누가 팔고, 누가 버티고, 누가 계속 사고 있는가? 미국 자본의 암호화폐 ETF 포지션 분화

- 핵심 견해: 2026년 1분기, 주요 기관들은 암호화폐 ETF 하락장 속에서 차별화된 전략을 보였습니다. 하버드 등 대학 기금은 적극적으로 비중을 줄여 AI로 전환했고, 골드만삭스 등 투자은행은 암호화폐 ETF 리스크를 축소하고 선별된 개별 주식으로 방향을 틀었으며, 아부다비 국부펀드와 JP모건은 오히려 지분을 늘리며 기관들이 암호화폐 자산에 대해 더 정교한 위험 순위를 매기고 있음을 보여줍니다.

- 핵심 요소:

- 하버드 대학 기금은 IBIT 보유분을 43% 줄이고 이더리움 ETF를 완전히 청산했으며, 동시에 AI 및 컴퓨팅 파워 관련 주식 비중을 늘려 '암호화폐 축소, AI 확대'라는 구조적 리밸런싱 전략을 보여줍니다.

- 골드만삭스는 2026년 1분기에 비트코인 및 이더리움 ETF를 대폭 축소하고 모든 XRP 및 Solana 관련 ETF를 청산한 반면, Circle(+249%) 및 Coinbase(+65%) 지분은 늘려 ETF 리스크에서 선별된 개별 주식으로의 내부 순환을 보여줍니다.

- 아부다비 국부펀드 무바달라는 IBIT 보유분을 약 15.9% 늘렸으며, 가격 하락으로 시가총액이 6억 3100만 달러에서 5억 6600만 달러로 줄었음에도 불구하고, 국부 자금의 장기적인 투자 인내심을 보여줍니다.

- JP모건은 IBIT 보유분을 174% 늘려 약 830만 주로 만들고 이더리움 ETF 익스포저도 확대하여, 대형 은행으로서 상품 라인업을 확장하고 고객 포트폴리오 수요를 충족시키는 전략을 반영합니다.

- 미국 대학 기금(브라운, 다트머스)은 관망하거나 온건하게 조정하는 선택을 했습니다. 예를 들어 다트머스 대학은 비트코인 베이스 포지션을 유지하고 이더리움 상품을 스테이킹 기능이 있는 ETF로 전환하여 장기적인 투자 규율을 보여줍니다.

Original Author: KarenZ, Foresight News

The most noteworthy aspect of the first quarter is not how much prices fell, but how institutions navigated this drawdown.

Looking solely at market trends, crypto ETFs didn't have an easy time in Q1 2026. Bitcoin and Ethereum faced pressure during the quarter, and the book value of spot ETFs generally declined. Even if many positions weren't sold, their performance at the end of the quarter didn't look impressive. However, the truly interesting part of a downturn is never the net value curve itself, but the different actions various institutions took on the same drawdown chart.

As of the latest round of 13F filings disclosed in mid-May 2026, the market can now see the quarter-end holdings of a group of institutions as of March 31, 2026. University endowments, large investment banks, sovereign wealth funds, market makers, and wealth management firms have provided several distinctly different answers.

Some Reduced Positions: Risk Contraction First

Let's first look at the sellers.

