ทำนายตลาด 10 ความจริง: ใน 172,000 ที่อยู่ของ Polymarket มีเพียง 3.14% ที่เป็น "ผู้ชนะที่แท้จริง"

- ประเด็นหลัก: เรื่องเล่า "ภูมิปัญญาของฝูงชน" ของตลาดทำนาย (เช่น Polymarket) ถูกท้าทาย: มีเพียงประมาณ 3.14% ของบัญชี "ผู้ชนะที่มีทักษะ" เท่านั้นที่กำหนดประสิทธิผลของการค้นพบราคา ในขณะที่ผู้เข้าร่วมมากกว่า 67% อยู่ในสถานะขาดทุน ซึ่งโดยพื้นฐานแล้วเป็นการจ่ายเงินให้กับผู้ที่มีข้อมูลได้เปรียบส่วนน้อย

- องค์ประกอบสำคัญ:

- ชนกลุ่มน้อยขับเคลื่อนราคา: มีเพียง 3.14% ของบัญชี (ประมาณ 54,000 บัญชี) ที่ถูกระบุว่าเป็น "ผู้ชนะที่มีทักษะ" ซึ่งเป็นแรงผลักดันหลักในการค้นพบราคาและชี้นำผลลัพธ์สุดท้าย

- คนส่วนใหญ่ขาดทุน: ผู้เข้าร่วมมากกว่า 67% (ผู้แพ้ทั้งที่อาศัยโชคและมีทักษะ) รับภาระขาดทุนทั้งหมด พฤติกรรมการซื้อขายของพวกเขาไม่มีประโยชน์ต่อการค้นพบราคา ถือเป็น "ผู้ใจบุญ" ล้วนๆ

- ประสิทธิผลของทักษะสูง: ความมีประสิทธิผลในการระบุผู้เล่นที่มีทักษะในตลาดทำนาย (44%) สูงกว่าผู้จัดการกองทุนแบบดั้งเดิม (10%) มาก ซึ่งบ่งชี้ว่าตลาดนี้มีความแตกต่างอย่างชัดเจนระหว่างผู้เชี่ยวชาญกับ "นักลงทุนรายย่อย"

- ผลกระทบจากการซื้อขายโดยใช้ข้อมูลภายในมีจำกัด: บัญชีที่疑似ใช้ข้อมูลภายในประมาณ 1,950 บัญชี มีความแม่นยำในการทำนายเหตุการณ์บางอย่างสูงมาก แต่ไม่มีส่วนสำคัญต่อการค้นพบราคาโดยรวมของตลาด

- การกระจายธุรกรรมไม่เท่าเทียมอย่างยิ่ง: ปริมาณธุรกรรมเฉลี่ยของบัญชีที่活跃บน Polymarket อยู่ที่เพียง 72 ดอลลาร์สหรัฐฯ ในขณะที่บัญชี 1% แรกมีปริมาณธุรกรรมเฉลี่ยสูงถึง 74,000 ดอลลาร์สหรัฐฯ ความแตกต่างมากกว่า 1,000 เท่า

Source: Prediction Market Accuracy: Crowd Wisdom or Informed Minority?

Compiled by Odaily Planet Daily (@OdailyChina)

Translator: Wenser (@wenser2010)

Editor's Note: For a long time, prediction market platforms like Polymarket and Kalshi have positioned themselves as the "concentrated manifestation of crowd wisdom" to differentiate from betting platforms, using this narrative to boost their valuations. However, a recent paper from the London Business School and Yale University analyzed Polymarket's on-chain data and found that less than 4% of addresses drive price changes and generate substantial profits, while the remaining ~97% are mostly "participants along for the ride," with over 67% incurring losses. Considering that Polymarket now has over 2.43 million user addresses, the research data may have some lag, but the underlying phenomenon it reveals is still worth pondering.

Below are the key findings of this paper, summarized by Odaily Planet Daily.

Truth #1: Prediction Market Accuracy is Not About "Crowd Wisdom," But Determined by 3.14% of a Minority

This is the paper's most central conclusion and a direct challenge to the industry's narrative.

