龙头倒下,加密ATM告别扩张时代

- Core Insight: Bitcoin ATM giant Bitcoin Depot has filed for bankruptcy due to stricter regulations, rampant fraud, and a collapsing profit model, highlighting the industry's inherent flaws of high fees and high compliance costs, relegating it to a niche channel serving only small-scale cash transactions.

- Key Elements:

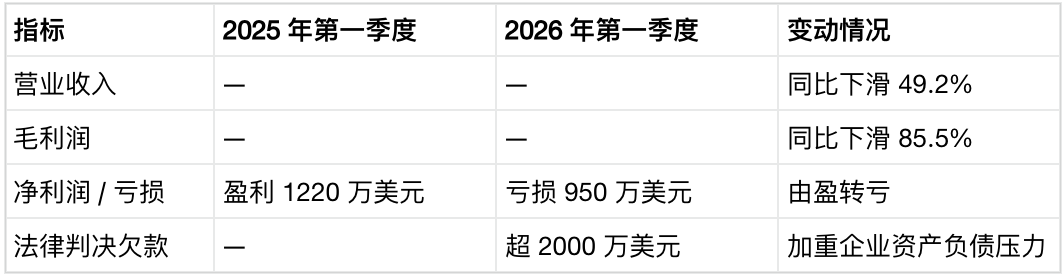

- Bitcoin Depot filed for Chapter 11 bankruptcy. Its Q1 2026 revenue plummeted 49.2% year-over-year, with a net loss of $9.5 million, compared to a $12.2 million profit in the same period last year.

- The U.S. Federal Bureau of Investigation received 13,000 crypto ATM-related complaints in 2025, with total losses reaching $389 million, a 58% increase year-over-year. Losses among the elderly accounted for $257.5 million.

- Multiple U.S. states have enacted bans or heavy penalties, such as Indiana's comprehensive ban and Tennessee classifying it as a Class A misdemeanor, driving regulatory crackdowns.

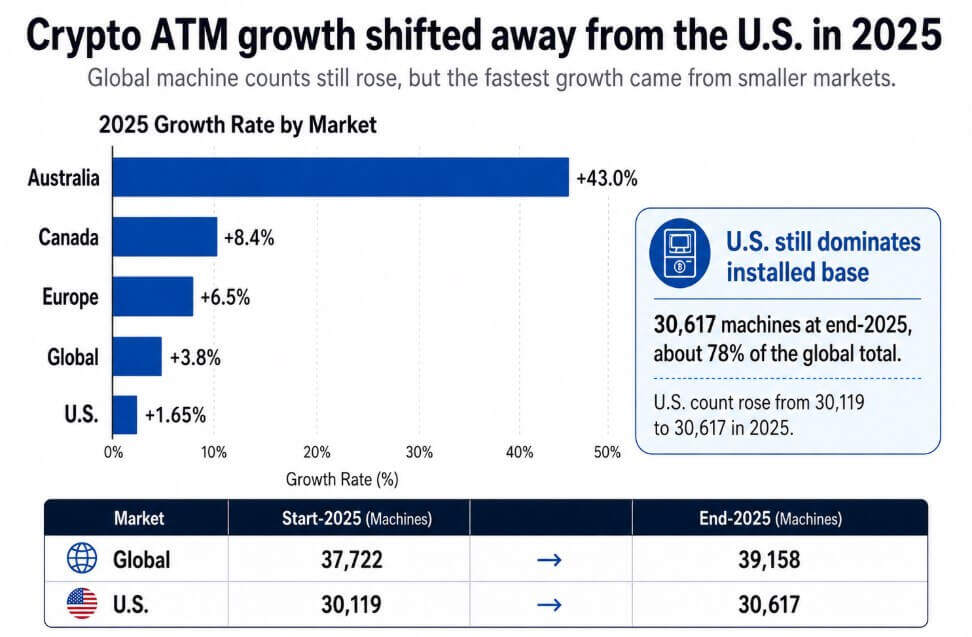

- The global number of Bitcoin ATMs increased to 39,000 in 2025, but growth in the U.S. was nearly stagnant at just 1.65%. Australia saw a 43% growth rate amid more relaxed regulatory attitudes.

