FALX กำลังทำอะไรกับระบบคัดสรรเครดิตบนเชน?

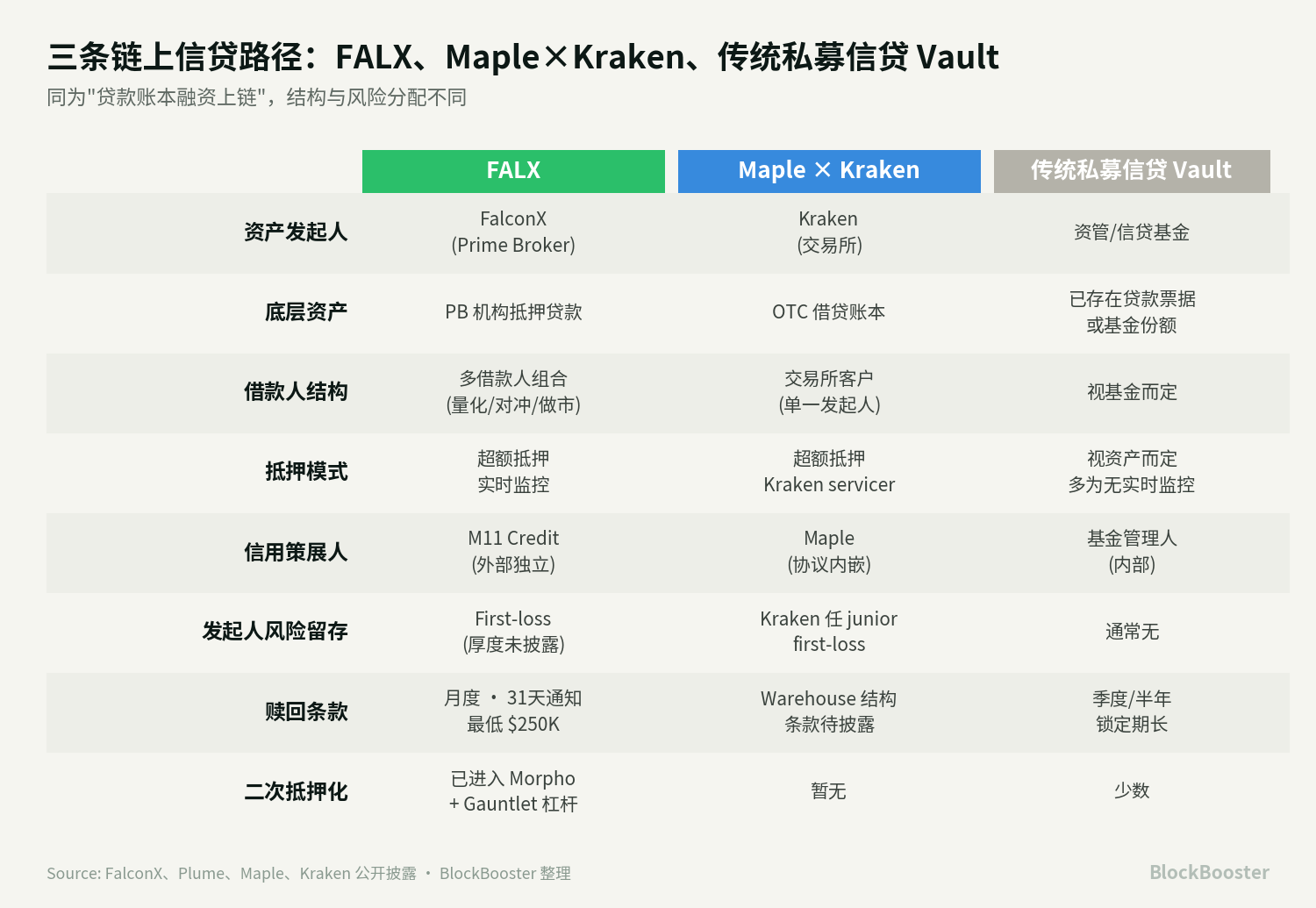

- มุมมองหลัก: FALX คือระบบการก่อตัวของทุนที่แปลงสินเชื่อที่มีหลักประกันเกินมูลค่าจาก Prime Brokerage ของ FalconX ผ่านกลไกที่มีโครงสร้าง เช่น SPV, การคัดสรรเครดิต และ Vault บนเชน ให้เป็นสินทรัพย์รายได้คงที่บนเชน ซึ่งแหล่งที่มาของผลตอบแทนมีความซับซ้อน และโครงสร้างความเสี่ยงแตกต่างจากการให้กู้ยืมแบบดั้งเดิมของ DeFi อย่างมีนัยสำคัญ

