Smart money hoards $40B in cash awaiting the tide to turn, while retail investors pile $2.6 trillion into call options: The US stock market's AI narrative reaches a tipping point

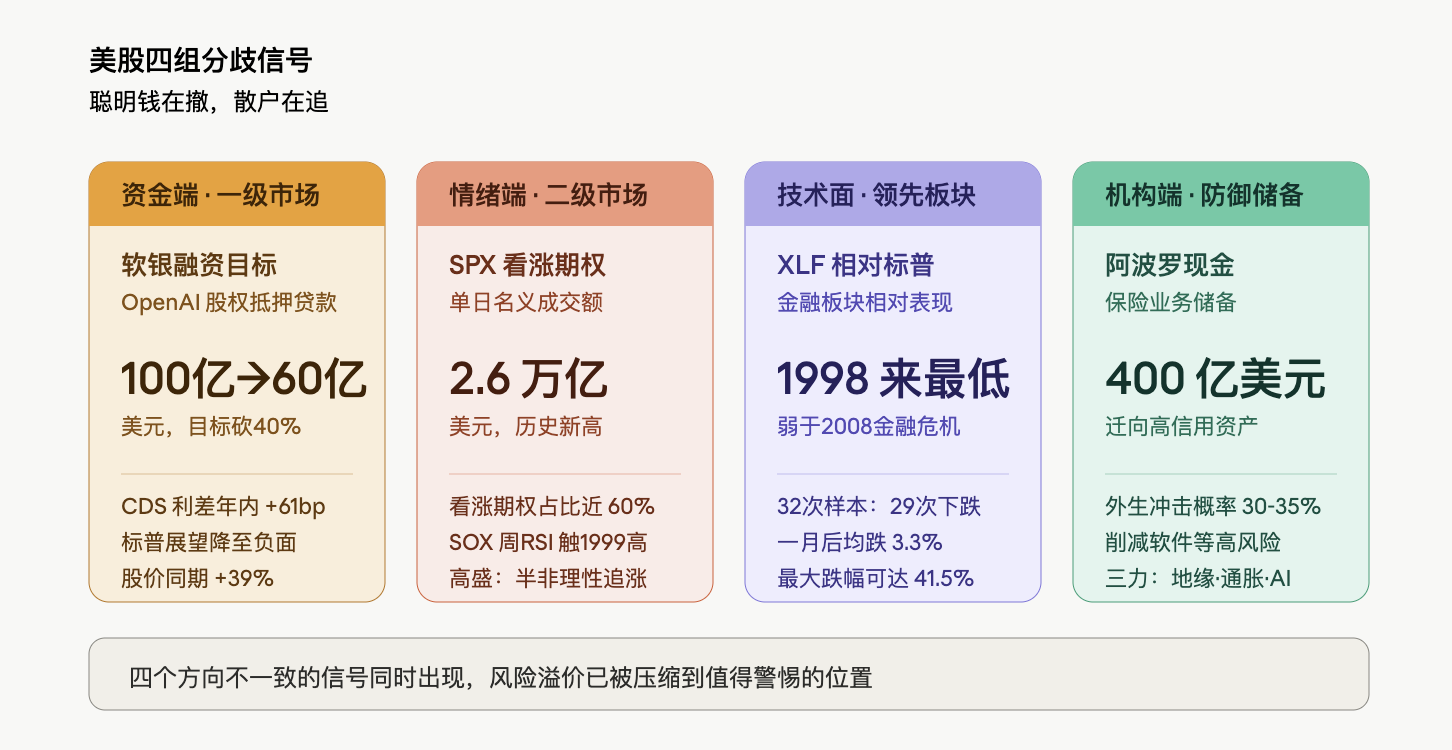

- Core Insight: The current US stock market shows a significant divergence: the S&P 500 has hit new highs, but the financial sector has fallen 6% year-to-date. Options market sentiment is extreme (with single-day call option volume reaching $2.6 trillion), while primary markets and institutional behavior (e.g., SoftBank's downgraded financing, Apollo reserving $40 billion in cash) are sending defensive signals, suggesting risk premiums are excessively compressed.

- Key Elements:

- SoftBank has lowered its financing target, backed by OpenAI equity, from $10 billion to $6 billion (a 40% reduction), mainly due to lenders' doubts about OpenAI's valuation and the company's failure to meet internal sales and user targets.

- Single-day notional value of S&P 500 call options reached a record $2.6 trillion. Goldman Sachs describes the market as being in a "semi-irrational momentum-chasing mode," with the Philadelphia Semiconductor Index's weekly RSI climbing to its highest level since 1999.

- The US financial sector (XLF) has accumulated a loss of about 6% year-to-date, while the S&P 500 has risen 7% over the same period. Its relative performance is the weakest since 1998, seen as a leading warning signal for economic liquidity and risk appetite.

