Bitcoin mean reversion, but $80K resistance and profit-taking could be bottlenecks

- Core View: Bitcoin has broken through the $78.1K real market mean, but faces strong resistance at the $80.1K short-term holder cost basis. A surge in profit-taking and low volatility signal the need for caution; upward momentum will depend on sustained spot demand and ETF inflows.

- Key Elements:

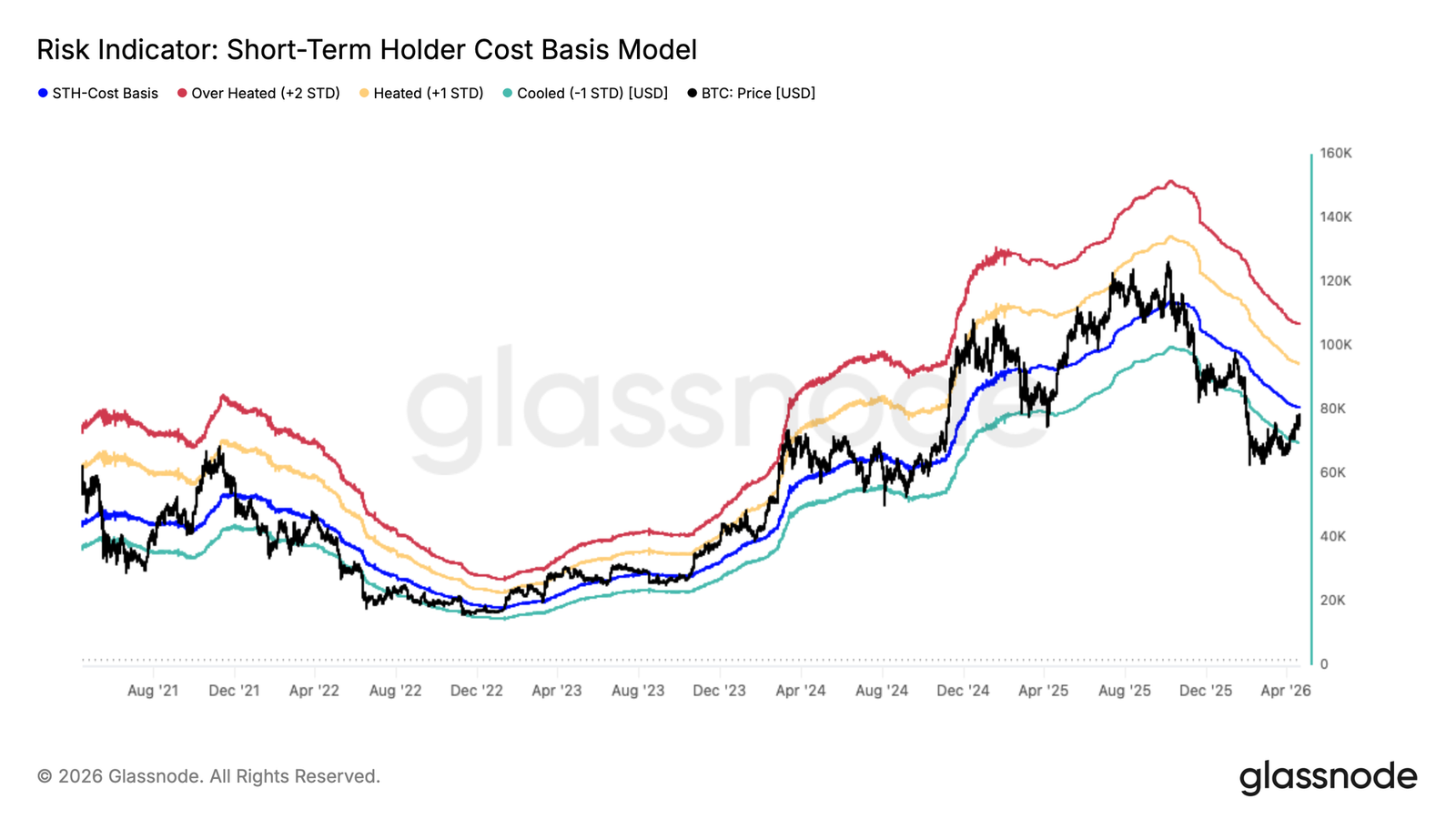

- Bitcoin has surpassed the $78.1K real market mean, a key signal of a shift from a bear market to a constructive market. However, the next critical resistance level is the $80.1K short-term holder cost basis.

