Reputation DAO:建立链上信用体系,探索DeFi广泛用例

在金融、消费、教育、社交等领域中,信用都扮演着重要的角色。信用评分体系在我们的日常生活中非常常见。例如,共享充电宝可以使用信用评分享受免押金服务,淘宝的信用评分较高则可以享受极速退款服务,而银行的信用评分则可以用来评估是否能够享受大额贷款等。这些行为都需要用信用评分来做背书。

那么信用数据从哪里来呢?其实一切数据皆为信用数据,包括借贷的额度、教育背景、职业收入、邮件、电话号码和住址,甚至是消费习惯、爱好等这些都可以通过大数据收集到,并作为信用数据来评估个人的信用得分。信用评分除了可以享受一些额外的服务之外,还可以作为用户是否具有偿还贷款能力的判断依据。

除了个人信用评分之外,一些大型机构、商铺、产品等也具有信用评分。他们可以根据用户的评价、产品的销量、商铺的口碑等等来生成信用评分,用来作为是否值得信赖(放贷)的依据。

在 Web3 的世界中,金融场景、社交行为以及交易方式都发生了极大的变化。此外,DeFi 也已经重新定义了全球金融行业,它在金融包容性和准入、支付速度和弹性等方面都带来了明显的优势。随着 DeFi 的高度采用,信用评分体系也是其至关重要的一个环节。但是参与 DeFi 的个人资产、交易等数据都被记录在链上,而传统的财务、信用评分和银行评估等数据是在链下。如何实现链上链下数据交互,将现实世界的数据安全传输到区块链,为 DeFi 打造一个全面的信用体系,是现在亟待解决的问题之一。

基于此,诸如 Reputation DAO 的链上信用评分系统也是不断地涌现和发展。

Reputation DAO 是 DeFi 和传统金融之间的一座桥梁,使个人能够在与智能合约交互时利用其真实世界的金融数据和身份。它借助强大的数据流引擎,通过分析链上账户、预言机和 DAO 的特定数据来解锁 DeFi 中更广泛的用例。

它是由澳大利亚区块链平台 Mycelium 推出的,它们的上一个产品是 Tracer DAO,一个部署在 Arbitrum 上的衍生产品生态系统,当前总交易量在 $137,154,334。

Reputation DAO 于近日宣布完成了 475 万美元种子轮融资,由 DACM、AirTree Ventures、 Koji Capital 和 Framework Ventures 等参投。Chainlink 联合创始人 Sergey Nazarov 也加入了 Reputation DAO 担任顾问。

DeFi 贷款仍处于初期阶段

近几年,DeFi 处于野蛮生长阶段,新产品层出不穷,越来越多的投资者和资金涌入 DeFi 市场。随着产品不断地更新和迭代,其产品架构和收益率也日渐成熟和稳定。投资者也不仅局限于流动性挖矿这一个需求,而是涉及到了借贷、算法稳定币、组合型投资等能够获得多样化收入的产品。