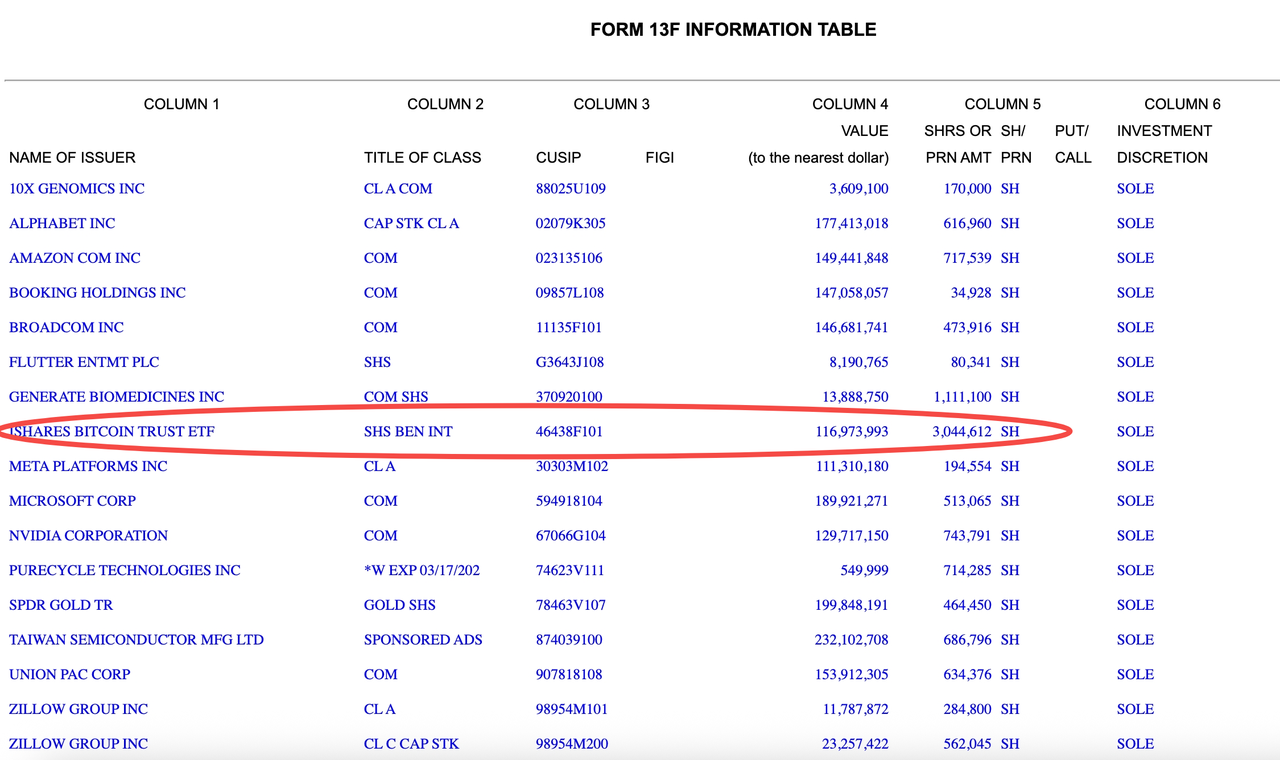

Harvard Management, which manages the Harvard University endowment and related financial assets, is one of the most typical examples from this round. According to its 13F filing, its IBIT (iShares Bitcoin Trust ETF) holdings decreased from 5,353,612 shares at the end of Q4 2025 to 3,044,612 shares at the end of Q1 2026, a reduction of about 43%. The corresponding book value also dropped from approximately $266 million to around $117 million. Meanwhile, its holdings in ETHA (iShares Ethereum Trust), which it still held in the previous quarter, were completely exited this quarter. This indicates that Harvard wasn't just responding to price declines but was actively compressing its public exposure to spot Bitcoin and Ethereum ETFs.

This change in holdings has another implication. Harvard didn't shift entirely to a defensive posture. Instead, it reallocated a portion of its positions to assets related to the AI and computing power chain, increasing its holdings in stocks like NVIDIA, Broadcom, and TSMC. Viewed together, these actions are closer to a structural rebalancing of "reducing crypto, adding AI," rather than a comprehensive risk contraction.