- FinCEN regulations have resulted in ATM fees of 7%-20%, far exceeding those of online exchanges. Additionally, compliance costs like KYC have completely eroded any profit advantage.

Original Author: Gino Matos

Original Translation: Saoirse, Foresight News

On May 18, 2026, Bitcoin Depot, a leading Bitcoin ATM operator, filed for Chapter 11 bankruptcy protection in the U.S. District Court for the Southern District of Texas, announcing a complete shutdown of its operations and the disposal of its assets. Its global network of over 9,000 machines, which it had as of August 2025, also ceased operations on the same day.

Financial data disclosed by the U.S. Securities and Exchange Commission on May 12 showed that the company's revenue in the first quarter of 2026 plummeted 49.2% year-over-year, while gross profit nosedived 85.5%. Management stated that there is substantial doubt regarding the company's ability to continue as a going concern. The company had reported a net profit of $12.2 million in the same period last year, but directly incurred a loss of $9.5 million in the first quarter of this year.

Bitcoin Depot attributed its deteriorating operations to: operational restrictions imposed by state and local governments, platform trading limit reductions, stricter KYC standards for users, a slew of lawsuits, and accumulated legal judgments requiring the company to pay over $20 million in damages.

This series of operational chaos ultimately drove the company into bankruptcy, vividly illustrating how increasingly stringent regulatory compliance has completely dismantled the original profit logic of Bitcoin ATMs.

The Original Positioning of Bitcoin ATMs

Bitcoin ATMs allow users to exchange cash for cryptocurrencies without linking a bank account, serving those who prefer cash transactions, lack access to formal banking services, or wish to transact offline rather than through online exchanges.

However, this business model has had a structural flaw from its inception. The U.S. Financial Crimes Enforcement Network stipulates that transaction fees for crypto ATMs range from 7% to 20%, far higher than the rates of mainstream online cryptocurrency exchanges.

Such high fees can only support niche needs like emergency transactions or one-time small cash exchanges, making widespread adoption fundamentally impossible. These offline machines were inherently a high-cost entry point to cryptocurrencies, and relying on them for low-cost, high-frequency user transactions to generate profit was never viable from the start.

Data from the Federal Trade Commission shows that in the first half of 2024, nationwide reports of Bitcoin ATM-related scams resulted in total losses exceeding $65 million, with an average loss of $10,000 per scam case. Statistics from the Federal Bureau of Investigation for 2025 indicate that the bureau received 13,460 complaints related to offline cryptocurrency machines that year, with total losses amounting to $389 million, a year-over-year increase of 58%.

Among these, total losses for seniors aged 60 and over were approximately $257.5 million. The large number of elderly victims has provided strong public and policy support for regulatory crackdowns, which have been far more stringent than typical anti-money laundering measures.

Many parts of the U.S. have already enacted strict control policies: Indiana has completely banned all virtual currency kiosks within its borders; Tennessee has classified the installation and operation of such machines as a Class A misdemeanor; Minnesota has also passed a relevant ban, set to take effect in 2026.

Rigorous user identity verification mechanisms have significantly reduced machine transaction volume, with scam warnings and lowered transaction limits further depressing per-device revenue. Coupled with various litigation costs, this exacerbated the company's existing $20 million in legal debts, forming the core reason for Bitcoin Depot's bankruptcy.

The very compliance measures intended to regulate the industry and reduce transaction risks ultimately erased the remaining profit advantage of the high-fee model.

Compiled data from industry research institutions shows that in 2025, the global number of Bitcoin ATMs increased from 37,722 to 39,158, an average daily increase of about 4 units.

By the end of 2025, the number of crypto ATMs in the United States reached 30,617, accounting for 78% of the global total. However, compared to 30,119 units at the start of the year, the annual growth rate was only 1.65%, indicating a nearly stagnant market.