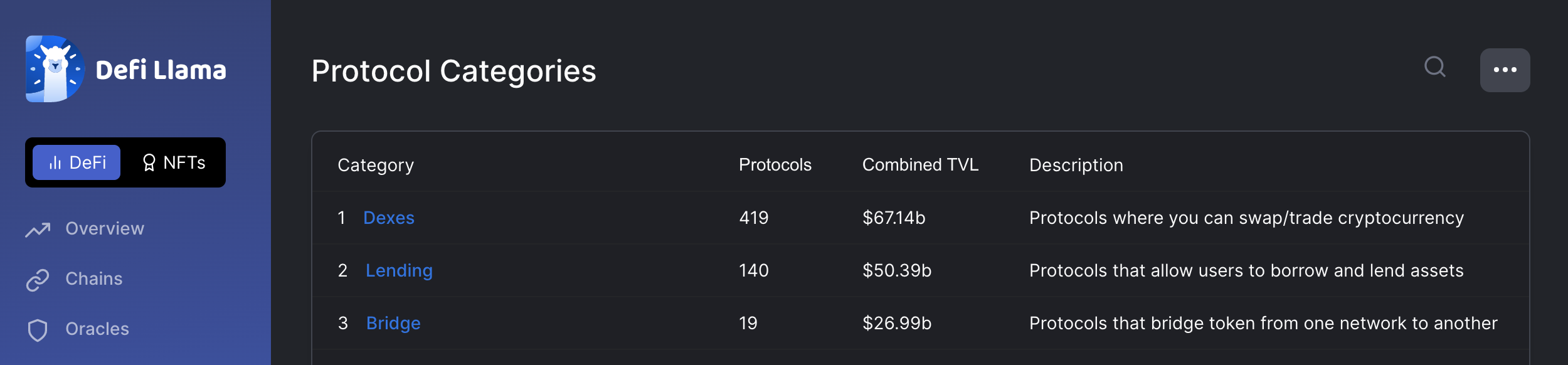

据 DefiLlama 数据 ,截至目前,DeFi 的总锁定价值是 $211B,借贷协议占总 TVL 的 23.69%,共 140 个项目,位列第二。排名第一是去中心化交易所。

与这一成绩对比,DeFi 的借贷市场结构还并未发展成熟。其表现在 DeFi 的数据整合能力还比较弱,缺少信用评分系统,无法广泛延伸信用链条,使得超额抵押贷款现象(及伴随而来的资本效率低下)仍然存在。

Reputation DAO 是一种可验证、去中心化和可编程的 DeFi 信用评分系统,它可以映射链下数据,如 AML/KYC、传统信用评分和社交媒体数据,为 Chainlink 预言机、DAO、智能合约协议及其用户提供可信的中立信用服务,以增强对特定账户风险指标的评估,并减少抵押贷款流程,让无抵押贷款成为可能。

Reputation DAO 如何工作?