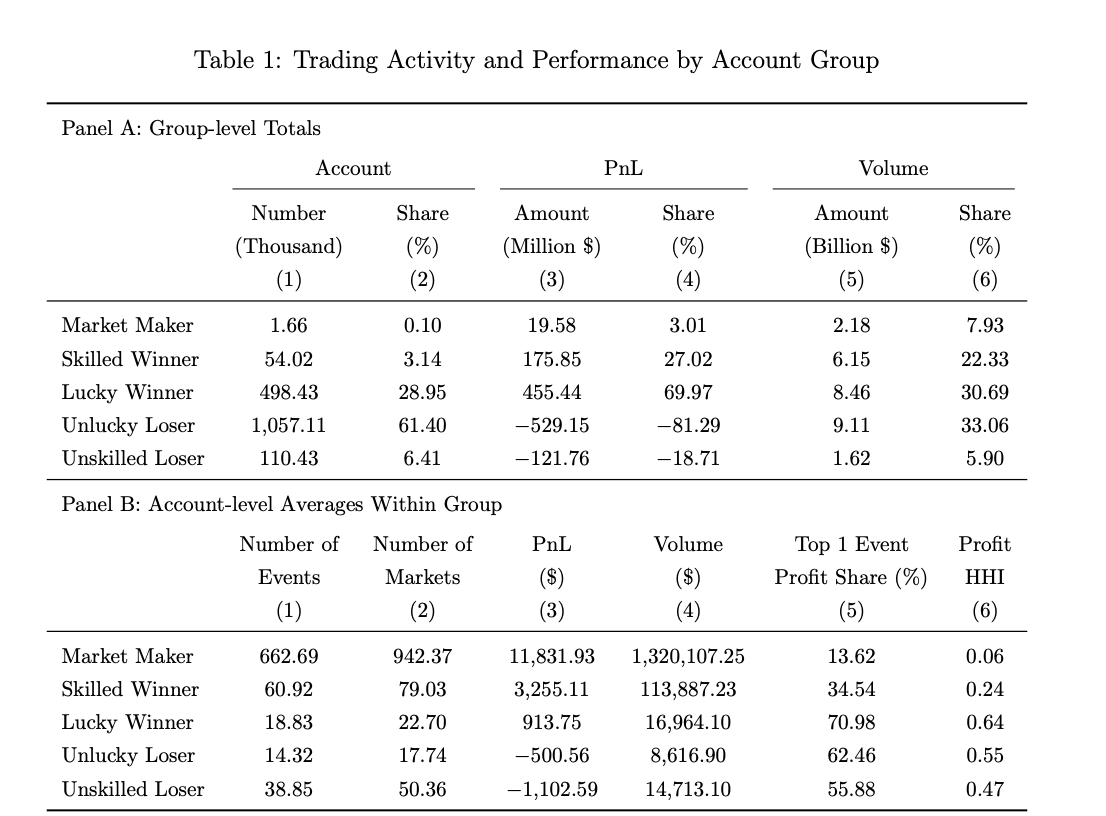

Previously, several prominent industry figures took pride in this: Kalshi CEO Tarek Mansour said prediction markets "leverage crowd wisdom," Polymarket CEO Shayne Coplan repeatedly claimed "financial stakes can aggregate information more effectively than experts," and Robinhood CEO Vlad Tenev called it "capitalism's quest for truth." But the research data tells a different story: out of 1.72 million Polymarket accounts, only about 54,000 accounts (3.14%) were identified as "skilled winners" (Odaily Planet Daily note: The paper describes these individuals as professional players who can both predict and absorb information on average and react efficiently to news).

The primary drivers of price discovery in prediction markets are this minority group, not the crowd hiding behind the concept of "crowd wisdom" most of the time.

Truth #2: Winning or Losing Can Be a Matter of Luck; 67% of Participants Are Essentially "Philanthropists"

In this paper, Roberto Gómez-Cram and others used a sign-randomization method to classify all trader accounts into four categories: Skilled Winners (3.14%), Lucky Winners (29.0%), Lucky Losers (61.4%), and Skilled Losers (6.4%).

