比值修复下半场:黄金让位,比特币何时登场?

- 核心观点:比特币/黄金比值已在2026年2月触底,此后因黄金回调而回升46%,预计周线金叉将于6月形成,下半年比特币将跑赢黄金,但宏观环境因高通胀、鹰派美联储及地缘冲突而更复杂。

- 关键要素:

- 比特币/黄金比值从2月低点12.5回升至17.6,因黄金从5589美元历史高点回调18%,而非比特币强势拉升。

- 周线9/21 EMA多头金叉预计于2026年6月第一周形成,历史数据显示金叉后比值涨幅可达148%至641%。

- 美国CPI通胀率达3.8%,美联储降息预期落空,新任主席沃什于5月上任,市场转向鹰派定价,削弱了比特币上涨的流动性支撑。

- 中国央行连续17个月增持黄金,总量达2313吨,占比扩至9.6%,全球央行购金意愿持续,为黄金价格提供底部支撑。

- 比特币从6.5万美元稳步回升至8万美元附近,市场持仓结构更健康,但行情修复仍依赖黄金走弱,尚未切换至比特币主导拉升阶段。

- 下半年核心矛盾为美联储鹰派政策与财政宽松刚需之间的博弈,中美领导人会晤及美伊局势缓和可能成为风险偏好回暖的催化事件。

- 当前比值距离2025年10月31.5的高点仍有巨大修复空间,在保守假设下(比特币8-10万美元,黄金4200-4700美元)比值可升至19至21.3。

Original Author: that1618guy, Analyst at Delphi Digital

Original Translation: Chopper, Foresight News

Three months ago, I published the article "Bitcoin vs. Gold: Positioning for the Next Relative Cycle" with a very clear core thesis: Within the weekly 9/21 Exponential Moving Average (EMA) framework, the Bitcoin/Gold ratio had dropped to its second-largest retracement in history, data-wise nearing a bottom. (Note: The weekly 9/21 EMA is a commonly used trend-following signal combination for determining trends and inflection points.)

