错过币股浪潮,韩国加密交易所被迫“炒土狗”

- 核心观点:韩国加密交易所因监管严格,无法上线衍生品、代币化股票等多样产品,收入严重依赖现货手续费。在业绩下滑背景下,为吸引交易量,被迫上线与SpaceX股票代码相似的投机性“土狗”代币,反映了保护性监管反而加剧市场风险与交易所经营困境。

- 关键要素:

- 2026年Q1,Upbit营收同比下降54.6%至2346亿韩元,Bithumb营收下降57.6%至825亿韩元并出现净亏损,业绩集体下滑。

- 韩国交易所超97%收入来自现货交易手续费,但被禁止开展代币化股票、期货、衍生品及ETF等业务,业务范围极为狭窄。

- 海外交易所如Coinbase、币安、Bybit已转型“万物交易所”,上线代币化股票等产品,SpaceX上市24小时内加密货币市场交易额达90亿美元。

- 韩国交易所无法参与SpaceX上市盛宴,唯一竞争手段是在适当时机上线能吸引眼球的投机性代币,如Spacecoin和SPX6900。

- 监管初衷是保护投资者,但剥夺了交易所收入来源,使其在市场萎缩时更倾向上线高风险资产,同时刺激投资者转向币安等海外平台,造成监管失效与收入流失。

- 韩国金融机构正通过入股加密交易所(如韩华投资证券增持Dunamu、未来资产收购Korbit),推动证券公司与交易所整合,但传统交易所转型为“万物交易所”的可能性极低。

Original article from Four Pillars

Translation / Odaily Golem (@web3_golem)

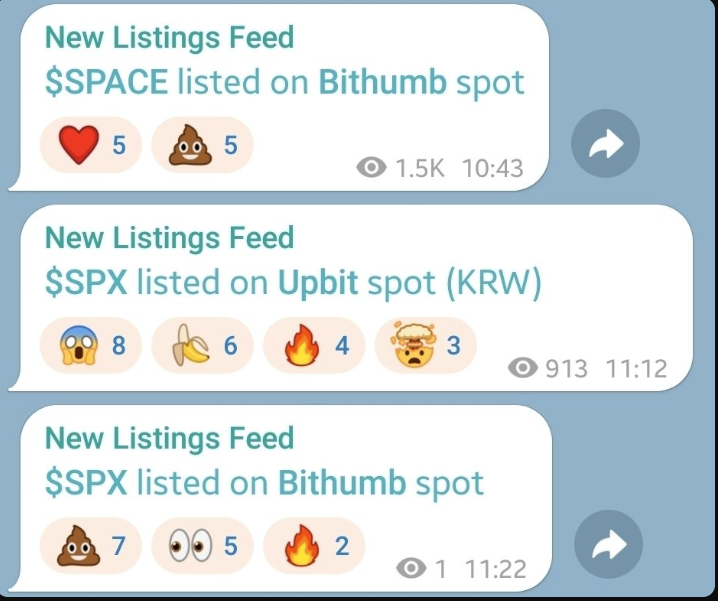

Editor's Note: On June 16, the Korean exchange Bithumb listed a so-called "shitcoin" named Spacecoin, followed closely by Upbit listing an outdated meme coin, SPX6900. The community widely believes that the reason these two major Korean crypto exchanges listed these tokens was their coincidental similarity to SpaceX's stock ticker, with exchanges attempting to capitalize on the hype around "shitcoins" to attract trading volume.

Against the backdrop of a weakening crypto market and Korean crypto investors shifting towards stock trading, Korean exchanges saw a collective decline in Q1 2026 performance. Consequently, they urgently need measures to reverse their downturn. However, unlike overseas exchanges that can transform into "everything exchanges" by listing large numbers of tokenized stocks to meet crypto traders' demands, Korea classifies tokenized stocks as securities, thus prohibiting crypto exchanges from engaging in such transactions. Korean exchanges are also not permitted to offer crypto futures, derivatives, or spot exchange-traded funds (ETFs).