具体来说,Reputation DAO 将通过以下几种方式来收集和分析信用数据。

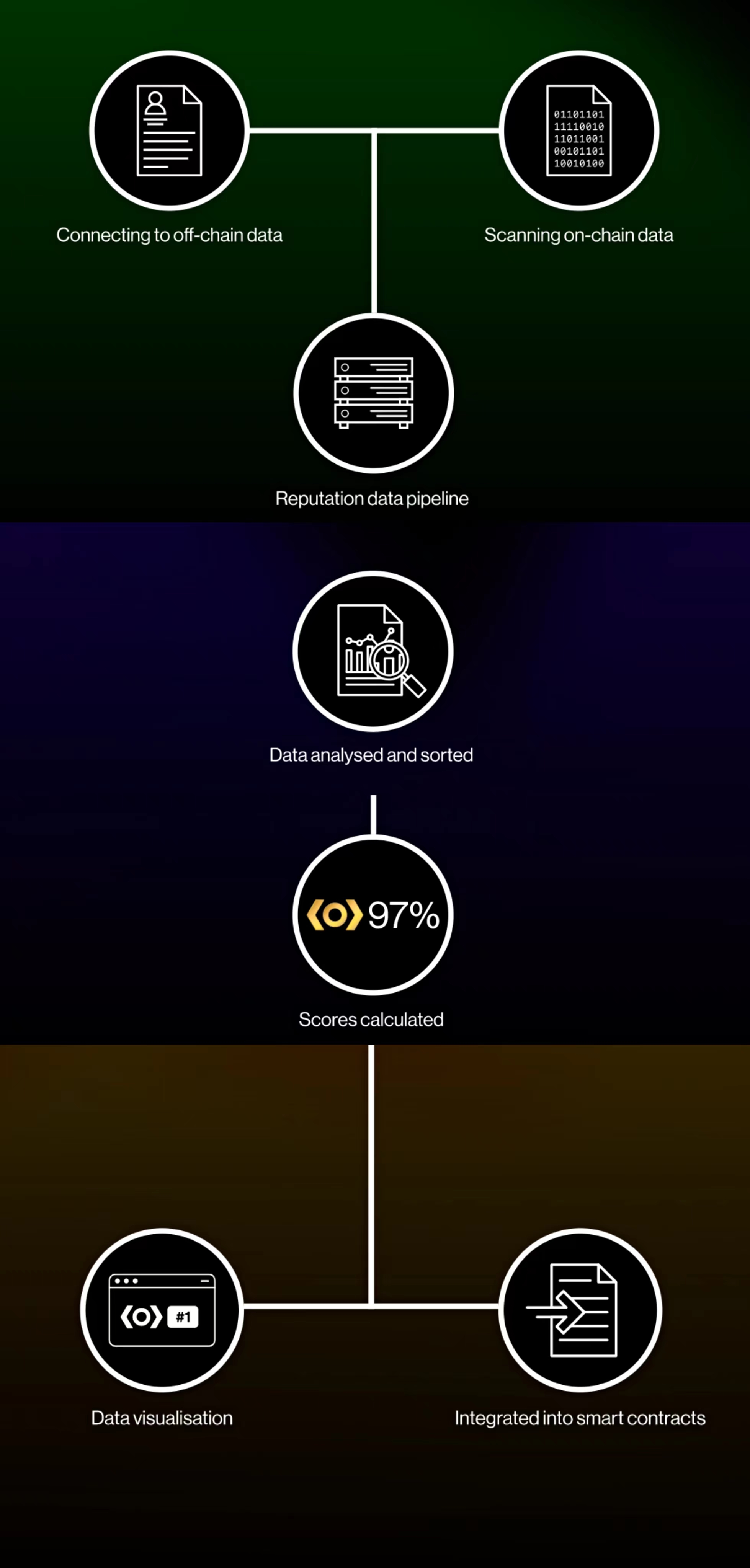

1. 扫描并连接

使用 Reputation DAO,DeFi 用户可以扫描并检查其智能合约中底层预言机数据的安全性。通过构建数据聚合管道,可以快速的传输任何基于 EVM 的数据。借助信用链接,用户可以了解预言机的性能以及对特定数据馈送的洞察。Reputation DAO 专注于扫描个人 DeFi 账户、预言机和 DAO 的数据。

之后,再使用由 Chainlink 提供支持的去中心化预言机网络,来连接所需的相关链下信用服务,例如身份服务、相关 AML/KYC 检查、FICO/Vantage 分数和相关社交媒体数据。

2. 分析和计算

获得数据之后,Reputation DAO 将对与个人账户、预言机和 DAO 相关的扫描数据进行分析和排序。Reputation DAO 开发了 RepScores,这是一种使用链上数据源的声誉评分算法。将 RepScores 集成到合同中,能够降低个人在 DeFi 中的抵押品要求。

3. 可视化

分析后的数据会被可视化,以便用户可以使用并了解自己或他人的链上交互信息。账户、预言机和 DAO 将能够查看和检查他们在链上的交易历史,同时评估相关的信用指标。信用数据可通过免费 API 公开访问。

Reputation DAO 的第一个产品——Oracle Reputation

Reputation DAO 将将创建不同的平台和应用程序以获得服务于开放区块链生态系统的信用。第一个产品是 Oracle Reputation。Oracle Reputation 将有关 Oracle 质量的链上信息转换为知识,人类(和机器)可以使用它来做出决策。Oracle Reputation 使用 Repscore 模型,通过协调和聚合信用指标,将人类可读和可编程的知识附加到 Web3 中。

