เมื่อ 24/7 ไม่ใช่สิ่งที่หายากอีกต่อไป: CME น้ำมันดิบ, Binance หุ้นสหรัฐฯ รุมล้อม Hyperliquid จุดยึดมูลค่ากำลังสั่นคลอน

- มุมมองหลัก: CME, Binance และ NYSE/ICE ต่างกำลังเปิดตัวผลิตภัณฑ์การซื้อขายแบบโทเค็นหรือแบบ 24/7 ชั่วโมง ซึ่งลอกเลียนความสามารถในการซื้อขายสินทรัพย์แบบดั้งเดิมตลอด 24 ชั่วโมงที่ Hyperliquid เคยมีแต่เพียงผู้เดียว สิ่งนี้ทำให้เกิดการประเมินค่าจุดยึดมูลค่าของ HYPE ใหม่ จากการตรวจสอบผลประกอบการไปสู่การแข่งขันด้านความคาดหวัง

- ปัจจัยสำคัญ:

- CME วางแผนเปิดตัวสัญญาฟิวเจอร์สน้ำมันดิบ WTI ขนาดเล็ก 10 บาร์เรล และฟิวเจอร์สทองคำ 1 ออนซ์ ที่สามารถซื้อขายได้ 24/7 ในปี 2026 โดยเน้นย้ำถึงการอยู่ภายใต้การกำกับดูแลและเกณฑ์การเข้าถึงที่ต่ำ มีเป้าหมายเพื่อเติมเต็มช่องว่างในการบริหารความเสี่ยงในช่วงเวลาที่ตลาดแบบดั้งเดิมปิดทำการ

- Binance เปิดตัว bStocks ซึ่งนำเสนอการซื้อขายหุ้นโทเค็นของสหรัฐฯ เช่น NVDA, TSLA ตลอด 24/7 ชั่วโมง ซึ่งเป็นการก้าวไปสู่จุดเริ่มต้นของหุ้นโทเค็นที่นอกเหนือไปจากสัญญา Perpetual แบบสังเคราะห์

- ผลิตภัณฑ์เหล่านี้แม้จะมีรูปแบบที่แตกต่างกัน (ฟิวเจอร์ส, หุ้นโทเค็น, Perpetual บนเชน) แต่ก็ลอกเลียนแก่นเรื่องที่สำคัญที่สุดของ Hyperliquid นั่นคือ: การสามารถซื้อขายสินทรัพย์แบบดั้งเดิมได้แม้ในช่วงเวลาที่ตลาดปิดทำการ

- สำหรับ Hyperliquid แม้ว่าแรงเฉื่อยด้านสภาพคล่อง เลเวอเรจสูง และประสบการณ์บนเชนจะสามารถดึงดูดผู้ใช้บางส่วนไว้ได้ แต่ “ความเป็นเอกลักษณ์” ของการเปิดรับสินทรัพย์แบบดั้งเดิมกำลังลดลง ตลาดเริ่มตั้งคำถามถึงการเติบโตของปริมาณการซื้อขายและค่าธรรมเนียมในอนาคต