- Apollo Global Management's CEO estimates the probability of an exogenous shock at 30%-35%, has reserved approximately $40 billion in cash within its insurance operations, and is simultaneously reducing high-risk exposure, exhibiting a markedly defensive posture.

- Consumer-side divergence: Whirlpool plunged 16% due to a "sharp deterioration in macroeconomic conditions," while DoorDash rose approximately 10% on strong demand for small-ticket, immediate consumption items, underscoring the structural contradictions within the market.

Source: TechFlow

An extremely unusual divergence is unfolding in the U.S. stock market. While the S&P 500 repeatedly hits new highs, the financial sector has fallen 6% year-to-date, underperforming the broader market even more severely than during the 2008 financial crisis and the COVID-19 shock. At the same time, the single-day notional trading volume of S&P 500 call options surpassed $2.6 trillion, setting a new record, while the RSI of the Philadelphia Semiconductor Index reached its highest level since 1999. In the primary market, SoftBank's financing plan, backed by its OpenAI equity as collateral, was forced to reduce its target size from $10 billion to $6 billion. On the institutional side, Apollo has already accumulated around $40 billion in cash reserves within its insurance business. Smart money is pulling back while retail investors are chasing.

The narrative revolving around the scarcity of AI computing power continues to drive the acceleration of U.S. tech stocks, but signals from capital flows, sentiment, technical indicators, and institutional actions are pointing in conflicting directions. This divergence itself merits closer scrutiny than any single data point.

Lenders Skeptical of OpenAI's Valuation, SoftBank Cuts Financing Target by 40%

According to Bloomberg citing insiders, SoftBank has lowered its target size for a margin loan backed by its OpenAI equity from $10 billion to at least $6 billion, a reduction of 40%. The core obstacle lies in valuation. Some investors solicited for participation have reservations about how to determine a fair value for OpenAI, a private company. Potential lenders involved in the discussions include private credit institutions, financial entities, and hedge funds, with related talks initiated as early as mid-March.

OpenAI's own fundamentals are also under pressure. The company reportedly failed to meet its monthly sales targets multiple times in early 2026. Competitor Anthropic has been steadily eroding its market share in programming and enterprise markets, and OpenAI also missed its internal goal of reaching 1 billion weekly active users for ChatGPT by the end of last year. OpenAI's CFO, Sarah Friar, refuted these claims, stating that the company is achieving its goals and witnessing a "vertical climb" in product demand.

SoftBank's own financial leverage is also at historically high levels. The group recently committed an additional $30 billion to OpenAI, bringing its total investment to over $30 billion. A $40 billion loan completed in March set a record for its dollar-denominated loans, with part of the funds used to support the latest follow-on investment in OpenAI.

Capital market assessments of SoftBank have shown significant divergence. SoftBank's stock price has risen 39% year-to-date, vastly outperforming the 12.3% gain of Japan's benchmark Topix index. However, its credit default swap spread has widened by approximately 61 basis points this year. In March, S&P Global Ratings revised SoftBank's credit outlook from "stable" to "negative," citing that the investment in OpenAI could impair the company's liquidity and asset credit quality.

The pricing disagreement in the primary market for leading AI assets is manifesting in the most direct way possible: lenders are willing to lend 40% less than what SoftBank wanted to borrow.

$2.6 Trillion in Single-Day Options Volume, Goldman Partner Calls It "Semi-Irrational"

The secondary market presents a different picture. On Thursday, the notional trading volume of S&P 500 (SPX) call options exceeded $2.6 trillion, a new all-time record, with nearly 60% of all SPX options traded that day being calls. Rich Privorotsky, head of Goldman Sachs' One-Delta trading desk, described the current state of the U.S. market as a "chase mode where the spot is rallying and volatility is also rallying."

The weekly RSI of the Philadelphia Semiconductor Index (SOX) has reached its highest level since 1999. A Goldman Sachs partner stated bluntly, "It feels like we are in a semi-irrational chase mode." Privorotsky cited 1999 as a more fitting historical analogy, when a surge in orders for telecom equipment providers supported the rally with a narrative of "physical bottlenecks," which closely resembles the current logic centered on computing scarcity and AI infrastructure deployment.

QQQ implied volatility has risen sharply in tandem with the market rally, and its spread versus SPX volatility has widened to over 6 volatility points. Goldman Sachs' volatility trading desk described the day as "one of the most insane trading days in the past several weeks." Notably, the number of S&P 500 component stocks experiencing moves greater than three standard deviations on a single day reached 35, the highest level since February 3rd of this year.

A team at Bank of America's global equity derivatives research also noted that the latest record-breaking rally in the S&P 500 is reminiscent of the late 1920s and the internet bubble of the 1990s, but the market's pricing of "tail options" remains lower than what is implied by realized volatility. Simply put, the market is chasing gains but unwilling to pay for downside risk.