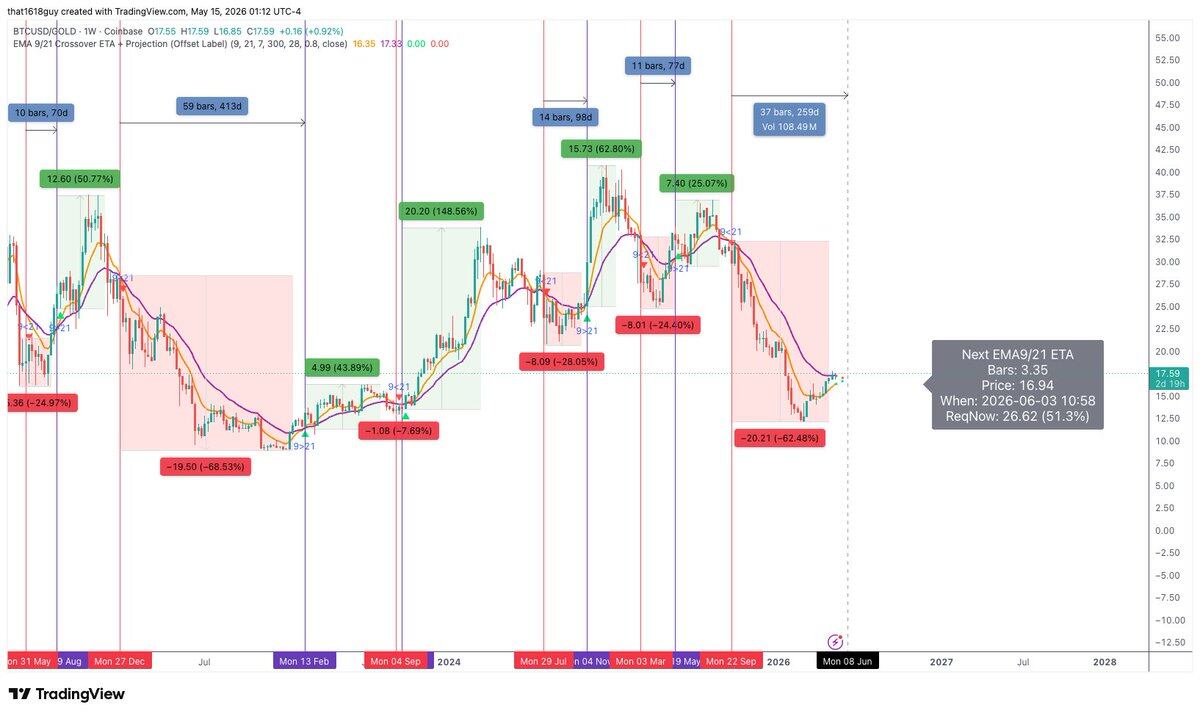

This thesis has now played out. The ratio has recovered approximately 46% from its February low. Gold has corrected 18% from its all-time high of $5,589, while Bitcoin has steadily climbed from the $65,000 range back to near $80,000. The primary confirmation signal, the weekly 9/21 EMA golden cross, is currently projected to officially form in the first week of June. Historically, when a golden cross follows a deep death cross, the subsequent ratio rallies have been 148%, 641%, and 148%, respectively.

However, the macro environment has changed dramatically. With the current inflation rate at 3.8%, expectations for a Fed rate cut completely dashed, the ongoing US-Iran conflict, and Kevin Warsh officially assuming the role of Federal Reserve Chair on May 13, the market landscape for H2 2026 is far more complex than in February. Nevertheless, the overarching trend of Bitcoin strengthening relative to gold remains unchanged.

This article will review the previous forecast for the Bitcoin/Gold ratio, assess how the gold and macro perspectives from the "2026 Market Outlook" have materialized, and provide an updated analytical framework for the second half of the year.

Bitcoin/Gold Ratio Recovery Underway

When the article was published in late February, the Bitcoin/Gold ratio was hovering around 12.5 to 13, at historically extreme lows. At that time, Bitcoin was priced around $65,000, while gold was at $5,100 after a significant rally.

Now, the ratio has risen to 17.6, a substantial increase from the lows. This rebound has been entirely driven by one specific price action: it's not Bitcoin's explosive rally, but gold's price correction that has allowed it to show relative strength. This is the scenario I highlighted in my previous article that is most easily overlooked by the market. Few realize that the core driver of Bitcoin outperforming gold recently has been gold's weakness, which has been the market reality since mid-February.