目前,在 Oracle Reputation 上可以查看预言机、合约和集成协议的数据分析。

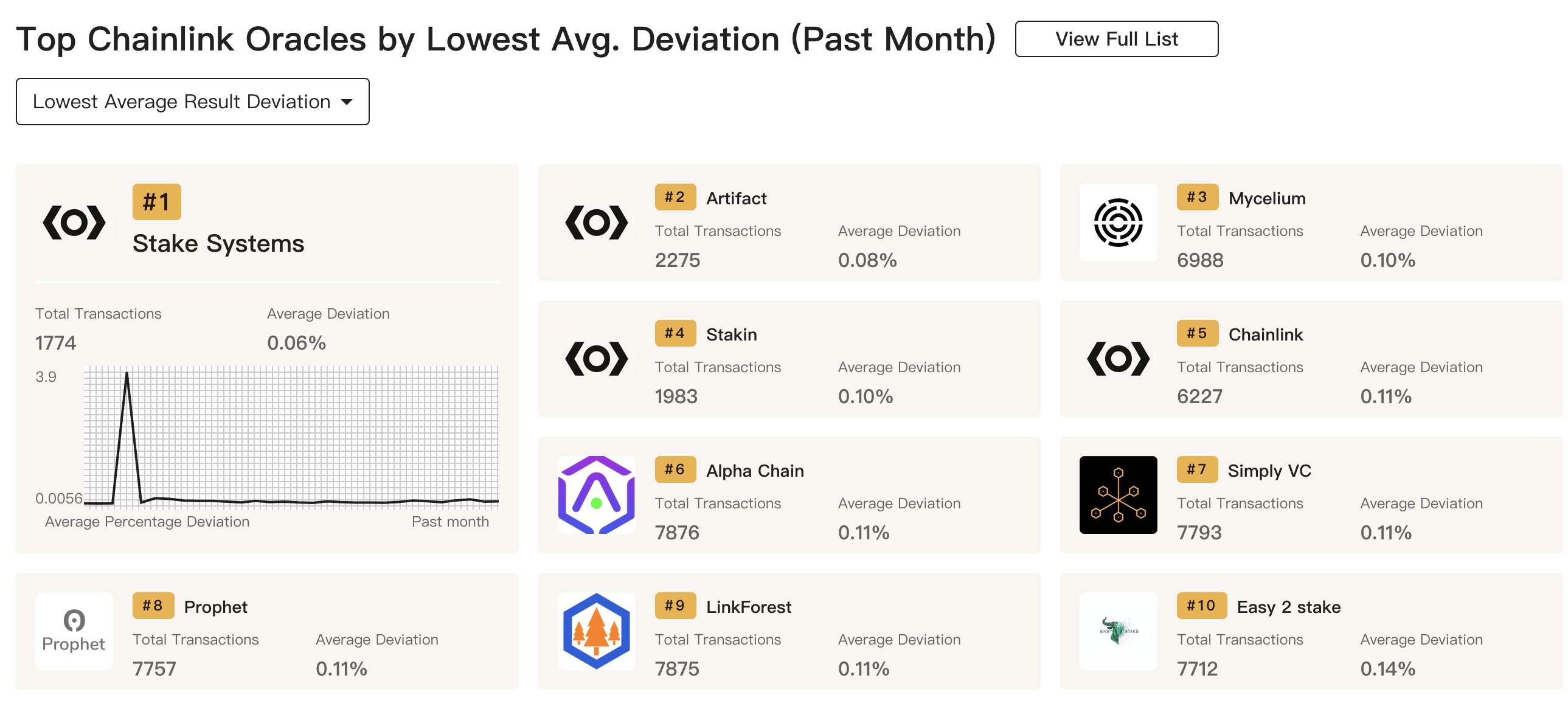

1. 预言机

比如 Oracle Reputation 根据平均偏差或提交的总交易量对预言机进行排名。这些排名就可以让用户一目了然地了解 Oracle 的可靠性。

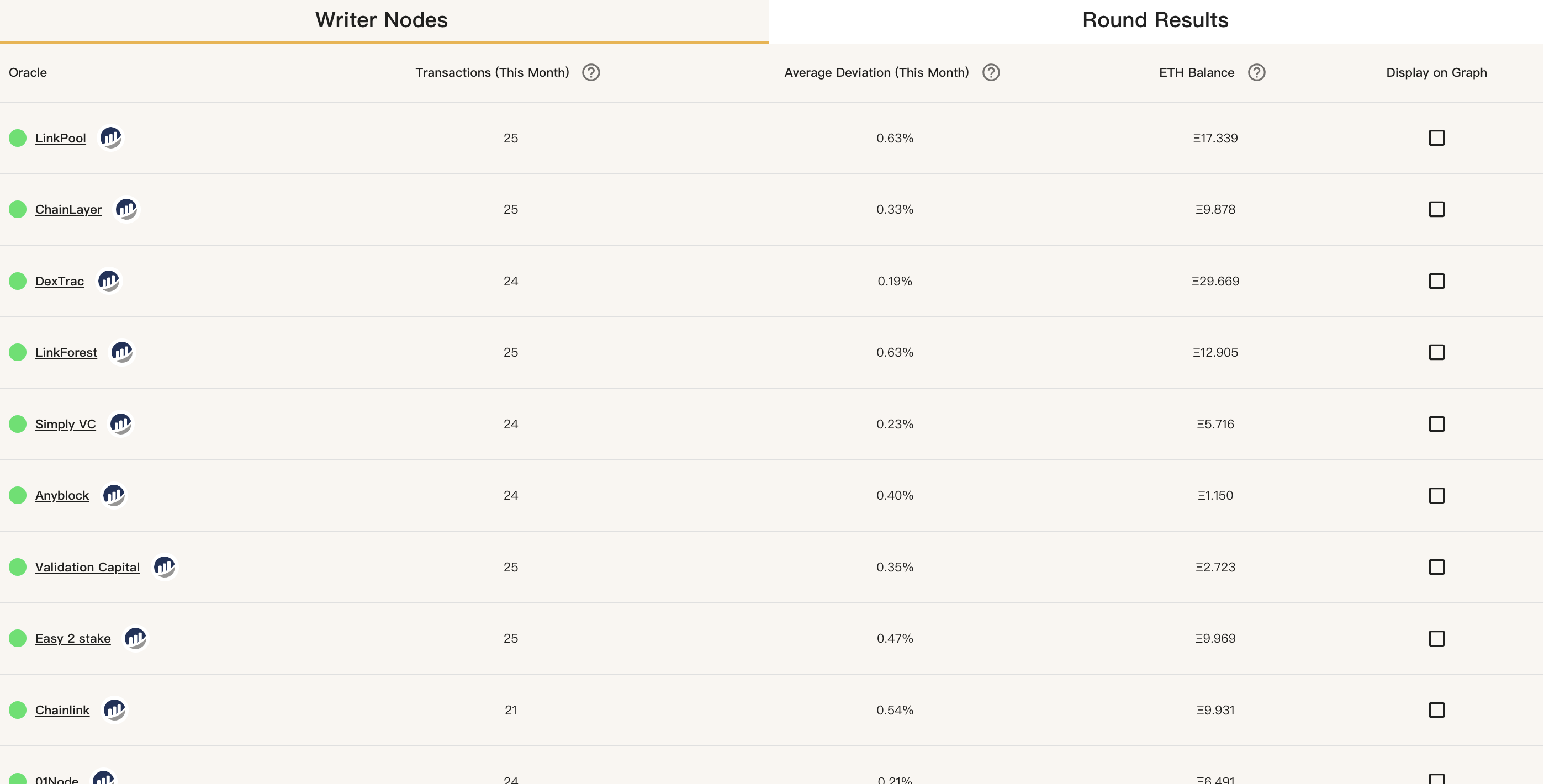

2. 合约

可以查看预言机合约在链上提交的时间、该预言机的数据与真实数据之间的偏差以及预言机地址持有ETH的数量等。

3. 协议

Oracle Reputation V2 平台更新了一项新功能——协议可视化环境(PVE),PVE 可用于与 Reputation DAO 集成的 DeFi 协议。它是一个小部件,显示在协议前端。当用户单击小部件时,它会将他们定向到该协议在 Oracle Reputation 的数据仪表盘,在那里你可以查看与该协议相关的数据。

目前,Oracle Reputation 已经集成了Aave 、Tracer DAO、Arbitrum 和 DeFi Safety。用户可以根据需求查看特定协议的预言机的数据安全性。

例如,它为 Aave 提供了以下数据:

Aave 合约从 Chainlink 中读取的价格和时间,以及单个预言机和预言机网络的价格更新。

每日和每小时 TVL、预期的 gas 和支付的 gas,以及借款的规模和数量。

Chainlink 在其平台上使用的所有数据源的概述,包括最近交易的日志。