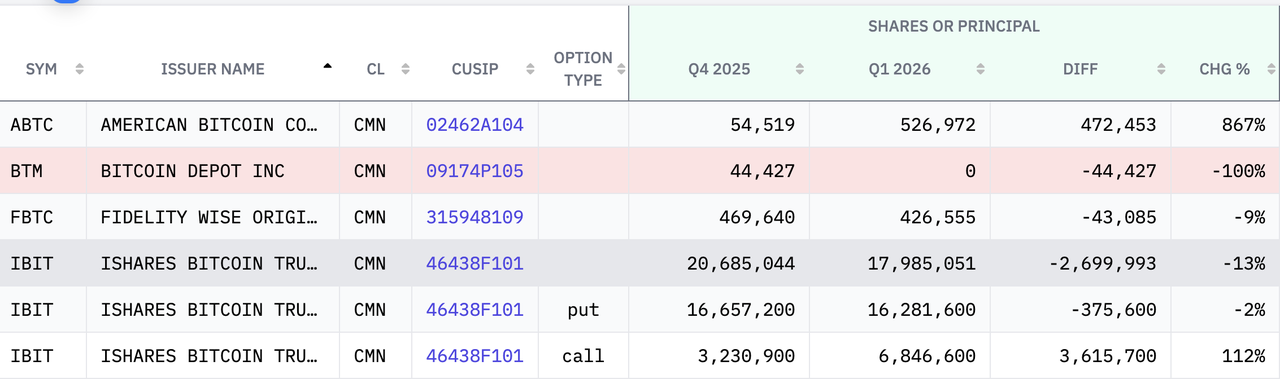

Goldman Sachs adopted a broadly similar strategy, but with more complex tactics. Comparing the last two 13F filings, Goldman Sachs held approximately $690 million in IBIT and about $25.18 million in FBTC (Fidelity Wise Origin Bitcoin Fund) at the end of Q1 2026, both down from the previous quarter. More noteworthy than the simple position reduction is its position structure: Goldman Sachs holds spot, call options, and put options on IBIT, indicating this isn't just a directional bet but has a clear trading and hedging component.

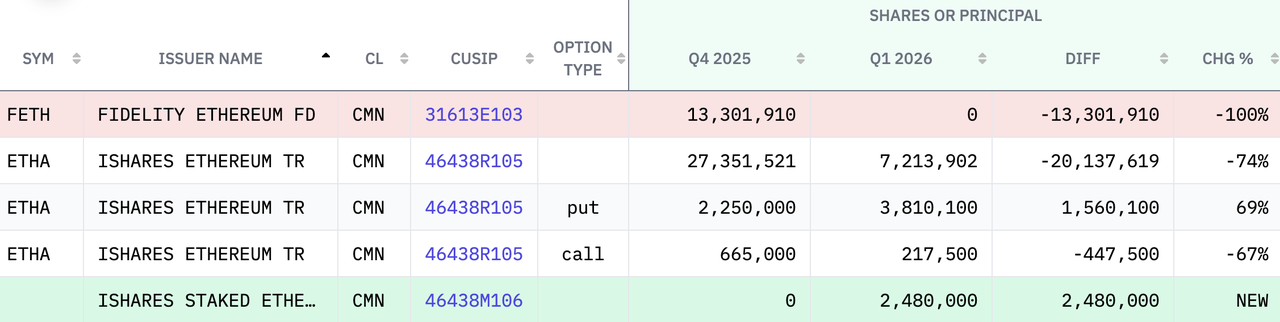

Goldman Sachs was more aggressive with Ethereum. It not only liquidated its holdings in the Fidelity Ethereum Fund (valued at $394 million at the end of Q4 2025) but also significantly cut its spot position in the iShares Ethereum Trust (ETHA) by approximately 74%, leaving a remaining position of about $114 million. Additionally, it newly held $66.885 million in the iShares Staked Ethereum Trust ETF.