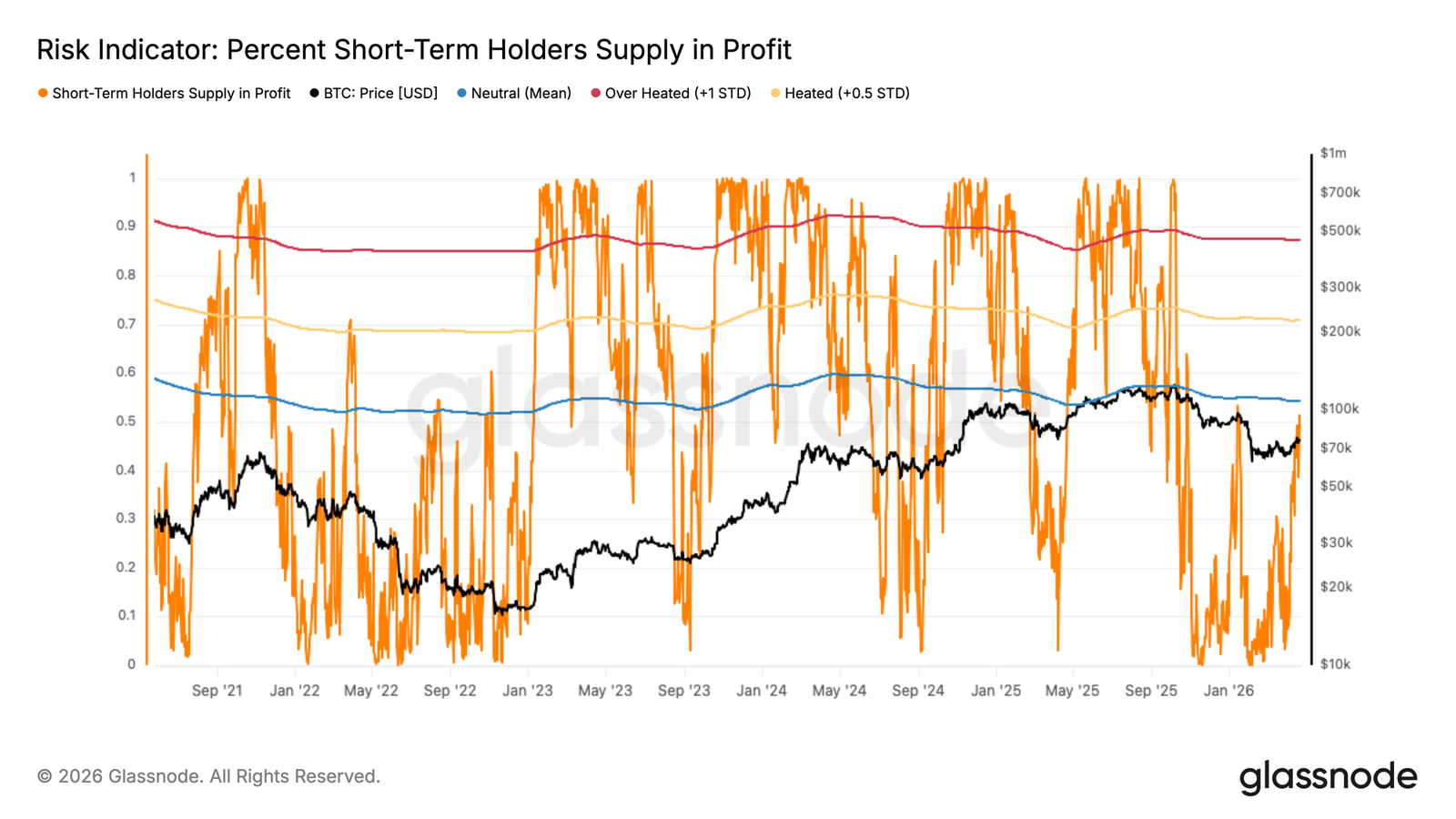

- The proportion of profitable supply among short-term holders has reached the historical threshold of 54%, which typically coincides with the exhaustion of selling pressure in bear market rallies. The current market structure marks only the second occurrence of this pattern in the current cycle.

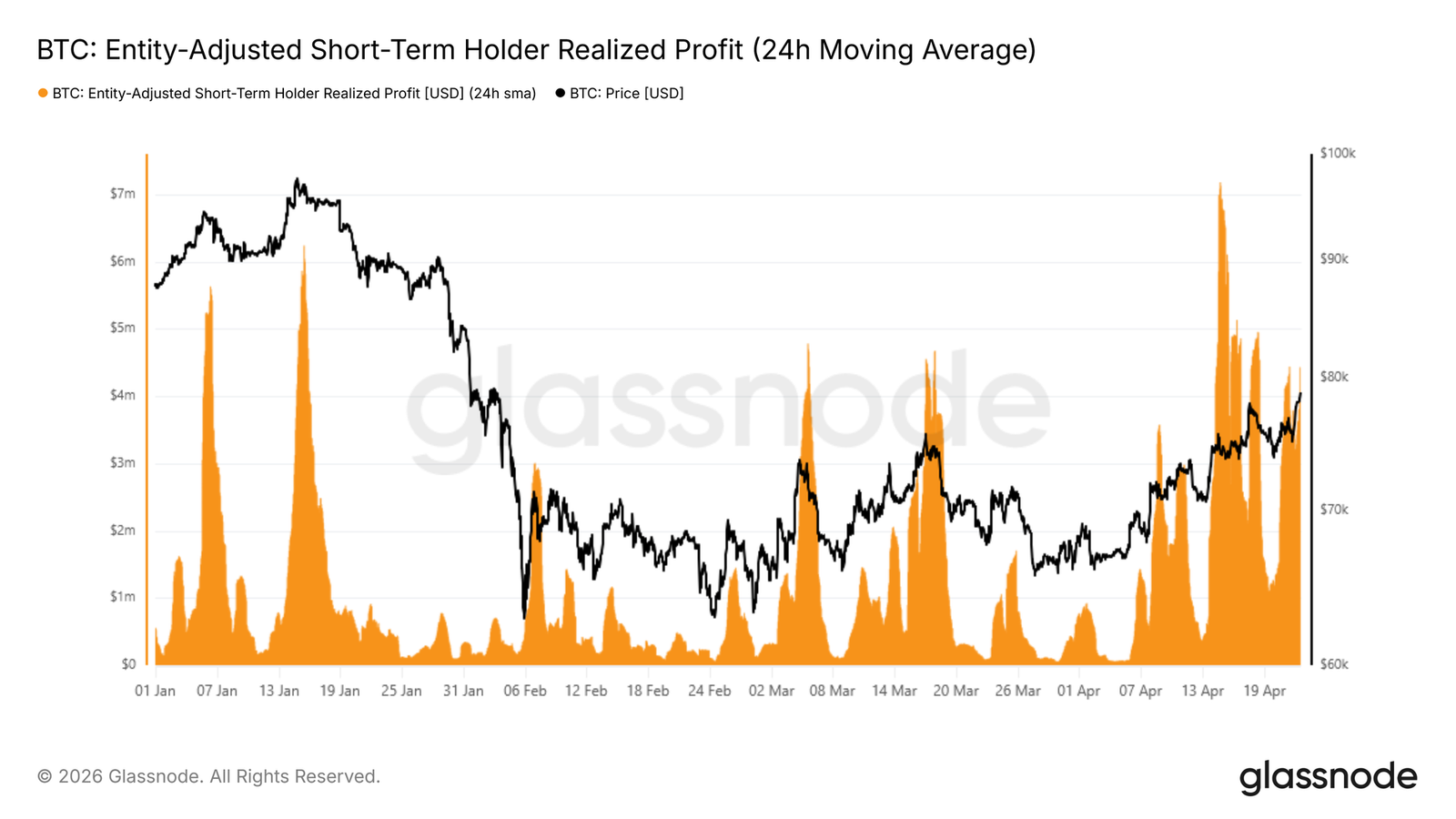

- Realized profits by short-term holders have surged to $4.4 million per hour, nearly three times the local top threshold of $1.5 million seen earlier this year, signaling immense profit-taking pressure.