- องค์ประกอบสำคัญ:

- ผลตอบแทนของ FALX มาจากต้นทุนทางการเงินที่ผู้กู้ของ Prime Brokerage จ่ายเพื่อเพิ่มประสิทธิภาพในการใช้ทุน ซึ่งรวมถึงอัตราดอกเบี้ยพื้นฐานของดอลลาร์สหรัฐ, ส่วนต่างความผันผวนของหลักประกันสินทรัพย์ดิจิทัล, ส่วนต่างการจัดสรรระหว่างกระดานซื้อขาย และส่วนต่างค่าบริการ PB

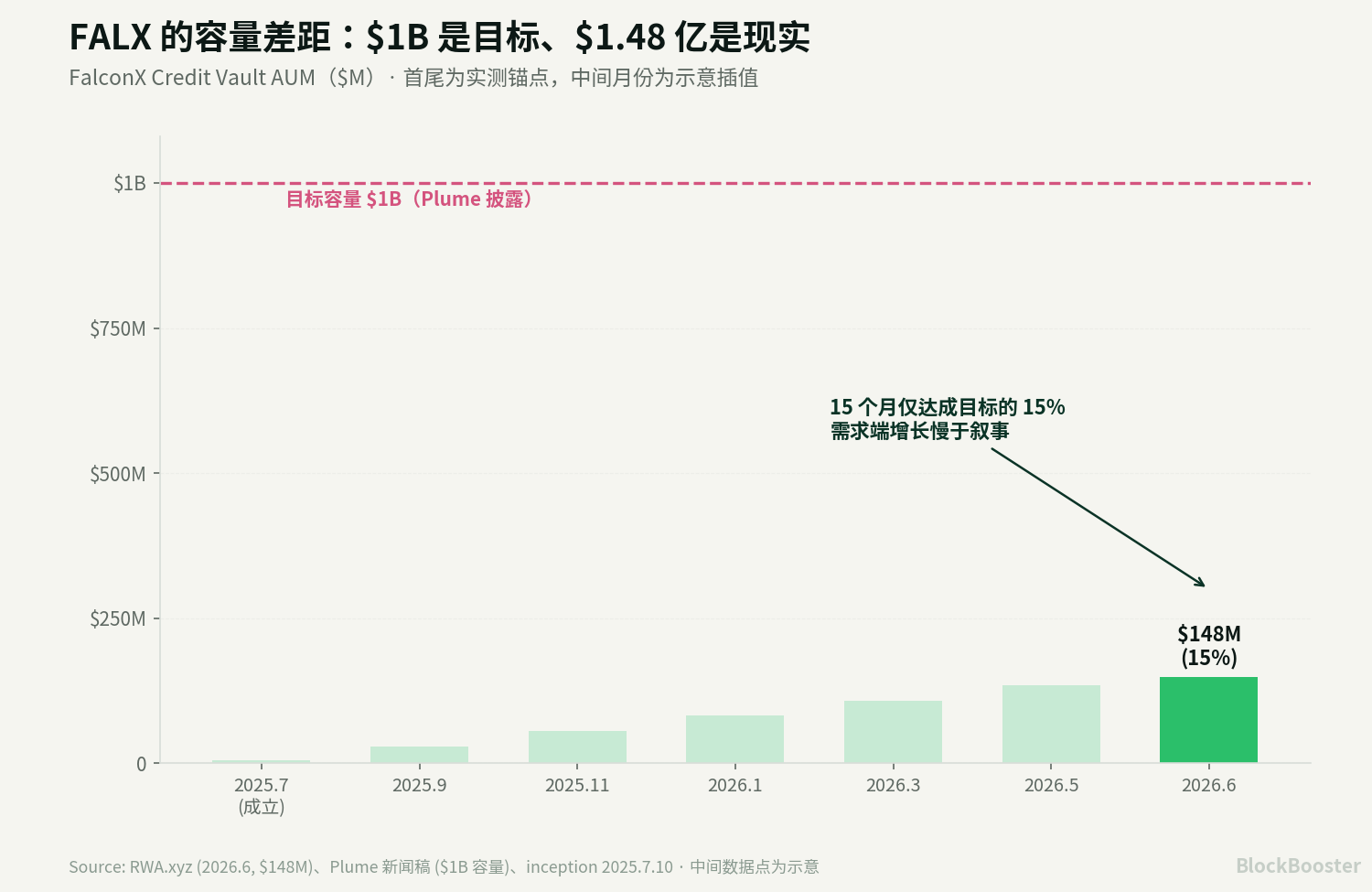

- ปัจจุบันสินทรัพย์รวมของ FalconX Credit Vault อยู่ที่ประมาณ 148 ล้านดอลลาร์สหรัฐ ซึ่งต่ำกว่าเป้าหมายความจุ 1 พันล้านดอลลาร์สหรัฐที่เคยประกาศไว้มาก แสดงให้เห็นว่าความต้องการเงินทุนบนเชนยังคงเผชิญกับความท้าทายในการเติบโต

- M11 Credit ทำหน้าที่เป็นผู้คัดสรรเครดิตหลักใน FALX แต่มีประวัติที่ด่างพร้อยจากการผิดนัดชำระหนี้ของ Orthogonal Trading บนแพลตฟอร์ม Maple ในปี 2022 (มูลค่าประมาณ 36 ล้านดอลลาร์สหรัฐ) ซึ่งเกิดจากการพึ่งพาข้อมูลที่รายงานด้วยตนเองจากผู้กู้มากเกินไป และการขาดการควบคุมการกระจุกตัว

- เบื้องหลังของ FALX คือสินเชื่อที่มีหลักประกันเกินมูลค่า และมีการป้องกันหลายชั้น เช่น การสนับสนุนทุน First-loss จาก FalconX โครงสร้างความเสี่ยงจึงแตกต่างโดยพื้นฐานจากสินเชื่อเครดิตแบบไม่มีหลักประกันของ Maple ในปี 2022

- FALX Token ถูกนำไปใช้เป็นหลักประกันรองในโปรโตคอล DeFi อย่าง Morpho ซึ่งในขณะที่ช่วยเพิ่มประสิทธิภาพในการใช้ทุน ก็เป็นการนำความเสี่ยงด้านเครดิตภาคเอกชนเข้าสู่ระบบการชำระบัญชีบนเชน ซึ่งอาจก่อให้เกิดความเสี่ยงแบบลูกโซ่ที่นำไปสู่การแห่ไถ่ถอนและราคาที่ลดลง