Korea's investor-protective regulatory measures have paradoxically pushed crypto exchanges into the most speculative corners of the market. With revenue streams and new product lines such as derivatives, tokenized stocks, and prediction markets all banned, exchanges, in their quest to boost platform trading volume, tend to opt for listing attention-grabbing, and therefore more speculative, "shitcoin" tokens.

Upbit and Bithumb List "Fake SpaceX Stocks," Shocking the Korean Community

Bithumb and Upbit listed tokens with tickers similar to SpaceX's stock

On the morning of June 16, the hottest topic in the Korean community was Bithumb's listing of the obscure project token Spacecoin (SPACE) and Upbit's listing of the meme coin SPX6900. One might ask, isn't this just an ordinary token listing announcement? What truly stirred the community's reaction was not the listings themselves, but the names of the tokens and the timing of the listings.

Four days earlier, on June 12, SpaceX listed on Nasdaq under the ticker SPCX. As is well known, SpaceX's IPO broke historical records, and with stock-related topics now dominating the Korean crypto community, SpaceX became the hottest topic in the space over the weekend.

Therefore, after Upbit and Bithumb's listing announcements, suspicion began to circulate within the community that these two exchanges listed tokens with names and tickers very similar to SPCX, aiming to ride the hype and generate trading volume. Although this connection might merely be a coincidence, such an interpretation not only seems plausible but also reflects the current state of Korean exchanges.

Now, overseas platforms like Coinbase, Binance, and Bybit allow users to trade SpaceX and other foreign stocks directly on the exchange. However, due to regulatory restrictions, Korean exchanges cannot offer such products, so they may have to resort to listing, at the very least, a token with a name similar to SpaceX.

But this incident shouldn't just be dismissed as a joke. It precisely reflects the difficult position Korean crypto exchanges face in competing with their overseas counterparts.

The Current State of Korean Exchanges

Overall Performance Decline, Some Facing Losses

The Q1 2026 performance of Korea's two largest exchanges was lackluster.

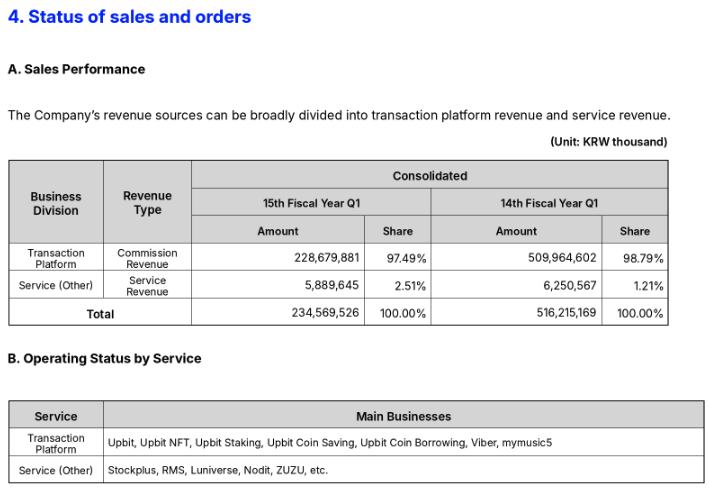

Upbit Q1 2026 Performance Source: FSS DART

According to the quarterly report submitted via the Financial Supervisory Service's DART system on May 15, Dunamu, which operates Upbit, reported consolidated revenue of 234.6 billion KRW, down 54.6% year-on-year. Operating profit plummeted 77.8% to 88 billion KRW, and net profit fell 78.3% to 69.5 billion KRW. Upbit's fee income decreased 55.2% to around 200 billion KRW, while operating costs rose 22% over the same period, squeezing profit margins.