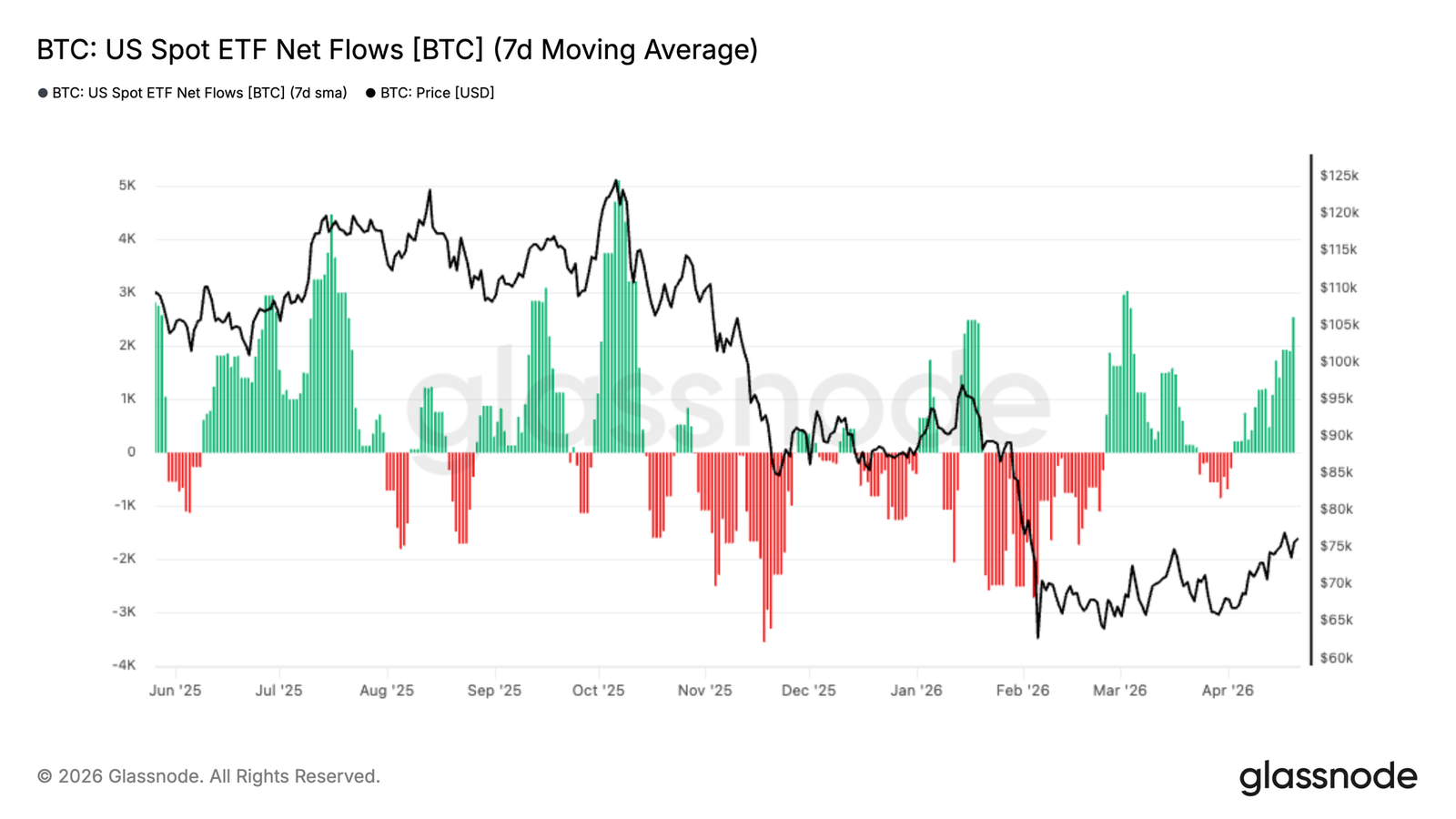

- The 7-day moving average of US spot ETF flows has turned positive again, indicating the initial return of institutional demand after a prolonged period of outflows, though inflow levels remain below the peaks seen in late 2025.