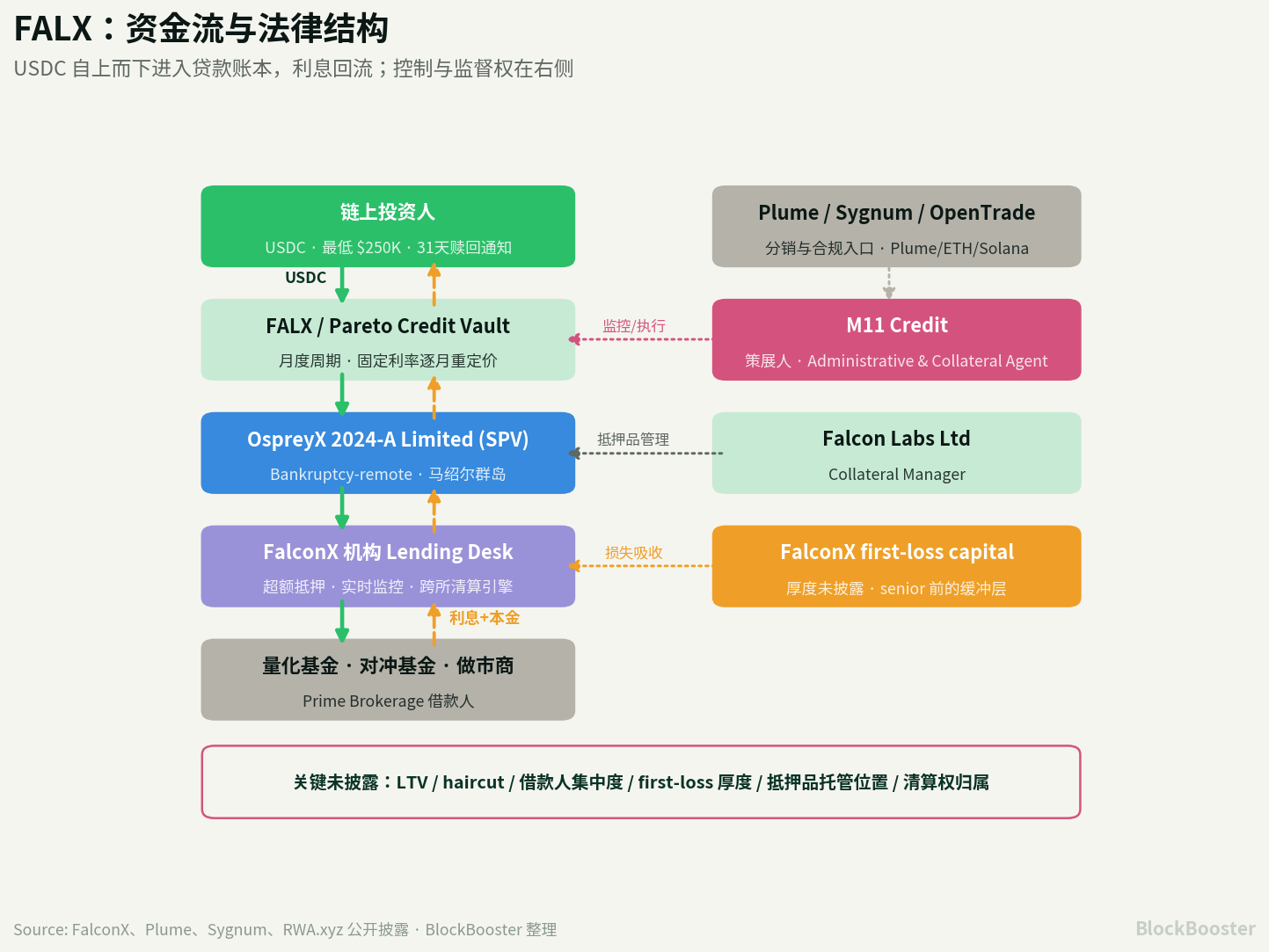

FALX is a capital formation mechanism that transforms the Prime Brokerage loan ledger into on-chain fixed income assets.

Its core structure is:

- FalconX originates mortgage-backed loans

- → Loan exposure enters a FalconX-managed SPV

- → Pareto provides the on-chain Credit Vault

- → M11 Credit acts as credit curator, administrative agent, and collateral agent

- → Distributed to investors via on-chain entry points like Plume / Ethereum / Solana

1. What FALX Actually Is

FALX more closely resembles an on-chain structured credit facility: Investors deposit USDC into the Pareto/FALX-related Vault, funds enter a bankruptcy-remote SPV associated with FalconX, which then extends over-collateralized loans to institutional clients such as quantitative funds, hedge funds, market makers, and asset managers through its institutional credit system.

In March 2025, FalconX announced its Structured Credit Facility, packaging FalconX-originated loans into structured products. This allows investors to access them through Pareto's private credit Vault, with M11 Credit serving as curator. FalconX views this as integrating institutional credit asset formation with on-chain capital.

On June 30, 2026, Plume announced the launch of the FALX Structured Credit Facility. According to Plume's disclosure, this Vault utilizes Pareto's infrastructure, is curated by M11 Credit, and directs funds into a FalconX-managed SPV, with the underlying exposure originating from over-collateralized loans on the FalconX Prime Brokerage platform. The facility is described as scalable to approximately $1B in capacity.

Thus, FALX on Plume is more akin to a new on-ramp and expansion of the existing structured credit facility involving FalconX, Pareto, and M11, rather than an entirely new asset pool built from scratch.