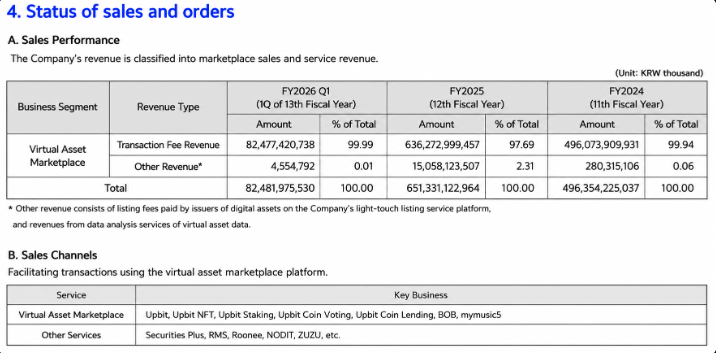

Bithumb Q1 2026 Performance Source: FSS DART

Bithumb's situation was more severe. Q1 revenue fell 57.6% to 82.5 billion KRW, operating profit plunged 95.8% to 2.9 billion KRW, and the company recorded a net loss of 86.9 billion KRW, its second consecutive quarterly net loss. The direct cause of the loss was an 87% drop in fee income due to reduced trading volume. Additionally, a 36.9 billion KRW fine from the Financial Intelligence Unit (FIU) for violating the Act on Reporting and Using Specified Financial Transaction Information, along with a six-month partial business suspension order, were also reflected in the Q1 results.

The biggest problem for Korean exchanges is that their revenue structure relies almost entirely on transaction fees. Transaction fees account for approximately 97.5% of Dunamu's revenue and 99.99% of Bithumb's revenue, making fees essentially their sole income source. However, rather than any negligence in the exchanges' operational methods, this structure is a consequence of the regulatory environment faced by Korean crypto exchanges (detailed below).

Narrow Business Scope, Limited to Spot Crypto Trading

In reality, the business activities permissible for Korean crypto exchanges are limited to spot crypto trading. Most other areas are virtually inaccessible, either explicitly prohibited or implicitly avoided. Below are the businesses that Korean crypto exchanges are not permitted to operate:

- Tokenized Stocks: In June 2026, the Financial Services Commission (FSC) and the Financial Supervisory Service (FSS) began classifying tokenized stocks as securities rather than virtual assets. Regardless of the issuance format, securities are governed by the Capital Markets Act. Under the Electronic Securities Act, only licensed electronic registration agencies can perform electronic rights registration. If a crypto exchange that is not such an agency issues or circulates security tokens, it constitutes unlicensed business. In other words, tokenized stocks, which are developing rapidly overseas, are structurally prohibited assets for Korean crypto exchanges, and this situation is unlikely to change.

- Futures and Derivatives: Korean crypto exchanges can only offer spot trading; they cannot provide domestic users with derivatives like perpetual futures or options. This is less a matter of explicit legal prohibition and more a shadow cast by a previous attempt. Coinone, one of Korea's top five exchanges, operated a contract trading service with up to 4x leverage starting in December 2016 for about a year. In late 2017, following government regulatory measures and a police investigation, the service was completely shut down. In 2018, police treated it as gambling because the service operated without financial regulatory approval. CEO Cha Myung-hoon and others were referred to prosecutors on charges of running a casino, and 20 users with trading volumes exceeding 3 billion KRW were arrested on gambling charges. The case concluded three years later in 2021 without indictment due to insufficient evidence. However, no Korean crypto exchange has been involved in leveraged or futures trading since then.

- Implied Circumvention under Self-Regulation: Korean crypto exchanges are subject to self-regulation by the Digital Asset Exchange Alliance (DAXA), comprising the five major KRW exchanges. Its listing review criteria include opaqueness due to de-anonymization, potential for securitization, and potential for money laundering. These standards effectively exclude privacy coins emphasizing anonymity and lead exchanges to avoid listing tokens that could be considered securities. For the same reason, assets that could raise security or gambling controversies, such as exchange tokens or prediction market tokens, are rarely seen on Korean exchanges.

In summary, almost all new areas that overseas exchanges are expanding into—such as crypto derivatives, tokenized stocks, privacy coins, and prediction markets—are restricted for Korean exchanges.

Korean Exchanges Fall Behind in Global Competition

Have Korean Exchanges Lowered Their Listing Standards?