The most counter-intuitive number is that Lucky Winners accounted for nearly 30%. They made money, but their trading contributed nothing to price discovery, statistically indistinguishable from flipping a coin randomly.

In other words, making money in prediction markets and being "skilled at predicting the future" are two different things. The ~67% of losers bear all the losses, essentially paying for the information advantage of a minority.

Truth #3: Among Top Profit Leaders, 88% Relied on Luck to Make Money

Among the top 54,000 traders on Polymarket ranked by actual profit, only 12% were also identified as "skilled winners" by the statistical method.

This means the vast majority of big winners on the leaderboard achieved their large profits through a lucky bet or two.

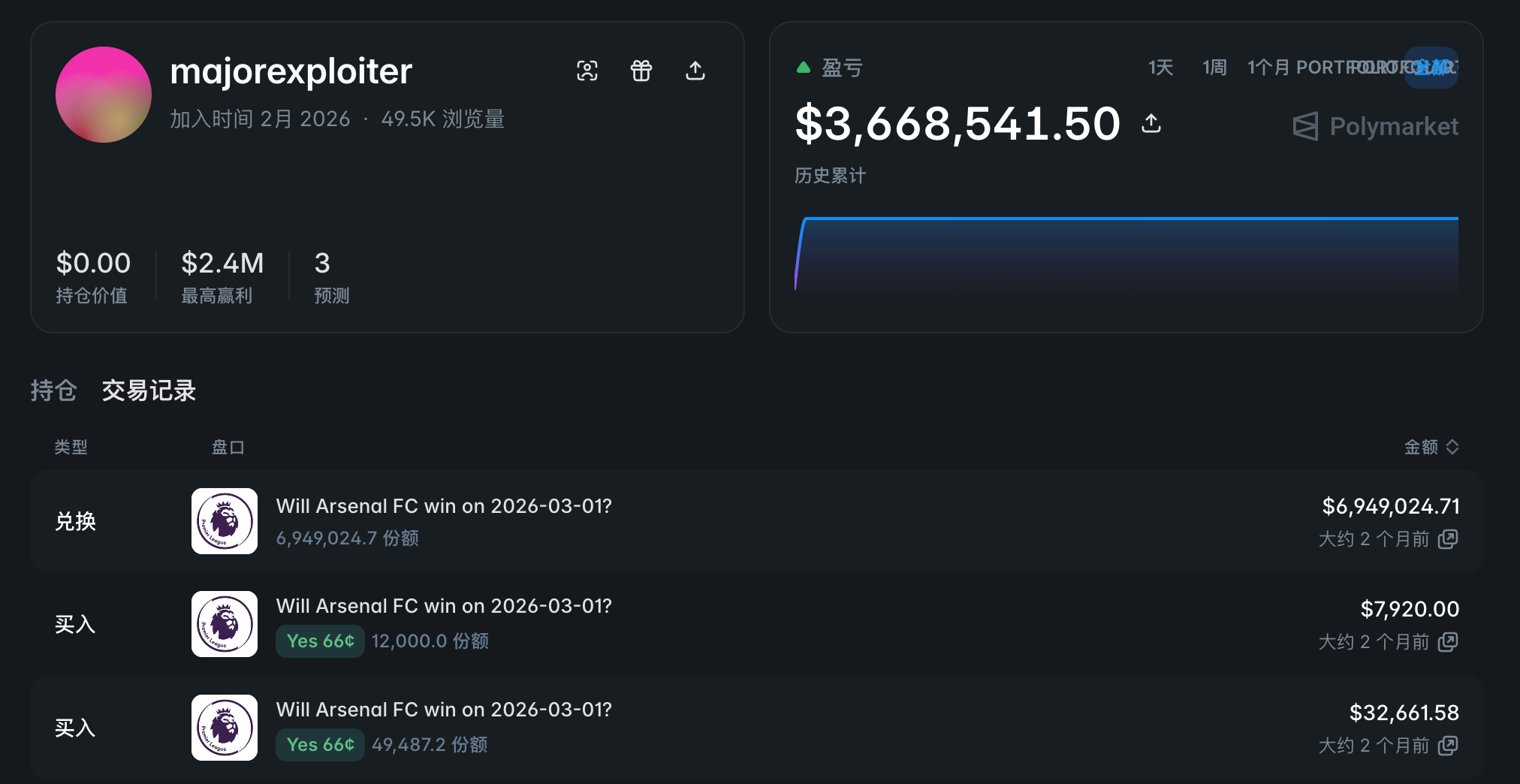

A typical case is the account @majorexploiter – over one weekend in early 2026, the account placed $4.5 million in bets on three sporting events, making a profit of over $3.6 million.

Returns from such concentrated bets are extremely unsustainable; 60% of "Lucky Winners" become losers in out-of-sample validation.