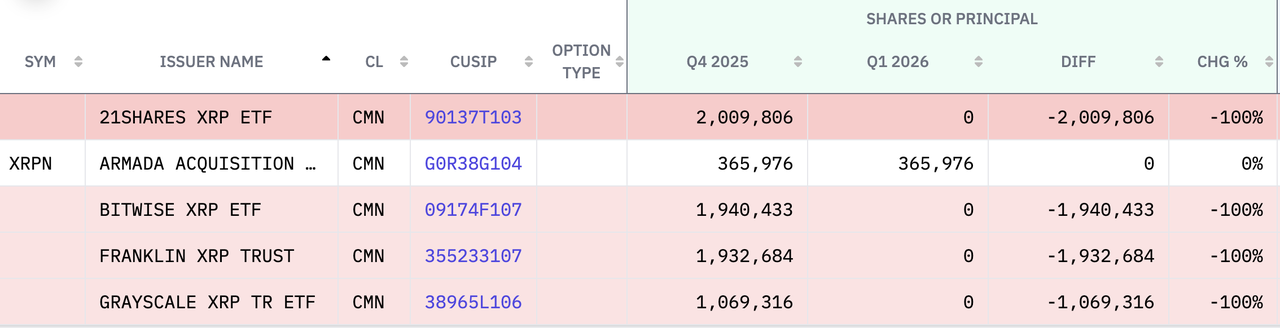

Concurrently, Goldman Sachs liquidated all its XRP and Solana-related ETFs. As of the end of Q4 2025, it held a total of approximately $152 million in XRP ETFs from Bitwise, Franklin Templeton, Grayscale, and 21shares. It also cleared all its Solana ETFs/Trusts from Grayscale, Bitwise, and Fidelity (valued at $109 million at the end of Q4 2025).

Regarding crypto stocks, Goldman Sachs increased its position in Circle by 249% to around $140 million, and its position in Galaxy Digital also increased by 205% (reaching $41.48 million). Holdings in Coinbase (+65%), Robinhood (+35%), and PayPal also increased. During the same period, it reduced holdings in Strategy and Riot Platforms. Overall, this looks more like an internal rotation of "compressing ETF risk, shifting to selected stocks."

Among hedge funds, Millennium Management also signaled similarly. Publicly compiled data shows its IBIT holdings dropped from 34.334 million shares to 19.287 million shares, a decrease of about 43.8%. ETHA holdings also decreased simultaneously (down about 34.3%), indicating a significant reduction in spot Bitcoin and Ethereum ETF positions.

Capula Management Ltd, a hedge fund management firm headquartered in London, UK, went even further. As of December 30, 2025, it held $470 million in IBIT, $160 million in FBTC, $207 million in ETHA, and $61.43 million in FETH. However, the latest 13F filing shows these ETFs have been completely liquidated. Simultaneously, Capula Management Ltd has fully liquidated its Coinbase position (while retaining a small options position).

Holding Steady: An Attitude in Itself

The second category consists of those who held their positions steady.

Brown University's IBIT holdings remained at 212,500 shares, with no increase or decrease. Based on disclosure values, this position dropped from approximately $10.551 million at the end of 2025 to about $8.164 million at the end of Q1 2026. This type of university endowment doesn't convert quarterly price fluctuations directly into trading instructions, instead emphasizing portfolio discipline and long-term allocation pacing.

Dartmouth College's handling of crypto assets in Q1 2026 looks more like a moderate expansion than aggressive rotation. Comparing its filings with the previous quarter, the college retained its existing Bitcoin ETF core holdings, with the IBIT share count essentially unchanged. However, due to the price decline in the first quarter, the book value dropped from over $10 million to about $7.7 million. For its Ethereum exposure, it executed a product switch, swapping its Grayscale Ethereum Mini Trust for the staking-oriented Grayscale Ethereum Staking ETF, holding approximately 178,100 shares. It also established a new position in the Bitwise Solana Staking ETF, about 304,803 shares, with a book value of approximately $3.3 million.

Another Approach: Buying More as Prices Fall

The third category includes those who increased their positions against the trend.

Abu Dhabi sovereign wealth fund Mubadala is one of the most prominent names. Its IBIT holdings increased from 12,702,323 shares to 14,721,917 shares, a gain of about 15.9%. However, despite the increase in share count, the position's market value at the end of the quarter still fell from approximately $631 million to about $566 million. This set of numbers is quite telling. The act of adding positions doesn't automatically lead to profitability, especially when the market is still in a drawdown channel. Increasing allocation first leads to greater exposure, and only potentially to higher future upside.

JPMorgan's actions can also be understood within this logic. According to the latest 13F data, JPMorgan increased its IBIT holdings from about 3.028 million shares to approximately 8.3 million shares, a 174% increase, while also adding some exposure to FBTC, BITB, and Ethereum ETFs. Looking at the change in share count, it's clearly more aggressive. However, this doesn't necessarily mean it has locked in excess returns in this volatile period. For large banks, increasing ETF positions often involves expanding their product shelf, meeting client allocation needs, and balancing liquidity and book risk, rather than being simply a directional bullish bet.