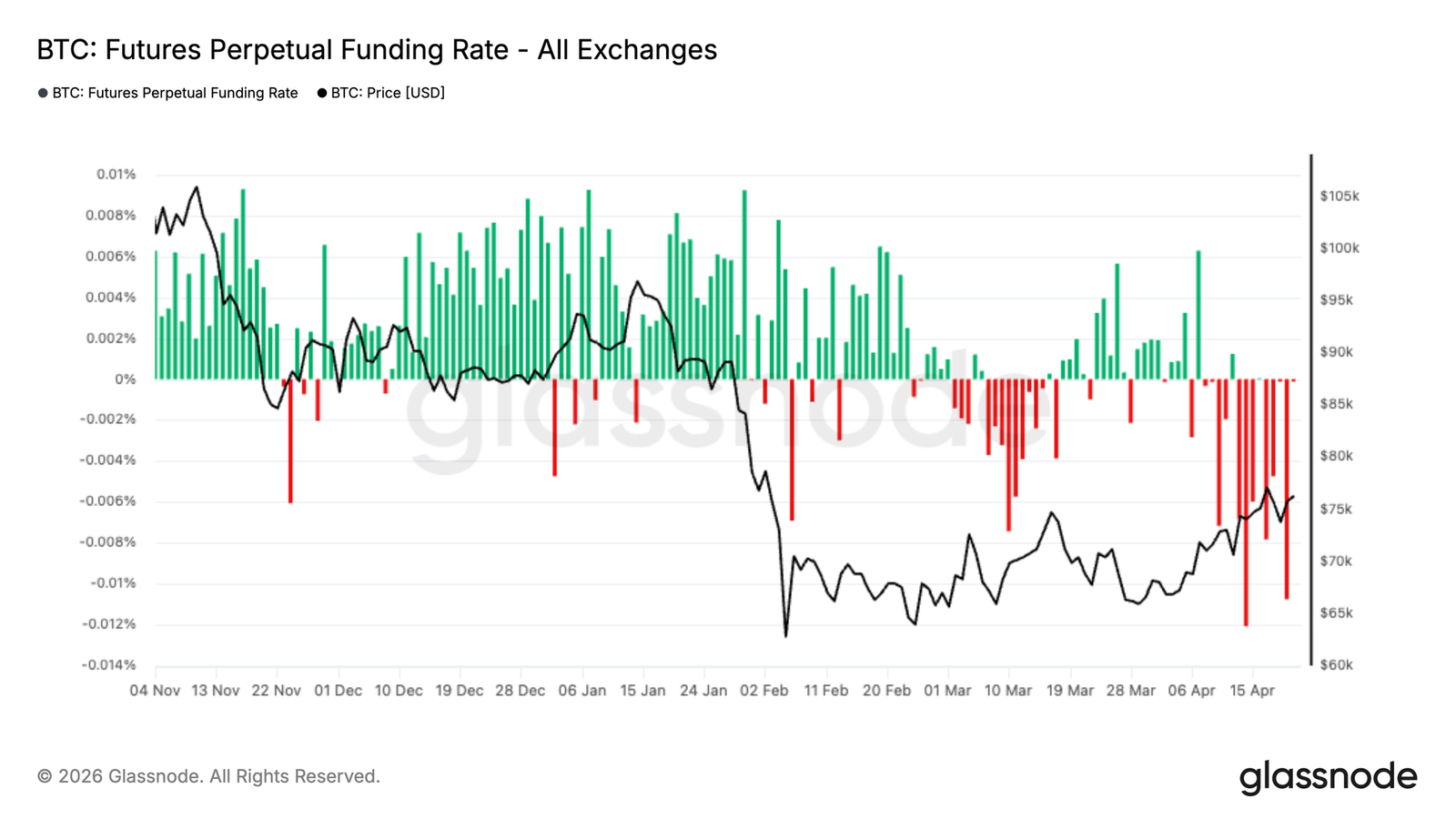

- Perpetual contract funding rates remain negative, pointing to overcrowded short positions in the market. If spot demand strengthens, this could serve as fuel for upward price action.