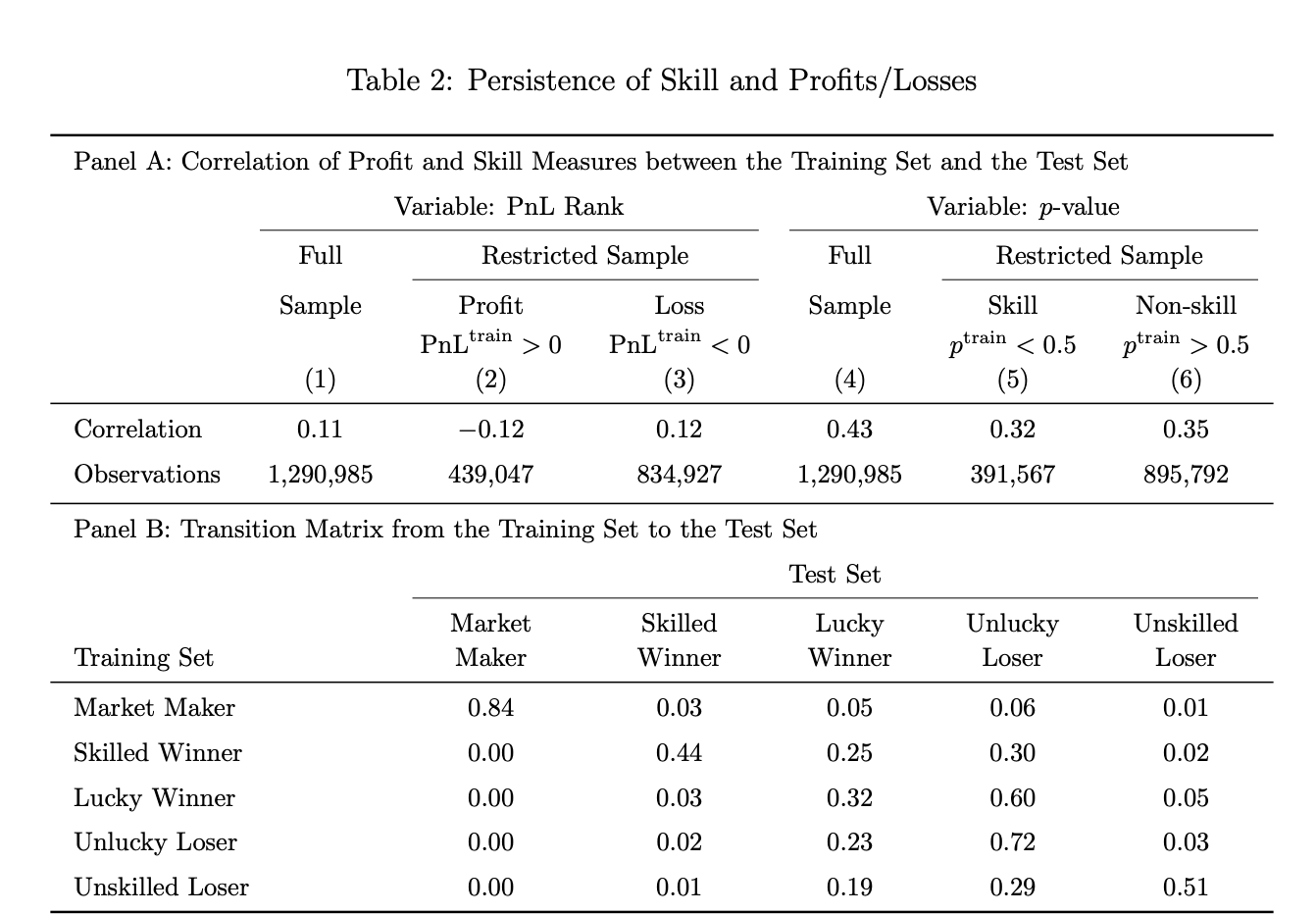

Truth #4: Skill Persistence in Prediction Markets Far Exceeds That in Traditional Fund Management

The researchers split betting events into training and test sets for out-of-sample validation.

Results showed that 44% of accounts identified as "skilled players" in the training set were also identified as "skilled users" in the test set. In comparison, when the same test was applied to actively managed U.S. mutual funds, skill persistence was only 10%.

Conversely, "anti-skill" (persistent losses) also showed high consistency: 51% of "Skilled Losers" in the training set remained losers in the test set, while this figure for U.S. mutual funds was 20%.

The final conclusion is that in prediction markets, the experts are truly experts, and the "diamond hands" are truly just along for the ride.

