세계는 새로운 인플레이션에 대응하며 '장기 국채 폭풍'이 전 세계를 휩쓸고 있다

- 핵심 시각: 중동 전쟁이 유가와 인플레이션 기대를 끌어올리면서 미국 장기 국채 수익률이 2007년 이후 최고치로 급등했고, 이는 글로벌 채권 시장 매도를 촉발했다. 시장은 연방준비제도(Fed)가 금리를 인하하기보다 인상할 것으로 예상하며, 금리가 장기간 높은 수준을 유지하는 새로운 시대가 시작되었을 수 있다.

- 핵심 요소:

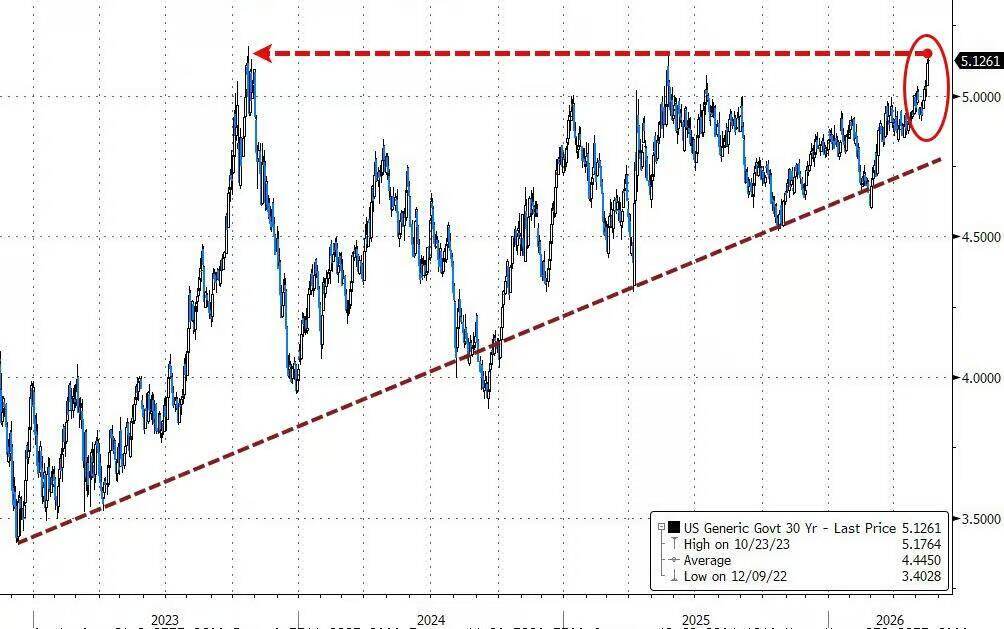

- 미국 30년물 국채 수익률이 5%를 돌파하며 16년 만에 최고치를 기록했다. 30년물 입찰 수요는 부진했으며, 이는 투자자들이 고점에서도 여전히 매수 의향이 부족함을 보여준다.

- 트레이더들은 내년 3월 금리 인상을 유력한 시나리오로 보고 있으며, 이는 2월 말 시장이 예상했던 2026년 금리 인하와 근본적으로 반대되는 전망이다. 인플레이션 내러티브가 시장 가격 결정을 주도하고 있다.

- 호르무즈 해협 봉쇄가 지속되면서 유가와 인플레이션 기대가 상승하며 채권 시장 변동성의 핵심 동력이 되고 있다. 이 교착 상태가 해소되지 않는 한 채권 시장의 압력은 가라앉기 어렵다.

- 시장은 다음 소비자물가지수(CPI) 보고서가 2023년 이후 최고 수준인 연간 인플레이션율 4%를 기록할 것을 우려하고 있으며, 미국 재정 적자 확대는 기간 프리미엄에 대한 보상 요구를 더욱 강화하고 있다.

- JP모건의 미국 국채 투자자 조사에 따르면 공매도 포지션이 13주 만에 최고치를 기록했으며, 시장은 채권 시장의 추가 하락에 베팅하고 있다. 일부 투자자는 관망세를 유지하고 있다.