Wells Fargo's position changes are also worth noting. Comparing the latest filings, this bank retained its core IBIT position while increasing allocations to products like BITB and the Grayscale Bitcoin Mini Trust. More notably, it significantly increased allocations to Ethereum ETFs, with ETHA holdings rising from approximately 672,600 shares to about 1.1 million shares, and ETHW holdings also increasing simultaneously. In other words, Wells Fargo adopted a strategy of "maintaining the Bitcoin core position while raising the weight of Ethereum."

Market maker Jane Street demonstrated another typical style. Comparing the two 13F filings, it significantly reduced exposure to spot Bitcoin ETFs in Q1, with IBIT holdings dropping from about 20.3 million to roughly 5.9 million shares, and FBTC also declining markedly. However, simultaneously, it added approximately $82 million in Ethereum ETF exposure. On the crypto stock side, Jane Street increased holdings in Galaxy Digital (8746%), Circle (1162%), Coinbase (+14%), and BitMine (+47%). This combination looks more like a typical trading rebalance: reducing Bitcoin ETFs, adding Ethereum ETFs, while seeking higher upside in selected individual stocks.

Bitcoin, Ethereum, and Solana: Institutions are Making More Detailed Risk Rankings

This round of 13F filings also reveals another noteworthy signal: Institutional attitudes towards BTC ETFs, ETH ETFs, and even Solana ETFs are no longer uniform. The more critical question now is which crypto assets institutions plan to keep in their core holdings, which to place in tactical growth holdings, and which to simply remove first.

Take Harvard Management as an example. While reducing IBIT, it completely exited ETHA. This looks like a risk ranking. The Bitcoin ETF retained a relatively core position, while the Ethereum ETF was prioritized for cutting during the portfolio rebalancing.

Goldman Sachs' approach also shows that large financial institutions are refining this ranking. It maintained a relatively large Bitcoin ETF exposure in Q1 but reduced its Ethereum-related products much faster, while essentially clearing out XRP and Solana-related ETFs. Viewed together, Goldman Sachs is re-concentrating its positions into the layer of assets it considers most liquid, easiest to hedge, and most readily incorporated into institutional risk models. Bitcoin here acts as the "core position," Ethereum is a compressible position, while products like Solana and XRP are closer to marginal experimental holdings. Once market volatility amplifies, these are often the first to be cut.

On the other hand, Wells Fargo and Dartmouth College present completely different answers. Wells Fargo proactively increased its weight in Ethereum ETFs, suggesting that within its internal framework, Ethereum looks more like a secondary position worth increasing allocation to during a drawdown to gain upside. Dartmouth College's strategy is perhaps more representative: It didn't touch its Bitcoin ETF core but extended its new tactical exposure to Solana-related ETFs, especially those with staking features.

The 13F Offers a Snapshot of the Market, but Also Leaves Blanks

This is also where the most caution is needed when analyzing institutional holdings.

The 13F allows outsiders to see, on a uniform basis, how mainstream institutions are allocating to crypto ETFs. However, it has very clear limitations. Firstly, it has a time lag. What investors see in May is merely the snapshot of institutional holdings as of March 31st. If significant portfolio adjustments were made in Q2, the filings wouldn't show it. Secondly, the 13F only displays holdings, not the actual cost basis. A decline in an institution's reported position value over a quarter doesn't necessarily mean it's in an overall loss, as it could have purchased at lower prices or executed intra-quarter reductions and re-additions.

Furthermore, for institutions like Goldman Sachs, positions beyond spot ETFs are often supplemented with options, hedges, and market-making-related holdings. Looking solely at the filing table can easily lead to misinterpreting trading activities as long-term strategic stances.

Yet, precisely because of its incompleteness, the 13F acts more as a window into institutional sentiment than a conclusion sheet. Seeing the Abu Dhabi sovereign wealth fund Mubadala increase its position while its book value falls reveals sovereign patience. Seeing Brown University stay put and withstand the drawdown shows long-term allocation discipline. Seeing Harvard University reduce Bitcoin and exit Ethereum ETFs reveals the real sensitivity of university endowments to volatility. And seeing JPMorgan, Wells Fargo, and Jane Street continue adjusting their exposure across different products shows that Wall Street still views crypto ETFs as a category that needs to be kept on the shelf and constantly re-priced.