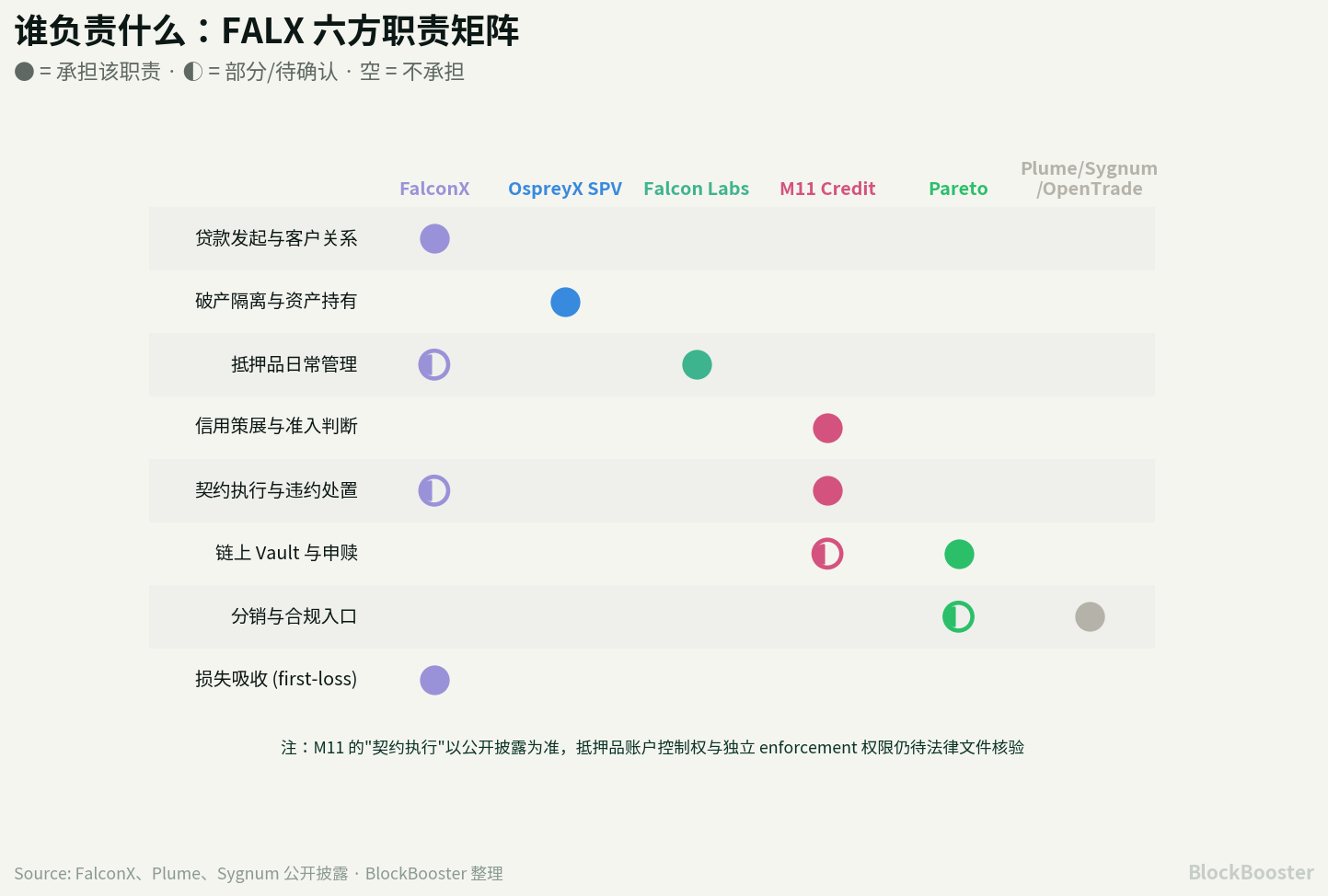

2. Fund Flow and Participants

The six main participants are as follows:

In a statement from June 2026, FalconX disclosed that the Vault lends to OspreyX 2024-A Limited, a SPV designed to be bankruptcy-remote, isolating investor capital from FalconX's corporate balance sheet. Falcon Labs Ltd serves as the Collateral Manager, M11 Credit acts as the Administrative and Collateral Agent, and FalconX provides a first-loss capital contribution.