Goldman Sachs warned that the dynamic of "rising spot, rising volatility" is limiting the room for further additions by systematic strategies. Commodity Trading Advisors (CTAs) are already essentially fully long, and with rising upside realized volatility, the marginal incremental demand from volatility control strategies is also diminishing. In other words, systematic buying power from institutions is nearing its limit, and further upward momentum will rely more on retail and sentiment-driven capital.

XLF at Weakest Relative to S&P 500 Since 1998, Financial Stocks Sound Alarm

If the options market represents an extreme reading of sentiment, then the relative performance of the financial sector is a warning signal from technical analysis.

The U.S. financial sector has fallen approximately 6% year-to-date, while the S&P 500 index has risen 7% over the same period and closed at record highs on 14 out of the last 17 trading days.

Relevant data is analyzed in the article "Cracks Beneath the S&P's New Highs: Financial Sector Down 6% YTD, $2 Trillion Private Credit Undercurrent Spreading".

The financial sector is considered a leading indicator due to its core role as a liquidity provider in the economy. Concerns within the private credit market are considered a major reason for the pressure on the financial sector. Melissa Brown, Global Head of Investment Decision Research at SimCorp, pointed out that the financial system is highly interconnected and related risks "could spread more widely than currently anticipated." She suggested that investors might consider gradually reducing exposure to "chip stocks" rather than continuing to chase gains, and certainly not add new capital to the market.

Apollo Reserves $40 Billion Cash, Rowan Estimates 35% Probability of Exogenous Shock

Defensive measures at the institutional level have already begun. Marc Rowan, CEO of Apollo Global Management, stated during the company's quarterly earnings release that he estimates the probability of an exogenous shock occurring to be between 30% and 35%, significantly higher than normal levels.

Rowan attributes this risk to the convergence of three forces: a geopolitical reset, inflationary pressures driven by trade tariffs and immigration policies, and the profound reshaping of the economic structure by AI. He describes the current AI wave as "unquestionably the biggest tech cycle" in his career, specifically highlighting the vulnerability of government finances, noting that governments' balance sheets are under more stress compared to corporations and consumers.

Apollo has implemented a series of defensive measures: shifting its fixed-income portfolio towards higher credit quality, reducing exposure to high-risk sectors like software, and building approximately $40 billion in cash reserves within its insurance business. "This means we are investing with an eye on preserving capital, ensuring we can navigate the cycle, and if there's a correction, which frankly we expect there will be, we're ready," Rowan said.

Rowan reserved his sharpest criticism for industry competitors. He warned that not all insurance companies are running their businesses as they should, with some relying on what he termed "egregious" practices, including Cayman Islands offshore structures, complex mortgage arrangements, and aggressive credit assumptions, making their balance sheets appear stronger than they actually are. "We are definitely worried about contagion effects," he said.

It is noteworthy that Apollo reported strong quarterly results, with assets under management surpassing $1 trillion and fee-related earnings reaching record highs. Choosing to implement maximum defensive posture at the very peak of its own operating performance is, in itself, a telling judgment.

Consumer Sector's Tale of Two Halves Confirms Macro Divergence

Consumer data provides micro-level evidence for this macro judgment. Whirlpool (WHR) fell 16% in after-hours trading Thursday, with management describing the current environment as a "sharp deterioration in macroeconomic conditions" and announcing "decisive actions" such as price increases and accelerated cost-cutting to restore profitability. The chill in the housing and big-ticket consumer goods sectors stands in stark contrast to the red-hot semiconductor sector.

In comparison, DoorDash stated that the second quarter is "off to a good start" and demand remains "still quite robust," causing its stock to rise about 10%.

This divergence reflects the deep logic behind current consumer behavior: large expenditures (e.g., home renovations, appliances) feel like a recession, while small, immediate consumption (e.g., food delivery) remains largely unaffected. Consumers haven't disappeared, but have become highly selective. This strongly aligns with the corporate sector's narrative: investment in AI infrastructure is accelerating, while consumption of traditional durable goods is contracting.

When you plot these four sets of signals on the same chart—lenders unwilling to value OpenAI at $10 billion; the options market betting $2.6 trillion on a rally in a single day; the financial sector at its weakest relative level since 1998; Apollo hoarding $40 billion in cash—it doesn't necessarily constitute a judgment of an "imminent crash." Even Scott Brown himself emphasized that such warning signals can sometimes persist for a long time before being absorbed by the market, or may even ultimately prove false. However, when the primary market, secondary market, leading sectors, and top-tier institutions are simultaneously giving inconsistent readings, it at least suggests that the risk premium embedded in current price levels has been compressed to a level worthy of caution.