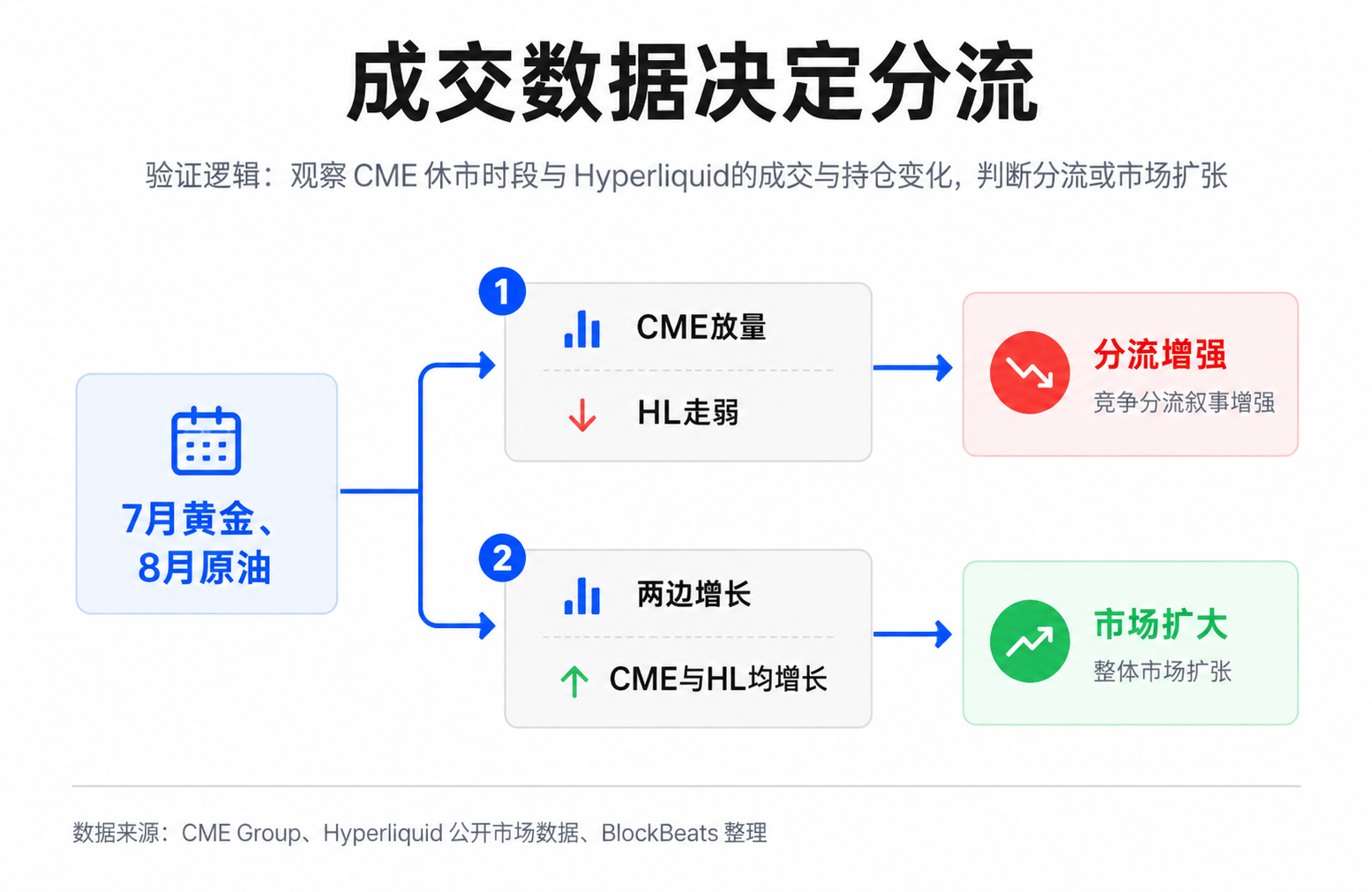

- ผลิตภัณฑ์ทองคำและน้ำมันดิบใหม่ของ CME มีแผนเปิดตัวในเดือนกรกฎาคมและสิงหาคม 2026 ซึ่งปริมาณการซื้อขายจริงและข้อมูล Depth ในช่วงกลางคืนและวันหยุดสุดสัปดาห์ในขณะนั้นจะเป็นหน้าต่างสังเกตการณ์สำคัญในการยืนยันว่าการแบ่งส่วนการแข่งขันนั้นเกิดขึ้นจริงหรือไม่

TL;DR

- CME plans to launch 24/7 trading for mini-sized crude oil and 1-ounce gold, as traditional markets are filling the risk management gap during off-hours.

- Binance, NYSE/ICE are also advancing 24/7 tokenized assets, and Hyperliquid's advantage of "trading traditional assets anytime" is being repriced.

- Related tokens: HYPE, CME, ICE, BNB, and products related to tokenized crude oil, gold, and US stocks.

HYPE's recent pullback can easily be attributed to unlocks, large holder selling, or issues with TradeXYZ's SpaceX pre-IPO. But on a longer timeline, another issue is becoming more important: Hyperliquid's ability to "trade traditional assets anytime," which was previously rewarded by the market, is now being replicated by traditional finance and centralized trading platforms.

On June 11, CME announced plans to launch 24/7 mini-sized WTI crude oil futures, subject to regulatory approval, and to extend its existing 1-ounce gold futures to 24/7 trading. Around the same time, according to public reports, Binance launched bStocks, allowing users to trade tokenized US stocks like NVDA and TSLA using liquidity from the main Binance exchange. NYSE/ICE is also developing its own 24/7 tokenized securities and on-chain settlement platform.