Original author: Zhao Ying

Original source: Wall Street CN

The global bond market is at a historic turning point. Surging oil prices driven by the conflict in the Middle East and rising inflation expectations are pushing U.S. Treasury yields to two-decade highs, triggering a cascading sell-off in major markets like the UK and Japan. A new era of persistently high interest rates may have quietly begun.

The U.S. 30-year Treasury yield has breached the 5% mark, hitting its highest level since 2007. Demand at last week's 30-year bond auction was tepid, failing to spark buying interest even at these elevated levels. Meanwhile, market expectations for the Federal Reserve's policy path have undergone a fundamental reversal. Traders now see a rate hike next March as a high-probability event, with roughly a three-in-four chance of a hike by December. This contrasts sharply with expectations in late February this year, when the market anticipated two rate cuts by 2026.

This bond market turmoil is weighing on equities and has drawn significant attention from G7 finance ministers, who will dedicate a portion of their meeting this week to discussing the sell-off. Priya Misra, Portfolio Manager at J.P. Morgan Asset Management, warns, "The synchronized rise in long-end rates globally tends to be self-reinforcing, and expectations of a Fed rate hike are also entering the market narrative."

The Iran Conflict Flips the Bond Market Narrative

The blockade of the Strait of Hormuz is the core driver of the current bond market turbulence. This disruption to the world's most critical oil shipping channel is continuously pushing oil prices higher and rekindling inflation expectations.

Investors broadly believe that as long as the standoff in the Middle East persists, pressure on the bond market will be difficult to dissipate. Priya Misra stated bluntly, "Unless the strait reopens, the entire interest rate range has shifted upwards."

Data shows that U.S. Treasury yields are now roughly 50 basis points or more above levels seen in late February. The 2-year yield briefly rose to 4.09%, its highest since February 2025; the 10-year yield was 4.58%, near a one-year high. U.S. Treasuries have posted negative returns year-to-date, after gaining nearly 2% in the period up to late February.

Inflation Narrative Dominates Market Pricing

The market's core concern is the re-anchoring of inflation expectations. Karen Manna, fixed income strategist and portfolio manager at Federated Hermes, stated, "We are witnessing a world that is truly grappling with a new wave of inflation."

Kevin Flanagan, Head of Investment Strategy at WisdomTree, expects the next Consumer Price Index report could show an annual inflation rate of 4%, which would be the highest since 2023 – the April CPI came in at 3.8%. He notes, "The inflation narrative is dominating the market, and the bond market demands a higher premium to compensate for holding newly issued government debt."

Concerns over the burgeoning U.S. fiscal deficit, coupled with signs of economic resilience despite wartime headwinds, further reinforce the logic for investors demanding higher term premiums. Last week's Treasury auctions reflected this: the 30-year bond auction rate was 5%, the highest since 2007, but demand was lackluster; demand from investors for the 3-year and 10-year auctions was also tepid.

Rate Hike Expectations Reshape the Fed's Outlook

This inflation storm also puts immense pressure on the incoming Fed Chair Kevin Warsh, dashing market bets on rapid rate cuts after he assumes office.

Chicago Fed President Austan Goolsbee stated last week that broad price pressures might even signal an overheating economy; Fed Governor Michael Barr called inflation the "overwhelming" risk facing the economy. This Wednesday, the minutes from the Fed's April meeting will be released, and the market will be closely watching the level of support the dissenting committee members received.

In the latest J.P. Morgan U.S. Treasury Investor Survey, bearish positioning on Treasuries reached its highest level in 13 weeks, indicating a clear increase in market bets on further declines in the bond market.

Investors Wait and See, Looking for More Signals

Faced with sustained selling pressure, some investors are choosing to hold steady. Kevin Flanagan stated his stance is to hold floating rate notes and maintain lower duration exposure, preferring to "be late rather than early." He believes the 4.5% level for the 10-year yield is "more psychological," and if tensions in the Middle East escalate further, pushing oil prices higher, yields could retest last year's high of 4.62%.

Hank Smith, Head of Investment Strategy at Haverford Trust, takes a more cautious approach. He stated that whether the rise in consumer and producer prices is temporary "or will persist into 2027" remains an open question, requiring more data to determine the direction of the bond market.