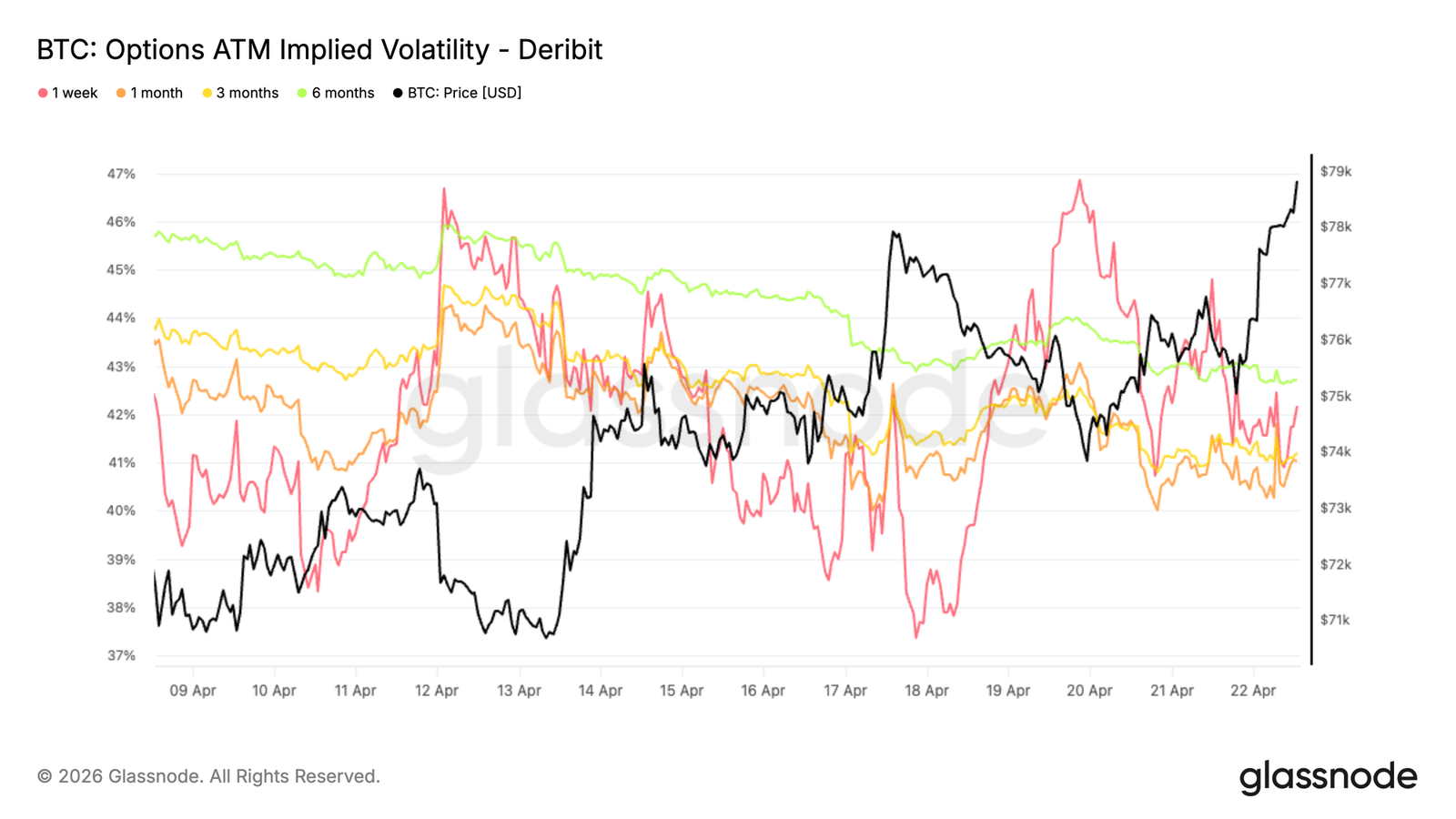

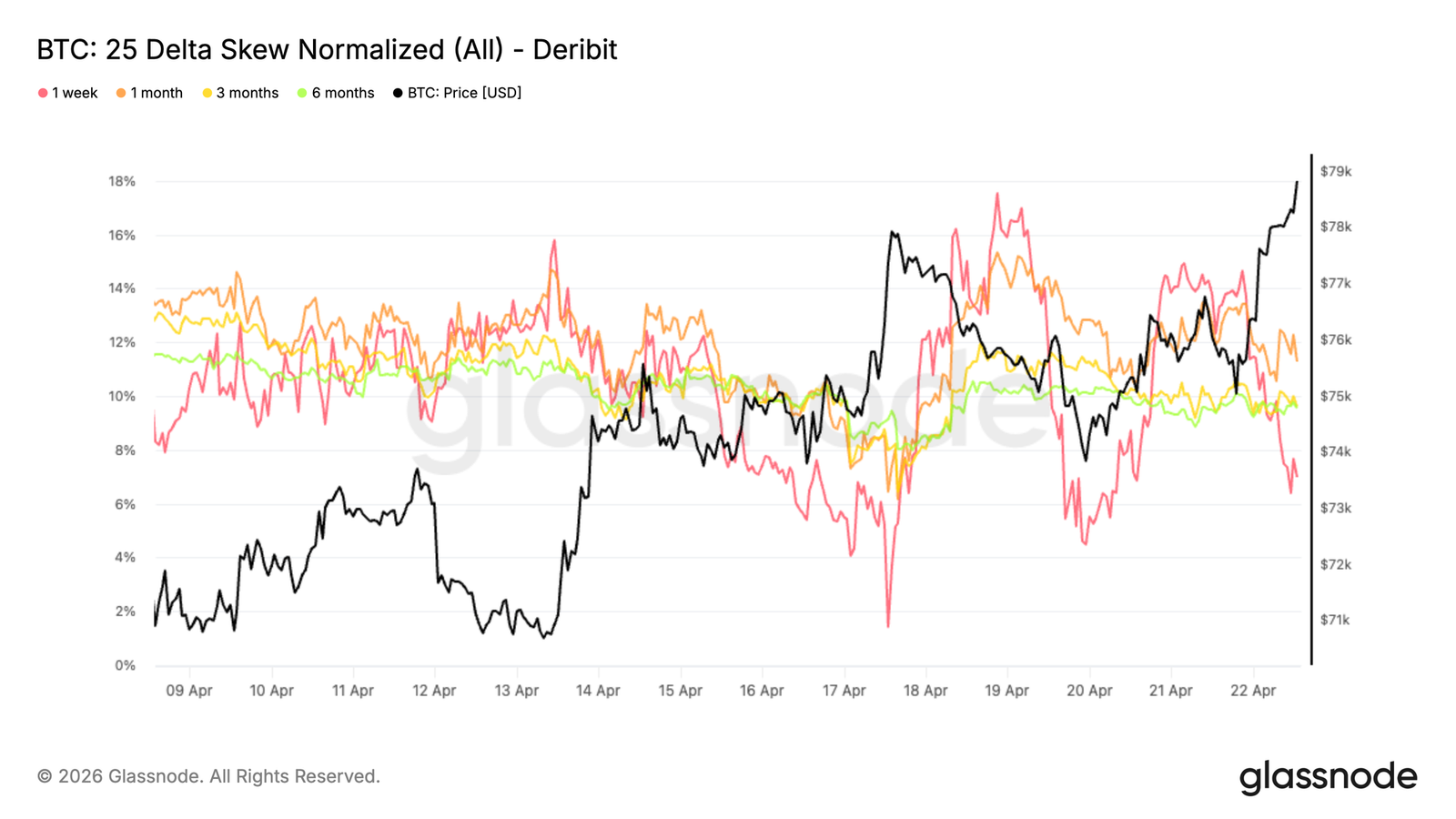

- The volatility market is soft, with implied and realized volatility continuing to decline and no premium in option pricing. Skew suggests short-term adjustments, but longer-dated maturities still show buying of downside protection.