These products are not the same. CME deals with regulated futures, Binance bStocks is more akin to a tokenized stock entry point, and Hyperliquid offers on-chain perpetual contracts. However, they are vying for the same demand: when crude oil, gold, and US stocks are closed in traditional markets, traders still want immediate exposure or the ability to hedge risks instantly.

So this is not a story of "CME already stealing Hyperliquid's volume." CME's new crude oil product hasn't launched yet, and gold's 24/7 trading won't start until July. Actual diversion still needs to be verified by trading data. It's more like a repricing of expectations: if 24/7 is no longer a scarce capability unique to Hyperliquid, how should the market understand HYPE's valuation anchor?

24/7 Trading Is Evolving from a Crypto Advantage to an Industry Standard

For the average investor, the issue can be simplified: news doesn't wait for market open.

Geopolitical conflicts can happen over the weekend, instantly changing expectations for oil and gold prices. An earnings report, regulatory investigation, or unexpected event for a US-listed company can also occur outside traditional trading hours. In the past, traders either had to wait for the market to open, bearing the risk of price gaps, or find alternative tools for hedging. The crypto market, with its naturally 24/7 trading, has benefited from this.

Hyperliquid seized this gap. It's not just a crypto perpetual trading platform; it brings exposure to traditional assets like stocks, crude oil, and gold on-chain. Some third-party HIP-3 markets and ecosystem products even extend to earlier-stage assets. For some traders, Hyperliquid acts like a "convenience store for risk that never closes": when US stocks are closed or commodity futures lack liquidity, on-chain contracts still allow them to express a directional view, hedge, or even trade with leverage.

CME is now targeting this exact pain point. According to CME's June 11 announcement, the new 10-Barrel WTI crude oil futures will be approximately 10 barrels, one-tenth the size of the existing Micro WTI, scheduled for launch on August 30, 2026, and will be cash-settled. The existing 1-ounce gold futures are planned for 24/7 trading starting July 26, 2026, also cash-settled.

In simpler terms, mini-sized futures cut large commodity contracts into smaller units, allowing traders to manage risk with less capital and more precision. CME's Global Head of Commodities, Derek Sammann, stated in the announcement that amid geopolitical uncertainty, traders need regulated products of appropriate size available 24/7 to manage risk exposure when news breaks.

The key here isn't just "24/7," but also "regulated" and "appropriate size." The former targets institutional and compliant capital, while the latter lowers the entry barrier. CME doesn't necessarily need to replicate Hyperliquid's high leverage or on-chain experience; it aims to provide a different kind of 24/7 exposure: more traditional, more compliant, and more easily accepted by the existing financial system.

CME, Binance, and NYSE Target the Same Layer of Demand

While CME, Binance, and NYSE/ICE have different product forms, they are collectively replicating one of Hyperliquid's previously clearest advantages: the ability to trade traditional assets during market off-hours.

CME's entry point is commodities. Crude oil and gold are core assets for global macro trading. The greater the geopolitical tension, the stronger the demand for risk management outside trading hours. For traditional institutions, if CME provides sufficient liquidity at night and on weekends, they may not need to take on the additional compliance, custody, and operational risks of an on-chain perpetual platform.

Binance's entry point is US stock tokenization. According to public reports, the initial batch of bStocks includes NVDAB, TSLAB, CRCLB, MUB, SNDKB, emphasizing 24/7 trading, 1:1 conversion, and self-custody support. It's important to distinguish bStocks from other crypto stock products. bStocks is more like a tokenized stock entry point and should not be confused with stock perpetuals.

Think of tokenized stocks as "on-chain versions of stock certificates," different from Hyperliquid's synthetic perpetuals. Synthetic perpetuals are contracts that trade on price changes, where traders don't hold the actual stock. Tokenized stocks aim for price anchoring closer to the real asset and enhance trust through conversion mechanisms.

NYSE/ICE's direction is more like underlying infrastructure. In a January announcement, ICE/NYSE stated they are developing a platform for trading and settling tokenized securities on-chain, aiming to support 24/7 trading, instant settlement, orders in USD, and stablecoin transfers, pending regulatory approval. If realized, this would not just extend trading hours but move a part of the securities market's settlement and trading logic closer to an on-chain experience.

These three cannot be directly equated. CME futures have margin, delivery, and regulatory frameworks. Binance bStocks is more like a tokenized stock entry point on a centralized exchange. Hyperliquid perpetuals lean towards high leverage, on-chain margin, and fast speculation or hedging. Their users, risk controls, leverage, and KYC requirements differ.