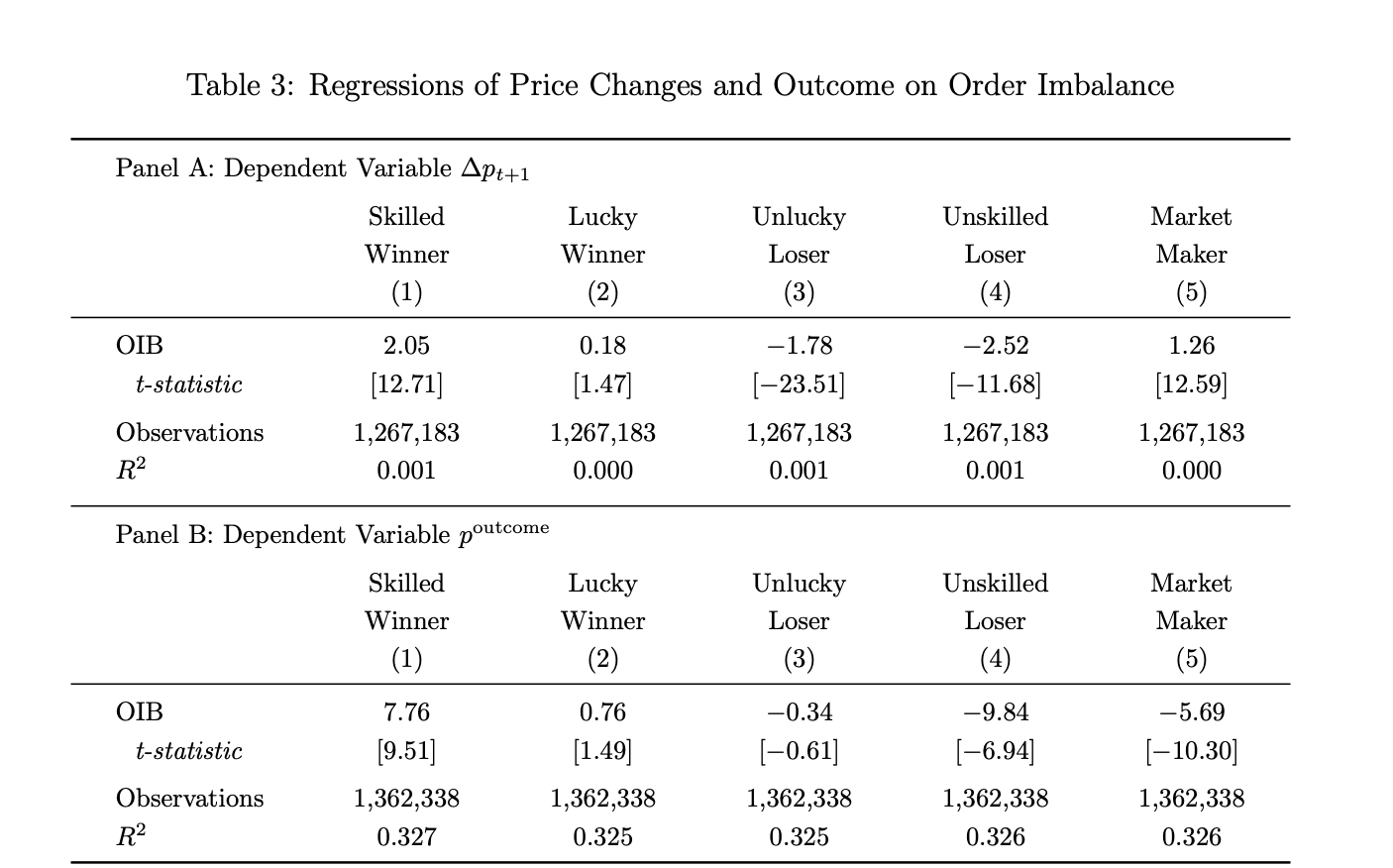

Truth #5: Skilled Winners' Orders Are Highly Correlated with Final Event Outcomes

Using a constructed order imbalance formula, researchers found that for every 1% increase in the net buying indicator (OIB) of Skilled Winners, the next period's price rises by about 2 basis points, and the probability of the final event occurring increases by about 8 basis points, with high statistical significance (t-values of 12.71 and 9.51, respectively).

In contrast, the order flow of Lucky Winners showed no significant effect on either indicator (t-values of only 1.47 and 1.49).

In other words, although Lucky Winners are profitable, their trading activity contains no informational value – from a data perspective, this conclusion is very robust.

The observed phenomenon from the research is: in markets that resolved to "Yes," Skilled Winners were net buyers; in markets that resolved to "No," they were net sellers. They consistently built positions in the direction of the final outcome. Market makers were mostly net sellers in "Yes" markets and net buyers in "No" markets, consistent with their role of accommodating directional order flow and profiting from bid-ask spreads rather than establishing insider positions.

Truth #6: Skilled Traders Are the Only Ones Making Prices More Accurate

Based on the premise that some trades actually drive prices toward the final outcome, the researchers constructed a "Price Discovery Contribution Indicator" to measure whether prices move closer to or further from the final outcome accuracy within each time window.

