbase's revenue will only be known after the Q2 2026 earnings report is released.

Under earnings pressure, Coinbase seems to have finally seen the light. Since competitors are coming to the US to take its users, why shouldn't it venture abroad? After all, outside the US lies a world of growth. Consequently, Coinbase's first target is the Chinese-speaking market, one of the top three global crypto trading markets.

Coinbase's opening of Chinese KYC also exploits a loophole in US law.

Crypto KOL Phyrex (X: @PhyrexNi) noted that Coinbase cannot provide services to countries and regions sanctioned by the US OFAC. As China is not on the list, providing services to Chinese users is not illegal for Coinbase in the US. However, for Chinese users, Coinbase is not compliant within China, and crypto trading itself operates in a grey area. If a dispute arises between a Chinese user and the Coinbase platform, the worst-case scenario is that neither US law nor Chinese law may protect the Chinese user.

Coinbase's Advantages Are Primarily Within the US

Beyond compliance issues, from a product usability perspective, most Chinese-speaking users are already disillusioned with Coinbase. Its advantages are mainly in the US; internationally, crypto users have too many choices. More bluntly, registering for Coinbase now offers little utility. Most users rushing to register do so with a "better to have it and not need it" mentality.

From 2021 to 2024, Coinbase did have a "coin listing effect." When Coinbase announced support or listing for a token, the token's price often experienced a significant short-term surge. Examples include LINK, POL, and AAVE, all of which saw price spikes after being listed on Coinbase.

At the time, Coinbase was the largest compliant US exchange with an extremely strict listing process, perhaps listing only a few dozen projects a year. This meant tens of millions of US investors and institutions could only buy coins compliantly through Coinbase. Hence, listing on Coinbase equated to an influx of new demand, making the listing effect highly significant.

However, with the relaxation of US crypto regulation in recent years and investors having more purchasing channels—including numerous traditional brokerages and DEXs—Coinbase's role as a "capital gatekeeper" for the US crypto market has diminished, and the listing effect has naturally disappeared.

Coinbase CEO Brian Armstrong proudly stated during the Q1 earnings call, "Customers choose us not because we are the cheapest, but because we can offer products that meet their needs." Let's put aside Coinbase's high fees for retail trading (up to 1.2%) and examine the product and user experience. Coinbase not only lacks differentiation but also fails to meet the needs of Chinese users.

Firstly, although Coinbase has opened KYC for Chinese users, it does not support fiat currency deposits and withdrawals, a restriction enough to deter most people. Secondly, looking at the currently popular tokenized US stocks, while Coinbase claims to heavily develop this business, its supported offerings and market share lag far behind Binance's bStocks and Hyperliquid—just today, Hyperliquid even listed a pre-market contract for ChangXin Memory Technologies (CXMT) A-shares. Furthermore, Coinbase shows no significant advantage in product experience and support for Meme coins, prediction markets, etc.

Today's Coinbase can only be described as "expensive and useless." To truly open up the Chinese-speaking market, besides quietly relaxing registration, it will need corresponding exclusive token launch events or other wealth-generating activities. Otherwise, interest will remain minimal.