However, market repricing doesn't require them to be identical. As long as they cover some of the same needs, Hyperliquid's narrative changes. The old narrative was: if you want to trade crude oil, gold, or US stock exposure anytime, on-chain perpetuals are one of the most direct ways. The new narrative becomes: you can still go to Hyperliquid, but you also have choices like CME, Binance, and potentially NYSE's tokenized platform in the future.

Hyperliquid Needs to Prove Traders Will Stay

For Hyperliquid supporters, the moves by CME and Binance are, of course, not perfect substitutes. The appeal of on-chain perpetuals has never been solely about 24/7 trading.

Hyperliquid's advantages include high leverage, self-custody, on-chain speed, trading culture, and an established liquidity network. For crypto-native traders and some high-frequency speculative capital, advantages like less KYC, faster listings, and more flexible margin usage are experiences that traditional platforms cannot easily replicate. Even if CME offers 24/7 crude oil and gold, it won't cause all traders willing to take on-chain risks and seek higher leverage to migrate immediately.

Liquidity itself creates inertia. Where traders go depends not only on product specifications but also on depth, slippage, fees, available leverage, and counterparty. If Hyperliquid already has deep order books for certain contracts, new compliant products may not immediately steal volume. Especially in the early stages, whether CME's night and weekend trading will be truly active remains to be seen in actual trading data, not just product announcements.

The pressure here is also clear: Hyperliquid can no longer rely solely on "we are 24/7" to justify the scarcity of its traditional asset exposure. It needs to prove that even when other platforms offer 24/7 trading, traders will still choose to keep their positions, margins, and volume here.

This will filter down to HYPE's valuation logic. Some investors typically view HYPE as a platform asset correlated with trading volume and fees: more trading means more fees, stronger protocol buyback capacity for HYPE, and a stronger cash flow narrative. This fee and buyback cycle has been a key reason HYPE has been distinguished from many pure narrative tokens in the past.

The moves by CME, Binance, and NYSE/ICE may not immediately change Hyperliquid's realized revenue, but they will alter market expectations for future revenue growth. HYPE's pullback can be explained by many factors, including unlocks, large holder behavior, overall risk appetite, and competitive expectations, not simply CME's new product. But when competitors start to fill the 24/7 capability gap, the market naturally asks: can the future volume growth in traditional asset perpetuals translate into fees and buybacks as smoothly as before?

This is why the current discussion feels more like a repricing of expectations rather than a verification of performance. CME's new crude oil contracts haven't launched, and there's no clear data on user migration between Binance bStocks and Hyperliquid's stock perpetuals. What is confirmed is that Hyperliquid's "uniqueness" in traditional asset exposure is diminishing. What is not confirmed is the extent to which this will translate into real volume loss.

July and August Will Provide the First Round of Verification

The real focus going forward isn't which platform announces 24/7 trading in its press release, but whether there will be actual trading volume and depth during off-hours.

CME's 1-ounce gold futures are planned for 24/7 trading starting July 26, 2026, and the new 10-barrel WTI crude oil futures are scheduled for August 30, 2026. These two milestones will provide the first batch of verification samples: whether night and weekend trading will be sufficiently active, spreads narrow enough, and whether institutions and professional traders will truly migrate their risk management back to regulated futures.

For Hyperliquid, the more direct observation metrics are the volume, open interest, and fee contribution of its corresponding commodity and stock perpetuals. If CME's gold and crude oil products start to see volume while Hyperliquid's corresponding market volume and open interest weaken simultaneously, the competitive diversion narrative will strengthen. If both grow, it may indicate that 24/7 trading is expanding the overall market rather than simply moving volume from on-chain to off-chain.

This is where the key for HYPE lies. Unlocks and large holder trading affect short-term prices, but the longer-term valuation anchor still rests on whether the platform can sustainably generate fees and convert those fees into buybacks. As long as trading volume and buyback strength can cover new supply and emotional pressure, competitive expectations may not necessarily turn into a trend of damage. Conversely, if growth in traditional asset perpetuals slows down while external platforms' 24/7 liquidity begins to form, the market's pricing of HYPE could shift from a "high-growth platform token" to a more cautious cash flow expectation.

It's not yet time to draw conclusions about Hyperliquid. A more accurate statement is that the demand it pioneered and validated is now being acknowledged and replicated by larger financial platforms. The next round of data will determine whether this repricing remains at the narrative level or continues to filter down to revenue and token prices.