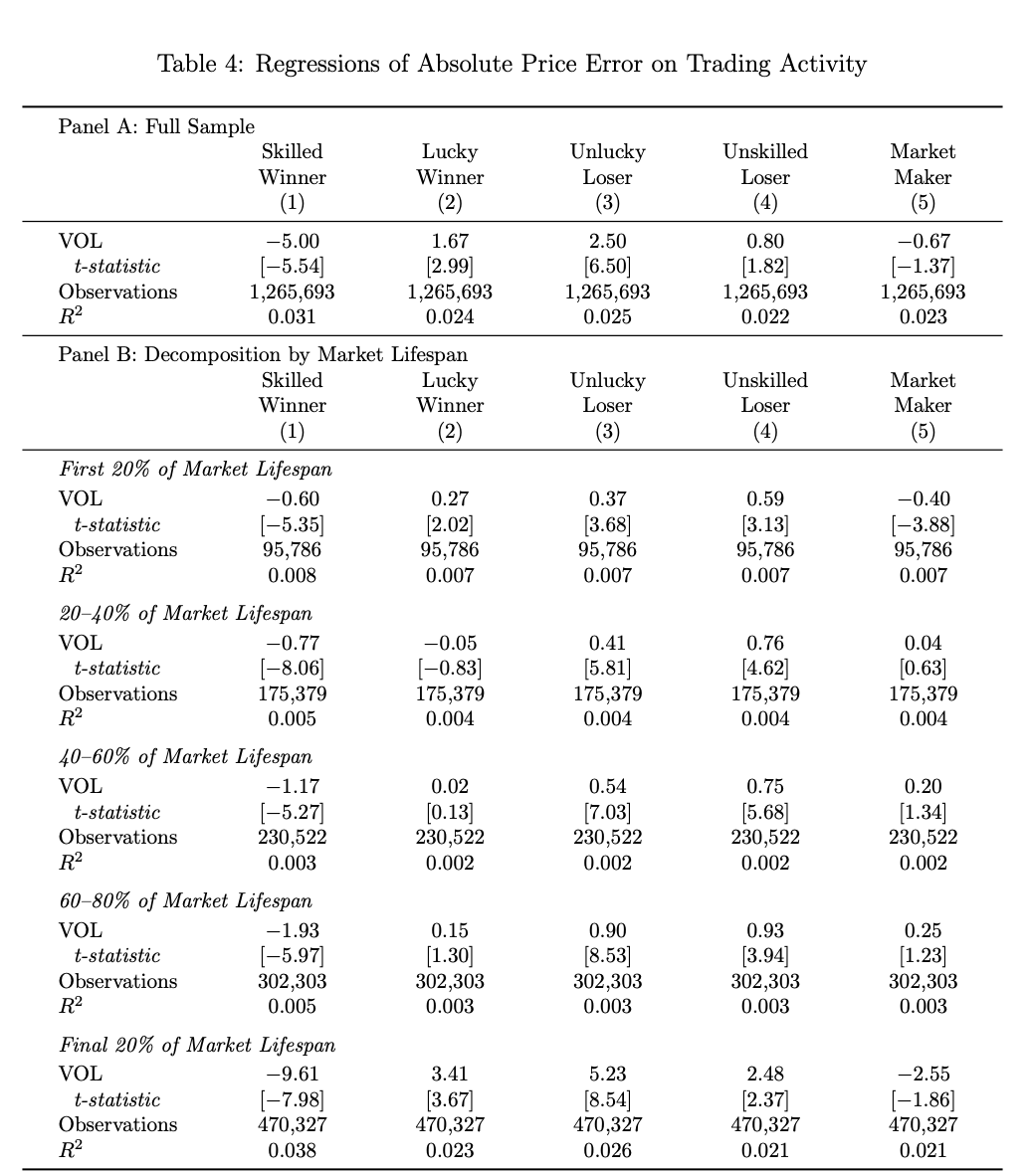

The results showed that only when the trading volume share of Skilled Winners increased did the pricing error for that betting event significantly decrease (coefficient -5.00, t-value -5.54).

Conversely, the trades of the other three groups – Lucky Winners, Lucky Losers, and Skilled Losers – actually moved prices away from the final outcome. In reality, most people are just creating noise at the trading level, and this effect grows larger as the market approaches settlement. During the last 20% of a betting event's lifecycle, the contribution coefficient for Skilled Winners expands to -9.61.