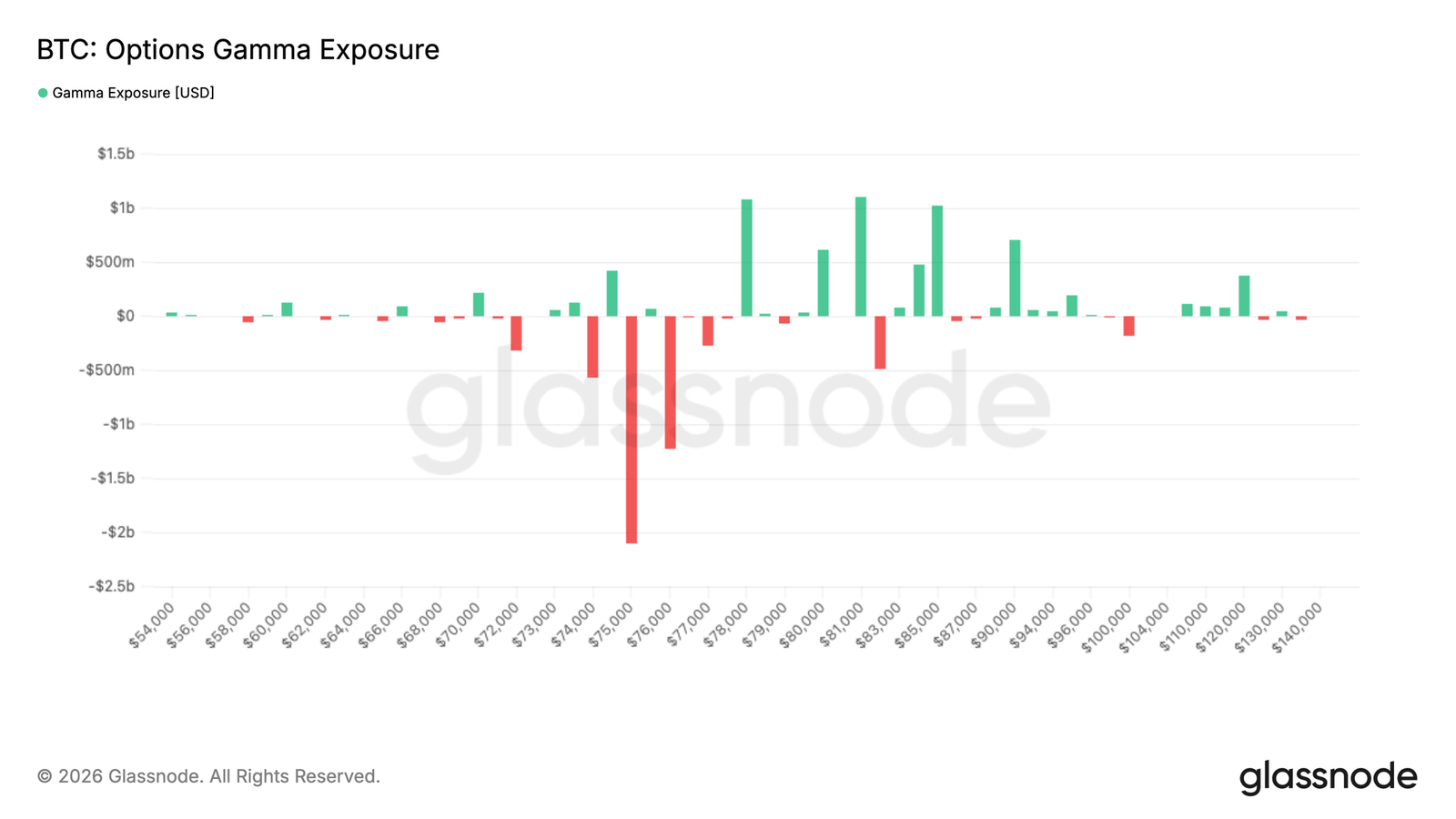

- Gamma data indicates mechanical resistance near the $80K level, while a pullback to the $75K zone faces the risk of accelerated downside due to market maker hedging.

Original Author: Glassnode

Original Translation: AididiaoJP, Foresight News

Bitcoin returns to $78,000, accompanied by a resurgence in spot demand and ETF inflows. Short positions are increasing, and funding rates are negative, creating potential for a short squeeze. However, high realized profits and weakening volatility suggest caution, with resistance above $80,000.

Summary

Bitcoin has broken through the True Market Mean of $78,100, its first significant mean reversion since mid-January. The Short-Term Holder Cost Basis is currently at $80,100, acting as the immediate resistance ceiling.

A rally to $80,000 would push over 54% of recent buyers into profit. Historically, this threshold often marks the point of exhaustion for selling pressure during bear market rallies. This is already the second time such a structure has emerged in this cycle.

Realized profits for short-term holders have surged to $4.4 million per hour, nearly three times the ~$1.5 million per hour threshold that has marked every local top this year to date. Caution is warranted in the absence of a meaningful demand catalyst.

ETF flows have turned moderately positive again, with the 7-day moving average returning to inflow territory, signaling an initial return of institutional demand after an extended period of outflows.

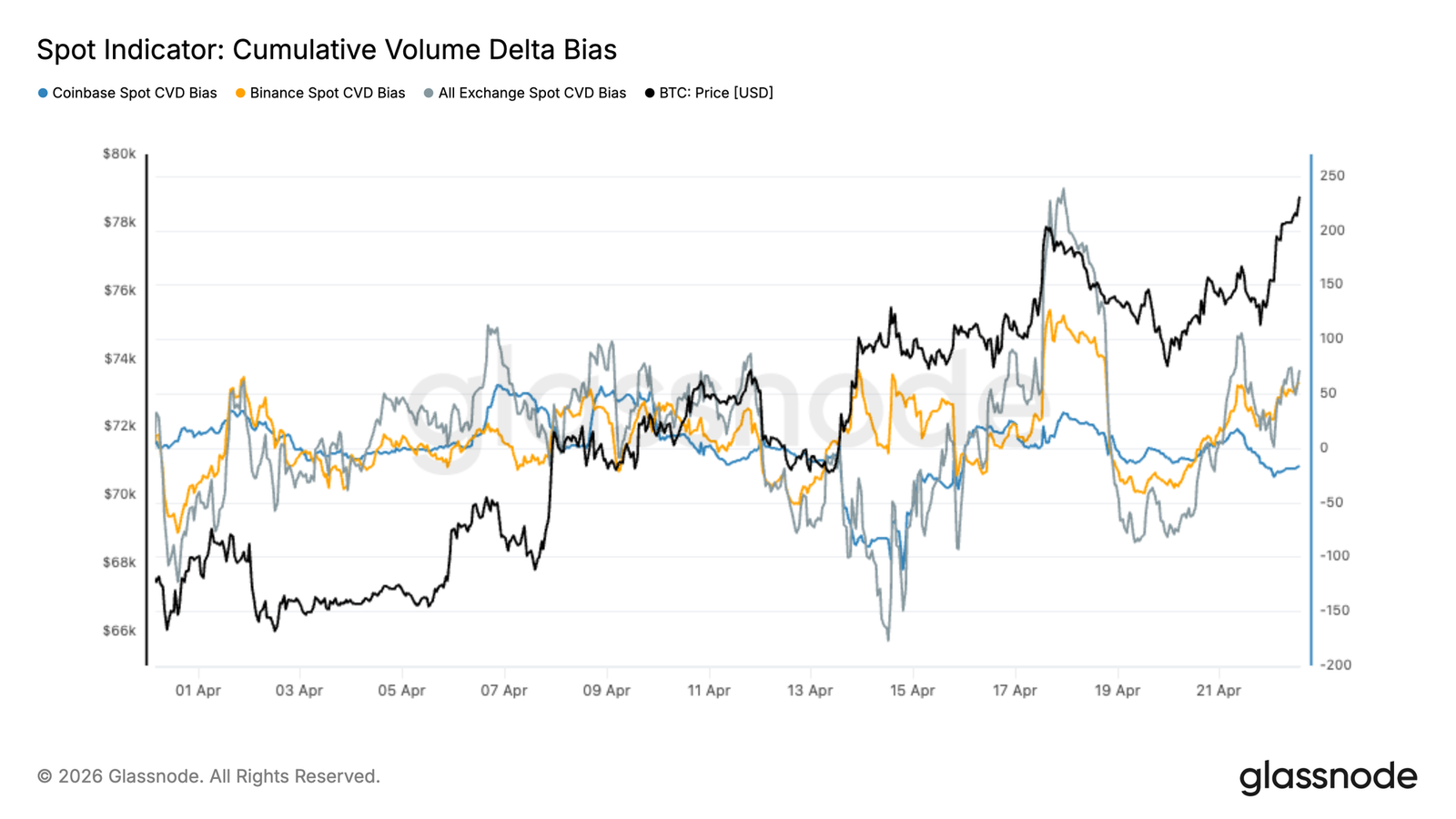

Spot demand shows early signs of recovery, with the Cumulative Volume Delta (CVD) turning positive, indicating increasing buyer aggression, particularly on offshore exchanges.

Perpetual swap funding rates remain negative, reflecting a growing market bias towards short positions, which could serve as fuel for an upside move if spot demand continues to strengthen.