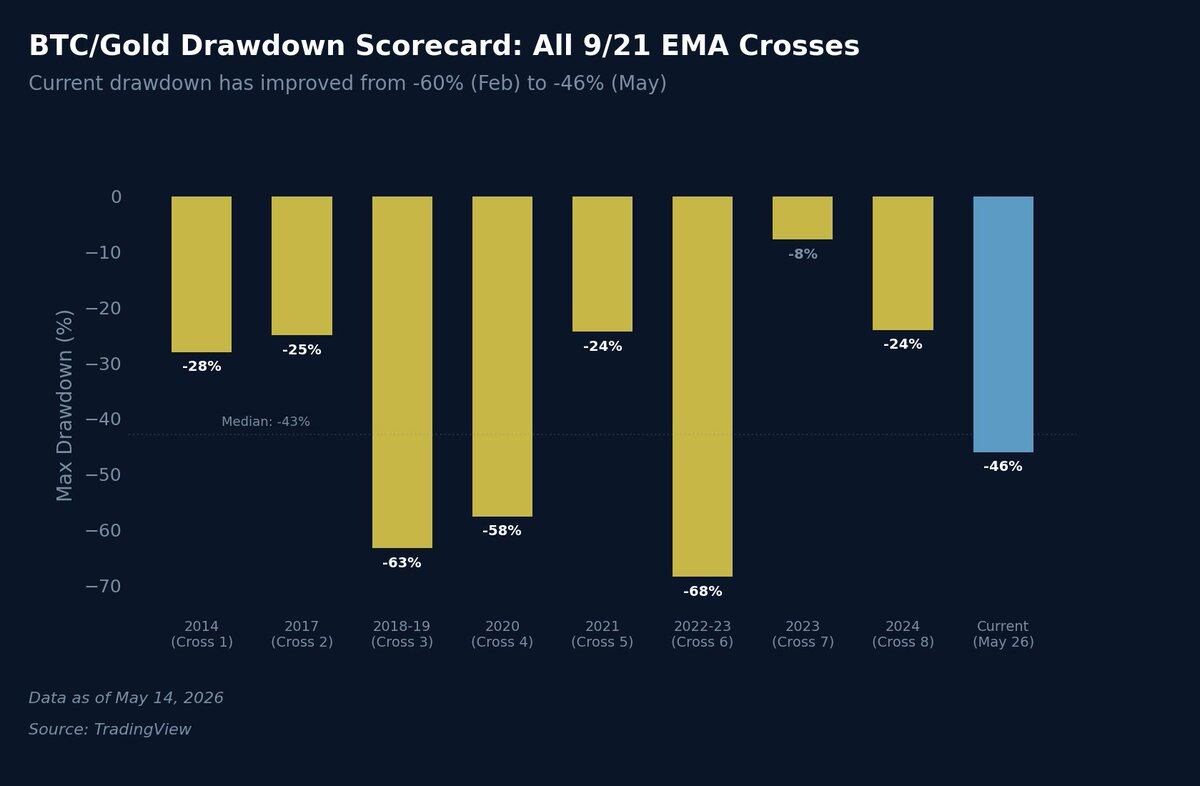

The retracement of the ratio from its October 2025 highs has narrowed from approximately 60% to 46%. While still deep from a historical perspective, it has exited the extreme trough and moved from the second-largest retracement to a moderate retracement level.

Looking back at eight historical downturns, only the 2018 bear market (63% retracement) and the 2022 bear market (69% retracement) saw deeper declines than the February lows. The current retracement of 46% is now close to the historical median retracement of 43%, showing significant market repair compared to the extreme lows three months ago.

The convergence of the 9/21 weekly EMAs, which I previously highlighted as a key event, hasn't fully materialized yet. Both moving averages are still in a bearish (death cross) configuration, but the gap between them is narrowing rapidly. Based on trading models, it will take approximately 3.5 more weekly candlesticks for a bullish golden cross to occur, which points to around the first week of June 2026.

After the previous weekly death cross, the Bitcoin/Gold ratio plunged 62%, closely mirroring the three historical deep death crosses (2018: -63%, 2020: -57%, 2022: -68%). This technical framework has been fully validated during the downtrend.

Similarly, the uptrend phase offers a strong reference. Once a golden cross is confirmed and holds, history suggests a powerful rally often follows. The golden crosses following the three deepest death crosses yielded ratio gains of 148%, 641%, and 148%. Even for shallower retracements, post-golden cross rallies ranged from 25% to 62%.

A critical caveat: not all moving average golden crosses are sustainable. A false breakout occurred in 2023, where the cross quickly reversed, leading to a 7.69% decline in the ratio—the smallest and shortest death cross in the statistical sample. Investors can use momentum indicators like MACD or Stochastic to assess the strength of a golden cross and distinguish genuine signals from false ones.

I maintain my view that Bitcoin will continue to outperform gold for the remainder of 2026, a trend that could even extend into the first half of 2027. The core market focus now is on the magnitude of the potential rally once the golden cross is confirmed and holds.

Reviewing the Annual Gold Forecast

In the "2026 Market Outlook" report, with gold trading around $4,600, we identified it as one of the most notable asset classes. We clearly pointed to solid structural tailwinds: continued central bank gold accumulation (especially by the People's Bank of China), fiscal deficits fueling currency debasement, and the global trend of de-dollarizing foreign exchange reserves.

Following this, gold rallied sharply, reaching an all-time high of $5,589 on January 28, 2026, a gain of over 26% from our initial assessment. Currently, gold has pulled back to around $4,700, a 16% decline from its high. Three factors converged to cause this reversal:

- In January, Kevin Warsh was nominated as Fed Chair, leading to a rapid hawkish repricing by the market and substantial profit-taking after gold's rally.

- The US-Iran military conflict erupted on February 28, pushing oil prices above $100/barrel, further increasing inflationary pressure. The April US CPI inflation rate rose to 3.8%, its highest since May 2023, crushing hopes for Fed rate cuts. While gold can hedge multiple risks, a prolonged period of high interest rates acts as a significant headwind for a non-yielding asset.

- The heightened hawkish expectations drove the US Dollar Index higher, adding further pressure on gold prices.

As mentioned in our annual outlook, gold's weekly RSI briefly exceeded 85, entering extremely overbought territory rarely seen in modern history. This signaled an inevitable slowdown in short-term upward momentum and a likely period of consolidation—a prediction that has now fully materialized.

Gold's historic rally is now in a digestion and adjustment phase, but the underlying structural buying has not dissipated. The short-term weakness is merely being temporarily suppressed by adjustments to rate expectations and a stronger dollar.

PBoC Continues to Accumulate Gold

The view from the annual outlook regarding the People's Bank of China's (PBoC) gold accumulation has also fully materialized. The report stated that the PBoC is one of the largest and most consistent gold buyers globally; that China's continued accumulation is a key part of its national strategic layout, potentially using its ample gold reserves to optimize debt structure and build a cross-border RMB settlement system.

Since the annual report was published, the PBoC has increased its gold reserves for 17 consecutive months, reaching a total official gold reserve of 2,313 tons, representing 9.6% of its total foreign exchange reserves (data from the World Gold Council). In March 2026 alone, it purchased about 5 tons, the largest monthly increase in nearly a year.

Global central bank gold buying remains robust. Net purchases by global central banks in Q1 2026 totaled 244 tons, higher than the previous quarter's total and the five-year average. While Goldman Sachs had forecasted average monthly purchases of 70 tons for 2026, the actual pace has been slightly lower (the PBoC added only 1 and 1.2 tons in Jan-Feb), but the increased buying in March confirms that the central bank's purchase rhythm is driven by actual market demand, not a gradual exit.

The most telling market signal is that the PBoC has not stopped buying even with gold above $5,000. Historically, central banks often pause purchases or even sell after new highs. However, as we predicted, the aggressive buying during this significant price rally proves this is a long-term structural strategic allocation, not short-term speculative hoarding.

This trend is deeply intertwined with the relative strength logic between Bitcoin and gold. The PBoC's sustained large-scale gold purchases are essentially a statement on the creditworthiness of the US dollar. For every ton of gold bought, a ton of reserve assets is moved out of the dollar system. The de-dollarization wave is accelerating.

According to a March 2026 World Gold Council survey, the proportion of central banks planning to increase their gold reserves within the year rose from 62% in 2025 to 68%. Despite short-term headwinds like the Fed's hawkish stance, a strong dollar, and rate hike fears suppressing gold prices, this structural central bank buying provides a solid floor. This significantly limits gold's downside, meaning that for the Bitcoin/Gold ratio to continue its recovery, it will increasingly depend on Bitcoin attracting capital on its own merits—the second type of market scenario.