Truth #7: Skilled Winners Are the Only "News Trading" Players

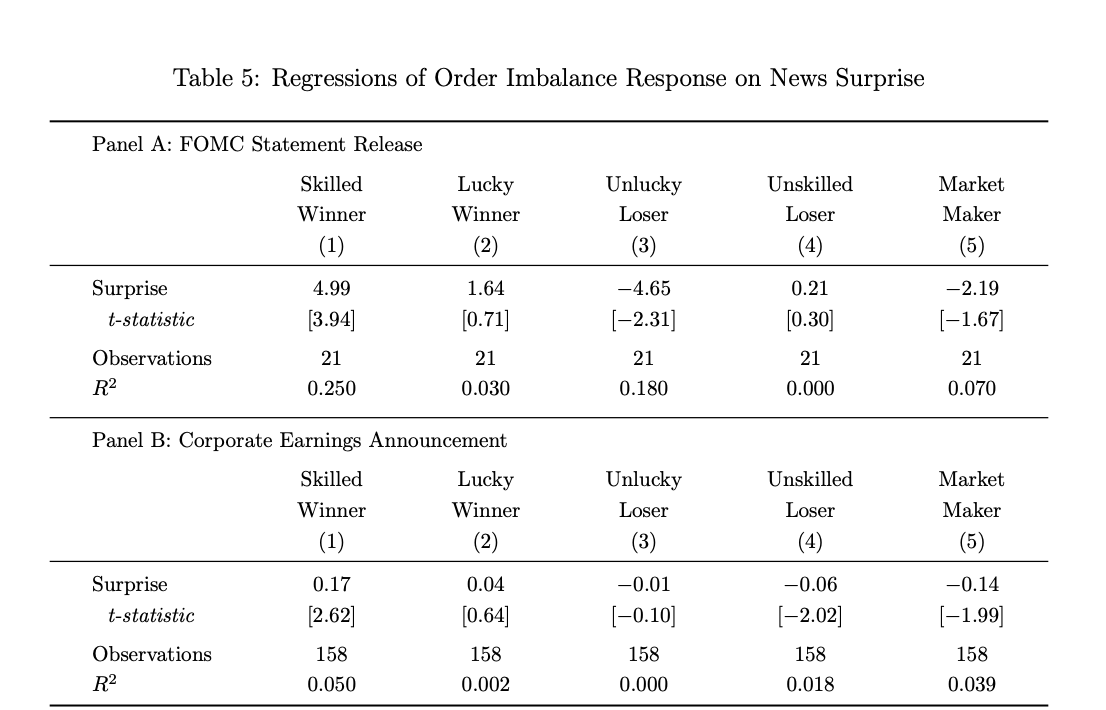

To minimize errors caused by news transmission time, the researchers selected two types of events with clearly defined information release times as study samples: FOMC interest rate decisions and corporate earnings announcements (Odaily Planet Daily note: The former is core for monetary policy expectations; the latter is core for understanding company fundamentals).

Research data shows that only the order flow of Skilled Winners significantly shifts in the "unexpected direction" within short windows after news announcements.

In FOMC betting events, a 1% increase in the unexpected direction corresponds to an approximate 5% increase in the net buying volume of Skilled Winners (t=3.94). Since the magnitude of FOMC surprises is relatively small (max ~6 percentage points), the contrarian buying is substantial. For earnings announcements, a 1% increase in the unexpected direction corresponds to an approximate 17 basis point increase in the net buying volume of Skilled Winners (t=2.62). In contrast, all other groups showed no consistent reaction to the news, with some even trading in the opposite direction.

Truth #8: Market Maker Profits Come from Liquidity Spreads, Not Information Asymmetry

Research data shows that market makers on Polymarket represent only 0.1% of total accounts (approx. 1,660), but they participate in an average of 942 betting markets, with each account averaging a profit of $11,832.

Furthermore, their order flow can predict short-term price movements (because they are constantly "taking the other side"), but its predictive impact on final event outcomes is negative (Chart 3 data: coefficient -5.69, t=-10.30).