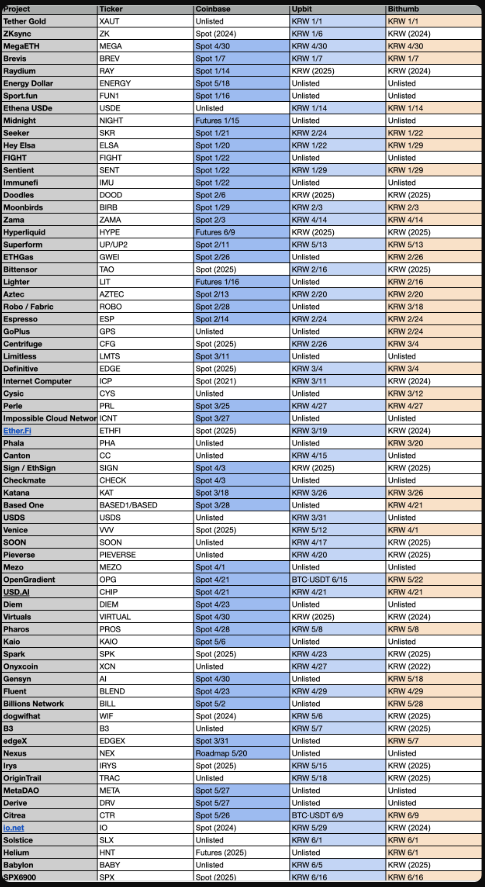

Recently, the community has accused Upbit and Bithumb of relaxing their listing review standards. The table below provides a complete comparison of tokens listed by Coinbase, Upbit, and Bithumb in 2026:

Tokens listed by Coinbase, Upbit, and Bithumb in 2026 Source: Four Pillars (@c4lvin)

In terms of the number of listed tokens, Coinbase leads. Coinbase lists many assets not available on the two Korean exchanges, and a significant portion offers not only spot trading but also futures trading, providing trading opportunities earlier than other platforms. Just based on frequency and timing, Coinbase is actually more aggressive.

In 2026, a considerable number of the new KRW tokens listed on Upbit had already been listed on Bithumb, such as Bittensor (TAO), Internet Computer (ICP), Ether.fi (ETHFI), io.net, dogwifhat, Spark (SPK), and Babylon. Most of these had low trading volume on Bithumb. They were not newly issued assets but tokens that had existed on the market for a while, only listed on Upbit later. This may make Upbit's listings seem less fresh.

This perception of declining token quality stems not from a lowering of standards per se, but from the diminishing effect of listing-induced trading volume. In an environment where trading volume from a single token listing quickly dries up and new assets worthy of listing become increasingly scarce, Upbit maintains its listing pace by adding tokens already listed on Bithumb.

Ultimately, user complaints in Korea are less about specific names and more about the perceived gap in convenience compared to other markets, which offer newer products like tokenized stocks.

Korean Exchanges Shut Out of the SpaceX Listing Feast

Meanwhile, large overseas exchanges are moving in the opposite direction. They are striving to transcend the limitations of virtual assets and build "everything exchanges"—a single application where all assets can be traded.

Coinbase is a prime example. In its Q4 2025 shareholder letter, Coinbase stated that besides cryptocurrencies and derivatives, it had begun trading stocks and ETFs within its app, offering early access to around 3,000 assets, aiming to integrate traditional and digital assets into a unified portfolio experience. The letter also highlighted that Coinbase had become the first in the industry to launch 24-hour US perpetual contract products, boosting its share of the derivatives market.

Binance's approach was more direct. From June 1, 2026, Binance opened US stock trading to eligible users, allowing them to trade over 7,000 US-listed stocks and ETFs directly. Furthermore, Binance launched bStocks, which tokenize US stocks on a one-to-one basis, settled in stablecoins, withdrawable to user self-custody wallets, and tradable 24/7.

Bybit joined the xStocks alliance and listed tokenized stocks created by a regulated Swiss issuer. These price-tracking tokens are backed by real stocks and trade 24/7 using stablecoins.

In short, overseas crypto trading platforms have made tokenized stocks a key promotional focus. The difference in trading environments between Korea and abroad was most starkly illustrated during the SpaceX listing. For overseas exchanges, this event tested their tokenized stock capabilities, and they launched pre-market contract products and tokenized stocks.

Within 24 hours of the SpaceX-related product launches, the total trading volume in the entire crypto market reached approximately $9 billion, with Binance alone accounting for $5.6 billion.