Reviewing Bitcoin and Gold's YTD Performance

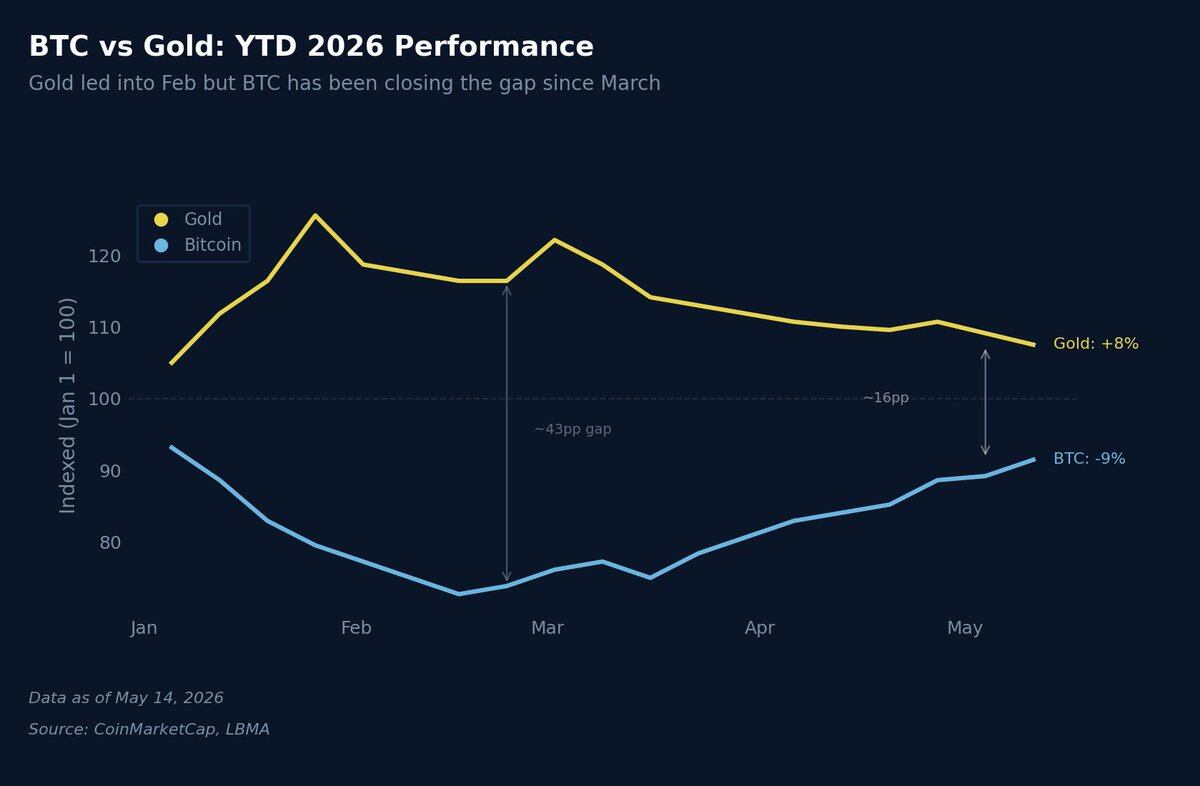

Looking at year-to-date (YTD) performance from January 1, 2026, the market trend is clear. Gold surged early in the year, with YTD gains reaching as high as 25% by the end of January. In contrast, Bitcoin's YTD decline was around 25%, marking an extreme divergence in asset performance. This divergence was exactly the point at which I predicted the ratio would bottom in February.

Since then, the performance of the two assets has converged: gold has given back most of its YTD gains, now up only 8% YTD. Bitcoin has narrowed its maximum YTD decline of 27% to just 9%. The difference in their YTD performance has shrunk from 50 percentage points to 17 percentage points, a direct reflection of the ongoing recovery in the Bitcoin/Gold ratio.

This convergence has been driven almost entirely by gold's weakening rather than a strong Bitcoin rally, which offers important insights for asset allocation. The current dominant market logic remains the first scenario (gold correction, Bitcoin sideways). The core market suspense for H2 is whether the market can switch to the second scenario (Bitcoin attracting capital for a rally) or will remain in a prolonged range-bound consolidation.

An additional historical correlation pattern: Past data suggests that movements in gold and global broad money supply (M2) often lead Bitcoin by 3 to 4 months. When gold broke out and rallied in mid-2025, global M2 supply was also hitting new highs. According to this time-lag pattern, Bitcoin should have rallied in late 2025 to early 2026. However, this did not materialize; the lag period has extended to 5 to 6 months. This type of delayed correlation is not unprecedented. The 2020 COVID shock also extended the correlation cycle, and when the linkage eventually reasserted itself, it was followed by significant price volatility.

Today's US-Iran geopolitical conflict is playing a role similar to the pandemic, introducing new inflationary pressures and directly postponing the Bitcoin rally that loose liquidity signals were supposed to catalyze.