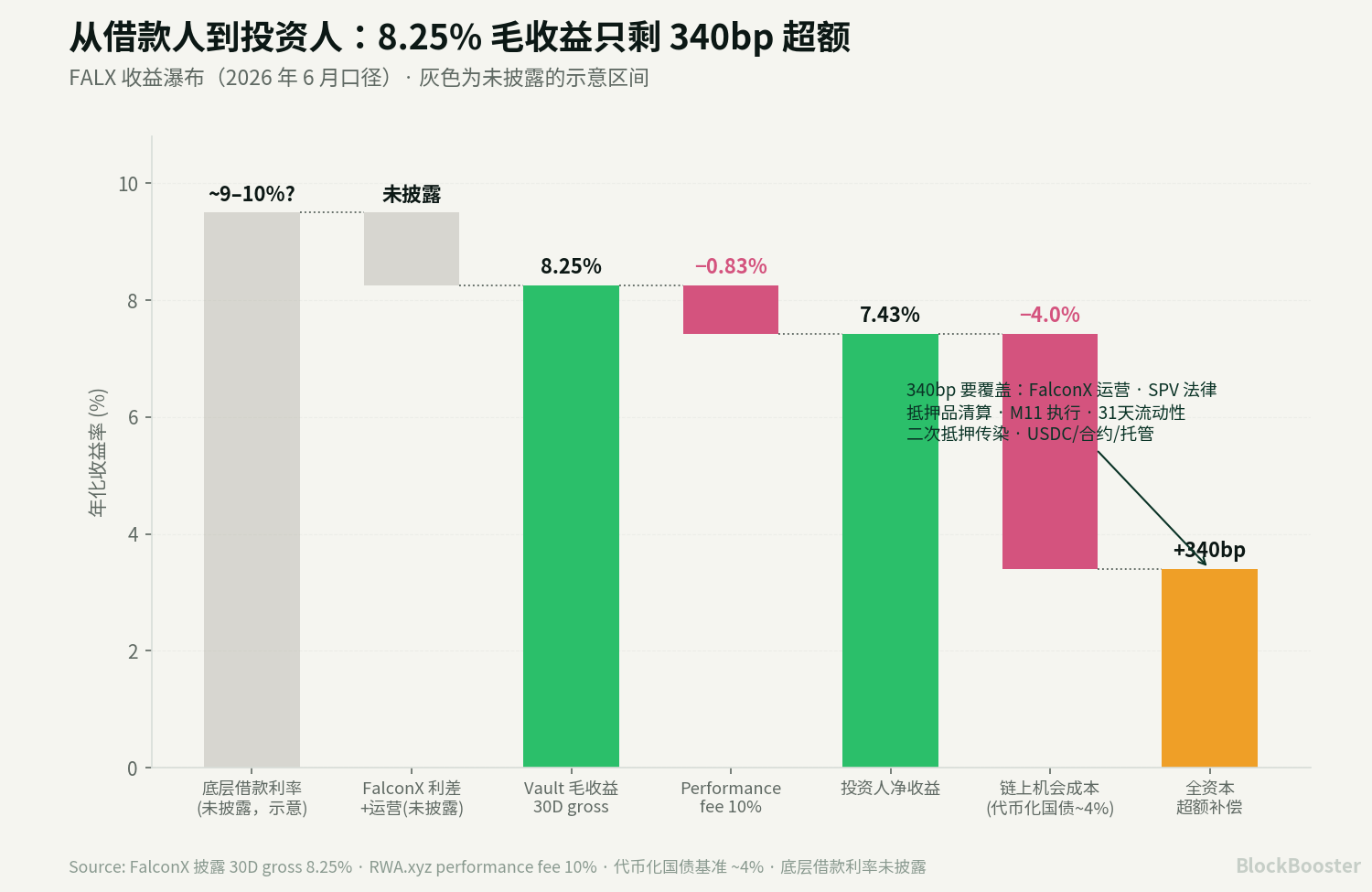

3. Who Pays the Yield

The yield of FALX represents the financing cost that Prime Brokerage borrowers pay to achieve capital efficiency.