Volatility remains under pressure. Implied volatility continues to decline, realized volatility confirms the compression, and there is no premium priced into options.

Skew indicates short-term position adjustments, but downside protection further out the curve is still being firmly bought.

Gamma and flow dynamics outline the current landscape: mechanical resistance near $80,000 on the upside, while a pullback to $75,000 faces a higher risk of downside acceleration.

On-Chain Insights

Breaking the Ceiling, But Not Yet Clear

Last week, this report identified the True Market Mean of $78,100 as a key short-term resistance zone, anticipating selling pressure from underwater investors would cap any rally. Bitcoin has since broken through this level, a development with significant cyclical implications.

The True Market Mean tracks the cost basis of the actively traded supply. Historically, reclaiming this model often signals a transition from deep bear market conditions towards a more constructive market environment. This breakout represents a significant mean reversion within the current bear market, and the next logical target is the Short-Term Holder Cost Basis of $80,500.

However, selling pressure from investors who accumulated in the $60,000-$70,000 range is beginning to impact momentum. This group is approaching their breakeven point, creating a behavioral incentive to exit. This dynamic increases the probability of forming a local top in the short term, warranting caution despite the constructive nature of breaking the True Market Mean.

The Next Wall: Short-Term Holder Cost Basis

Having broken the True Market Mean, the market now faces a more formidable test. The Short-Term Holder Cost Basis of $80,100 represents the average purchase price of investors who bought in the last 155 days. This cohort has historically proven to be the most price-sensitive group in the market.

As the price approaches their breakeven point, the behavioral incentive to exit strengthens, making this zone a natural source of selling pressure. In bear markets, rallies towards the Short-Term Holder Cost Basis often require multiple attempts to resolve, with prices retracing towards the -1 standard deviation level (approximately $69,900) between each attempt. This pattern suggests the $78,000-$80,100 range constitutes significant short-term resistance, while $70,000 is increasingly acting as a developing medium-term support floor.

Where Bear Market Rallies Exhaust

With the Short-Term Holder Cost Basis at $80,100 acting as the immediate resistance ceiling, the Percent of Short-Term Holder Supply in Profit provides a complementary perspective, precisely explaining why this level holds such significant behavioral importance. This metric measures the proportion of recently purchased supply currently in unrealized profit. Historically, readings above 54% have frequently coincided with peak selling pressure during bear market rallies, as the concentration of profitable short-term holders becomes sufficient to overwhelm demand.

A rally towards the $80,000 zone would push this metric above its statistical mean of 54%, triggering a wave of profit-taking by recent buyers looking to exit near breakeven. Notably, this is not an isolated event in this cycle; it is the second time this structure has appeared, with similar setups observed in previous bear markets. Multiple touches of this threshold reinforce its reliability as a local top indicator.

Surge in Profit-Taking Confirms the Warning

Further reinforcing the signals of potential exhaustion, the real-time spending behavior of short-term holders is validating the structural picture. As the price tests the Short-Term Holder Cost Basis for the second time, pushing over 50% of recent buyers back into profit, the 24-hour simple moving average of realized profit volume for short-term holders has surged above $4.4 million per hour.

Placing this reading in the context of the year is particularly telling: every single surge above $1.5 million per hour so far this year has coincided with the formation of a local top, making the current reading nearly three times the historical warning threshold.

In the absence of a meaningful demand catalyst to absorb this wave of profit-taking and sustain momentum above $80,000, a retreat from current levels would perfectly align with the patterns outlined in this report. The combined signals point towards caution rather than conviction.

Off-Chain Insights

ETF Flows Turn Positive Again

Flows into US spot ETFs have begun to recover, with the 7-day moving average returning to positive territory after an extended period of sustained outflows. This marks a significant shift in institutional demand, following substantial outflows seen in late January and February.

The recent cluster of inflows suggests a reallocation by traditional investors, coinciding with Bitcoin's rally from lows around $65,000 to the mid-$70,000 range. While the magnitude of inflows remains below the peaks seen in late 2025, the directional change is significant, indicating a return of institutional appetite.

From a structural perspective, ETFs remain a key marginal buyer for the market. Sustained positive flows would provide a robust demand base, helping to absorb selling pressure and reinforce price strength. However, consistency will be key, as past rallies have struggled to be sustained when ETF demand faded.

Spot Demand Returns

The spot CVD bias has clearly shifted towards the buy side in recent trading sessions, with a notable uptick in cumulative volume delta across major exchanges. This indicates that the recent price strength is supported by genuine spot demand, rather than being purely derivatives-driven flow.

Exchange-level dynamics reveal some divergence beneath the surface. Binance's spot CVD has dominated recent buying pressure, while activity on Coinbase has been relatively subdued, pointing towards stronger participation from offshore or retail-driven flows. Nevertheless, the aggregate CVD trend across all exchanges has turned positive, reinforcing the view that buyers are stepping in with conviction.

Importantly, this recovery in spot demand coincides with the price moving higher, suggesting a more constructive market structure compared to previous rallies that lacked underlying volume support. If sustained, this shift in spot positioning could provide a more durable foundation for further upside, especially against the backdrop of a growing short bias in the derivatives market.

Short Positions Building, Funding Rates Stay Negative

Perpetual swap funding rates have shifted decisively lower in recent weeks, with major exchanges consistently printing negative values. This marks a clear departure from the positive regime that dominated November and December, when long positioning was dominant and traders were willing to pay a premium to maintain exposure.

The current structure reflects a market increasingly biased towards short positions, with participants adopting defensive positioning following the sharp sell-off in early February. Notably, funding rates have remained negative throughout March and April, suggesting this is not a fleeting shift in sentiment but a more entrenched bias towards bearish hedging and speculative short exposure.

From a positioning perspective, this creates a constructive backdrop. Crowded short positions can act as fuel for an upside move, particularly if spot demand re-emerges or macro conditions stabilize. However, in the absence of strong directional flow, this imbalance could simply reflect a market that remains cautious.

Implied Volatility Continues Downward

Starting with implied volatility, the dominant trend across the curve remains downward. The 1-month, 3-month, and 6-month tenors have been steadily decreasing over the past two weeks, reflecting a steady compression in volatility expectations.