What Has Changed in the Market Since February

Three months have passed since the previous report, and the market environment has changed substantively. Here is a review of the forecasts made:

Confirmed Forecasts

- The Bitcoin/Gold ratio bottomed as predicted within the forecast range, initiating a recovery driven by gold's correction.

- The deep correction in gold after its rally has materialized.

- The trend of global central banks continuing to accumulate gold remains unchanged.

- The convergence pace of the weekly 9/21 EMAs is broadly in line with the previously estimated timeline.

Unfulfilled Forecasts

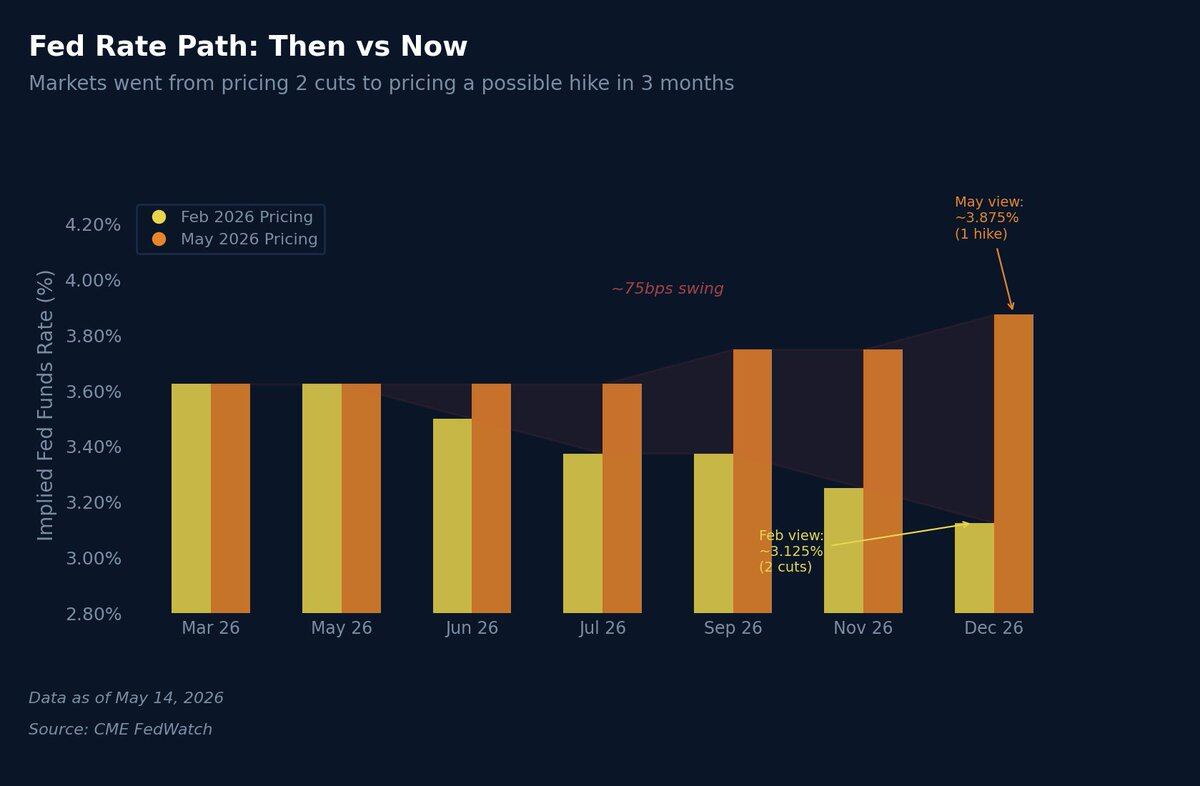

Expectations for a Fed rate cut have completely evaporated. In February, my base case was for 1 to 2 rate cuts by the Fed in H2 2026, a view widely shared by the market. This logic is now entirely invalid. With US CPI inflation at 3.8%, rising PPI, oil prices holding above the $100 mark, and the US-Iran conflict continuously feeding supply-side inflation, the market has not only abandoned rate cut expectations but is beginning to price in the possibility of rate hikes by year-end. This is the most significant logical deviation from my earlier thesis.