Reputation Widget 显示每个 Aave 合约的端到端数据供应链。Aave 用户能够更清楚的了解预言机和 Chainlink 合约是如何与 Aave 协议上的智能合约进行交互的。

让用户更容易进行尽职调查,使用户在 Aave 网络上进行交易时可以安心。这有助于让用户建立对协议的信任。

Reputation DAO 未来发展路线

Reputation DAO 正在开发:

1.Repscore——预言机信用评分模型

Repscores 使用开源相对性能排名 (RPR) 的模型来评估每个预言机的性能并生成从 1 到 100 的“信用分数”。该模型将为全面评估和衡量预言机性能提供一个标准架构。

2.预言机的监控和警报

2.预言机的监控和警报

此功能能够在预言机出现故障时立即通知。用户将能够选择在哪些情况下通知他们以及他们如何接收通知。

资方 DACM 联合创始人兼首席执行官 Richard Galvin 表示:“信用评分是传统金融系统中银行和外部提供商的一项关键功能。迄今为止,对于借款人和贷方而言,这种清晰性还不是 DeFi 的功能。随着生态系统的成熟和独立、可靠信息 DAO 的兴起,我们认为 Reputation DAO 是该行业下一个增长阶段的基础设施。”

确实,DeFi 和传统金融之间的互操作性能够提供数万亿美元资本和数十亿用户流量,信用体系在其中是不可或缺的一部分。Reputation DAO 为这些数据流入智能合约提供了渠道,以及更高的安全性、利率和保证。