This means they absorb the sell orders of informed traders in the short term but get "harvested" by them in the long term, making money primarily from bid-ask spreads rather than directional bets.

Truth #9: Insider Trading Only Affects the Outcomes of a Few Events

Acknowledging the inevitability of insider trading in prediction markets, the study also analyzed the impact of insider trading on price discovery. (Odaily Planet Daily note: The study used two criteria to flag suspicious trades. First, timing: accounts opened shortly before a specific event, like 7 days, and ceased trading after the event's resolution. Second, conviction: accounts concentrated in a single event contract holding an unusually large position, with a minimum trade volume of $1,000 and profit of at least $1,000. Accounts meeting both criteria were classified as potential insider traders.)

Using the dimensions of "account timing characteristics + position concentration," the paper identified approximately 1,950 suspected insider trading accounts, with an average profit of $15,000 per address.

Notably, the orders from these accounts showed extremely high predictive accuracy for the prices and outcomes of a subset of events (final outcome prediction coefficient 94.63, 12 times that of Skilled Winners), but their activity was concentrated in a few events, making their overall contribution to price discovery in the prediction market insignificant.

It is worth mentioning that the study detailed the prediction market case of the "U.S. military raid on Maduro": three accounts placed bets several days before the operation, concentrating purchases on an event with only a 10% probability, eventually netting over $630,000 in combined profit – one of the account holders was later charged by the CFTC as an active-duty U.S. soldier. For details, see ![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()