FalconX's financing operations cover areas such as margin loans, flexible settlement, OTC lending, DMA credit, prime brokerage financing, structured products, and yield generation.

This product list indicates that the underlying cash flow for FALX comes from the comprehensive financing needs of institutions managing capital across multiple trading venues, diverse collateral types, and various settlement cycles.

Therefore, FALX's yield stems from four types of premiums:

- The USD base interest rate;

- Premiums for digital asset collateral volatility;

- Premiums for instant liquidity and cross-exchange capital dispatch;

- Premiums for Prime Brokerage services.

This also explains why FALX cannot be simply compared to the Aave USDC supply rate. Aave is on-chain over-collateralization with algorithmic interest rates and open pools. FALX is an institutional Prime Brokerage loan portfolio, bearing the risks associated with FalconX, the SPV, M11, collateral execution, and the underlying client portfolio.

4. Yield Metrics

FalconX disclosed:

- Base yield = FalconX's disclosed 30D gross yield of 8.25%

- After deducting a 10% performance fee

- Approximate net yield for investors ≈ 7.4%

The next step is calculating the excess yield. For on-chain USDC investors, the most relevant opportunity cost is the available on-chain low-credit-risk yield, such as tokenized treasuries, money market products like BUIDL, or Aave USDC. FalconX itself compared against Aave USDC at 3.26% in its article. Considering tokenized treasuries are roughly around 4%, this article uses 4% as the on-chain capital opportunity cost.

Therefore:

- FALX net yield approximately 7.4%

- − Low-risk on-chain USDC opportunity cost approximately 4.0%

- = Excess compensation approximately 3.4%

This 340 basis points must cover:

- FalconX operational risk;

- SPV legal risk;

- Collateral liquidation risk;

- M11 execution risk;

- Liquidity discount from the 31-day redemption notice;

- Contagion risk from DeFi rehypothecation;

- USDC, smart contract, cross-chain, and custody risks.

5. FALX Capacity Reality

Plume disclosed that FALX's current capacity is scalable to approximately $1 billion.

FalconX disclosed in March 2025 that its 2024 loan originations reached $2.5 billion, indicating FalconX indeed has loan origination capabilities.

However, RWA.xyz's current page shows the FalconX Credit Vault's total assets are approximately $148 million.

This is a significant signal: from the SCF announcement in March 2025 to June 2026, the Vault's AUM reached only about $148 million, roughly 15% of the $1 billion target capacity. This suggests that on-chain demand growth for this type of product is not trivial.

Capacity needs to be broken down into five layers:

- Legal and Contractual Capacity: How much the SPV and Vault can theoretically hold;

- Loan Origination Capacity: The total institutional loan demand available to FalconX;

- Eligible Loan Capacity: How many loans meet standards for LTV, collateral, borrower concentration, and covenants;

- Target Yield Capacity: How much borrowers are willing to borrow given a target net yield of 7%–8% for investors;

- Investor Demand Capacity: Whether on-chain capital accepts the $250,000 USDC minimum investment, 31-day redemption notice, and complex credit risks.

6. The Role of M11

6.1 M11's Positive Value in FALX

FalconX disclosed M11 as the Vault Curator, responsible for reporting, epoch cycles, subscription and redemption requests, credit assessment, enforcing loan covenants, and real-time risk monitoring.

Plume also disclosed M11 Credit serving as the curator.

Sygnum explicitly disclosed M11 Credit as the Administrative and Collateral Agent.

This indicates M11 is not a simple distributor. It assumes the most critical intermediary role in a credit product: representing investors in deciding which assets can enter the pool and supervising the originator and borrowers throughout the loan lifecycle.

6.2 M11's Historical Stains

M11 must be evaluated alongside its failure case on Maple in 2022. In December 2022, Orthogonal Trading defaulted on Maple for approximately $36M, of which $31M came from the USDC pool managed by M11, and roughly $5M from the wETH pool also managed by M11. This resulted in an approximate 80% hit for remaining investors in the M11 USDC pool.