The 1-week tenor has seen more dramatic swings, with sharp spikes towards 46% on a couple of occasions. However, these moves have not been sustained, quickly reverting back into the broader downtrend. This suggests a lack of willingness in the market to maintain long protection. Instead, volatility continues to be sold at every tenor.

The failure of implied volatility to expand, even as the price moves higher, points to a lack of urgency for hedging and limited upside chasing. The overall structure remains soft, with no clear sign of a broader volatility regime change, only persistent selling pressure from dealers.

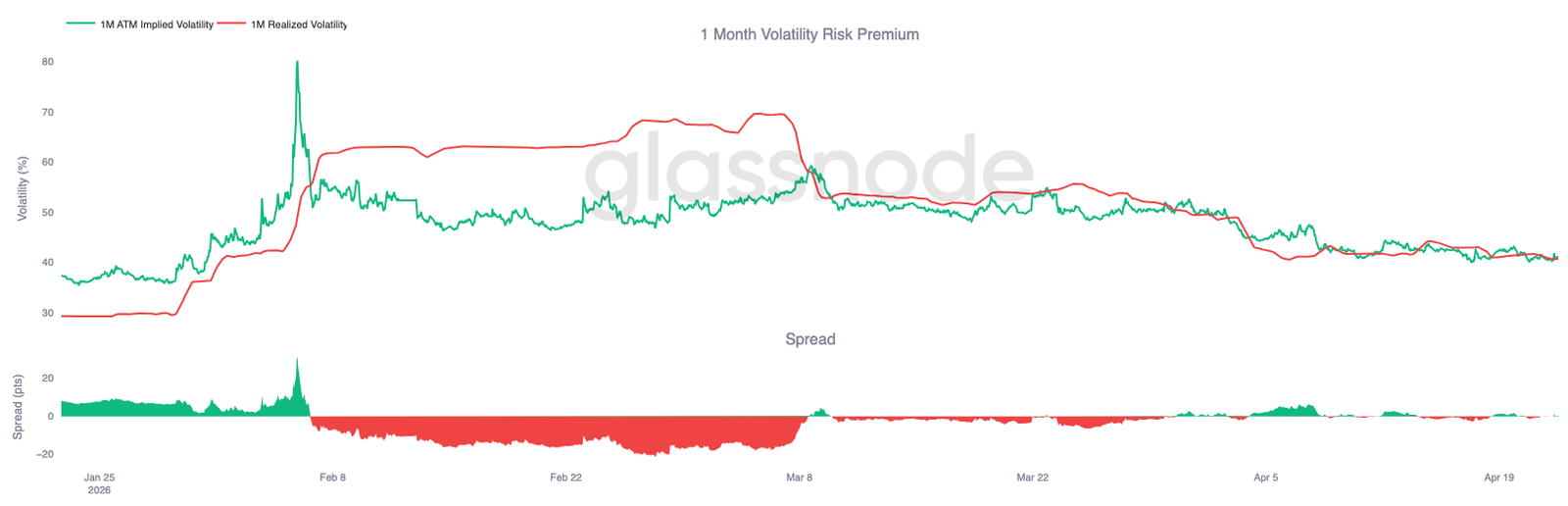

Realized Volatility Confirms the Compression

As implied volatility continues to be sold, realized volatility has moved in the same direction, reinforcing the trend.

Bitcoin's 30-day realized volatility currently stands at 40.7%, down from 49% in early April, with price action remaining contained and follow-through limited. This is important because realized volatility anchors how options should be priced. When realized volatility remains low, it becomes difficult for implied volatility to sustain any upside, as there is no underlying pressure to justify higher premiums.

This is clearly reflected in the volatility risk premium, which is currently near zero. This means implied volatility is no longer pricing in any meaningful premium over realized volatility. Options are being priced for what has happened, not for what could happen.

The combination of low realized volatility and persistent volatility selling keeps the overall environment soft, with no pressure forcing a re-pricing of volatility higher.

Short-Term Skew Volatile, Broader Structure Holds

Skew adds more nuance to the picture. The 25-delta skew (put option implied volatility minus call option implied volatility) saw sharp swings on the short end Friday, with 1-week put premiums briefly collapsing to 2% before bouncing back above 7% over the weekend.

This rapid round-trip highlights the reactive nature of short-term positioning. In contrast, the 1-month, 3-month, and 6-month tenors have remained relatively stable over the past two weeks, hovering around 10%-12% and continuing to reflect steady buying of downside protection. This divergence suggests the volatility was driven by short-term positioning rather than a broader shift in sentiment.

The temporary decline points to a brief unwinding of short-term hedges, but the rapid rebound shows that the demand for protection has not disappeared. The market is making tactical adjustments on the front end while maintaining a cautious stance further out the curve.

Gamma Positioning Outlines Short-Term Resistance and Downside Risk

The positioning picture becomes much clearer when looking at Dealer Gamma. There is a significant concentration of negative Gamma below the current price, particularly in the $75,000 area, where exposure reaches its most extreme levels.

Bitcoin is currently trading near $79,000, placing the price above this zone but just below positive Gamma territory on the immediate upside. In this range, hedging flows tend to dampen upward moves, creating mechanical resistance as dealers sell into strength. However, the risk lies to the downside. If the price retreats into the mid-$75,000 range, it would enter the negative Gamma zone, where dealer hedging could accelerate the downward price action.

Recent flow adds an important nuance. Over the past 7 days, call buying dominated activity, pointing to market positioning for an upside move. However, in the last 24 hours, as spot approached $80,000, flows shifted towards call selling, suggesting the upside is being monetized rather than chased.

Conclusion

Bitcoin's return to the True Market Mean marks a significant shift in market structure, reclaiming a key cost basis level that often defines the boundary between bear markets and more constructive phases. This recovery is currently supported by improving spot demand and an initial return of ETF inflows, suggesting that both retail and institutional participation are beginning to re-engage.

At the same time, derivatives positioning paints a more cautious picture. Persistent negative funding rates highlight a growing short bias, which could serve as fuel for an upside move if demand continues to strengthen. However, high realized profits and the lack of volatility premium suggest conviction remains fragile, with traders still hesitant to actively position for continuation.

Overall, the market appears to be transitioning into a more constructive phase, but confirmation is still needed. A sustained break above the $80,000 level will likely depend on continued spot absorption and stable ETF demand, while a failure to hold current levels could lead to accelerated downside due to the relatively thin liquidity environment.