In contrast, the development trajectory in other overseas markets was markedly different: Australia added 601 crypto ATMs in the year, a growth rate of 43%; Canada saw a growth rate of 8.4%, and Europe's rate was 6.5%. The core reason these regions continue to deploy crypto ATMs is that local regulators view them as convenient tools for enhancing inclusive financial services, rather than taking a harsh stance against them.

In 2025, the global number of cryptocurrency ATMs grew by 3.8% to 39,158, with Australia surging 43% while the U.S. grew just 1.65%.

Two Major Future Development Paths for the Crypto ATM Industry

Optimistic Development Scenario

Acquirers purchase Bitcoin Depot's high-quality existing assets, gradually restarting offline operations in U.S. states that haven't enacted bans, while the global crypto ATM market continues its slow, steady expansion.

New operators proactively absorb high compliance operation costs, transforming offline machines into regulated cash-to-crypto channels. While transaction volumes shrink and profit margins are significantly compressed, stable operations can still be maintained.

Industry-wide profits continue to erode, but crypto ATMs remain in the market, serving niche users who cannot or will not use online exchanges, becoming a legitimate, compliant cash-to-crypto transaction channel within a specific segment.

Bitcoin Depot has also stated its plan to orderly dispose of all its assets. This means its large inventory of offline physical machines could potentially re-enter the market under new ownership.

Under this development model, crypto ATMs would operate like physical cash exchange outlets, characterized by high fees and low volume, surviving on fixed niche demand. This model is only suitable for operators willing to accept a thin-margin business.

Pessimistic Decline Scenario

If the strict regulatory bans in Indiana, Tennessee, and Minnesota become a mainstream U.S. market trend, rather than regional anomalies, the scale of the U.S. crypto ATM market will shrink dramatically.

The 30,617 crypto ATMs currently in the U.S. account for nearly 80% of the global market share. Successive state-level bans would directly eliminate a large number of machines. Bitcoin Depot's nearly 9,000 offline machine locations held a 23% global market share by the end of 2025. If these devices are permanently shut down, the global installed base will suffer a severe blow, even before new regulations are introduced in other states.

Even without outright operational bans, strict KYC rules, transaction limit constraints, transaction liability, and incessant legal disputes will completely erode the profitability of high-fee crypto ATMs. This will likely lead to a voluntary, gradual withdrawal of industry machines from the market.

A Cash Transaction Channel Struggling to Scale

Today, the channels for cryptocurrency adoption extend far beyond offline kiosks. Data from blockchain analytics firms indicates that between July 2024 and June 2025, over $1.2 trillion in fiat currency flowed into major online cryptocurrency exchanges alone.

Spot crypto ETFs, mobile digital wallets, stablecoins, and various institutional compliant trading channels have become the core drivers of cryptocurrency adoption. In the 2025 Global Crypto Adoption Index, India, the U.S., Pakistan, Vietnam, and Brazil topped the list, all of which primarily rely on online exchanges, mobile trading, and institutional compliant channels for adoption.

Upon inception, Bitcoin ATMs built an offline transaction channel for cash-preferring users, bringing cryptocurrencies into physical retail scenarios and filling a market gap for offline crypto transactions.

Nevertheless, the stark fee disparity between offline machines and online exchanges destined them to never enter the mainstream market. Meanwhile, the potential for high profits from offline transactions fostered scam activities involving hundreds of millions of dollars.

In the future, only compliant crypto ATMs operating in regions with lax regulatory policies are likely to survive, continuing to serve the niche population with a rigid demand for offline cash transactions.

Looking back at the industry's development history, it's clear that crypto ATMs were, from the start, a high-cost entry channel. They demonstrated the possibility of offline cryptocurrency transactions to the masses but failed to consistently achieve low cost, high security, and high convenience. They ultimately missed the opportunity to become mainstream transaction infrastructure.