M11's own statement acknowledged that Orthogonal severely misrepresented its financial condition after the FTX collapse, only disclosing losses far exceeding prior claims on December 3rd, leading to its inability to repay. M11 stated that Orthogonal had consistently claimed, both in writing and verbally, that its FTX exposure was limited, severely impacting M11's ability to manage credit risk.

This case exposed four problems:

- Over-reliance on Self-Reported Borrower Data: If a borrower intentionally conceals information, the curator may not detect it in time;

- Loss of Concentration Control: By December 2022, roughly 80% of loans in one of M11's USDC pools were concentrated with Orthogonal, compared to about 14% at the end of August;

- Inadequate Pool Cover and Valuation Issues: The pool cover for three M11-managed pools was largely exhausted, covering only a small fraction of the bad debt. Concurrently, Maple's native token MPL significantly depreciated during the risk event. The underlying lesson is: if first-loss capital / insurance is primarily denominated in a related governance token, the insurance asset and the insured asset may shrink simultaneously during a risk event;

6.3 Essential Distinction Between FALX and Maple 2022

The core problem with Maple/M11 in 2022 was unsecured or under-collateralized institutional credit loans. It relied on borrowers disclosing balance sheets, exchange exposures, and financial health. Once a borrower lied, on-chain transparency could not automatically uncover off-chain asset black holes.

FALX's structure is different. It involves Prime Brokerage over-collateralized loans. FalconX disclosed the use of real-time collateral monitoring, automatic margin calls, cross-exchange liquidation engines, and first-loss capital contribution.

7. Loss Waterfall: Who Loses Money First. At least three layers of protection were disclosed:

FALX

- Underlying loans are typically over-collateralized;

- FalconX provides a first-loss capital contribution;

- M11 acts as Administrative and Collateral Agent, providing independent oversight.

The ideal loss waterfall should be:

- Collateral overage

- → Borrower posts additional margin

- → Collateral is liquidated

- → FalconX first-loss / equity tranche

- → Other junior protections

- → Senior investor principal loss.

However, public materials do not disclose the specific thickness of each layer.

8. Redemption Run and Rehypothecation Risk

FALX's base terms include a monthly cycle and a 31-day redemption notice. RWA.xyz shows the FalconX Credit Vault has a 31-day notice period for redemptions and discloses no management, subscription, redemption, or entry/exit fees besides the 10% performance fee.

This creates an Asset-Liability Management (ALM) problem: investors have a 31-day notice period, and underlying loans also roll on a monthly basis. But if investors request mass redemptions (e.g., 50%) in a given month, would the SPV require FalconX to compress the loan book early, queue redemptions with gates, or rely on a secondary market? Public materials do not fully answer this question.

More importantly, FALX has already entered the DeFi rehypothecation layer. The FalconX Credit Vault Token has become one of the significant RWA collaterals on Morpho. Gauntlet also launched the FalconX Levered RWA Strategy, which involves depositing FalconX CV tokens as collateral to borrow USDC and then purchase more CV tokens.

This creates a new transmission chain:

- FALX tokens are used as collateral on Morpho

- → Market pressure leads to a discount on FALX tokens or NAV adjustment

- → Morpho health factors decline

- → Liquidators sell or dispose of FALX tokens at a discount

- → Secondary price continues to fall

- → More holders submit redemptions

- → The SPV needs to release cash

- → FalconX's loan book is forced to contract or redemptions are potentially gated.

Rehypothecation of FALX enhances capital efficiency but also connects what was a relatively closed private credit risk to the DeFi liquidation system. It transforms from a 'credit product' into a 'composable collateral asset,' potentially accelerating the speed of risk transmission.

9. Conclusion

FALX's true innovation lies in combining FalconX's Prime Brokerage loan ledger, the SPV legal structure, M11's external credit curation, Pareto's on-chain Vault, and distribution entry points like Plume/Sygnum/OpenTrade into a cohesive on-chain capital formation mechanism.

It demonstrates that on-chain credit does not necessarily require solving the most difficult problem of "fully on-chain native credit scoring" first.

A more practical path is: first find professional originators with genuine cash flow and loan demand. Then, using SPVs, first-loss capital, over-collateralization, external curators, and on-chain capital flow transparency, transform these loans into investable assets.