In stark contrast, Korean crypto exchanges were completely excluded from this feast. Whether tokenized stocks, perpetual contracts, or any other SpaceX-tracking products, none are permitted for trading within Korea. While major global exchanges traded billions of dollars around the same hot topic, Korean crypto exchanges had no channels to participate.

Korean Exchanges Stifled by Regulation

For an exchange that cannot compete globally in product variety, the only remaining battlefield is the crypto market itself. Since Korean exchanges' revenue effectively depends on spot trading fees, and they cannot list derivatives or stocks, the sole way to increase trading volume is to list eye-catching tokens at the right time.

Korea's strict regulation of crypto exchanges aims to protect investors. It treats leveraged trading as gambling and bans it. It filters out security-type tokens with opaque rights structures. It excludes assets easily used for money laundering or price manipulation from listing reviews.

However, as this protective mechanism systematically strips exchanges of their revenue sources and product lines, their only remaining tool becomes listing crypto spot assets. And the more crypto market trading volume shrinks, the more Korean exchanges tend towards listing assets that garner higher attention and are thus more speculative. Protection at the product stage ultimately fuels the influx of speculative assets at the listing stage. The recent listing of tokens similar to SpaceX's stock ticker by the two major exchanges is a microcosm of this trend.

A deeper problem is that even this protective mechanism is not entirely effective. Korean investors who want to buy perpetual contracts or tokenized stocks are not easily deterred; they simply turn to overseas platforms like Binance, Bybit, and Hyperliquid.

In other words, Korean regulation itself does not eliminate high-risk trading for investors; it merely pushes this high-risk trading outside the markets that Korean authorities can oversee. When taxation and the Crypto-Asset Reporting Framework (CARF) take full effect in 2027, the scale of this offshore trading will become apparent in the data. Ultimately, investors bear the speculative risk anyway, while losing domestic regulatory safeguards, and Korean exchanges lose the revenue these trades would have generated.

This structure also leaves Korean exchanges fragile, with a single product line, nearly all revenue from trading fees, and complete exposure to the cyclical volatility of trading volume. While Coinbase diversifies its revenue into custody, stablecoins, tokenized stocks, and derivatives to buffer market downturns, Korean exchanges must bear the same cyclical volatility solely with a single product. As this gap accumulates quarter by quarter, it eventually translates into differences in investment capability and product competitiveness, which become evident again, much like the perceived convenience gap felt by domestic users.

Of course, the Korean government is also actively pushing forward crypto regulation. A series of plans, including the second phase of the Digital Asset Basic Act, the institutionalization of Security Token Offerings (STOs), approval of corporate trading, and the issuance of KRW stablecoins and spot ETFs, are all set to be launched simultaneously in 2026, demonstrating the government's commitment. However, even if these new regulations are eventually implemented, they may not be operated by existing crypto exchanges but rather handed over to licensed entities like securities firms and electronic registration agencies.

Therefore, the ongoing convergence is not crypto exchanges transforming into securities firms, but securities firms and banks acquiring stakes in crypto exchanges and bringing them under the same umbrella. In 2026, Hanwha Investment & Securities increased its stake in Dunamu to 9.84%, becoming the third-largest shareholder. Hana Financial Group holds 6.55%, and Samsung Securities, Samsung Card, and Samsung SDS hold 4%. Korbit was acquired by Mirae Asset Group. Korea Investment & Securities signed a strategic equity investment agreement to acquire a 20% stake in Coinone, becoming its third-largest shareholder. As financial regulators remain cautious about the separation of finance and crypto and lean towards relaxing related restrictions, such alliances are rapidly increasing.

Is it likely that Korea will allow crypto exchanges to develop into "everything exchanges" like overseas? The possibility is minuscule.

However, this article does not advocate for the immediate removal of regulations. Instead, it argues that a protective framework designed for a bygone era is now generating significant hidden costs as the market rapidly trends towards asset convergence. Korean crypto exchanges operating under such a stringent environment will pass these costs onto users during bear markets like the current one, ultimately leading to the resurgence of fleeting, short-lived "shitcoins" as seen today, creating more victims.