Interest rate market expectations have undergone a dramatic reversal. In February, the market expected the December 2026 federal funds rate to be 3.125%, implying two cuts. Now, market pricing suggests the year-end rate will be flat or higher, with the implied rate near 3.875%. In just three months, the shift in market rate expectations is a massive 75 basis points, driven primarily by the energy inflation shock from the geopolitical conflict.

The change in Fed leadership has also broken the previous expectation of looser policy. The market previously thought that a post-Powell chair would lean dovish. However, Kevin Warsh, now officially in office, holds a much more hawkish policy stance than Powell. His first FOMC meeting is scheduled for June 16-17. Under his leadership, it is very difficult to see the Fed embarking on a significant easing cycle, even if economic growth slows. This directly alters the risk asset rotation logic I had predicted for H2. Market models currently price the probability of a rate cut at this meeting at virtually zero.

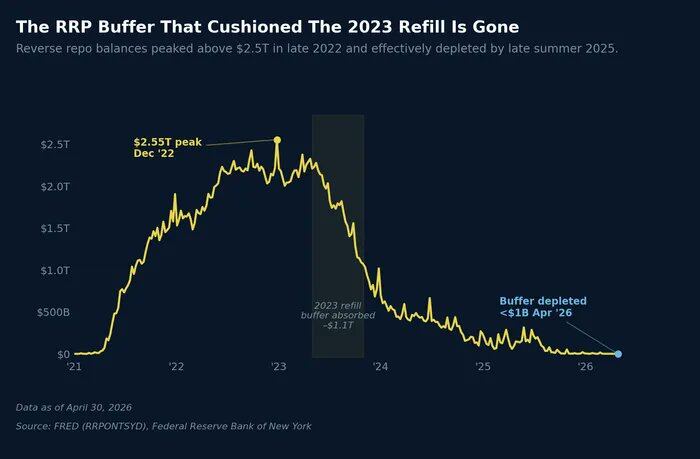

However, the previously proposed market logic of fiscal dominance remains intact. The US is pushing forward with debt monetization through the banking system. The annual fiscal deficit remains in the $1.5 to $2 trillion range. Regardless of the Fed's monetary policy stance, the sheer weight of fiscal pressure will eventually force more liquidity into the market.

US national debt has now surpassed $39 trillion. The Treasury still needs the market to absorb a massive supply of new bonds. Hedge fund basis trades continue to support long-end rates, and the balance of the overnight reverse repurchase facility (ON RRP) remains low.

Even if Warsh rhetorically maintains a hawkish tightening stance, the underlying functioning of the financial system requires liquidity support. The core contradiction for H2 is the tug-of-war between the Fed's hawkish monetary policy stance and the fiscal side's inherent need for accommodation.

Overall Market Landscape for H2 2026

My core thesis remains unchanged: the Bitcoin/Gold ratio is beginning to recover from historically extreme lows, and the overall trend is positive. The key drivers for H2 are as follows:

Gold Side

Gold's 18% correction from its all-time high has already provided ample room for the ratio to recover. Even if gold does not fall further and merely consolidates to digest its previous gains, Bitcoin's higher price elasticity means any positive market signal could drive the ratio higher. Combined with the structural support from continuous global central bank buying, gold's price floor appears locked in the $4,200 to $4,500 range. This relative strength cycle does not require a significant crash in gold; it only needs gold's rally to pause.

Bitcoin Side

Compared to February, the current positioning structure in the Bitcoin market is healthier. Since rallying from its $64,000 low, it has steadily climbed to $80,000 over more than ten weeks, successfully digesting multiple headwinds like the US-Iran conflict, the change in Fed leadership, and adjusted inflation expectations, without making new lows.

The key catalytic event I am focusing on is the potential meeting between US and Chinese leaders. Substantive progress on a trade truce, combined with a de-escalation in US-Iran tensions, could quickly revive market risk appetite. Bitcoin market positioning is currently subdued. If risk